Key points

- We expect global growth to be ~2.5% in 2024, below the long-run average of ~3% and lower than the IMF’s forecast.

- A global recession is unlikely. However, given that most major central banks have been raising interest rates, the risk of over-tightening is high, reflected in recent poor GDP growth in countries across Europe and Japan.

How is global growth tracking?

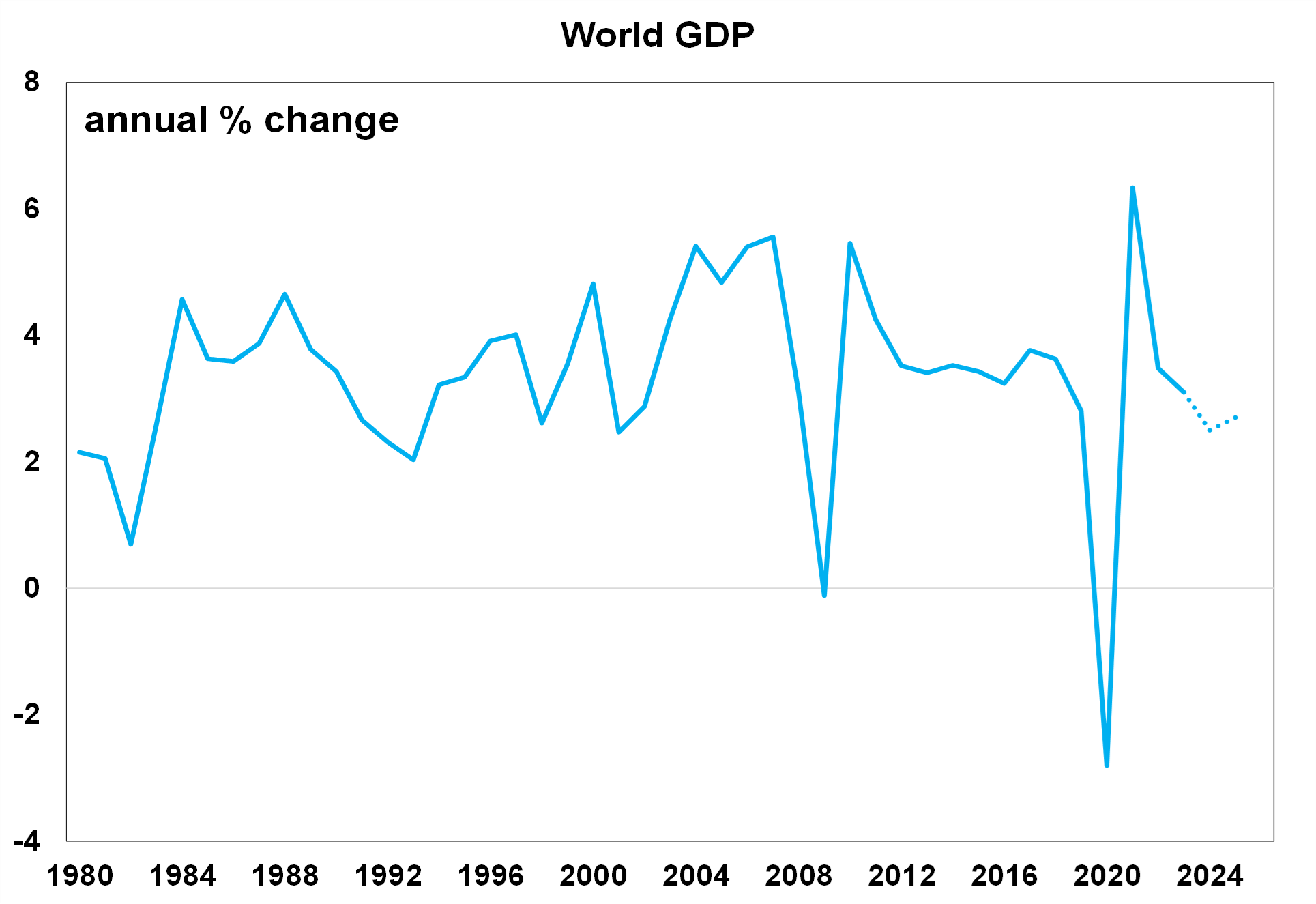

Global economic growth, as measured by GDP tends to average at 3% over the long run. This year we see global growth running at a sub-average 2.5% (see the chart below) after 3.1% in 2023. Institutions like the IMF are more optimistic, estimating 3.1% for 2024 and 3.2% for 2025.

Source: IMF, AMP

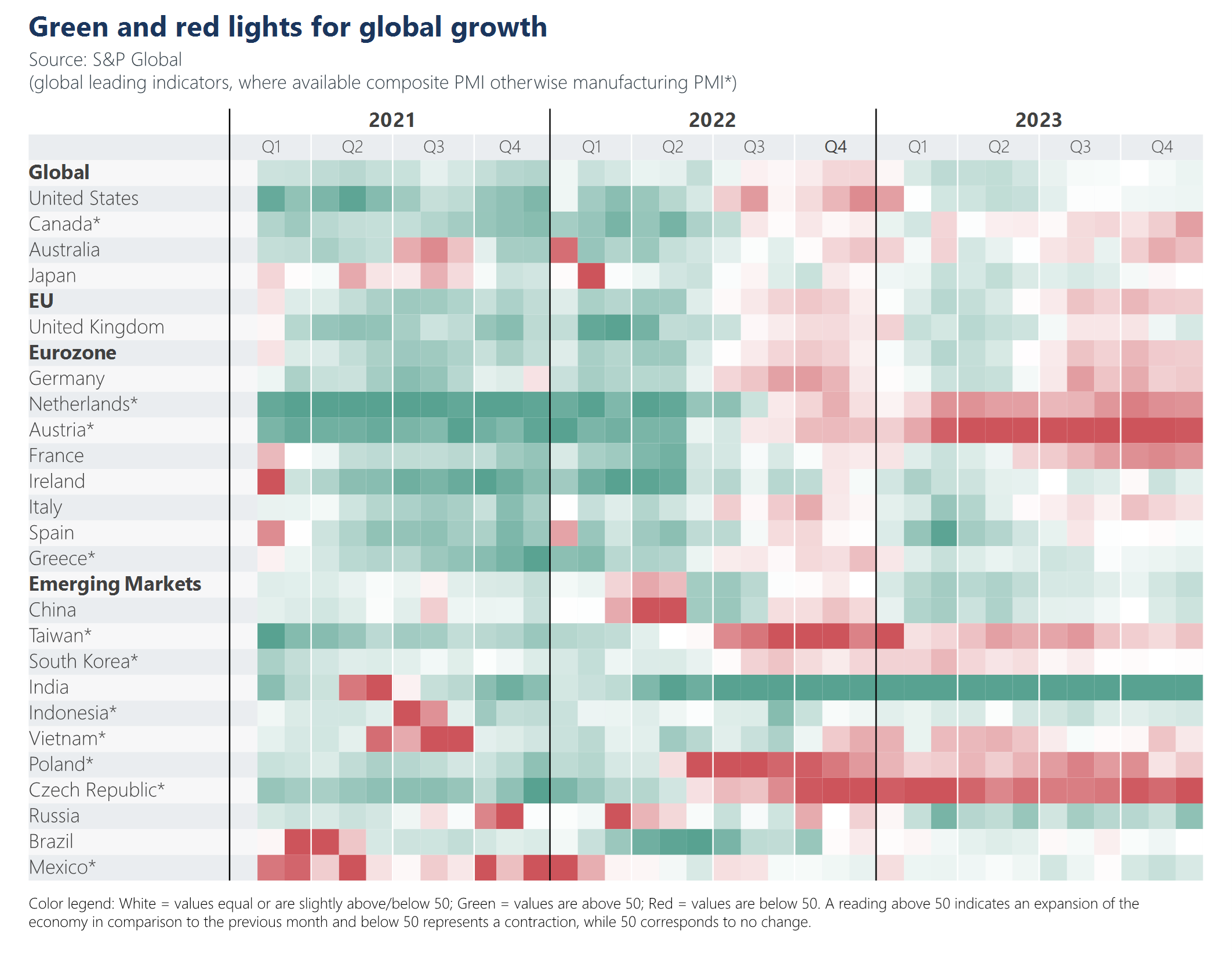

The “heatmap” below shows the evolution of economic growth across the largest economies in the world. GDP growth in 2023 was weaker compared to 2021, particularly in Europe and parts of the emerging world.

Source: Macrobond, AMP

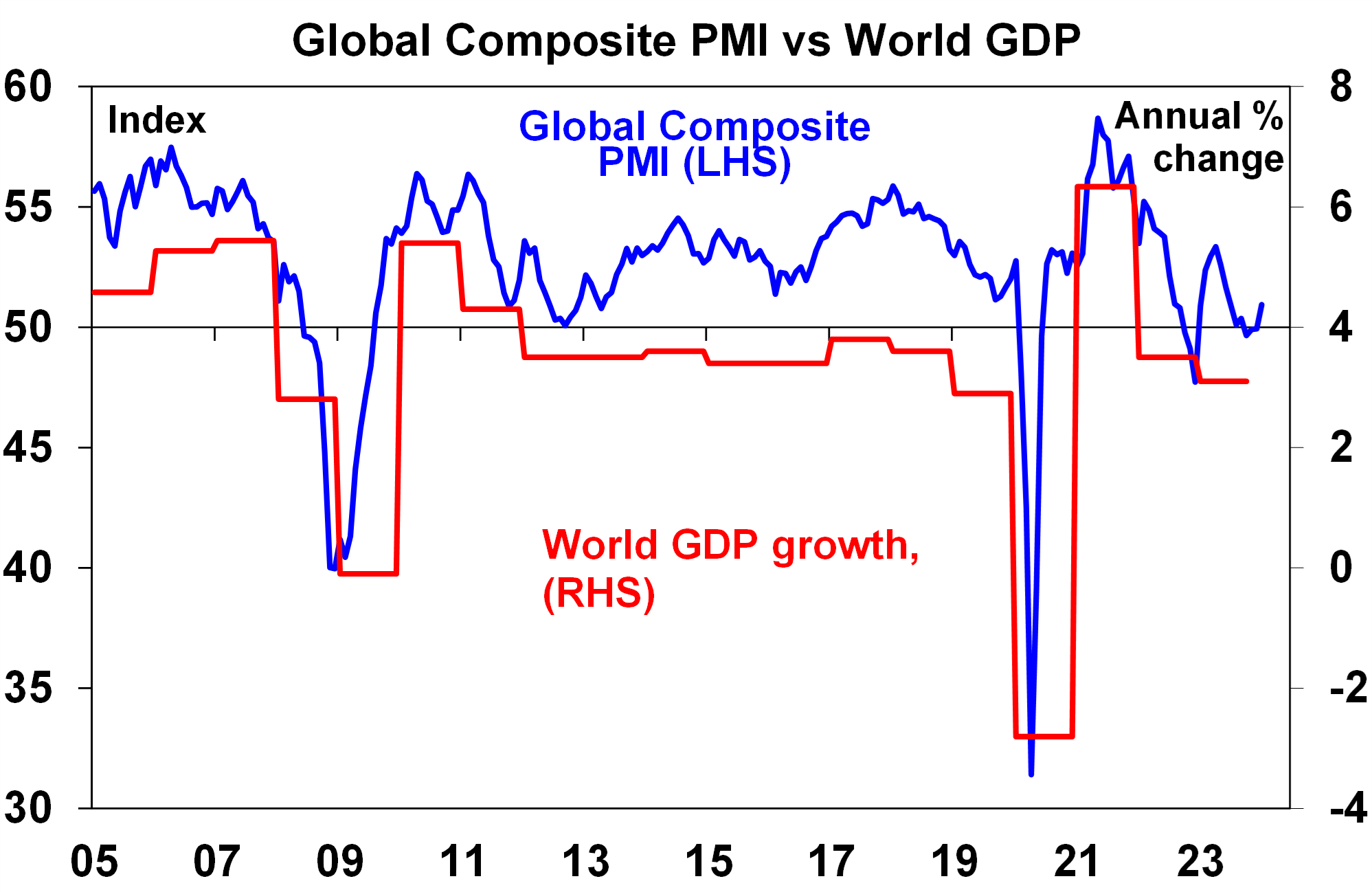

We often reference the Purchasing Managers Indices (or PMIs) as leading indicators of growth across manufacturing and services firms. The composite PMI (with is a weighted average of manufacturing and service conditions) has been trending up again since late 2023 (see the chart below), with better conditions for both manufacturing and service firms, a positive sign for global growth and not in line with a global growth downturn.

Source: Bloomberg, AMP

Will the US remain recession-proof?

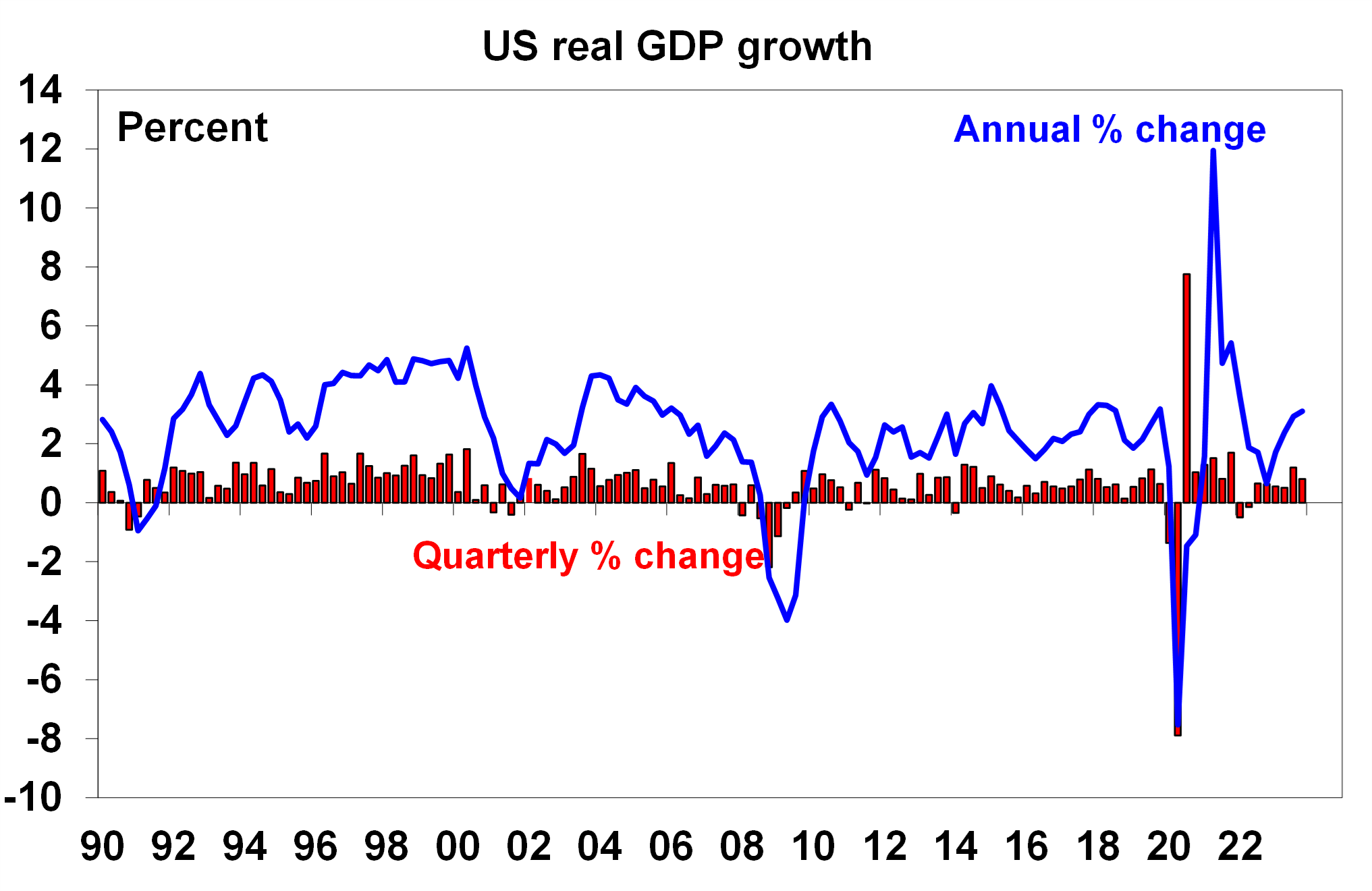

The strength in the US economy is often a barometer for the rest of the world through the demand channel, being the largest economy in the world, and the financial market channel, with many major equity, currency and fixed income markets taking their lead from US markets. The strength in the US economy in 2023 despite the tightening to interest rates since early 2022 was surprising. GDP growth in the December quarter of 2023 was at 3.3% annualised and current expectations for the March quarter this year is tracking at 3.4%. Consumer spending has been the strongest component of growth, with positive contributions from government spending and private business investment while net exports and inventories have detracted from growth.

Source: Bloomberg, AMP

Despite this strength, there is still a moderate chance of a US recession in 2024, according to some leading indicators like the inverted yield curve, ISM new orders, some measures of consumer confidence and lending standards. The labour market is weakening, with job advertisements falling and the unemployment rate ticking up (although it is still low compared to history). Inflation has dropped to 3.1% year on year, and we think it will be at 2.5% by December, as wages growth moderates and helps to reduce services inflation which should allow the US Federal Reserve to cut interest rates by mid-2024. We expect GDP growth to slow to 1.4% over the year to December, well below 2023 levels, but not quite consistent with a recession, which is positive for US earnings growth and the sharemarket.

Eurozone economy to struggle without rate cuts

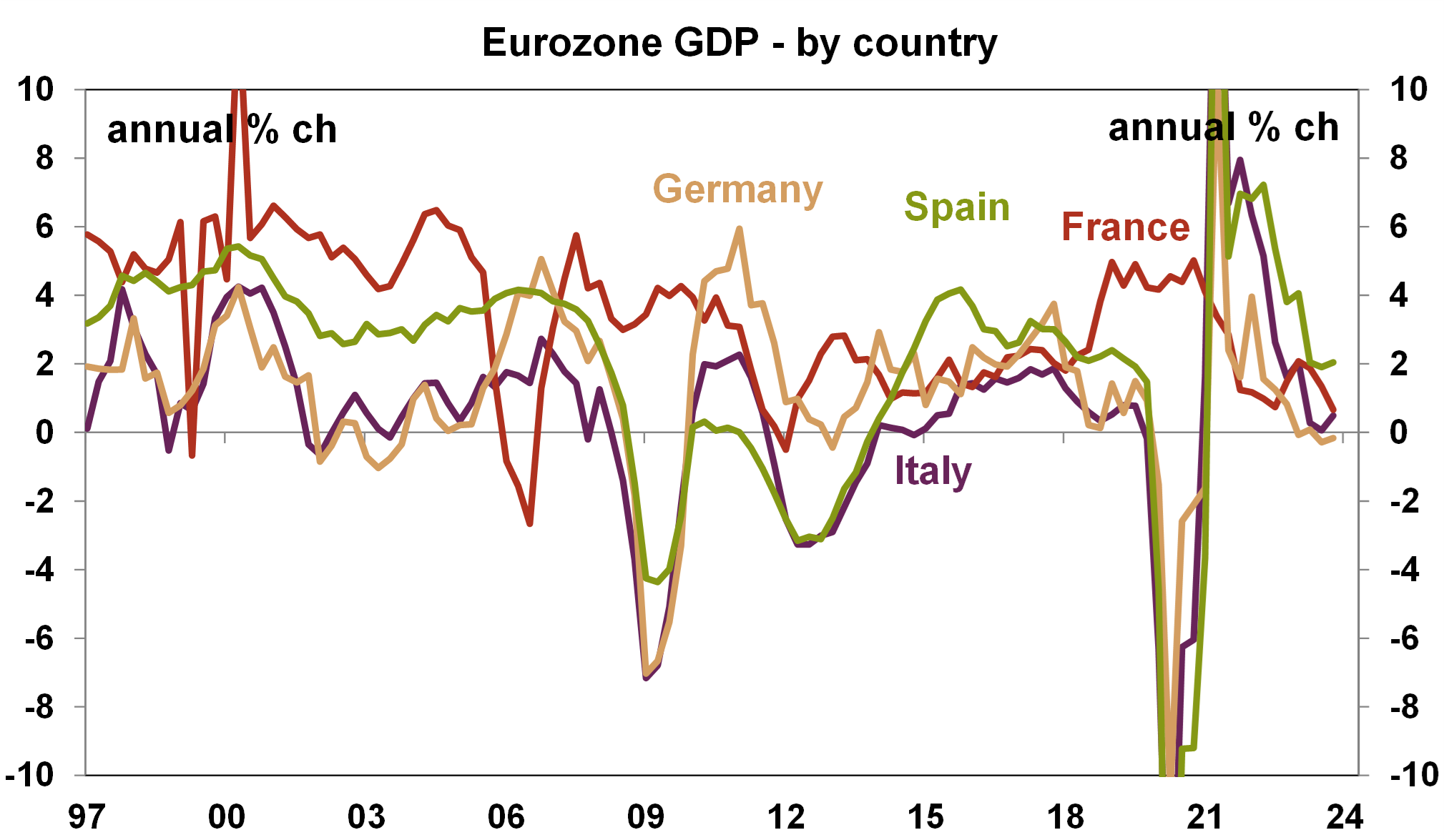

Eurozone GDP growth has barely increased over the past year, with GDP growth ending 2023 at just 0.1% over the year. Weakness is evident across Germany, France and Italy, while Spain is still holding up (see the chart below). Eurozone growth has suffered from the slowing in global manufacturing and lower Chinese imports which has weighed on Eurozone net exports. Inflation has dropped down to 2.8% over the year to January (according to the headline CPI), down from its cyclical high of 10.6% in October 2022. We think the poor growth environment and progress in inflation will see the European Central Bank start to cut interest rates around mid-year, or slightly earlier. An improvement in global manufacturing conditions in 2024 (according to the PMI) and rate cuts should see Eurozone growth at 0.9% in 2024, an improvement from last year.

Source: Reuters, AMP

China needs more stimulus… but it may not get it

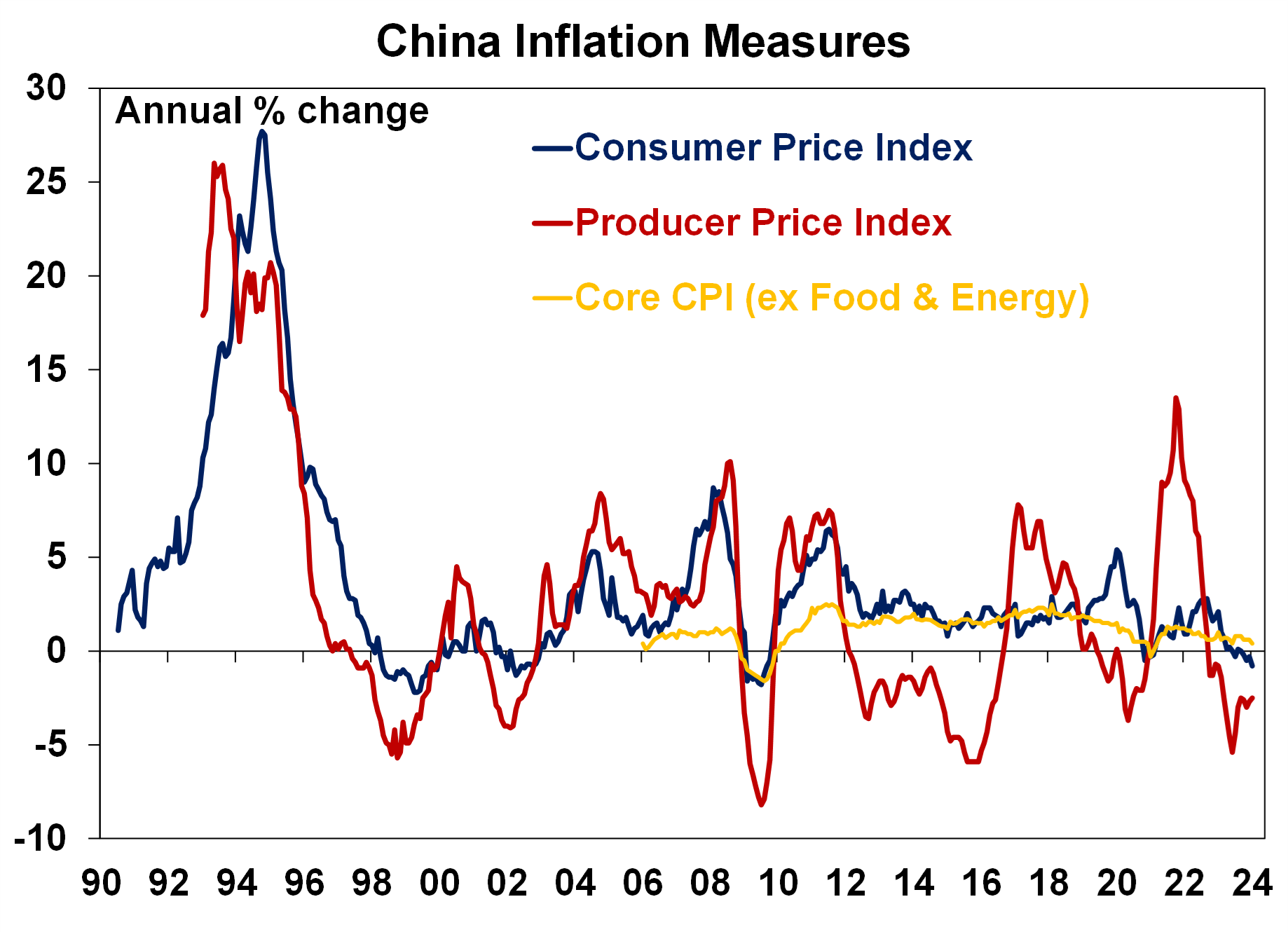

The Chinese economy is facing numerous concurrent growth headwinds. The lengthy COVID-19 lockdowns had a big negative impact on consumer spending (particularly for services) which is yet to fully recover, the property market is dealing with excess housing stock, overinvestment and problems with developers, an aging population has reduced workforce productivity and participation and Chinese shares are down more than 40% since their 2021 highs which is negative for consumer confidence as many Chinese people use the sharemarket as an investment (in the absence of a pension scheme). Reflecting soft growth conditions, China’s consumer prices are in deflation at -0.8% over the year to January (see the chart below) which weighs on corporate earnings, household wages and depresses sentiment.

Source: Bloomberg, AMP

Policymakers have focused stimulus measures on reducing borrowing costs, increasing corporate bond issuance and targeted infrastructure programs. But, without further monetary and fiscal easing (particularly for households to increase confidence and encourage spending rather than saving), Chinese growth will remain subdued. We expect GDP growth of around 4.6% in 2024 and 3% next decade. This is a much lower rate than the world has been used to given that China was growing at ~10% between 2006-10, although given the Chinese economy is now more than twice the size it was back then, there is still a positive and sizeable contribution to global growth and demand for commodities (which is important for Australia).

When will Japan start to tighten monetary policy?

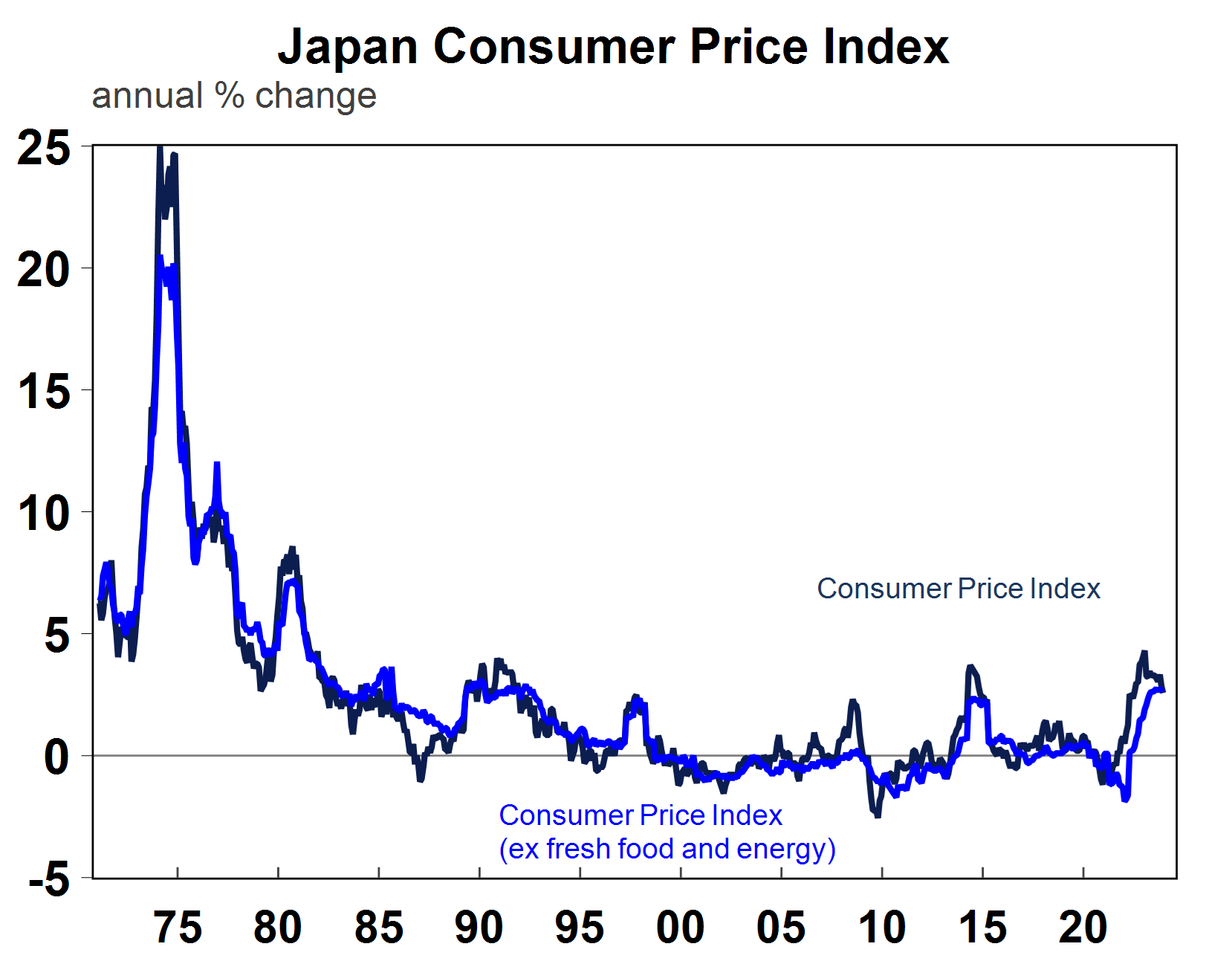

The Bank of Japan is the last major central bank that has not tightened monetary policy in the post-COVID period. The current policy rate is at 0.1%, and interest rates have ranged between -0.1% to 0.5% since the late 1990s. Low interest rates relative to global peers has seen the Japanese yen depreciate by over 30% since 2022. However, the pressure is building on the Bank of Japan to start tightening monetary policy. The Bank of Japan already loosened its yield curve control target on bond yields and the next step will be to fully remove yield control before eventually increasing interest rates. Headline consumer price inflation is running at 2.6% over the year to December 2023 and 2.8% for core inflation (which excludes food and energy). However, Japan’s historical difficulty in lifting and sustaining inflation and inflation expectations and recent poor GDP growth outcomes (which have seen GDP growth fall over the September and December quarters in 2023 meaning a technical recession) means the Bank of Japan will tread carefully in hiking rates and only 10-20 basis points of rate hikes likely this year.

Source: Macrobond, AMP

Implications for investors

2024 is likely to be a year of slower GDP growth around the world, but a global recession is unlikely. This is good news for global earnings and sharemarkets, as a result and we expect global equities to have positive returns in 2024 around 7%. A further decline in global inflation will allow numerous global central banks to start cutting interest rates later this year, which will make way for stronger global growth in 2025.

Geopolitics always matter for investors, but in 2024 this could matter more as around 50% of the global population will have an election. Elections cause uncertainty and potentially change which is likely to see additional volatility in share markets. The US Presidential election in November is a major risk event for both the US and the world, especially because of the potential impacts of the election on US fiscal policy (and how that translates to bond yields) and US trade policy (especially as it relates to China). Geopolitical issues often also cause disruptions to commodity prices and global transport costs, which impact inflation. A second-round lift in inflation or persistent elevated inflation is also a risk for the developed economies in 2024 which would delay the start of central bank interest rate cuts.

Weekly market update 26-07-2024

26 July 2024 | Blog Dr Shane Oliver discusses the risk off as tech hit continues; correction risks into August/September; global rate cutting cycle underway; Australian June quarter CPI to rise but the hurdle to another RBA rate hike should be high; and more. Read more

Oliver's insights - rise of populism and bigger government

24 July 2024 | Blog This article takes a look at the rise of populism and what it means for economic policies and investors. Read more

Weekly market update 19-07-2024

19 July 2024 | Blog This week shares are down; US election/Trump prospects starting to impact; global rates easing cycle on track; China Plenum; Australian jobs still tight but easing so RBA needs to be careful; and more. Read moreWhat you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.