Econosights

The financial literacy gender problem in Australia

In Australia, the gender gap is larger compared to our global peers. We look at this issue in this edition of Econosights.

6 min read

Key points

More than one third of adults in Australia are financially illiterate, with opportunities for improvement. There is also a gender gap in financial literacy in Australia. Women tend to have lower financial literacy than men. In Australia, the gender gap is larger compared to our global peers.

Lower financial literacy results in worse financial outcomes including slower wealth accumulation, poorer investment decisions and lower superannuation savings. There are also social impacts including reduced confidence and less financial freedom.

On top of a financial literacy gap, women also tend to earn less than men in Australia (due to a variety of reasons) which impact superannuation balances (with male superannuation balances exceeding female superannuation balances at every age bracket).

As at 2021, the average female superannuation balance was 21% below a male’s balance at retirement age.

Most of the solutions to the problem revolve around education. Businesses can offer financial well-being as an employee benefit through teaching staff about superannuation. Financial services providers can offer education resources to their customers.

The government has a role to play through in offering financial literacy in school, encouraging higher enrolments (especially for women) into economics and changing policy to pay superannuation during parental leave.

Assisting parents with childcare costs to get more women into the workforce is also critical as time out of the workforce can make substantial differences to retirement savings. And, parents need to teach children about personal finances.

Introduction

There was an interesting piece of research published by Alison Preston and Robert Wright in 2023 in the Economic Record about a gender gap in financial literacy in Australia. We look at this issue in this edition of Econosights.

What is financial literacy and what is the problem in Australia?

Financial literacy is the understanding of financial and economic concepts and the application of them to your personal finances. This ranges from topics around savings accounts, credit cards, mortgages, share trading and superannuation. As expected, financial literacy tends to increase with age, peaking at around middle-age and declining into the older years.

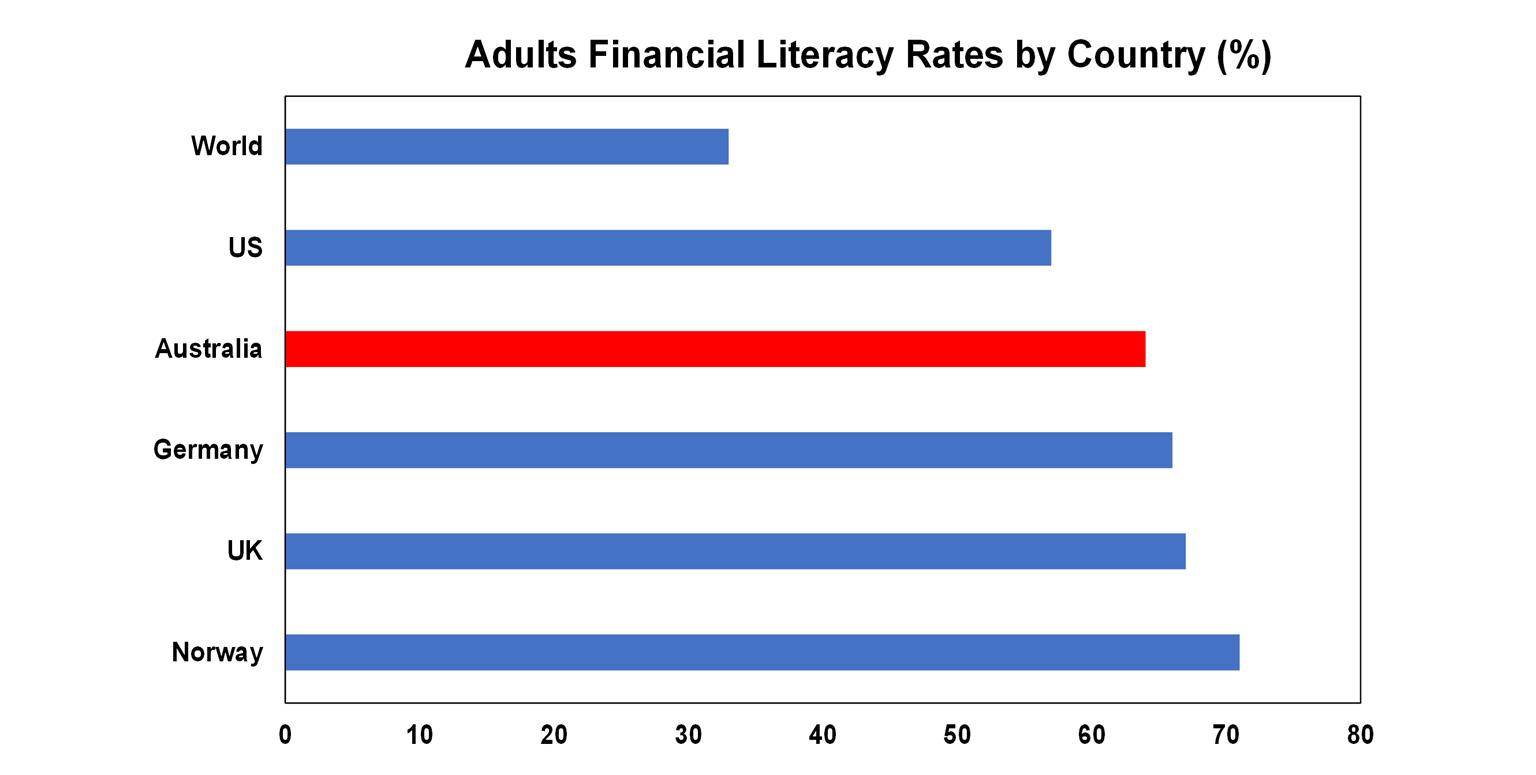

There have been studies to measure financial literacy around the world. In 2014, S&P released a Global Financial Literacy Survey which showed that around 33% of adults are financially literate (by answering simple questions around numeracy, compound interest, inflation and risk diversification). As expected, financial literacy is lower in emerging and developing countries (see the next chart).

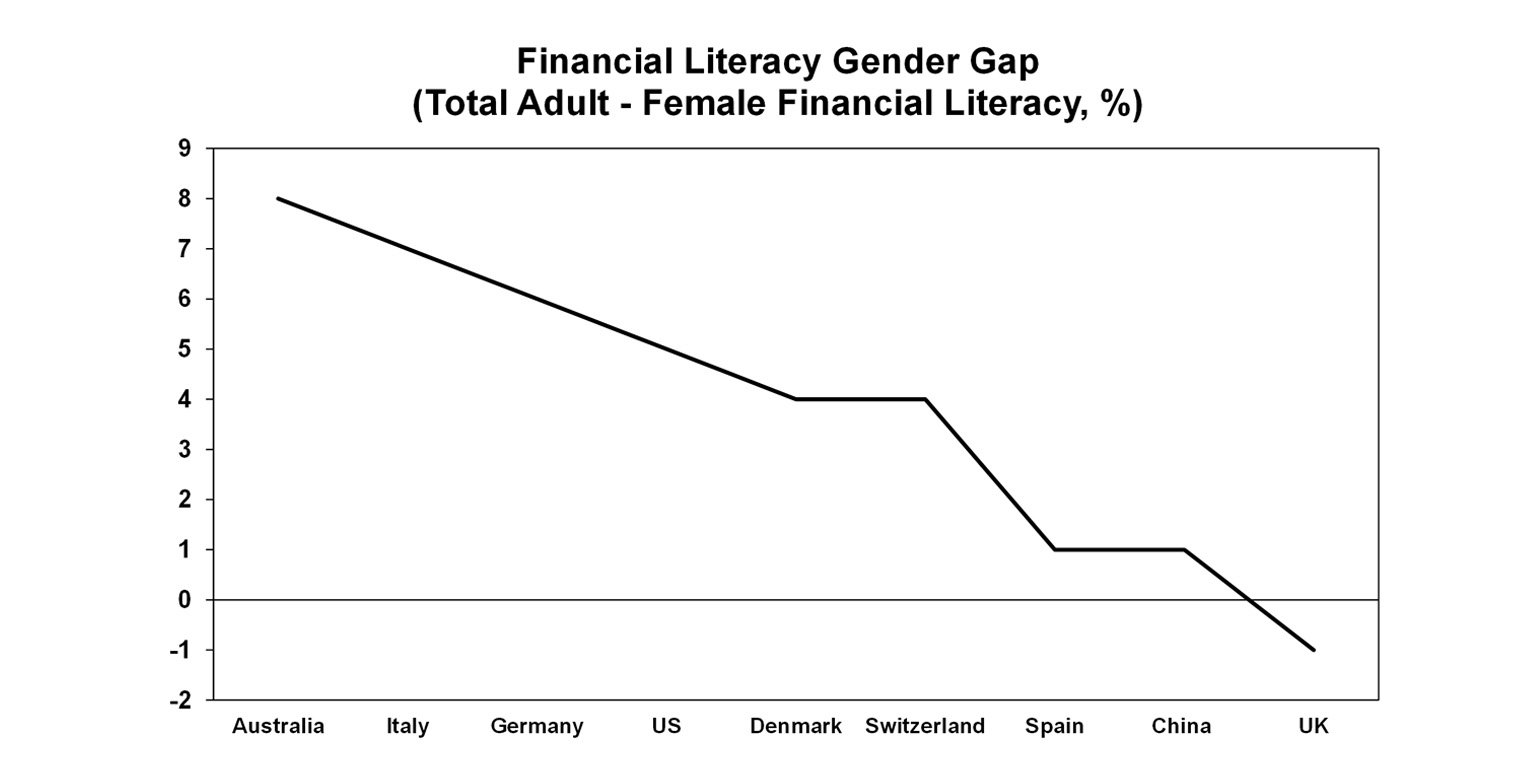

In Australia, 36% of adults are financially illiterate, and globally, women have lower financial literacy compared to men which is known as the “financial literacy gender gap” (which is calculated as the adult literacy rate minus the female literacy rate). However, in Australia, this gap is higher relative to our global peers (see the chart below).

Along with the S&P study about financial literacy, a long-running survey in Australia called the Household, Income and Labour Dynamics survey Australia (HILDA) measured financial literacy in 2018 through 5 simple questions (on similar topics to those asked by S&P) and also found a noticeable gap in financial literacy between men and women. As Preston and Wright note, financial literacy was found to improve with education, employment status and marriage status. They also found a statistically significant relationship between financial literacy and retirement savings.

The implications of a financial literacy gender gap

There are important financial implications of the financial literacy gender gap including poorer investment decisions, lower wealth accumulation and smaller retirement savings. In Australia, average female superannuation balances are below male balances at all ages (see the chart below).

In 2021, the average female superannuation balance around retirement age (at 60-64) was around 21% smaller than a males (at $406K for men versus $321K for women).

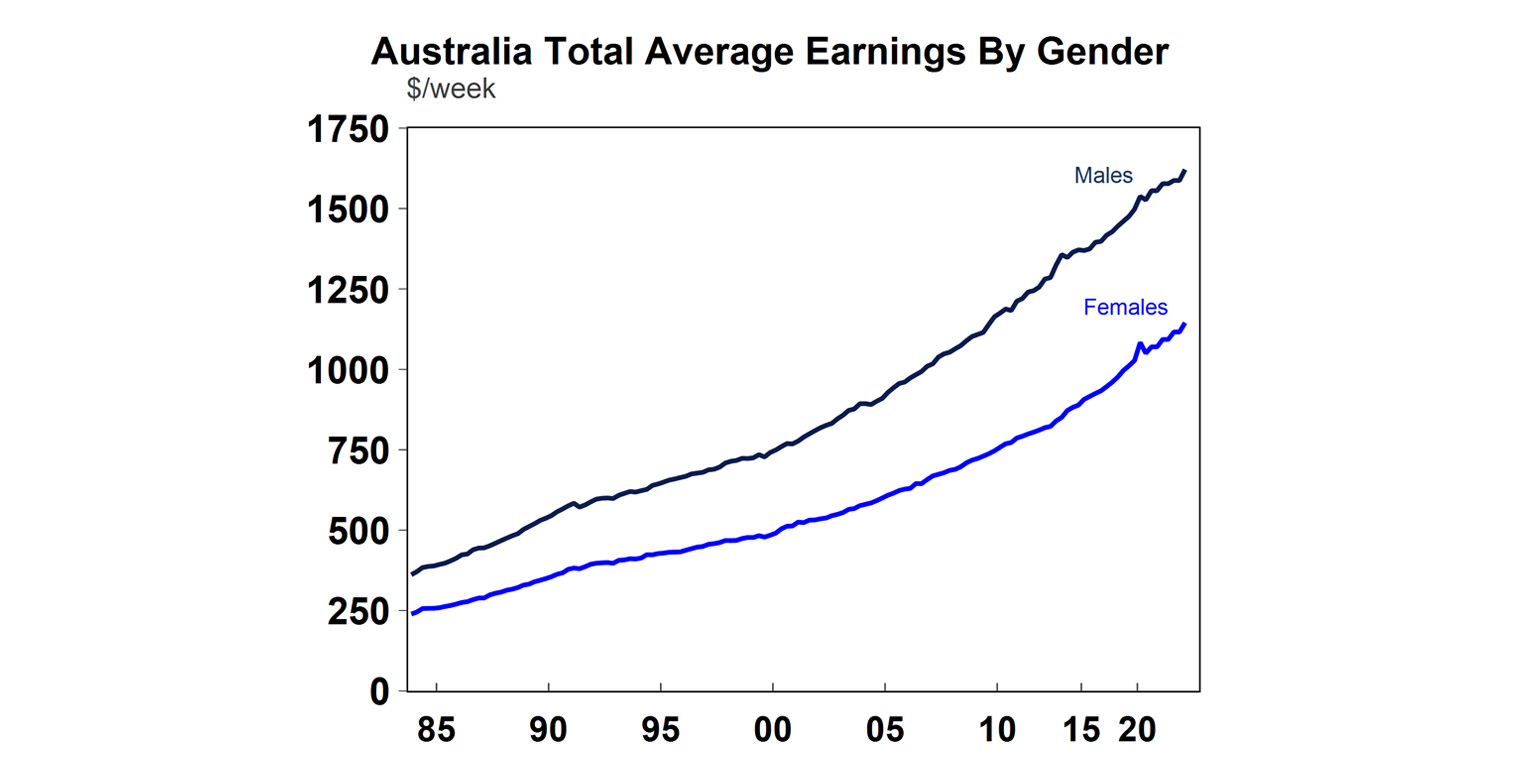

Female superannuation balances start below males from a young age because females (on average) earn less than males (see the chart below). Women take time out of the workforce if they have children, more females than males work part-time (often to look after young children), females tend to choose careers that have lower average earnings and the gender pay gap issue means that for comparable jobs females sometimes earn less than their male counterparts. So, women’s financial positions tend to start off behind men and this issue gets worse through time due to the financial literacy problem.

There are also other personal impacts of lower financial literacy which include things like lower confidence, less financial freedom and poorer living standards.

What can be done about the financial literacy gender gap?

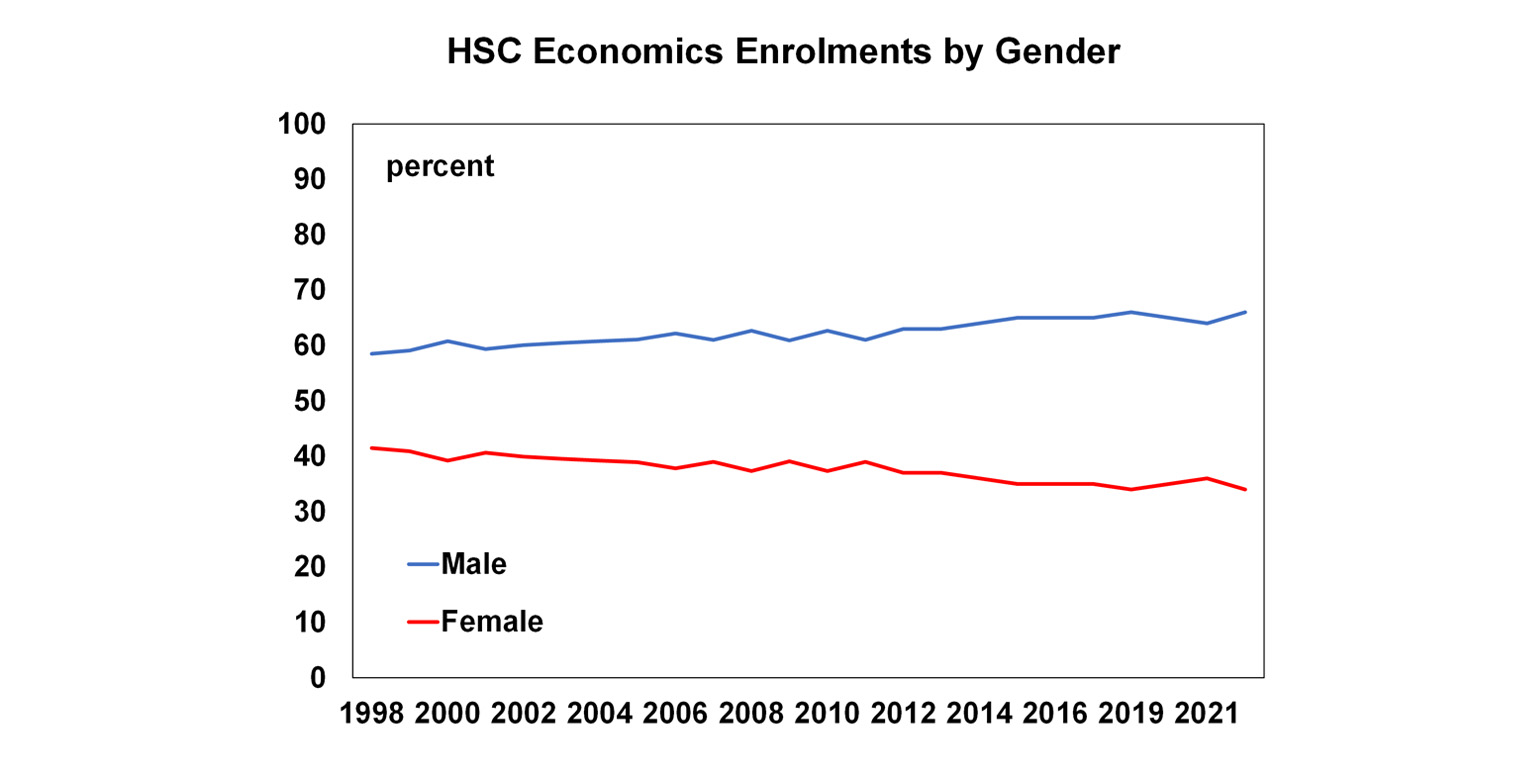

Knowledge is power and the key to alleviating the financial literacy gender gap is to provide more knowledge to women. This knowledge can come from multiple sources. The government has a role to play through offering financial literacy classes in school (which are currently mostly absent), providing better access to financial counselling and encouraging the study of economics in high school and university to females. HSC economics enrolments have been virtually flat over the past 20 years, but males still dominate enrolments and female enrolments have fallen slightly (see the chart below).

Financial services organisations, including banks and superannuation providers should be proactively making education resources available to their customers. And from an employer perspective, financial wellbeing can be offered as an employee benefit, for example encouraging staff to have knowledge about their superannuation. Other staff incentives like salary packaging childcare fees also benefit working parents and employees take this as a consideration in their total remuneration. The Labor government’s recent broadening of paid parental leave to both parents is a step in the right direction but a greater social push for men to take paid parental leave is also needed and take on a greater share of unpaid work around the home. A future policy consideration could also be to pay superannuation when an employee takes paid parental leave. The way compound interest works means that even a short break from work can lead to significant differences in total retirement savings. The Australian female participation rate in the workforce is in the normal range compared to its global peers but it could go higher.

Finally, there is also an onus on parents to teach their children about looking after their personal finances.

Ultimately, financial literacy improves with more knowledge. AMP have a “Simplifying Investing” podcast that educates listeners on the latest and topical issues in economics and the investing world. I highly recommend that you check it out.

You may also like

-

How to protect yourself from phishing and impersonation scams Phishing scams can look like everyday messages – emails, texts or calls. Learn the signs and simple steps to protect your money and personal information. -

Oliver's insights -2025-26 saw lots of noise but strong returns (again) – can it continue? The Iran War and Iran’s effective closure of the Strait of Hormuz disrupting 20% of global oil and gas supplies saw the world oil price initially spike to around $US120/barrel but it was gradually reversed as the world relied on reserves and in anticipation of an interim peace deal which has been agreed but remains shaky. This saw oil prices fall back to near pre-War levels around $US70. -

Weekly market update 19-06-2026 In Australia, the halving of the 32 cents a litre fuel tax cut from 1 July saw average capital city petrol prices rise but only from around $1.53/litre to around $1.62 leaving them still well below where they were before the War started.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.