Investment markets and key developments

Shares had another rough ride over the last week as higher than expected US inflation saw expectations for Fed rate cuts pushed out further, and reports of imminent strikes by Iran on Israel in retaliation for an attack in Syria pushed US shares down sharply on Friday not helped by a fall in some bank shares. For the week US shares fell 1.6% and Eurozone shares fell 0.9%. Chinese shares fell 2.6% but Japanese shares rose 1.4%. Despite the messy global lead and the local money market pushing RBA rate cuts out to later this year or early next year the Australian share market managed a modest gain of 0.2% for the week with gains in materials on the back of a rise in the iron ore price and utilities offsetting falls in property, consumer and IT stocks. Bond yields rose in the US, UK and Australia but fell in Europe. While oil prices dipped slightly despite fears about an escalation in the war around Israel to directly include Iran, the copper price rose to new cyclical high and iron ore prices also rose. The $A fell as the $US rose.

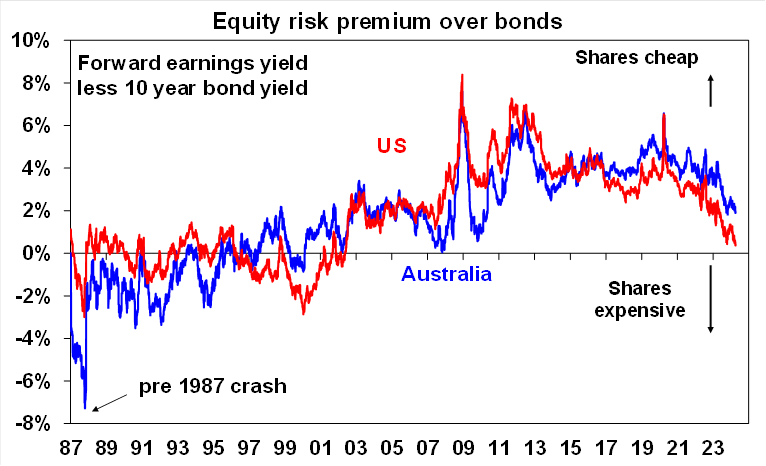

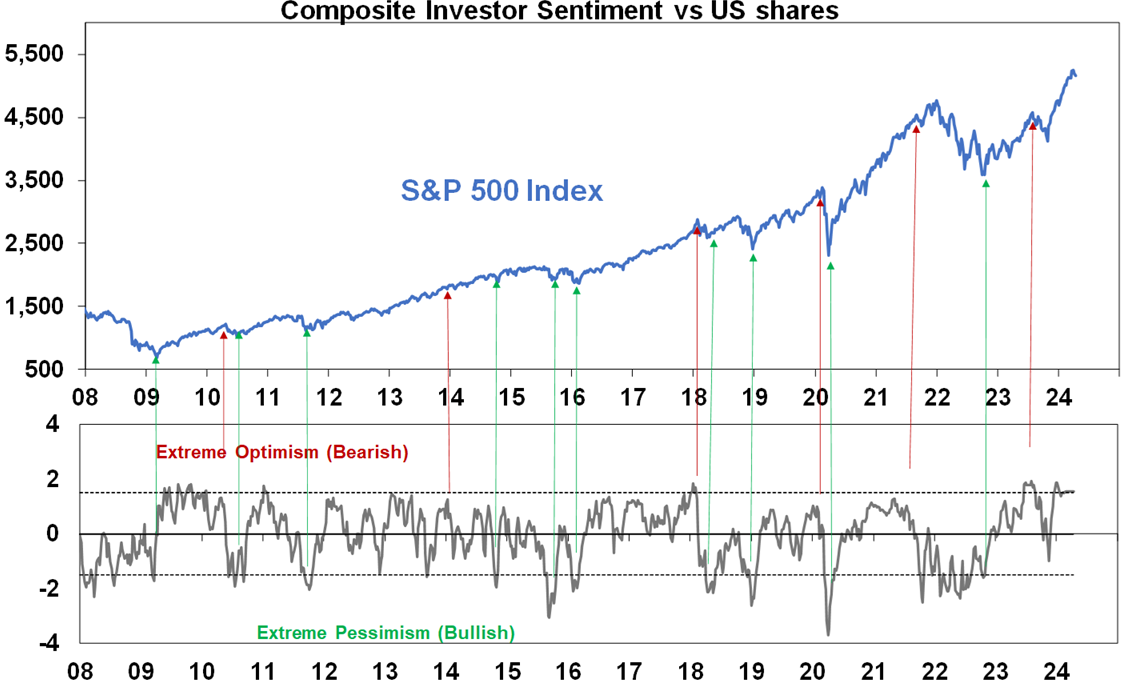

Despite the volatility over the last two weeks, we continue to see further gains in shares this year as inflation slows, central banks still cut interest rates and recession is avoided or proves mild. But shares remain vulnerable to more volatility and a possible correction as valuations are stretched particularly with higher bond yields (first chart below), investor sentiment is too bullish (second chart below), uncertainty remains high regarding the timing of rate cuts, recession risks remain high and there are multiple geopolitical threats (particularly around the war in the Middle East and the US election).

Source: Bloomberg, AMP

Source: Bloomberg, AMP

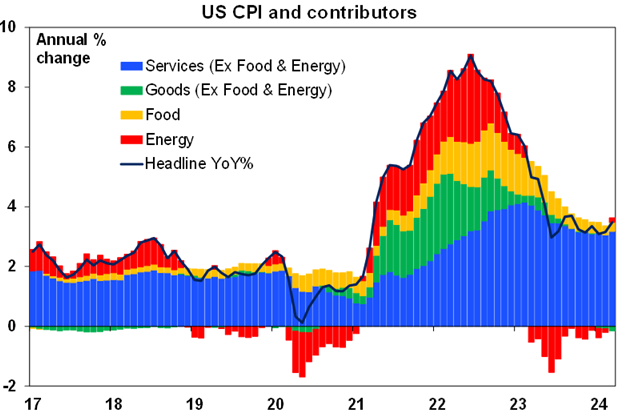

Hot US inflation for the third month in a row. US inflation came in at 0.4%mom in March for both headline and core which was yet again above market expectations for 0.3%mom, with key drivers of the upside surprise being rents and transport services.

Source: Bloomberg, AMP

Three hot US CPI’s in a row are a concern because it suggests a possible trend. To quote Goldfinger’s comment to James Bond: “once is happenstance, twice is coincidence, the third it’s energy action”. The good news is that producer price inflation came in less than expected at 0.2%mom, March core PCE inflation (which the Fed targets) looks like it will come in lower at 0.26%mom and asking rents still point to a slowing in CPI rents. But the three higher than expected CPI readings in a row and the renewed upswing in services inflation will be a concern for the Fed at a time when strong economic data means its in no hurry to cut. Fed speakers including Powell are likely to continue to highlight this caution. As such, in the absence of much lower inflation and jobs data releases ahead, a June Fed cut is now unlikely. July is possible but we now expect the first Fed cut to come in September. This runs the risk of being seen as political though given that the presidential election is in November, further raising Trump’s dislike for Powell.

Source: Bloomberg, AMP

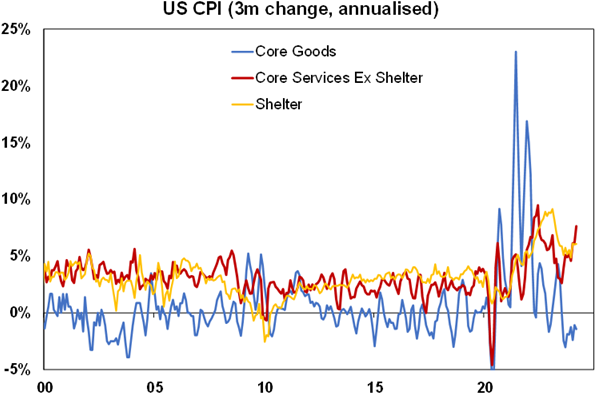

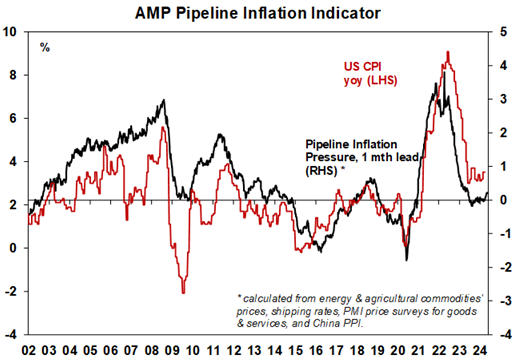

Our US Pipeline Inflation Indicator has edged up but is still averaging around a level consistent with 2% inflation. So, while inflation has surprised on the upside so far this year, we continue to see it resuming its downswing as wages growth continues to slow, allowing the Fed to start cutting rates in the second half. Expectations for Fed interest rate cuts have swung from extreme optimism earlier this year (with seven cuts priced in) to extreme pessimism now (with less than two rate cuts priced) and are likely at some point to start swinging back the other way.

Source: Bloomberg, AMP

While the Fed may be delaying rate cuts, the Bank of Canada is getting closer to them. As expected, the BoC left rates on hold at 5%, but noted that inflation has been falling and BoC Governor Macklem said a June cut is possible. The money market has a 65% probability of a 0.25% cut in June and a cut fully priced in for July.

Similarly, the ECB signalled its on track for a June cut noting that inflation has continued to fall, wages growth is moderating, incoming data has broadly confirmed the outlook and if it continues to gain confidence that inflation is converging on its target then it will be appropriate to cut. The money market continues to price the first ECB rate cut to start in June. Note that the dovishness from the BoC and ECB both came after the hot March CPI release in the US and highlights central banks will diverge from the Fed providing its supported by their own inflation data. And on this front both Canada and the Eurozone have been seeing lower than expected inflation in contrast to the US and both have been seeing weaker economic growth. While economic growth is running at 3.1%yoy in the US, its 0.9%yoy in Canada and only 0.1%yoy in the Eurozone.

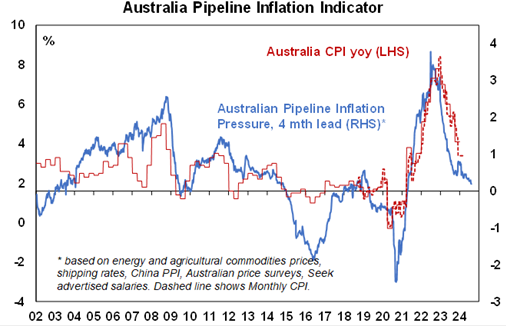

Hotter US inflation delaying Fed rate cuts adds to the risk of RBA cuts taking longer too, but ultimately local inflation will determine what the RBA does and the money market reaction pushing rate cuts off into December or February 2025 looks overdone. The message globally is not all in alignment with the US with both Canada and Europe heading towards rate cuts around mid-year, which will likely be ahead of the Fed, so central banks don’t have to follow the Fed and this also applies to the RBA. Like Canada and Europe, Australia also has weaker economic growth (at 1.5%yoy) than the US. But the US experience will concern the RBA and on its own adds to the risk that rate cuts here are also delayed beyond our expectation for cuts to start around mid-year. Ultimately though what the RBA does will be determined by Australian inflation and there is good reason to think it won’t follow US inflation up in the months ahead: consumer demand has virtually stalled in Australia whereas it’s still strong in the US; the Australian CPI has a much lower weighting to rising rents than in the US; the NAB business survey points to a further leg down in inflation pressures in March; and partly reflecting this our Pipeline Inflation Indicator for Australia is continuing to fall.

Source: Bloomberg, AMP

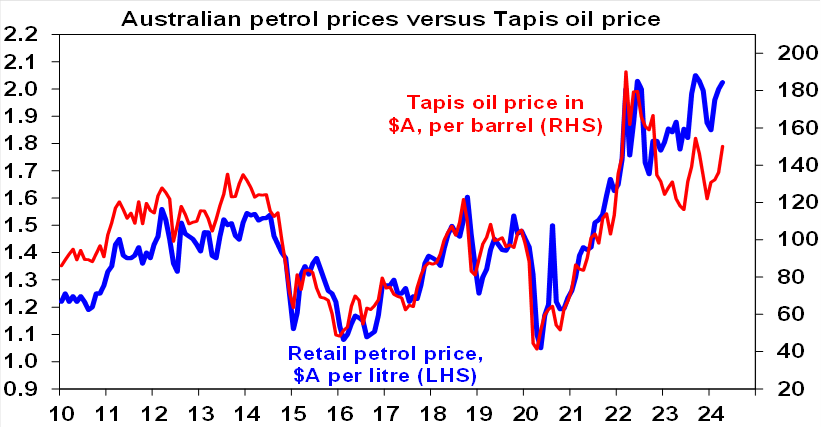

Petrol prices on the way back up again – what’s driving it? Of course a big risk on the inflation front is rising oil and petrol prices. Apart from the regular discounting cycle (which is currently on the way up in Sydney but varies from city to city) petrol prices on average are pushing back up to record highs. A big driver is a rebound in world oil prices where West Texas Intermediate has increased from lows below $US70/barrel last year to around $US86 reflecting stronger than expected global oil demand and potential supply threats particularly if Iran (which produces about 3.5% of world oil) directly enters into war with Israel. However, as can be seen in the chart below oil prices even measured in Australian dollars (red line) are well below their 2022 record high and yet petrol prices (blue line) are near record highs. The explanation appears to lie in widening refinery margins over the last 18 months. Higher oil and hence petrol prices are an obvious threat to the economic outlook as they add to inflation and act as a tax hike on consumers leaving less to spend on other things.

Source: Bloomberg, AMP

More bigger government – its popular, but we have seen it all before. The last two weeks have seen a further push towards bigger government involvement in the Australian economy – with the ACCC to be given power to review more mergers and the launch of a “Future Made in Australia” plan with more to come in the Budget. The bigger government trend started with the GFC, got a push along by Covid and is being supercharged by the energy transition, heightened national security concerns, a more left leaning electorate and the dimming of memories of the problems of high government intervention in the past. “Making more things in Australia” is a worthy objective. I was buying Holdens up to their very end in 2017, but ultimately not many fellow Australians were and so they went bust. I am all for making things in Australia but not if its dependent on subsidies, trade barriers and government trying to “pick winners”. Unfortunately, the “Future Made in Australia” plan sounds just like old fashioned protectionism. It will feel good for a while - just as government protection creating the industries of the post WW2 future (notably cars and consumer whitegoods) did initially. But there is little evidence that we have a comparative advantage in producing things like solar panels (where prices are collapsing globally) or that government has any ability to pick industry winners to be bestowed with taxpayer money.

The odds are that just as we saw with post war protectionism, we will end up with industries forever dependent on government support for survival and consumers and non-protected businesses will suffer with higher prices and/or lower quality products. A key lesson from the post war period is that government should avoid trying to pick winners but focus on making the business environment right in areas like tax, industrial relations, training and regulation. If taxpayers in other countries want to spend trillions subsidising products for us to buy or other countries can produce them more efficiently, then we should take them and produce things we have a comparative advantage in as determined by free market forces. It’s also hard to justify such industry policy from an employment perspective when we already have full employment and if national security is the justification, then surely products other than solar panels are more worthy. The proposed ACCC reforms to ensure industries remain competitive make some sense – the key though is that it’s done in a way that does not just further burden companies with regulation and costs, does not discourage start ups and does not prevent companies achieving economies of scale.

Major global economic events and implications

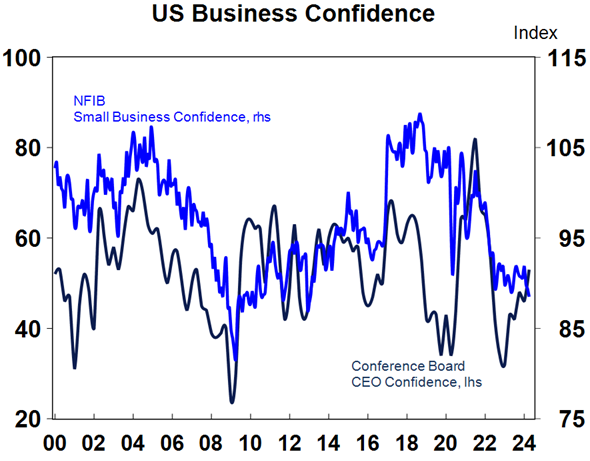

Mixed business sentiment data in the US – with small business optimism down in March with falling hiring plans and weak capex but CEO optimism up. Meanwhile, initial jobless claims fell and remain very low but continuing claims rose.

Source: Macrobond, AMP

The ECB’s March quarter bank lending survey showed continuing weak loan demand consistent with soft economic conditions.

The Reserve Bank of New Zealand left rates on hold as expected. While its guidance was little changed noting that monetary policy will need to remain tight for a “sustained period” it leant a bit dovish characterising growth as “weak” and removing references to concern about upside inflation risks. The money market expects the RBNZ to start cutting in October.

Japanese consumer confidence rose for the sixth month in a row in March and wages growth picked up, although the latter may be distorted by a change in the survey sample.

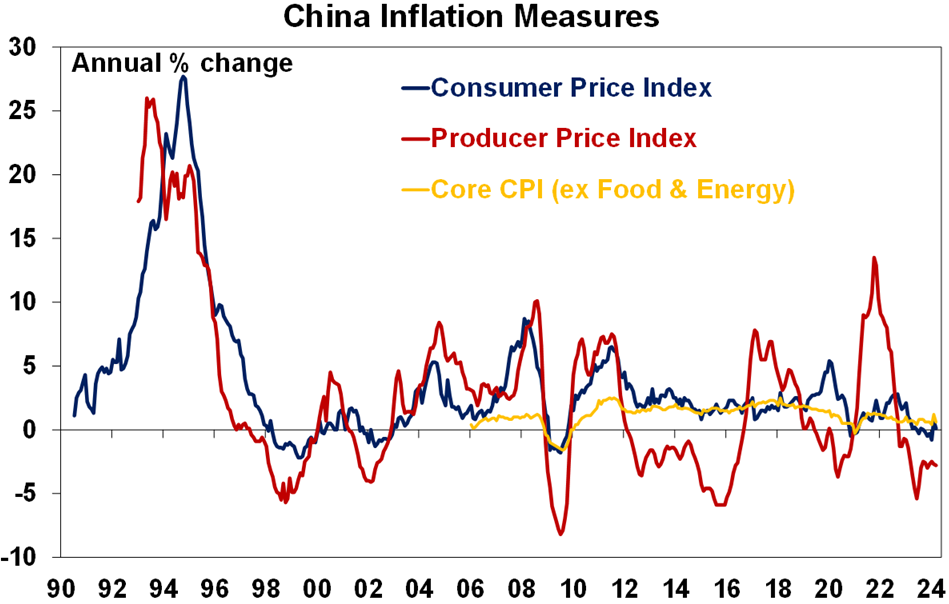

Chinese inflation down more than expected in March. CPI inflation fell back to 0.1%yoy and core inflation fell to 0.6%yoy after this year’s later Lunar New Year holiday pushed up inflation in February. Producer price deflation continued at -2.8%yoy pointing to a likely resumption of CPI deflation. Clearly the PBOC can afford to provide more monetary stimulus. Both exports and imports softened more than expected in March and money supply and credit data were mixed but with credit growth slowing further to 8.7%yoy from 9%.

Source: Bloomberg, AMP

Australian economic events and implications

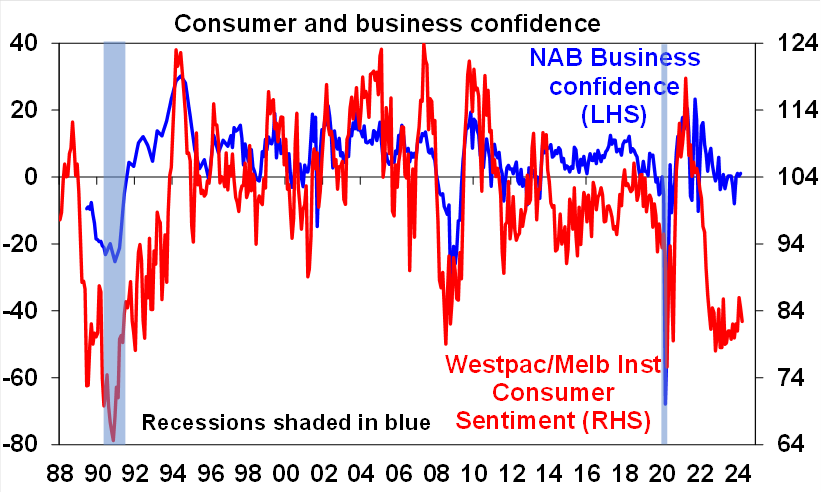

Australian consumer confidence remains weak. It fell again in April and remains around recessionary levels with perceptions around family finances, the economy and whether it’s a good time to buy major household items all remaining depressed pointing to still subdued consumer spending. Perceptions around whether now is a good time to buy a property also remain depressed acting as a constraint on the property market. By contrast business confidence remains far stronger reflecting slightly above average business conditions, although both are well down from their highs a few years ago. Businesses forward orders are also around levels associated with weak economic growth.

Source: Westpac/MI, NAB, AMP

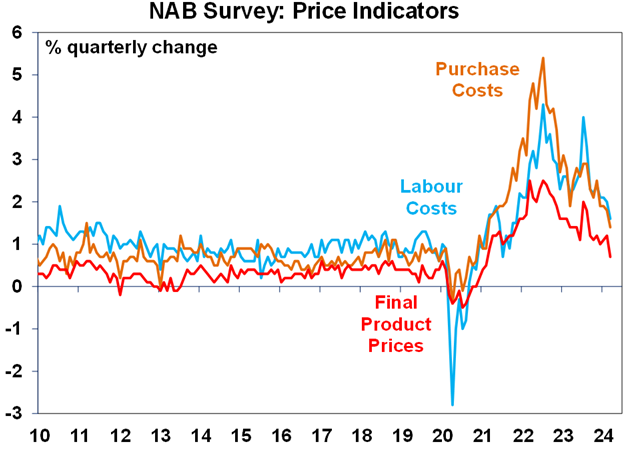

The good news is that business cost and price pressures continue to ease consistent with a further fall in inflation.

Source: NAB, AMP

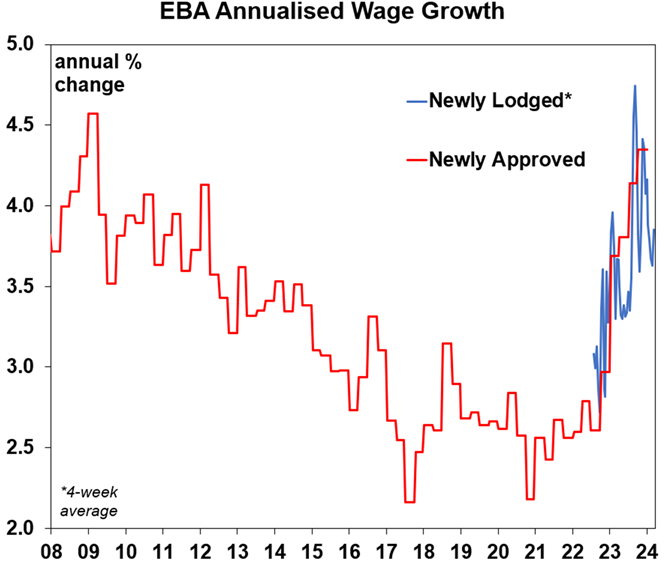

Consistent with the slowing labour cost pressures in the NAB survey, wage gains under newly lodged enterprise bargaining agreements are also consistent with a peak having been seen in wages growth.

Source: Fair Work Commission, AMP

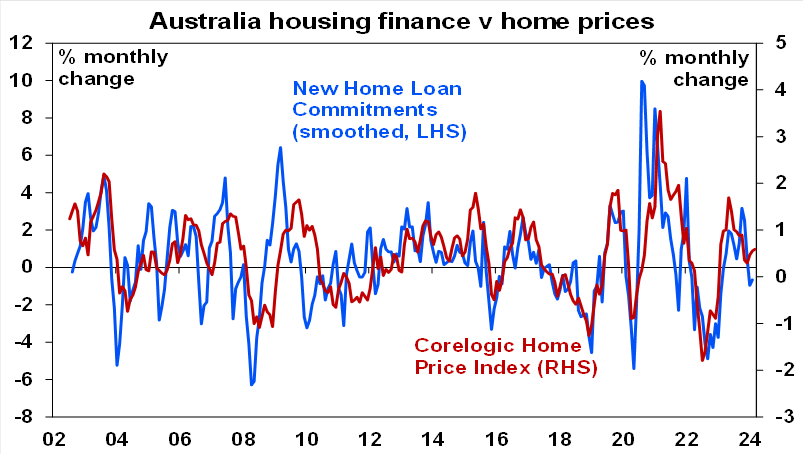

Housing finance picked up in February but it remains well down from its last cyclical high and its soft momentum is consistent with slower home price growth.

Source: ABS, AMP

What to watch over the next week?

In the US, expect modest gains in March data for retail sales (Monday) and industrial production (Tuesday), a fall in housing starts (also Tuesday) after a strong bounce in February, and continuing subdued readings in manufacturing conditions in the New York and Philadelphia regions. The March quarter earnings reporting season will also start to pick up pace with consensus earnings expectations currently around 4%yoy, but with another upside surprise likely on the back of strong March quarter economic growth and early reporters coming in well above this.

March inflation data will be released in both Canada (Tuesday) and the UK (Wednesday) and March quarter inflation will be released in New Zealand (also Wednesday).

Japanese March CPI inflation (Friday) is expected to rise to 2.9%yoy (from 2.8%) but with core inflation slowing to 2.3%yoy (from 2.5%)

Chinese March quarter GDP (Tuesday) is expected to come in at 1.6%qoq after just 1% in the December quarter but annual growth will slow slightly to 5%yoy from 5.2% due to base effects. March data is expected to show growth in industrial production slowing to 6%yoy and retail sales slowing to 5%yoy.

In Australia, jobs data for March (Thursday) is expected to show employment down by 15,000 after changed seasonal patterns led to a 116,500 surge in February with unemployment rising slightly to 3.9%.

Outlook for investment markets

Easing inflation pressures, central banks moving to cut rates and prospects for stronger growth in 2025 should make for good investment returns this year. However, with a high risk of recession and investors and share market valuations no longer positioned for recession and geopolitical risks, the remainder of the year is likely to be a rougher and more constrained ride than it has been so far.

We expect the ASX 200 to return 9% this year and rise to around 7900. This is now looking conservative. A recession is probably the main threat.

Bonds are likely to provide returns around running yield or a bit more, as inflation slows, and central banks cut rates.

Unlisted commercial property returns are likely to be negative again due to the lagged impact of high bond yields & working from home.

Australian home prices are likely to see more constrained gains compared to 2023 as still high interest rates constrain demand and unemployment rises. The supply shortfall should provide support though and rate cuts from mid-year should help boost price growth later in the year.

Cash and bank deposits are expected to provide returns of over 4%, reflecting the back up in interest rates.

A rising trend in the $A is likely taking it to $US0.72, due to a fall in the overvalued $US & the Fed cutting rates by more than the RBA.

Weekly market update 26-07-2024

26 July 2024 | Blog Dr Shane Oliver discusses the risk off as tech hit continues; correction risks into August/September; global rate cutting cycle underway; Australian June quarter CPI to rise but the hurdle to another RBA rate hike should be high; and more. Read more

Oliver's insights - rise of populism and bigger government

24 July 2024 | Blog This article takes a look at the rise of populism and what it means for economic policies and investors. Read more

Weekly market update 19-07-2024

19 July 2024 | Blog This week shares are down; US election/Trump prospects starting to impact; global rates easing cycle on track; China Plenum; Australian jobs still tight but easing so RBA needs to be careful; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.