Investment markets and key developments

Global share markets rose further over the last week helped by US data showing a softening jobs market and continuing moderation in underlying inflation in the US and Europe adding to expectations that the Fed and ECB will leave interest rates on hold in September. For the week US shares rose 2.5%, Eurozone shares rose 1.4% and Japanese shares rose 3.4%. The further rise in US shares over the last week curtailed a 4.8% fall earlier in August to a 1.8% loss for the month. This followed strong gains in June and July though. Chinese shares also rose 2.2% over the last week helped by a halving in stamp duty costs for share transactions which usually provides a temporary boost but also the roll out of more property stimulus measures and expanded tax breaks. Following the solid global lead and helped along by lower-than-expected Australian inflation data adding to confidence that the RBA will leave rates on hold, Australian shares rose 2.3% over the last week. As in the US the rebound curtailed an earlier 4% fall in August to just a 1.4% decline. For the week gains were led by consumer discretionary, material, finance and industrial shares. Bond yields eased further as expectations for further central bank rate hikes continued to ease. Oil, metal, iron ore prices and the $A rose despite a slight rise in the $US.

Shares have had a good rebound over the last two weeks and given the moderation in economic data and ongoing easing in inflation taking pressure off central banks its possible that we have already seen the correction (with the roughly 4-5% fall in share markets into mid-August). However, a further correction remains possible given that: the risk of recession remains high; China’s economy is still at risk; there is a risk that the disinflation process could pause in response to higher energy prices and sticky services inflation; central banks are still leaning hawkish; there is a high risk of another US Government shutdown from 1 October if US politicians fail to agree a budget or continuing resolution this month; high bond yields are still pressuring share market valuations; and the weak seasonal period for shares goes out to October. However, our 12-month view on shares remains positive as inflation is likely to continue to trend down taking pressure off central banks and any recession is likely to be mild.

On the global central bank front – better news for the Fed, less so for the ECB. US data showing more signs of a cooling jobs market – with payrolls remaining in a slowing trend and unemployment rising in August - and a moderation in monthly inflation further lower expectations that the Fed will have to hike rates again. By contrast Eurozone headline inflation was a bit stronger posing a dilemma for the ECB. We see both central banks leaving rates on hold this month, but the risks of another hike are higher in Europe.

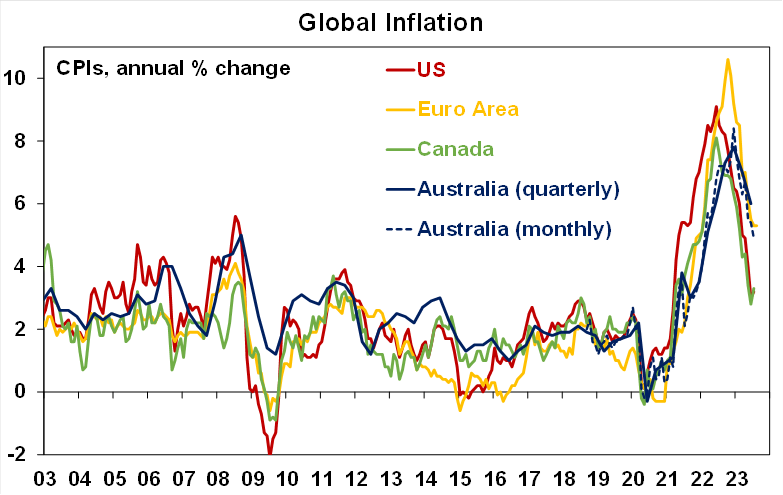

Australian inflation fell more than expected in July adding to the likelihood that the RBA’s cash rate has peaked. From its peak of 8.4%yoy in December, the Monthly Inflation Indicator has now fallen to 4.9%yoy in July. This was less than consensus and our own expectations. The bad news is that inflation is still too high and several key areas are still seeing very strong and accelerating inflation – notably rents, electricity and insurance costs - and higher petrol prices may boost inflation again in August. However, the good news is that the trend in inflation including for underlying inflation is down, the 3 month seasonally annualised rate of inflation at 2.7% is now within the RBA’s target range, while the Monthly Inflation Indicator can be volatile it’s looking like inflation will again come in below the RBA’s 6%yoy forecast for this quarter, government energy bill subsidies for eligible customers are taking the edge of electricity price rises (which otherwise might have added an extra 0.3% to inflation) and this will continue through 2023-24 and numerous CPI components are seeing lower rates of inflation (food, housing, furnishing and household equipment and holiday travel) or inflation within the target range (clothing and transport). It can also be seen in the next chart that Australian inflation is continuing to follow US inflation down with a lag of about six months, just like we lagged on the way up.

Source: Bloomberg, ABS, AMP

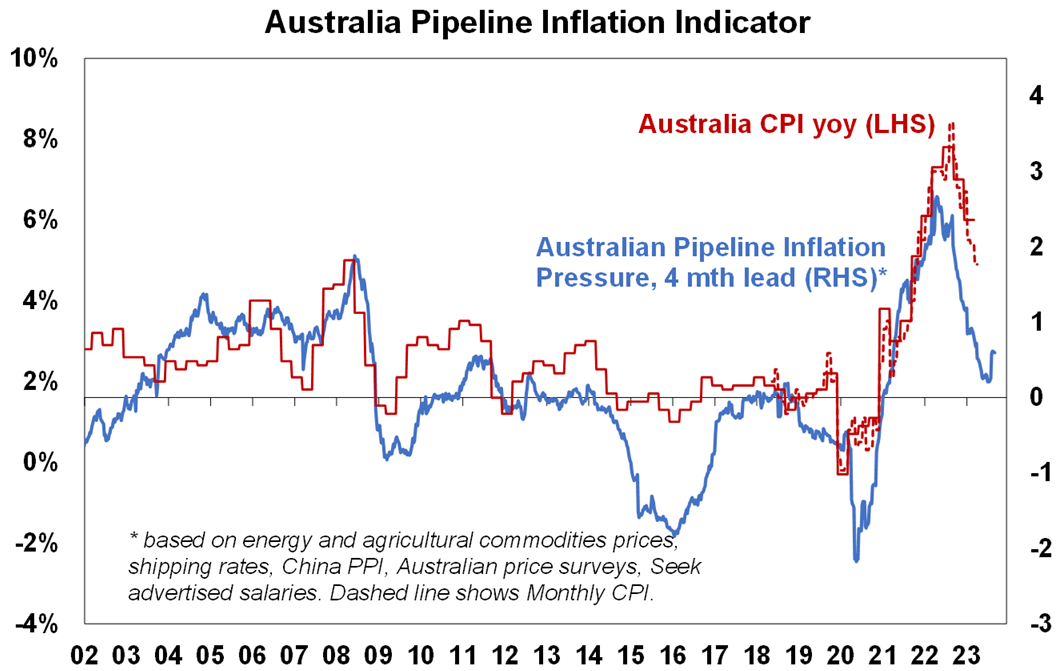

While our Australian Pipeline Inflation Indicator has picked up a bit recently with higher labour costs in business surveys it continues to point to a further sharp fall in inflation ahead. There is a good chance that inflation will be at 3% by mid next year, 12 months ahead of RBA expectations.

Source: Bloomberg, AMP

The RBA is expected to leave rates on hold at 4.1% on Tuesday. The further downside surprise on inflation coming on the back of weaker than expected wages growth, softer jobs data, a continuing flat trend in retail sales along with weaker business conditions globally are consistent with the RBA remaining in wait and see mode and therefore leaving interest rates on hold for the third month in a row. That said - given that inflation remains too high, the Monthly CPI Indicator is volatile, services inflation risks being sticky and the risks are on the upside risks for wages growth - the RBA is likely to reiterate that “that some further tightening of monetary policy may be required,” which was effectively reiterated by soon to be Governor Michelle Bullock in the past week. However, in the absence of stronger than expected wages growth, a further drop in unemployment and/or a reversal of the downtrend in inflation the RBA is expected to leave interest rates on hold for the rest of this year ahead of rate cuts next year. The money market is attaching a zero probability of a hike on Tuesday (which seems a bit extreme) and 25% chance of 0.25% hike by February next year.

Blocking Qatar’s request for 28 extra flights to Australia is hard to fathom in the context of the need to lower prices and boost productivity. If Qatar is proven to be “dumping” cheap flights into the Australia/Europe airline route then fair enough but this will be hard to prove. More fundamentally Australia needs more competition in key service industries to boost productivity and lower prices and blocking extra Qatar flights would seem contrary to this objective and against the interest of Australian consumers.

Economic activity trackers

Our Economic Activity Trackers are still not providing any decisive indication of recession (or a growth rebound).

Levels are not really comparable across countries. Based on weekly data for eg job ads, restaurant bookings, confidence, credit & debit card transactions and hotel bookings. Source: AMP

Major global economic events and implications

US economic data was mixed. Home prices continued to rise in June and personal spending rose sharply in July. The July manufacturing conditions ISM rose slightly more than expected but remains weak at 47.6, with the components for employment, new orders and prices paid all below 50. Consumer confidence unexpectedly fell in August and the sharp rise in consumer spending relative to incomes saw the household savings rate fall.

Source: Macrobond, AMP

With US excess savings built up during the pandemic now run down by around 75%, the jobs market slowing and the reopening boost behind us it’s unclear how long consumer spending on goods and services in particular can continue to remain above their pre-pandemic trends.

Source: Macrobond, AMP

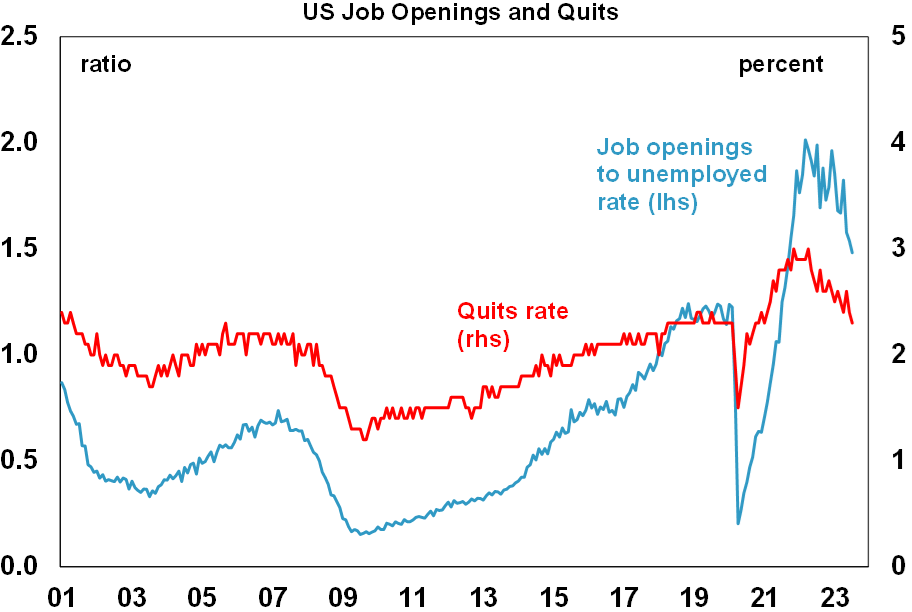

US labour market indicators are continuing to soften. Payrolls rose by a stronger than expected 187,000 in August, but the prior two months were revised down by 110,000, the trend in payroll increases remains down, unemployment rose to 3.8% and participation continues to recover. In addition, job openings, the hiring rate and people quitting for new jobs all fell in July and new layoffs rose to a new high for the post pandemic recovery. Its increasingly clear that that the jobs market is continuing to cool and this will further take pressure off wages growth which fell to 4.3%yoy in August. The softening trend in payrolls and other US labour market indicators supports the case for the Fed to leave rates on hold this month.

Source: Macrobond, AMP

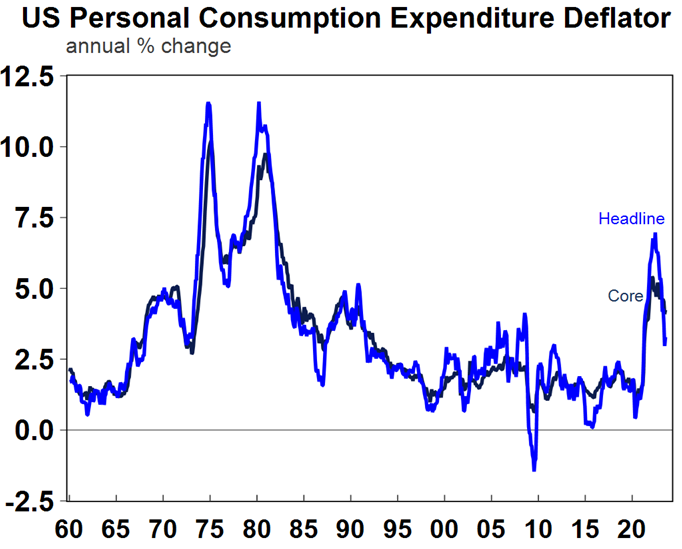

Meanwhile US core consumption price deflator inflation (which is the Fed’s preferred measure of inflation) rose to 4.2%yoy from 4.1%yoy in June but this was due to base effects as the monthly increase remained at 0.2%mom (or 2.4% annualised). This is likely consistent with the Fed leaving rates on hold at its September meeting.

Source: Macrobond, AMP

Eurozone economic data was soft, but inflation is a bit sticky. Economic confidence fell again in August and is now back to around last year’s lows and unemployment was unchanged at 6.4%. However, CPI inflation in August was unchanged at 5.3%yoy, which is down from a peak of over 10%yoy last year but higher than market expectations for a fall to 5.1%yoy. Core inflation still fell to 5.3%yoy from 5.5%. The latest inflation data poses a bit of a dilemma for the ECB, but on balance its likely to leave rates on hold in September as it waits for the lagged impact of rate hikes to slow growth and inflation, but the risks are high of another hike and its likely to retain a strong hawkish bias.

Japanese economic data for July was mostly softer than expected. Retail sales rose solidly but consumer sentiment weakened, unemployment rose slightly, job openings fell slightly relative to job applicants and industrial production fell by more than expected not helped by weak global demand.

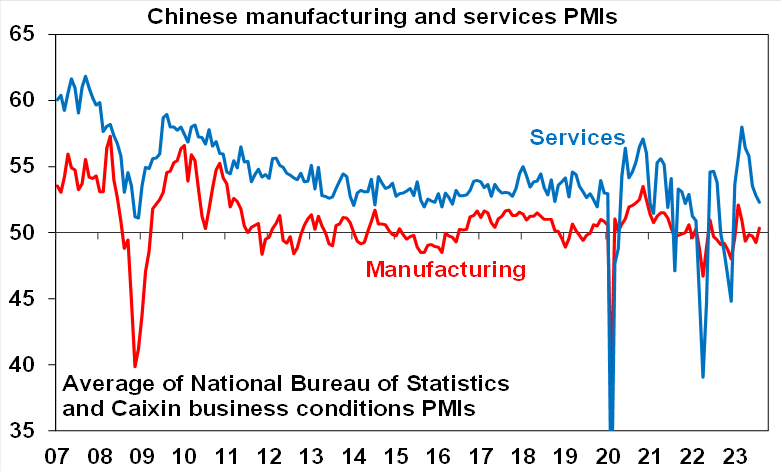

Chinese business conditions PMIs were mixed in August with manufacturing up but services down as more policy stimulus is announced. The overall picture is that growth is slow but it’s not collapsing and certainly not as negative as many appear to be portraying China. Meanwhile, policy makers unveiled further easing measures with the effect of lowering mortgage rates and downpayments for homebuyers and expanding individual tax breaks for childcare, parental care and education. The latter could mean a reduction in individual tax payments equivalent to around 0.3% of household disposable income. It remains doubtful that this is enough though with more forceful measures to boost consumer spending still required. But the quickening delivery of policy stimulus measures suggest that the Chinese Government is serious about stimulating the economy and supporting the property market. If stimulus continues to build its potentially positive for the iron ore price (which may explain its recent rebound), Australian resources shares and the $A.

Source: Bloomberg, AMP

In contrast to China’s softness (with GDP up 6.3%yoy in the June qtr), the Indian economy grew 7.8%yoy in the June quarter, with investment +8%yoy & consumer spending +6%yoy.

Australian economic events and implications

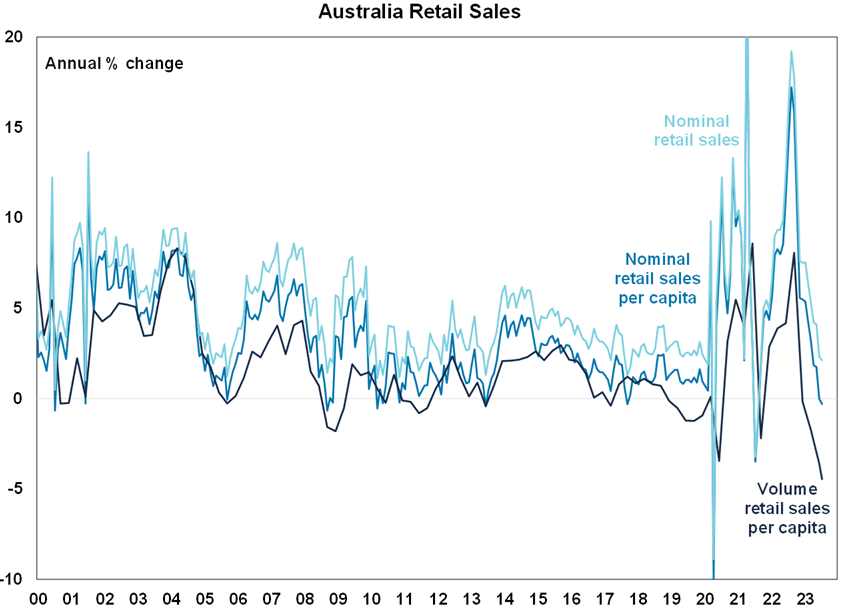

Australian economic data was soft. While retail sales rose 0.5% in July partly helped by soccer World Cup spending, this was after a 0.8% fall in June. In fact, after adjusting for the surge in population they are now down slightly in nominal terms on a year ago and real per capita retail sales are now running down 5%yoy, which is their weakest in the last two decades at least. In other words, take surging population growth away and the economy would look at lot weaker. See the next chart.

Source: Macrobond, AMP

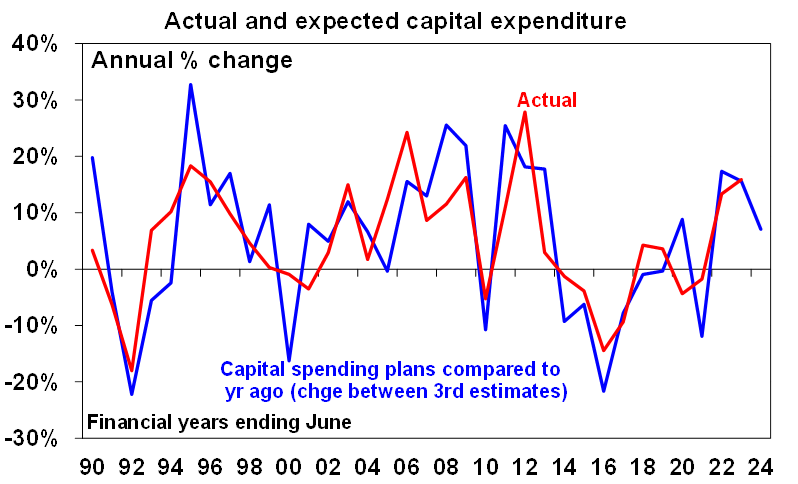

Business investment was a bit stronger in the June quarter than expected, although investment plans still point weaker growth ahead. For the quarter business investment rose 2.8% and will be a source of support for June quarter GDP growth. However, investment plans for the current financial year are only up 7.1% on the same estimate made for the last financial year pointing to a deceleration in growth from the 15.9% rise seen in 2022-23. This is in nominal terms so the slowdown after allowing for inflation will be greater.

Source: ABS, AMP

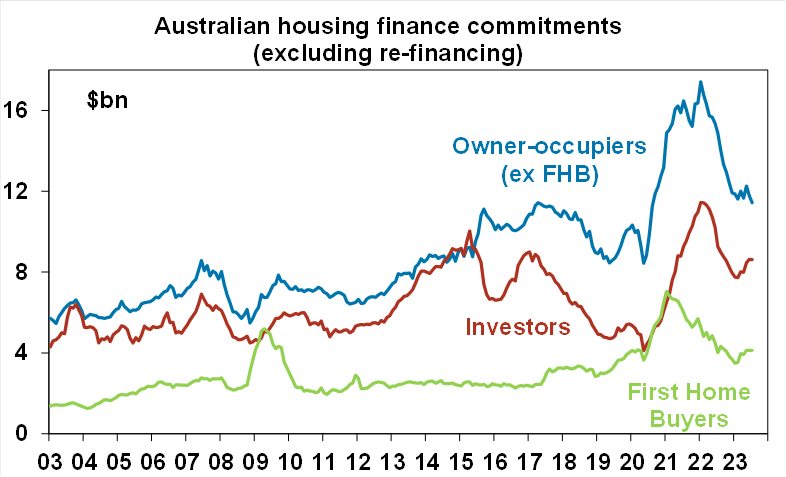

Housing construction related indicators were weak with building approvals down another 8.1% in July and down 10.6% on a year ago, the number of new loans for home construction fell 12.4% in July and are down 42%yoy and June quarter housing construction was flat implying a zero contribution to June quarter GDP growth.

Meanwhile, home price growth picked up a bit again in July according to CoreLogic to 0.8%mom. Prices are now up by 4.9% from their February low and although the pace of growth has slowed from May when it was 1.2%mom it’s still solid suggesting that the underlying supply shortfall in the face of surging immigration is continuing to dominate the impact of rate hikes. Our base case remains that home prices have bottomed with more gains likely next year as the RBA starts to cut rates. However, uncertainty is high given the pickup in listings that we are now seeing which will likely intensify in the Spring selling season, increasing levels of mortgage stress as the full impact of rate hikes flows through and the dampening impact on demand from reduced buying capacity as a result of the surge in mortgage rates since May last year. Interestingly housing finance commitments remain relatively weak (down 1.2% in July) and housing credit growth has not picked up in contrast to what would normally occur in a property price upswing.

Source: ABS, AMP

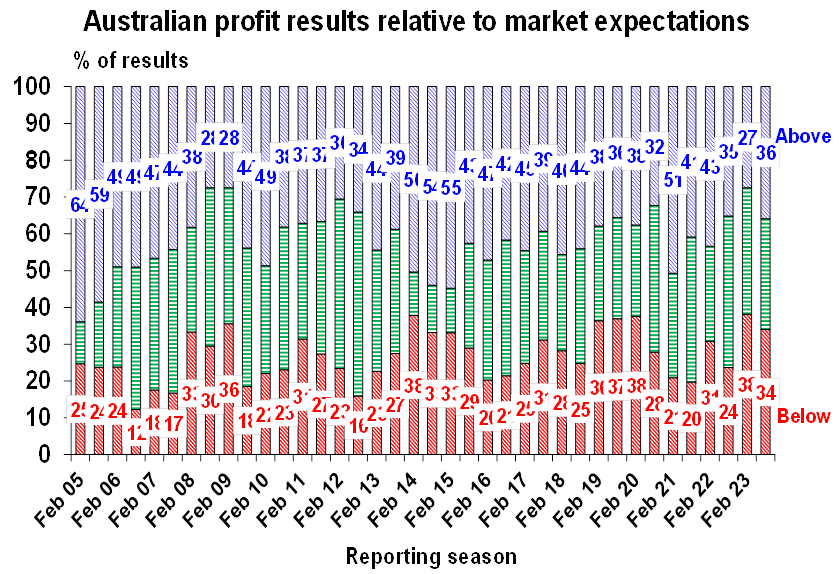

The Australian June half earnings reporting season is now a wrap. It’s been better than feared but expectations were still revised down on the back of cautious corporate guidance.

- Upside and downside surprises have been neck and neck with about 36% surprising on the upside which is below the norm of 43% and 34% surprising on the downside which is more than the norm of 26%.

Source: AMP

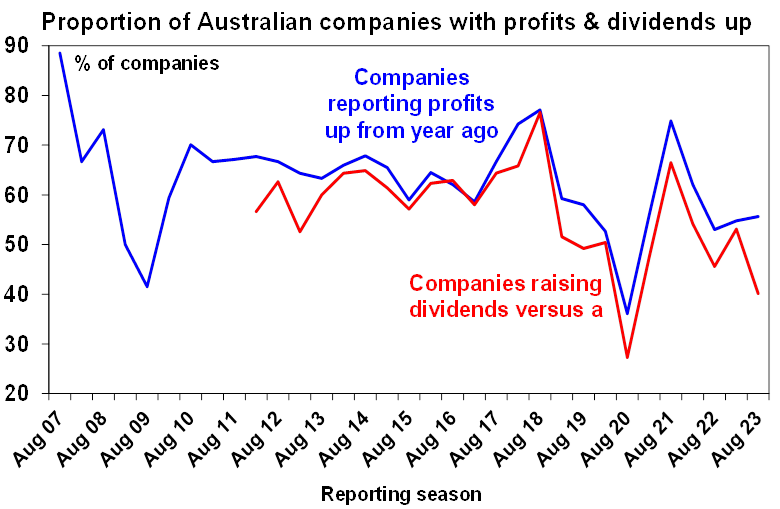

- 56% of companies have seen earnings rise on a year ago, but this is below the norm of 63%.

- Only 40% have increased their dividends on a year ago which is well below the norm of 58%, suggesting a degree of caution.

Source: AMP

- And 51% of companies have seen their share price outperform the market on the day they reported, which is better than in the February reporting season but less than the norm of 53%.

Key themes from the earnings results have been that: cost pressures remain a challenge; building material companies are still benefitting from strong activity although some are warning of a slowdown; insurers are seeing margin improvement at the expense of their customers with big premium increases; so far home borrowers are keeping up their payments (but rate hikes have yet to fully flow through); and corporate guidance has been cautious with more negative than positive guidance and retailers in particular are warning of tougher conditions and better off customers turning to discount stores for bargains. Partly reflecting the cautious outlook guidance consensus earnings expectations have been revised down since the reporting season started. The consensus is now for a +1.5% rise in earnings for 2022-23 and for a -5.7% fall in earnings in 2023-24, with both revised down from +2.5% and -0.8% respectively at the end of July.

What to watch over the next week?

It’s a light week ahead for US data releases but the services conditions ISM (Wednesday) for August is likely to slow slightly from 52.7 to 52.3.

Chinese August trade data (Thursday) is likely to show a further fall in exports and imports and inflation data (Saturday) is expected to see China remain in deflation.

The Bank of Canada (Wednesday) is expected to leave its key policy rate on hold at 5%, while signalling that it retains a bias to raise rates further.

In Australia, as noted earlier, the RBA (Tuesday) is expected to leave rates on hold at 4.1% but retain its mild tightening bias. Governor Lowe’s final speech on Thursday before he steps down is likely to expand on the RBA's thinking but may also offer a retrospective of his time as Governor.

On the data front in Australia, June quarter GDP (Wednesday) is expected to rise 0.4%qoq or 1.8%yoy, reflecting soft consumer spending, flat housing investment, moderate growth in business investment and public spending and a 0.4 percentage point contribution to growth from trade after a 0.2 percentage point detraction in the March quarter. Were it not for the contribution from net exports growth would likely be flat. Other data to be released includes the Melbourne Institute's Inflation Gauge, ANZ job ads and business indicators (Monday), net exports and public spending (Tuesday) and trade data (Thursday) which is expected to show a $9.7bn trade surplus.

Outlook for investment markets

The next 12 months are likely to see a further easing in inflation pressures and central banks moving to get off the brakes. This should make for reasonable share market returns, provided any recession is mild. But for the next few months shares are still at risk of a further correction given high recession and earnings risks, the risk of still more hikes from central banks, rising bond yields and poor seasonality out to October.

Bonds are likely to provide returns above running yields, as growth and inflation slow and central banks become dovish but given the recent rebound in yields this may be delayed a few months.

Unlisted commercial property and infrastructure are expected to see soft returns, reflecting the lagged impact of the rise in bond yields on valuations. Commercial property returns are likely to be negative as “work from home” hits space demand as leases expire.

With an increasing supply shortfall, our base case remains that home prices have bottomed with more gains likely next year as the RBA starts to cut rates. However, uncertainty around this is high given the lagged impact of interest rate hikes and the likelihood of higher unemployment.

Cash and bank deposits are expected to provide returns of around 4%, reflecting the back up in interest rates.

The $A is at risk of more downside in the short term on the back of a less hawkish RBA and weak growth in China, but a rising trend is likely over the next 12 months, reflecting a downtrend in the overvalued $US and the Fed moving to cut rates.

Oliver's Insights - seasonal patterns in shares

06 May 2024 | Blog This article looks at seasonal patterns in shares and whether its time to “sell in May and go away” along the lines of the old share market saying. Read more

Weekly market update 03-05-2024

03 May 2024 | Blog Fed less hawkish than feared; US stagflation or just getting back on track?; RBA to hold, with a tightening bias; Aust consumer remains weak; Aust budget preview. Read more

Econosights - positive supply shocks

02 May 2024 | Blog Post pandemic, the supply of labour has increased in many major economies, including the US and Australia, through elevated immigration and a lift in the participation rate to a record high. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.