For decades, Australians have associated wealth with home ownership. As our country has become more diverse and inclusive, and individual Australians achieve greater freedoms, these ideas are changing.

A recent study1 by AMP highlights how our definition of ‘wealthy’ is shifting – and how your bank, super fund and adviser can help you achieve wealth, no matter what that means to you.

Home ownership and financial security

Historically, home ownership in Australia was seen as a pathway to financial security and stability. Prior to WWI, almost half of the country’s housing stock was owned either outright or through a mortgage. This figure grew through the ‘40s and ‘50s, driven in large part by people’s memories of the financial turmoil endured through the wars and the Great Depression.

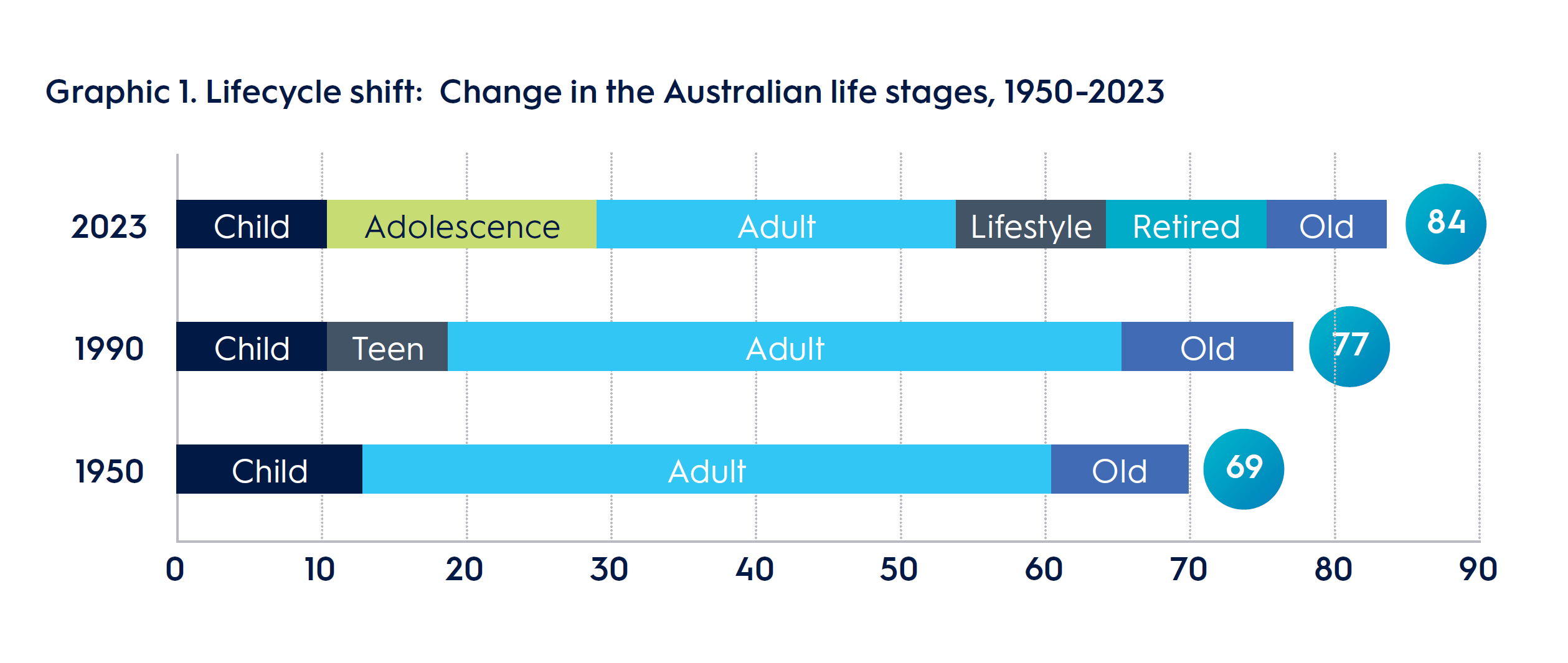

By 1966, home ownership had reached a peak of 73%. In the years that followed, however, Australia saw significant social and demographic change which altered our relationship with home ownership. These included:

- Longer life expectancy

- Fewer people in their 20s marrying or starting

families - Parents choosing to have fewer children

- Greater average individual wealth thanks to globalisation

- Greater migration

- Larger workforce participation

By 1986 – just 20 years after the ’66 peak – home ownership had fallen to 67%.

Retirement, home ownership, and ‘FORO’

Until the 1970s, few Australians gave much thought to retirement planning. Life expectancy was lower and most people typically only needed to make their money last for five years after leaving the workforce. As a result, the stability afforded by home ownership was often enough to act as a substitute for a real retirement plan.

Increasing life expectancy – now more than 80 years – means this is no longer a viable option. Today’s retirees can expect to live another 25 years after retiring. In response, the Australian Government introduced compulsory superannuation payments in 1992 to assure working Australians of a level of dignity and independence in retirement.

Source: ABS, The Demographics Group

Changing Australian life stages, 1950 – 2023

While at first Australians assumed this would be enough, more recently a ‘fear of running out’ (FORO) has begun to emerge, with women and single parents especially worried.

Common causes of FORO include:

- Longer life expectancy

- Rising living costs eroding the value of savings

- Super losses incurred by taking out savings during the COVID pandemic

The new ‘wealthy’ – and how advisers are helping

With Australians living longer, waiting to start families and increasingly concerned about running out of money in retirement, it’s understandable that our ideas around wealth have shifted.

Fifty years ago, asking someone what it meant to be wealthy would likely be met with the same response each time: owning their own home.

In the 2020s, our diverse lifestyles have led to an equally diverse understanding of what it means to be wealthy. The concept of wealth has shifted away from an exclusive focus on retirement savings to reflect a holistic sense of security, wellbeing and happiness for our entire lives.

It includes:

- Financial independence

- Having contentment

- Being in good health

- Being close to family

- Having the freedom to make choices

- Having time to do things for ourselves and others

- The absence of stress

- Being educated and being able to educate our children

- Having the ability to help and care for others

- Having a supportive social circle

- Having a sense of success in life

For some, ‘wealthy’ may still include home ownership, but it doesn’t have to. Instead, being wealthy could mean going on regular holidays, buying a rare collectible or having the financial security to chase personal dreams.

AMP is now offering digital mortgages which will enable borrowers to apply for a loan or refinance within 20 minutes, providing greater freedom and flexibility around home ownership. Find out more >

Explore how AMP can help you achieve whatever wealthy you want >

1 – What Wealthy means for Australians in 2023, an exploration of cultural preferences and change, AMP, The Demographics Group

How to maximise your 2024 tax refund

18 July 2024 | Finance 101 With tax time nearly upon us, you might be interested in the following tips, which may help to increase the amount of money you get back. Read more

Tax time checklist for property investors

17 June 2024 | Blog If you have an investment property, here are some tips to help you prepare at tax time Read more

8 tips to get a harder-working home loan

14 June 2024 | Blog There are many ways you can get your home loan to work harder – from setting up an offset account to reduce the interest you pay, to consolidating your debt. No matter what package you have, you can take control of your repayments and build your financial resilience. Read moreWhat you need to know

The credit provider for all banking products is AMP Bank Limited ABN 15 081 596 009, AFSL and Australian Credit Licence 234517. Approval is subject to AMP Bank guidelines. Terms and conditions apply and are available at amp.com.au/bankterms or by calling 13 30 30. Fees and charges are payable.

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account.

It’s important to consider your particular circumstances and read the relevant product disclosure statement, Target Market Determination or terms and conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy.

All information on this website is subject to change without notice. AWM Services is part of the AMP group.