Key points

- The last 20 years have seen a slump in productivity growth in Australia from over 2% pa to less than 1% pa. This has curtailed growth in living standards and real wages. It will adversely affect asset class returns if allowed to persist.

- Policies to boost productivity growth include: labour market reforms; more skills training; more infrastructure spending; increased housing supply; deregulation; and tax reform.

- Unfortunately, the political pendulum has moved against many of the policies necessary to boost productivity.

“Productivity isn’t everything, but, in the long run, it is almost everything”. Paul Krugman, Economist

“The only thing that we learn from history is that we learn nothing from history.” Georg Hegel, Philosopher

Introduction

Outgoing Reserve Bank Governor Philip Lowe has highlighted Australia’s weak productivity growth and noted that boosting it “should be the issue that dominates economic discussion”. So why is boosting productivity so important? And why is it seen as so hard to do? It’s worth having another look at it given its importance to our economy and investment markets.

What is productivity?

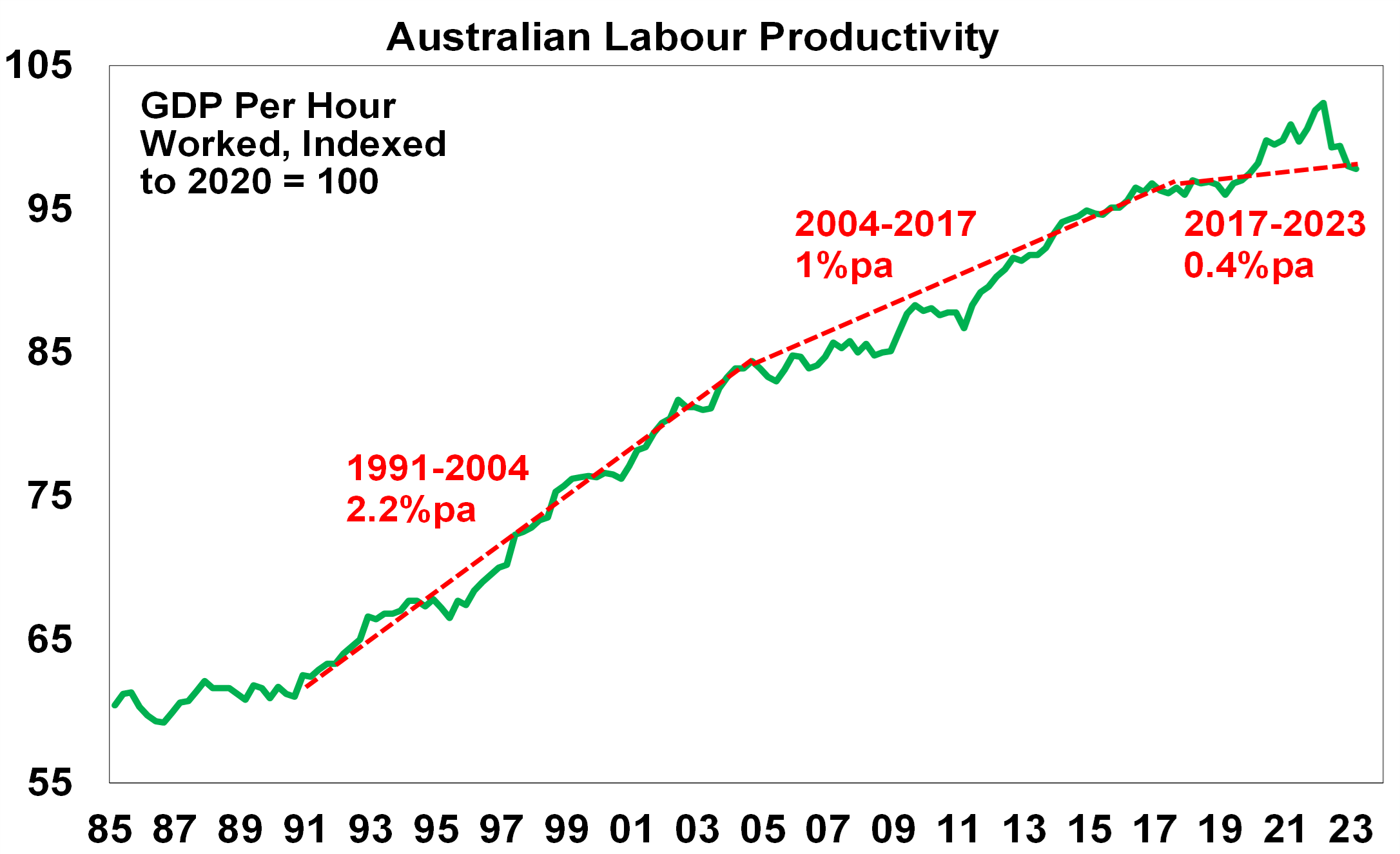

Productivity refers to the level of economic output for a given level of labour and capital inputs. Increased productivity means more is being produced for given inputs. Output usually refers to Gross Domestic Product and dividing inputs of labour (hours worked) and capital (structures and machinery) into GDP gives “multi factor productivity”. However, its more common to refer to measures of labour productivity, ie, GDP per hour worked. The next chart shows this for Australia.

Source: ABS, AMP

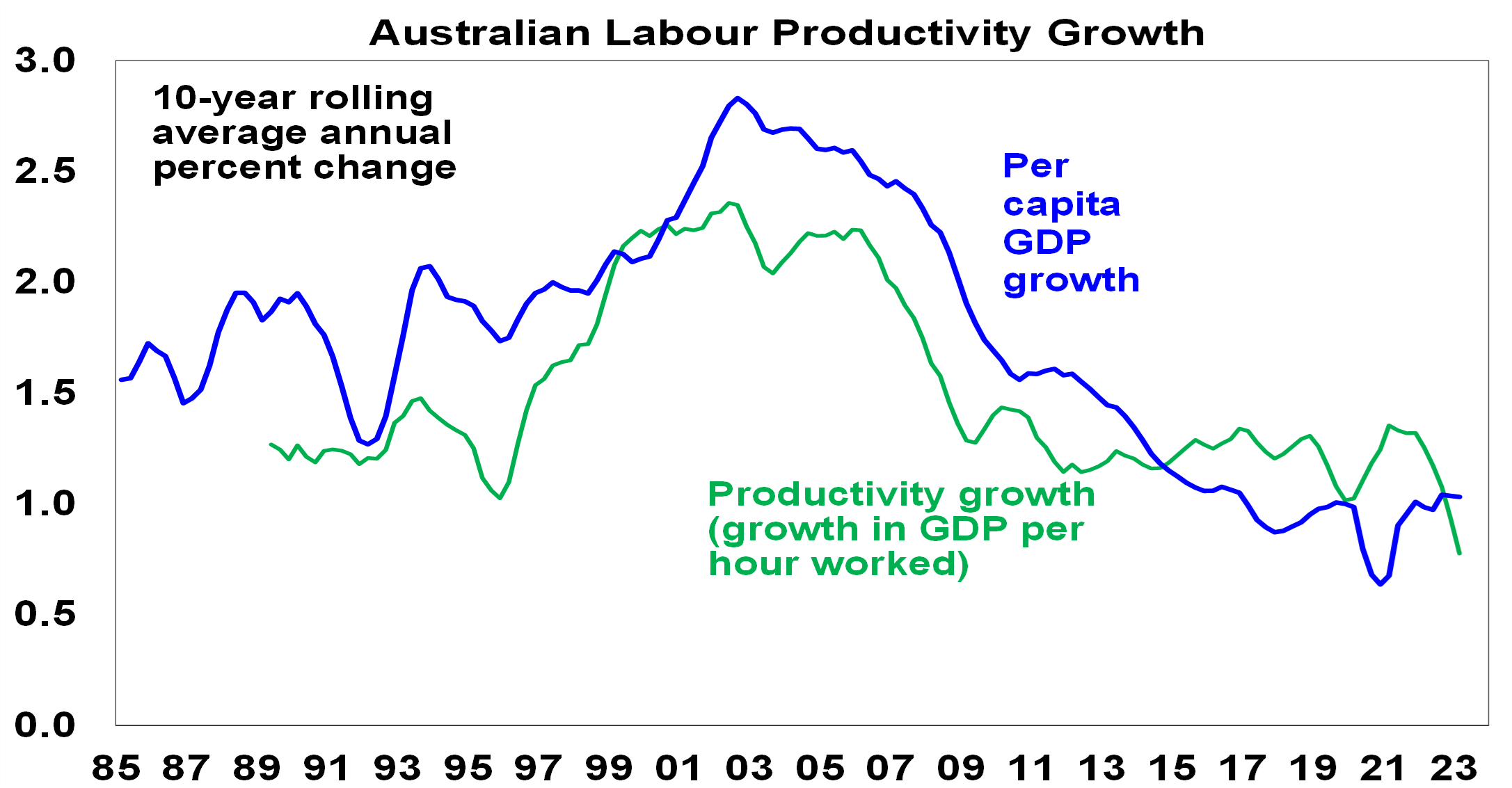

The next chart shows the annual rate of labour productivity growth (ie, the change in GDP per hour worked). Productivity growth rose to over 2% p.a. through the 1990s into the 2000s, but it’s slowed to less than one percent over the last decade. And since 2019 it’s stalled (see the first chart).

Source: ABS, AMP

Why does productivity matter?

Productivity matters because as Paul Krugman points out “a country's ability to improve its standard of living over time depends almost entirely on its ability to raise its output per worker”. As evident in the last chart, the longer-term pattern in labour productivity growth has correlated with a similar pattern in growth in GDP per capita (or GDP per person). Roughly speaking the slowdown in productivity growth from 2.2% pa in the 1990s to 0.8% pa over the last 10 years means that after a 10-year period annual GDP will be 13% (or $350bn) less than otherwise, which means lower material living standards than otherwise. Of course, we can make up for this by faster population growth as has been the case since the mid-2000s but this does not address the negative impact on living standards per person. Likewise in Australia the slump in productivity has been masked by the strong commodity prices and hence national income helped by the China boom – but medium-term threats to Chinese growth mean that we cannot rely on this indefinitely. Over time, lower productivity growth means lower real wages growth, slower growth in profits and a reduced ability for the government to provide services the community expects.

Why is it relevant for sustained decent wages growth?

If wages growth is 4% and output per worker goes up by 1.5% then the increase in labour costs for business is 2.5% which if passed on as higher prices is in line with the RBA’s 2-3% inflation objective. But if wages go up 4% and productivity growth is zero, business costs go up 4% and they will pass this on to their customers likely resulting in inflation above the RBA’s target. Hence 4% wages growth is consistent with the inflation target but only if productivity growth picks up to its long-term average of 1.5% pa.

So why the slump in productivity growth?

After the malaise of the high inflation/high unemployment 1970s, there was a focus in the 1980s on supply side economic reforms designed to improve productivity growth by making the economy more flexible and competitive, improving incentives and improving skills. This included financial deregulation, floating the $A, labour market deregulation, product market deregulation, reduced trade barriers, competition reforms, privatisation, tax reform and an improvement in educational attainment. Along with baby boomers reaching their peak productivity years, it saw productivity growth surge through the 1990s into the 2000s. But since then, a range of factors have contributed to slower productivity growth:

- There has been little in the way of new reforms since the GST and some backsliding – eg, the labour market has become less flexible.

- Very strong population growth with an inadequate infrastructure and housing supply response has led to urban congestion and poor housing affordability which contribute to poor productivity growth – notably via increased transport costs and increased speculative activity around housing diverting resources from more productive uses.

- The retirement of the baby boomer wave and replacement with a wave of less experienced millennials and Gen Z may drive slower productivity growth (just as baby boomers did in the 1970s).

- Growth in real business investment stalled in the 2010s.

- Market concentration has increased, reducing competition.

- Confusion regarding climate policies has contributed to underinvestment in power supply and high energy costs, and we have rejected an efficient market-based mechanism (carbon pricing and trading) to determine the best way to eliminate carbon emissions in favour of a “hotchpotch of measures” (according to former Productivity Commission chair Gary Banks).

- The services sector has grown as a share of the economy and it is more labour intensive and hence less productive.

- And the pandemic distorted productivity by first boosting it as (low productivity) services activity was curtailed by lockdowns and then reducing it as services activity rebounded with reopening.

The last point is arguably a temporary distortion which should pass as the reopening boost in services demand subsides – so the recent slump in productivity is likely to be reversed to some degree enabling us to get back to pre-pandemic trends. However, even this was relatively slow and all the other factors in the list above are likely longer lasting.

How do we boost productivity?

Unfortunately, there are no quick fixes. The key is to acknowledge the problem, discuss the options and chart a path forward. Fortunately, as Governor Lowe has regularly pointed out there are plenty of good ideas. At a high level, key areas for action include the following:

- Improving labour market flexibility and reviving Enterprise Bargaining.

- Measures to boost workforce capability – including apprenticeships.

- Maintain high levels of infrastructure spending to reduce congestion, lower transport costs & allow more to live away from expensive cities.

- Boost the supply of housing to more than match underlying population driven demand for several years until the housing shortfall is removed.

- Competition reforms to reduce market concentration.

- Better healthcare by focussing on prevention & management.

- More incentives to boost investment & adopt new technology, eg, AI.

- Improving public sector productivity.

- Reduce climate policy uncertainty and rely more on market signals as to how best to transition to net zero.

- Simplify regulations and remove redundant regulation.

- Limit the size of government.

- Tax reform to rebalance from direct tax to a broader GST, compensate those adversely affected, and remove nuisance taxes like stamp duty.

The Productivity Commission has recently updated its detailed list of recommendations. The use of AI in services will help but will take time & we’re yet to see much boost in measured productivity from the internet.

So, what’s stopping us?

The main constraint to boosting productivity is arguably political. The Government is focussed on improving skills, fixing energy supply and encouraging the adoption of new technology. However, support for the economic rationalist policies of the 1980s that gave rise to the supply side reforms of the Thatcher, Reagan, Hawke and Keating era (of smaller government, fundamental tax cuts, deregulation and privatisation) has long faded. In the 1980s the political pendulum swung to centre right policies in reaction to the failure of big government policies in the 1970s. Now the political pendulum has swung back to the left and away from free market solutions. This reflects a combination of:

- the feeling that the GFC showed de-regulation went too far;

- stagnant and recently falling real wages for median households;

- high household debt levels preventing individuals from taking on more debt as a way to boost living standards;

- rising levels of inequality and perceptions that “it’s unfair”;

- the perceived failure of the baby boomer generation to do much about climate change and housing affordability;

- examples of big business doing the wrong thing;

- a backlash against immigration in some countries;

- a backlash against globalisation and increasing geopolitical tensions;

- perceptions that government was able to protect us through the pandemic and if so it should be able to fix other problems too; and

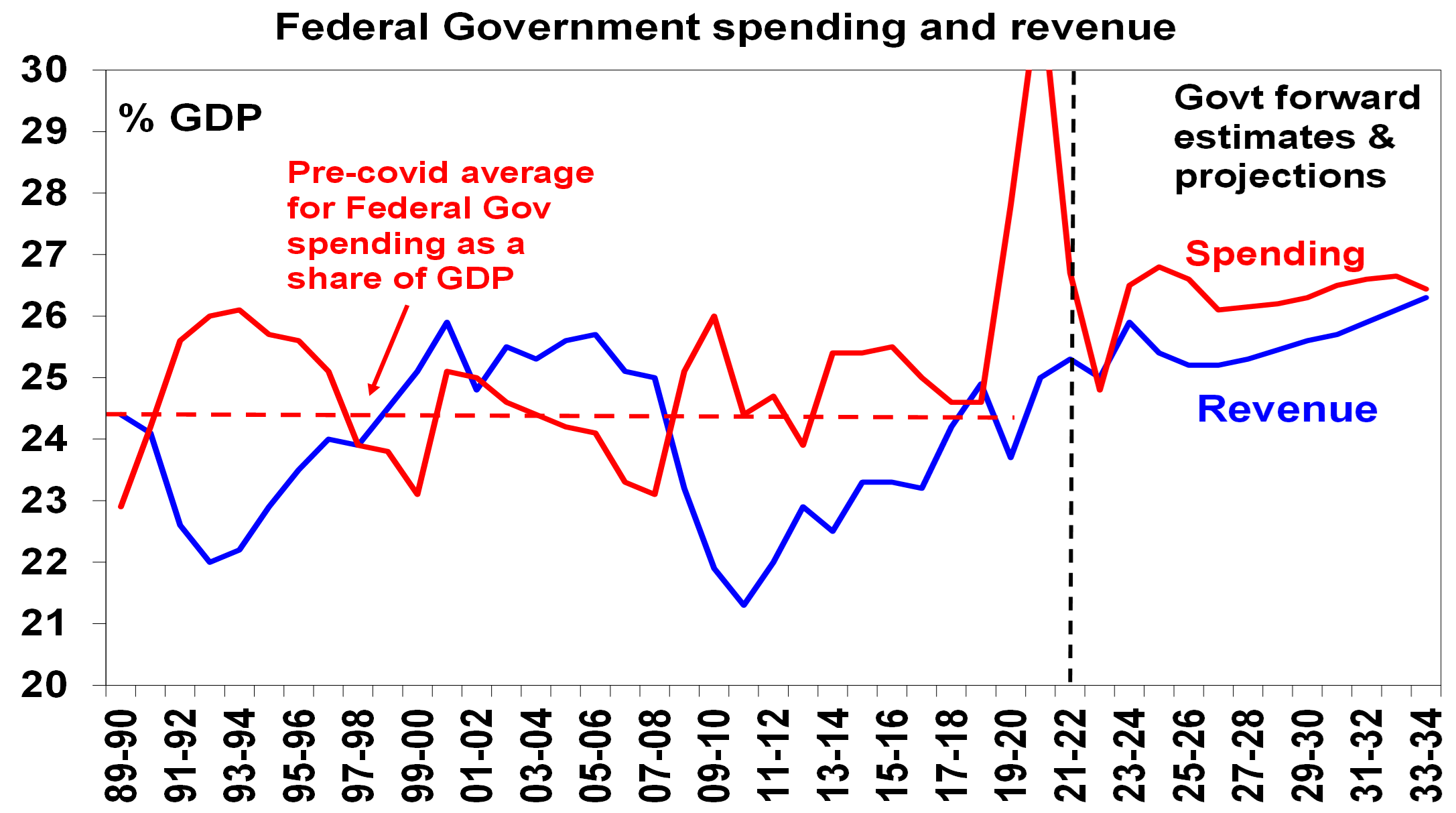

- the latter seems to have ushered in a permanently higher share of government spending and revenue in the economy.

Source: Australian Treasury – 2023-24 Budget Papers, AMP

Of course, it’s being aided by a dimming of memories of the stagflation of the 1970s and its causes. So, government related solutions – often tied to addressing national security & climate issues - seem more attractive than free market solutions. This is resulting in more government intervention - notably across advanced countries in subsidies to develop electric car or battery industries – reminiscent of the protectionism of the post WW2 era.

Concluding comment and implications for investors

Australia is in far better shape than many comparable countries – public debt is relatively low; unemployment is low; and we are less politically polarised and more open to compromise. However, after nearly two decades of policy drift, declining productivity growth is weighing on growth in living standards and sustainable real wages growth. Some boost in productivity is likely as pandemic related distortions drop out and some government measures will help. However, the political will for the sort of economic reforms necessary (particularly around taxation and labour markets) for another 1990s style rebound in productivity growth looks unlikely. This in turn makes the RBA’s job in getting inflation down a little bit harder and will constrain medium term investment returns.

Weekly market update 26-07-2024

26 July 2024 | Blog Dr Shane Oliver discusses the risk off as tech hit continues; correction risks into August/September; global rate cutting cycle underway; Australian June quarter CPI to rise but the hurdle to another RBA rate hike should be high; and more. Read more

Oliver's insights - rise of populism and bigger government

24 July 2024 | Blog This article takes a look at the rise of populism and what it means for economic policies and investors. Read more

Weekly market update 19-07-2024

19 July 2024 | Blog This week shares are down; US election/Trump prospects starting to impact; global rates easing cycle on track; China Plenum; Australian jobs still tight but easing so RBA needs to be careful; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.