Insurance

Insurance cover in super

Insurance in your AMP Super is there to support you and your family if something unexpected happens.

Manage your account anytime, anywhere with My AMP

The AMP Bank GO app is now available on your mobile

Or login to

Head to your app store to:

Insurance in super is designed to support you and your loved ones in case of unexpected events such as illness or injury.

AMP Super offers optional insurance in your personal super account.

You can easily add basic levels of insurance when you join AMP Super online with a few simple health and lifestyle questions.

Types of insurance

Also known as death cover, pays a lump sum if you pass away or become terminally ill.

Provides a lump sum benefit if you become permanently disabled or too ill to ever work again.

Pays a monthly benefit if you’re too injured or sick to work.

AMP is proud to partner with TAL to provide insurance to AMP super members. With flexible life stages insurance designed so you only pay for the basic cover you need.

Benefits of insurance cover in super:

Easy to manage

Digital tools help you easily manage your cover via app.

Wellbeing support

Keep on top of your health and wellness with Health Hub.

Compassionate claims

Support services while health experts fast track decisions.

Leading insurance

Insured by TAL, Australia's leading life insurer.

Your Member Statement has the name of the insurer of your plan, or you can contact us to find this out. To apply now, please download and complete the form applicable to the insurer of your plan, then return to us using the reply postal/email address on the last page of the form.

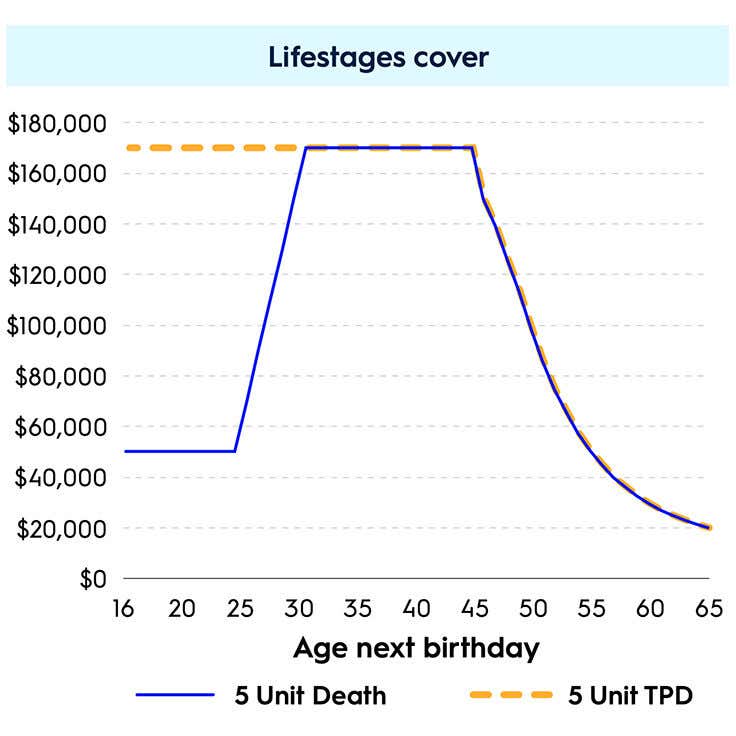

We've partnered with TAL to offer flexible lifestages insurance as part of your super so you only pay for the cover you need.

Lifestages cover automatically adjusts as you get older. Generally, the amount and cost of your cover is lower when you’re younger, increases as you get older and you have more financial responsibilities, then reduces again as you approach retirement.

When joining AMP Super you can apply for a basic level of death & total and permanent disablement (TPD) and income protection (IP) cover. You just need to answer a few short health and lifestyle questions as part of your online application.

Once you've added insurance you can make instant changes to your level of cover as well as making claims using My AMP on the app or web.

You can find out more in our Insurance Guide.

Tailored cover allows you to apply for a tailored amount of death, TPD or IP cover.

The insurer will need to assess your application and you will need to answer questions about your health and lifestyle.

Find out more in our Insurance Guide.

We want you to get super close to your super. That’s why we have a range of advice choices with no extra fees.

From the investment risk profiler to the reitrement needs calculator, you can explore and play out your future today.

AMP MySuper fees are lower than the average super fund1, with consistently strong performance over the long, medium and short term2.

Join AMP Super and add insurance today

Join today and follow the steps to add insurance to your AMP Super account.

1. Complete your personal details including your Tax File Number (optional)

2. You’ll be asked to add lifestages insurance as part of the application process*

3. Complete a few short health and lifestyle questions

4. You’ll know straightaway if you’ve been accepted and get paperwork emailed

* You can only join lifestages insurance as part of the application process, but tailored cover is available at any time.

You can manage your insurance in My AMP. Login to add insurance, make a claim or adjust your existing cover.

Our team of qualified super advisors can provide personal advice about the insurance in your AMP Super account with no extra fees.

We’ve partnered with TAL to launch Health Connect to support our super members through:

to identify risk factors for the most common conditions such as cancer or heart disease

through headlight recommendations to support yout mental health and wellbeing.

Find and connect with registered health practitioners.

We’re delighted to help our members focus on their health and wellbeing. Through Health Connect you’ll get rewarded for taking action

Tools & calculators

Member information

AMP Super refers to SignatureSuper® which is issued by N.M. Superannuation Proprietary Limited ABN 31 008 428 322 AFSL 234654 (NM Super) and is part of the AMP Super Fund (the Fund) ABN 78 421 957 449. NM Super is the trustee of the Fund.

® SignatureSuper is a registered trademark of AMP Limited ABN 49 079 354 519.

Before deciding what’s right for you, it’s important to consider your particular circumstances and read the relevant Product Disclosure Statement and Target Market Determination from AMP at amp.com.au or by calling 131 267.

Read AMP’s Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you.

Any advice and information provided is general in nature, hasn’t taken your circumstances into account, and is provided by AWM Services Pty Ltd ABN 15 139 353 496 AFSL 366121 (AWM Services), which is part of the AMP group (AMP). All information on this website is subject to change without notice.

The super coach session is a super health check and is provided by AWM Services. It is general advice conversation only. It does not consider your personal circumstances.

The Super Projection is provided by AWM Services to eligible members of the AMP Super Fund.

Simple Super (Intrafund) advice is provided by AWM Services Limited (AWM Services) ABN 15 139 353 496, AFS Licence No. 366121 (AWMS) to eligible members of the AMP Super Fund. AWM Services is a wholly-owned subsidiary of AMP. This service may not be offered where it is deemed it is not within the scope of the service or your best interest.

Issued by SuperRatings Pty Ltd (SuperRatings) ABN: 95 100 192 283 a Corporate Authorised Representative (CAR No.1309956) of Lonsec Research Pty Ltd ABN 11 151 658 561, AFSL No. 421445 (Lonsec Research). Ratings are general advice only and have been prepared without taking account of your objectives, financial situation or needs. Consider your personal circumstances, read the product disclosure statement and seek independent financial advice before investing. The rating is not a recommendation to purchase, sell or hold any product. Past performance information is not indicative of future performance. Ratings are subject to change without notice and SuperRatings assumes no obligation to update. SuperRatings use proprietary criteria to determine awards and ratings and may receive a fee for the use of its ratings and awards. Visit superratings.com.au for ratings information. © 2023 SuperRatings. All rights reserved.

Terms, conditions and footnotes

1Based on the simple average of total administration and investment fees and costs across all AMP MySuper Lifestages options (Capital Stable, 1950s, 1960s, 1970s, 1980s, 1990s Plus). Compared against the simple average of all super funds’ MySuper options included in the Chant West Super Fund Fee Survey March 2026 at balances of $50,000 to $750,000.

2The “MySuper – Growth Median” is taken from the Chant West Super Fund Performance Survey May 2026, being the median of all options contained in the MySuper – Growth table with a growth asset allocation of between 61-80%. AMP MySuper 1970s (our biggest MySuper option), 1980s, and 1990s Plus, have higher allocations to growth assets (approximately 90%) than other super funds’ MySuper options. Past performance is not a reliable indicator of future performance.