Key points

- Investment markets are driven by more than just fundamentals. Investor psychology plays a huge role and helps explain why asset prices go through periodic booms and busts.

- The key for investors is to be aware of the role of investor psychology and its influence on their own thinking. The best defence is to be aware of past market cycles (so nothing comes as a surprise) and to avoid being sucked into booms and spat out during busts. If an investor is looking to trade they should do so on a contrarian basis. This means accumulating when the crowd is panicking, lightening off when it is euphoric.

Introduction

Up until the 1980s the dominant theory was that financial markets were efficient – in other words all relevant information was reflected in asset prices in a rational manner. While some think it was the Global Financial Crisis that caused faith in the so-called Efficient Markets Hypothesis (EMH) to begin unravelling, this actually occurred in the 1980s. In fact, it was the October 1987 crash that drove the nail in the coffin of the EMH as it was impossible to explain why US shares fell over 30% and Australian shares fell 50% in a two-month period when there was very little in the way of new information to justify such a move. It’s also hard to explain the 80% slump in the tech heavy Nasdaq index between 2000 and 2002 on the basis of just fundamentals. Study after study has shown share market volatility is too high to be explained by investment fundamentals alone. Something else is at play, & that is investor psychology.

Investor psychology

Several aspects of investor psychology interact in helping drive bull and bear phases in investment markets, including individual lapses of logic and crowd psychology.

Individuals are not rational

Numerous studies by psychologists have shown that – apart from me and you! - people are not always rational and tend to suffer from various lapses of logic. The most significant examples are as follows.

- Extrapolating the present into the future – people tend to downplay uncertainty and assume recent trends, whether good or bad, will continue.

- Giving more weight to recent spectacular or personal experiences in assessing the probability of events occurring. This results in an emotional involvement with an investment strategy – if an investor has experienced a winning investment lately he or she is likely to expect that it will remain so. Once a bubble gets underway, investors’ emotional commitment to it continuing steadily rises, thus helping to perpetuate it.

- Overconfidence - people tend to be overconfident in their own investment abilities.

- Too slow in adjusting expectations - people tend to be overly conservative in adjusting their expectations to new information and do so slowly over time. This partly reflects what is called “anchoring” where people latch on to the first piece of inflation they come across and regard it as the norm. This partly explains why bubbles and crashes in share markets normally unfold over long periods.

- Selective use of information - people tend to ignore information that conflicts with their views. In other words, they make their own reality and give more weight to information that confirms their views. This again helps to perpetuate a bubble once it gets underway.

- Wishful thinking – people tend to require less information to predict a desirable event than an undesirable one. Hence, asset price bubbles normally precede crashes.

- Myopic loss aversion – people tend to dislike losing money more than they like gaining it. Various experiments have found that a potential gain must be twice the potential loss before an investor will consider accepting the risk. An aversion to any loss probably explains why shares traditionally are able to provide a relatively high return (or risk premium) relative to “safer” assets like cash or bonds.

The madness of crowds

As if individual irrationality is not enough, it tends to get magnified and reinforced by “crowd psychology”. Investment markets have long been considered as providing examples of crowd psychology at work. Collective behaviour in investment markets requires the presence of several things:

- a means where behaviour can be contagious – mass communication with the proliferation of electronic media are a perfect example of this. More than ever, investors are drawing their information from the same sources, which in turn results in an ever-increasing correlation of views amongst investors, thus reinforcing trends;

- pressure for conformity – interaction with friends, monthly performance comparisons, industry standards and benchmarking, can result in “herding” amongst investors;

- a precipitating event or displacement that gives rise to a general belief that motivates investors. The IT revolution of the late 1990s, the growth in China in the 2000s and crypto currencies more recently are classic examples of this on the positive side. The demise of Lehman Brothers and problems with some crypto currencies/markets are examples of displacements on the negative side; and

- a general belief which grows and spreads – eg, share prices can only go up – this helps reinforce the trend set off by the initial displacement.

Bubbles and busts

The combination of lapses of logic by individuals in making investment decisions being magnified by crowd psychology go a long way to explaining why speculative surges in asset prices develop (usually after some good news) and how they feed on themselves (as individuals project recent price gains into the future, exercise “wishful thinking” & get positive feedback via the media, their friends, etc). Of course, the whole process goes into reverse once buying is exhausted, often triggered by contrary news to that which drove the rise initially.

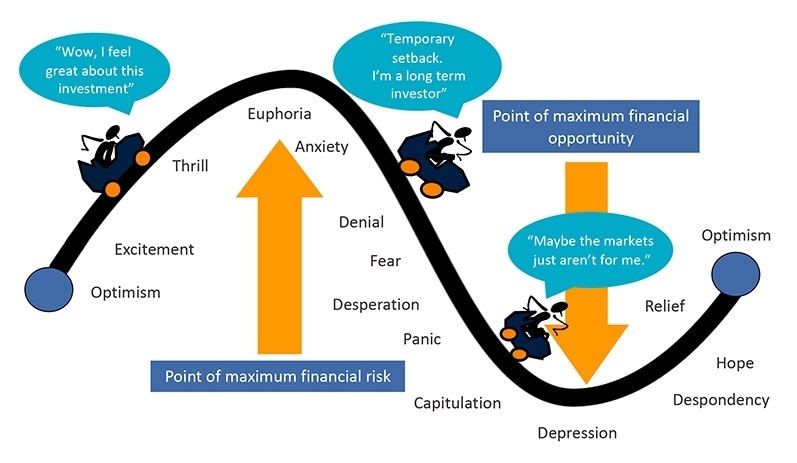

Investor psychology through a market cycle looks like what Russell Investments called the roller coaster of investor emotion. When times are good, investors move from optimism to excitement, and eventually euphoria as an investment’s price – be it shares, housing, gold, cryptos or whatever – moves higher and higher. So by the time the market tops out investors as group are maximum bullish and fully invested, often with no one left to buy. This ultimately sets the scene for a bit of bad news to push prices lower. As selling intensifies and prices fall further, investor emotion goes from anxiety to desperation, and eventually capitulation and depression. By the time the market bottoms out investors are maximum bearish and many are out of the market. This then sets the scene for the market to bottom as it only requires a bit of good news (or less bad news) to bring back buying, and then the cycle repeats.

The roller coaster of investor emotion through a market cycle

Source: Russell Investments, AMP

This pattern has been repeated time again over the years: in the early/mid 1990s with emerging markets; the late 1990s tech boom; late 2000s with the focus on credit, US housing; and arguably more recently with crypto currencies and yield plays.

Points to note

Firstly, confidence and investor psychology do not act in a vacuum. The move from depression at the bottom of a cycle to euphoria at the top is usually underpinned by fundamental developments, eg, strong economic growth and easy money.

Second, at market extremes confidence is best read in a contrarian fashion – major bull markets do not start when investors are feeling euphoric and major bear markets do not start when they are depressed. By the time investor confidence has reached these extremes, all those who wish to buy (or sell) have done so meaning it only requires a small amount of bad news (or good news) to tip investors the other way. So extreme low points in confidence are often associated with market bottoms, and vice versa for extreme highs.

Third, ideally one needs to look at what investors are thinking (sentiment) and what they are actually doing (positioning).

Finally, negative crowd sentiment at market bottoms can tend to be associated fairly quickly with market bottoms reflecting the steep declines associated with panics as a market falls. But during bull markets positive sentiment or even euphoria can tend to persist for a while as it takes investors longer to build exposures to assets than to sell them.

So where are we now in relation to shares?

The next charts shows the US share markets and a measure of US investor sentiment that includes surveys of investment newsletter writers and individual investors and the ratio of puts (options to sell shares) to calls (options to buy). It shows that extreme levels of pessimism tend to be associated with major market bottoms (indicated by the green arrows) and extreme measures of optimism tend to be associated with market tops (red arrows) although, as noted above, sentiment can be less reliable at tops.

Currently, the high levels of optimism seen last year are long gone after the plunge in shares, which left sentiment very negative and now sentiment is still negative but not extreme. If anything, this is mildly bullish from a contrarian perspective but after the rally since June it’s not a strong signal either way.

Source: Bloomberg, Sentimentrader, Investors Intelligence, AMP

What does this mean for investors?

There are several implications for investors.

- First, recognise that investment markets are not only driven by fundamentals, but also by the often-irrational and erratic behaviour of an unstable crowd of investors. The key here is to be aware of past market booms and busts, so that when they arise in the future you understand them and do not overreact (piling into unstable bubbles near the top or selling everything during busts and locking in a loss at the bottom).

- Second, try and recognise your own emotional responses. In other words, be aware of how you are influenced by lapses in your own logic and crowd influences like those noted above. For example, you could ask yourself: “am I highly affected by recent developments? Am I too confident in my expectations? Can I bear a paper loss?”

- Thirdly, to guard against emotional responses choose an investment strategy which can withstand inevitable crises whilst remaining consistent with your financial objectives and risk tolerance. Then stick to this even when surging share prices tempt you into a more aggressive approach, or when plunging values suck you into a defensive approach.

- Fourthly, if you are tempted to trade, do so on a contrarian basis. Buy when the crowd is bearish, sell when it is bullish. Extremes of bullishness often signal eventual market tops, and extremes of bearishness often signal bottoms. Successful investing requires going against the crowd at extremes. Various investor sentiment and positioning surveys can help. But also recognise contrarian investing is not fool-proof – just because the crowd looks irrationally bullish (or bearish) doesn’t mean it can’t get more so.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.