Weekly market update

Investment markets and key developments

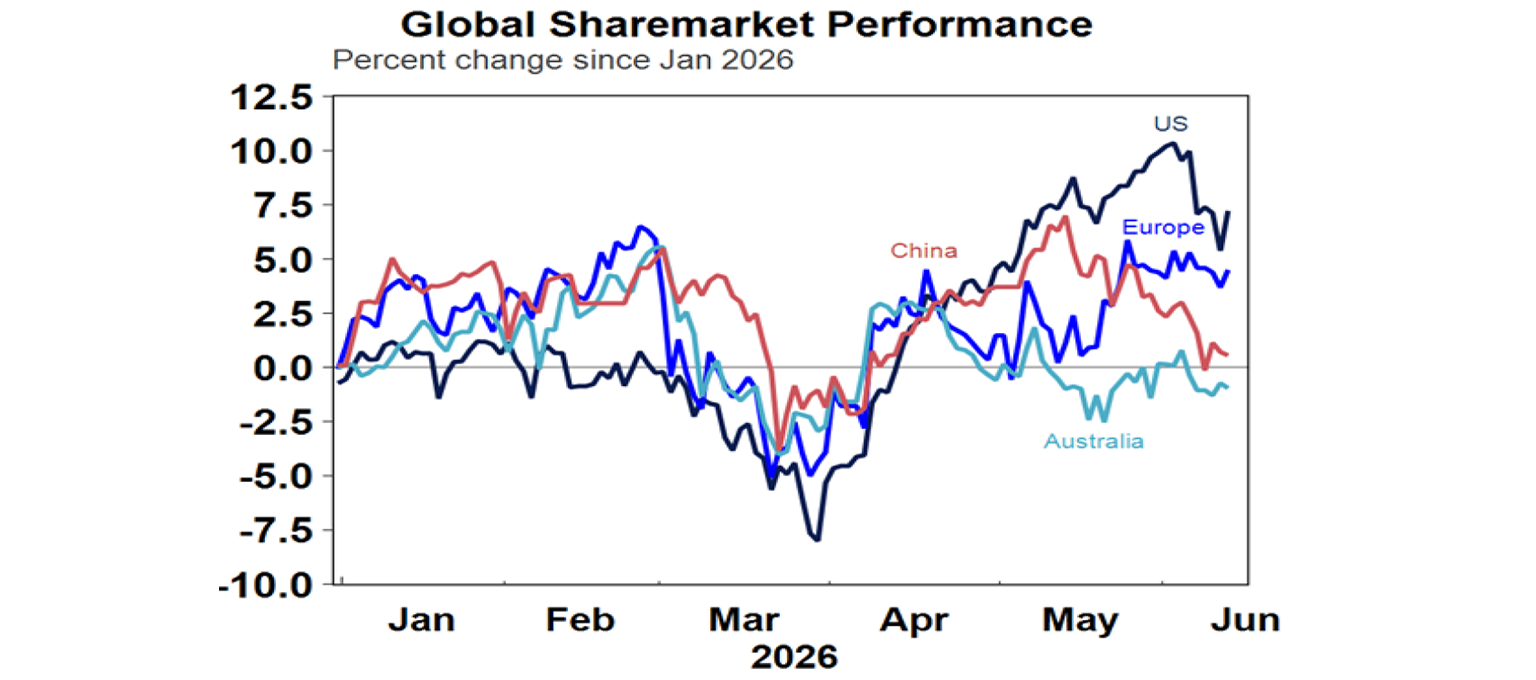

For the past week this left global share markets mixed – up 0.6% in the US and up 2.1% in the Eurozone but down 0.9% in Japan and down 0.8% in China. Australian shares rose a solid 2.1% for the week having proven more resilient in the face of US weakness mid-week and possibly getting a boost from talk that the RBA may be at or close to the top on interest rates.

8 min read

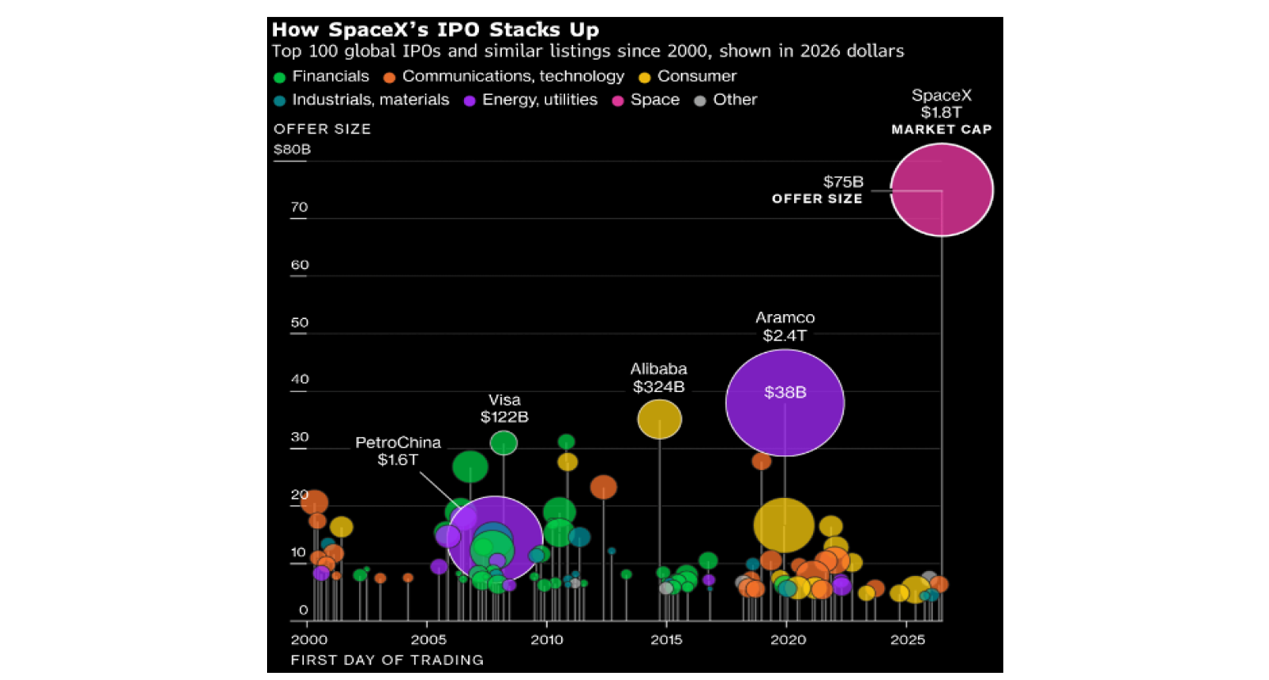

A US/Iran deal on the way (again) and SpaceX takes off to infinity and beyond. The past week saw another round of gyrations regarding whether there will be a US/Iran deal to end the war and reopen the Strait of Hormuz or not driving volatility in investment markets along with mixed US inflation data and the SpaceX intial public offering raising $US75bn, which is the biggest ever IPO. Around mid week shares were under pressure as missile exchanges with Iran ramped up to their highest since the ceasefire started as Trump said he will hit Iran “very hard”, driving oil prices up again. But on Thursday shares spiked as Trump (yet again) said a deal may be signed “in coming days” with tech stocks also buoyed by the successful SpaceX IPO. Optimism of a deal got a further boost on Friday with a Trump administration official saying there was an 80-85% chance of a deal soon with Iran’s foreign minister saying a deal has “never been closer”.

For the past week this left global share markets mixed – up 0.6% in the US and up 2.1% in the Eurozone but down 0.9% in Japan and down 0.8% in China. Australian shares rose a solid 2.1% for the week having proven more resilient in the face of US weakness mid-week and possibly getting a boost from talk that the RBA may be at or close to the top on interest rates. Gains on the ASX were led by consumer, property, health and industrial shares. Despite the bounce in the last week, Australian shares remain relative underperformers so far this year as RBA rate hikes, worries about the impact of the Iran war and Budget tax changes have impacted.

We continue to see shares overall providing positive returns this year but expect more volatility. The combination of sticky inflation – not helped by the oil supply shock and AI boom related demand, an upwards drift in central bank interest rates, flagging consumer demand, worries about an AI bubble, huge US IPOs (with $US200bn from SpaceX, Anthropic and OpenAI alone as against only $US77bn raised in the US for the whole of last year), and political uncertainty around the US mid-terms are likely to continue to result in a volatile ride.

Surging capital raising via IPOs are a mixed blessing for shares. On the one hand they add to hype around the market with many wanting to get on board. On the other they suck cash out of the market which can be a drag for future gains. I wouldn’t rely on them as a timing indicator though.

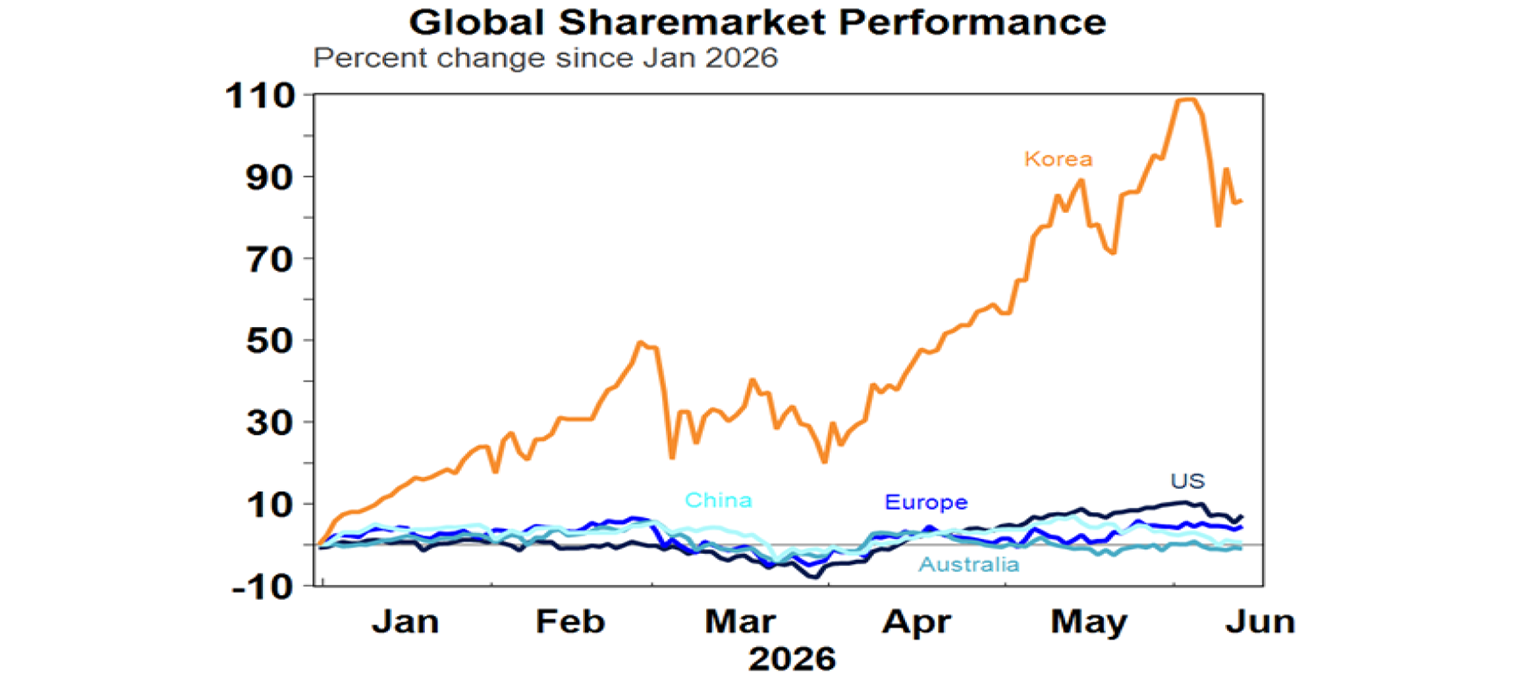

A 10% or so plunge in Korean shares earlier in the week caught a lot of attention. This just looks like a correction after a doubling year to date on the back of booming AI semiconductor demand. Such falls are not unusual after big run ups, but with Korean share valuations still cheap – with a forward PE of 7-8 times – and super strong earnings growth it may have further to go yet assuming the AI boom itself has further to run. The rise could be volatile though.

Bond yields were flat to down helped by news of another Iran deal. Gold and iron ore prices fell but metal prices rose and Bitcoin rose too continuing to bounce around its February low. The $US fell but the $A was little changed around $US0.704.

Trump’s latest claim that a deal is imminent could yet again come to nothing. Iran has proven far more resilient to US pressure than Trump seemed to expect, and it could yet string things out further given sticking points around its desire to toll ships through the Strait, it’s enriched uranium, it’s frozen assets, sanctions & Lebanon. That said Trump remains under intense political pressure with the mid-term elections approaching to find a way to dress up a deal sooner rather than later and both sides in the recent re-escalation of fighting appeared to be holding their punches with the aim of leaving room for negotiations. So, our base case remains that a deal will be reached leading to a reopening of the Strait.

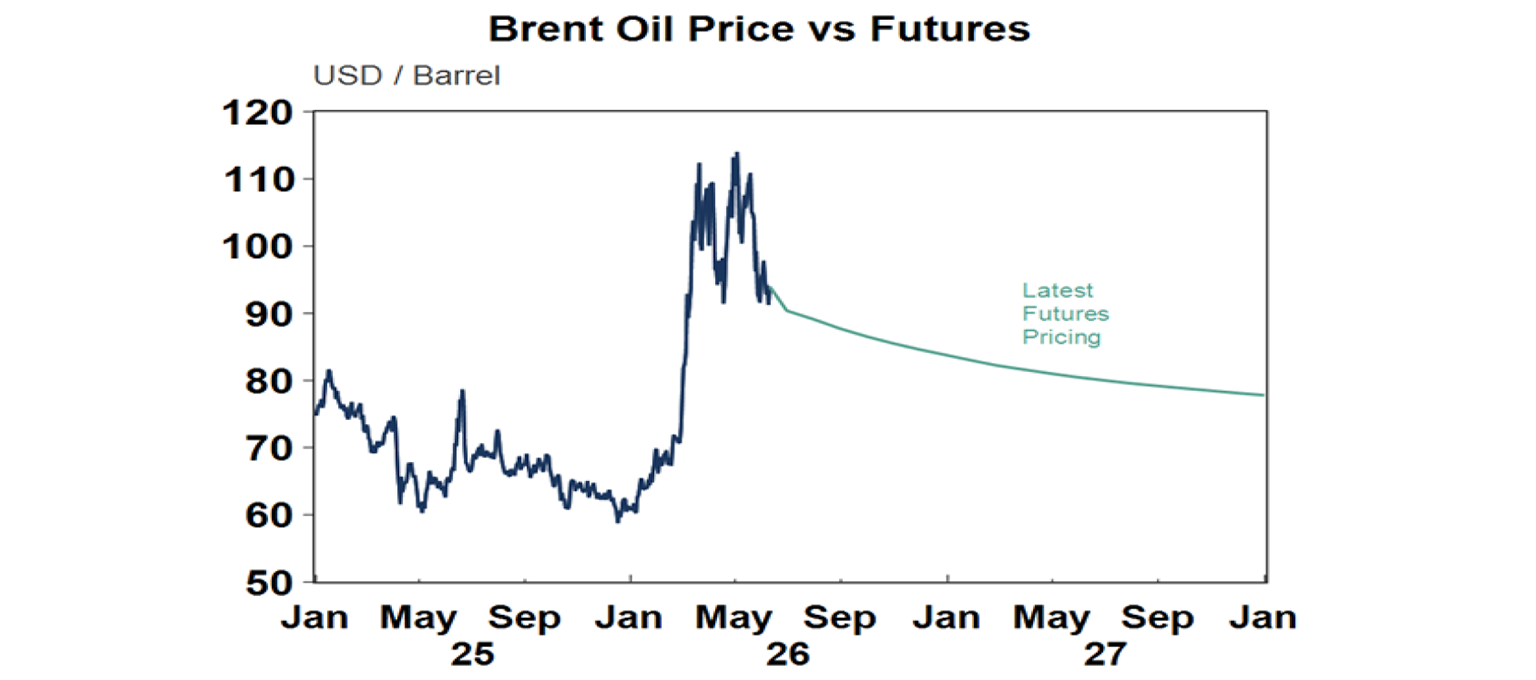

Renewed optimism for a deal on the back of Trump’s latest claims have pushed oil prices to the low end of the range they have been in since the War started, with oil futures tracing out a gradual decline into next year. This appears reasonable as in the short term it will take a while for oil production to return to normal and the oil market will price in a risk premium for a while, particularly if any deal does not resolve Iran’s nuclear ambitions, what to do with its enriched uranium and its desire to toll the Strait. That said past oil price shocks have eventually been followed by a big fall in prices as higher oil prices encourage more supply and kill more oil demand and this time is unlikely to be any different – especially with EV demand now going through the roof (even from me!). Of course, if a deal is not soon reached it will pose a major risk to markets. While the US has been helping ships get through the Strait, with Trump taking of 100 million barrels of oil through the Strait in recent weeks this is well below the normal flow of 600 million barrels a month. So far, the world has been able to get by through the 12-13% cut to global oil production by running down reserves but there is a limit to that.

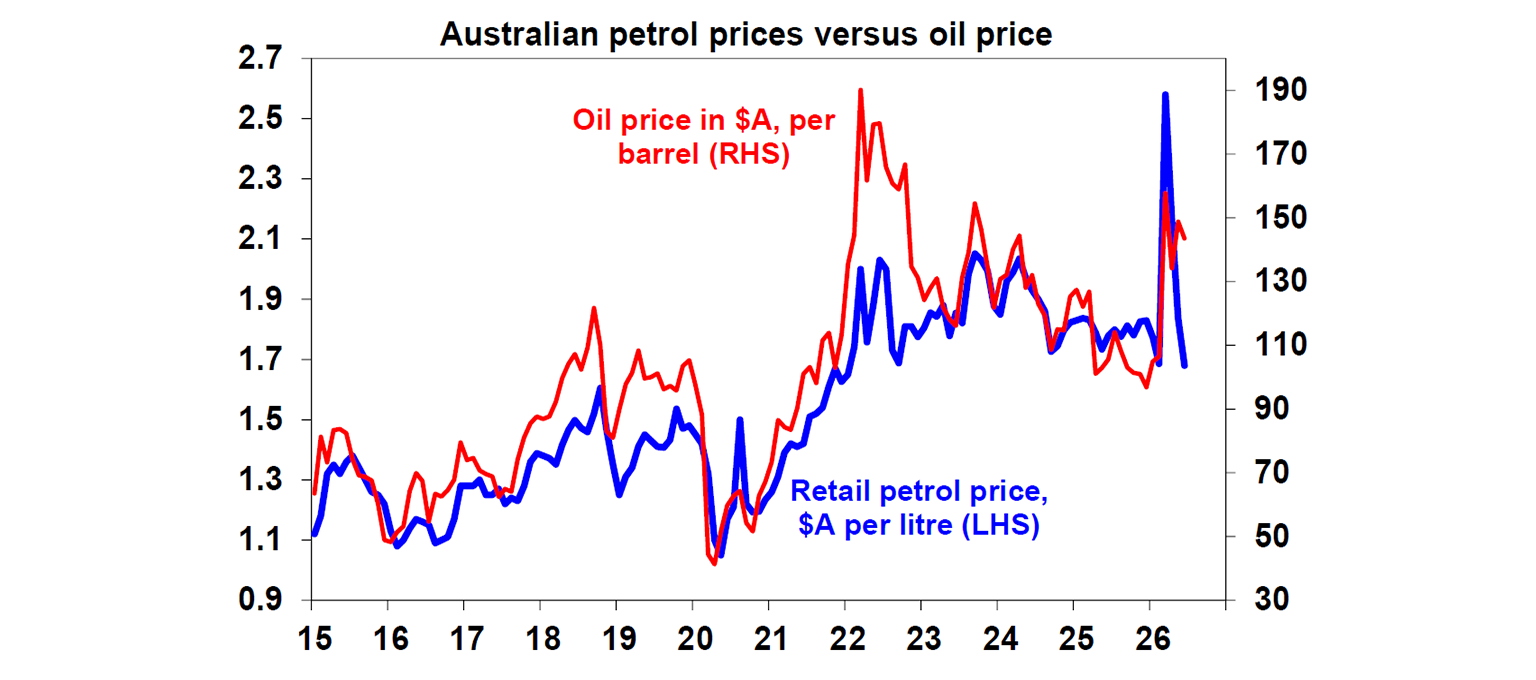

A deal to end the War and reopen the Strait of Hormuz may not necessarily lead to a further fall in Australian petrol prices just yet. At around $1.68 a litre they are currently around where they were before the War started! This is partly due to the $0.32 fuel tax reduction that is scheduled to end at the end of the month, implying a rebound to around $2 a litre which is just below what current oil prices and the $A imply they should be. Thereafter a gradual return to normal in global fuel markets would imply a gradual fall in petrol prices but they may still end the year above current levels. Unless of course the fuel tax cuts (costing $2.55bn each three months) are extended.

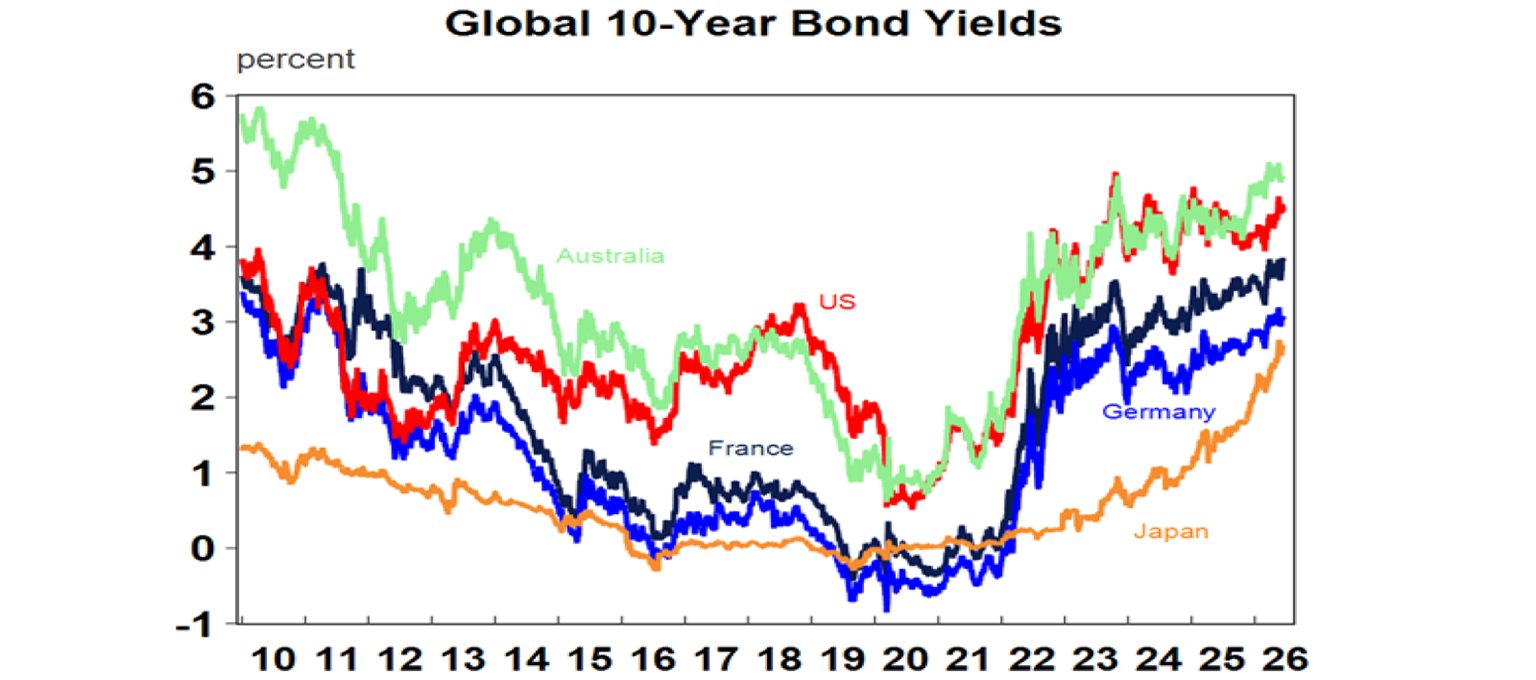

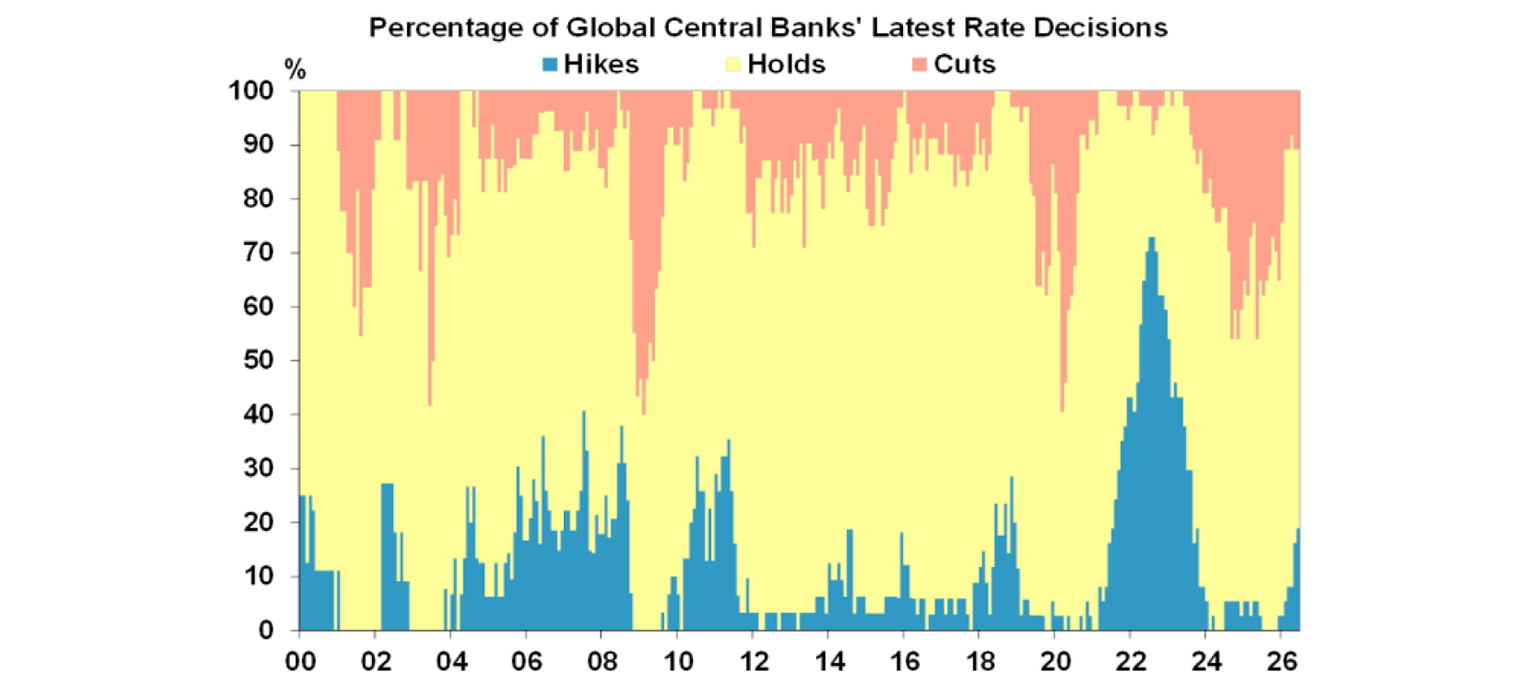

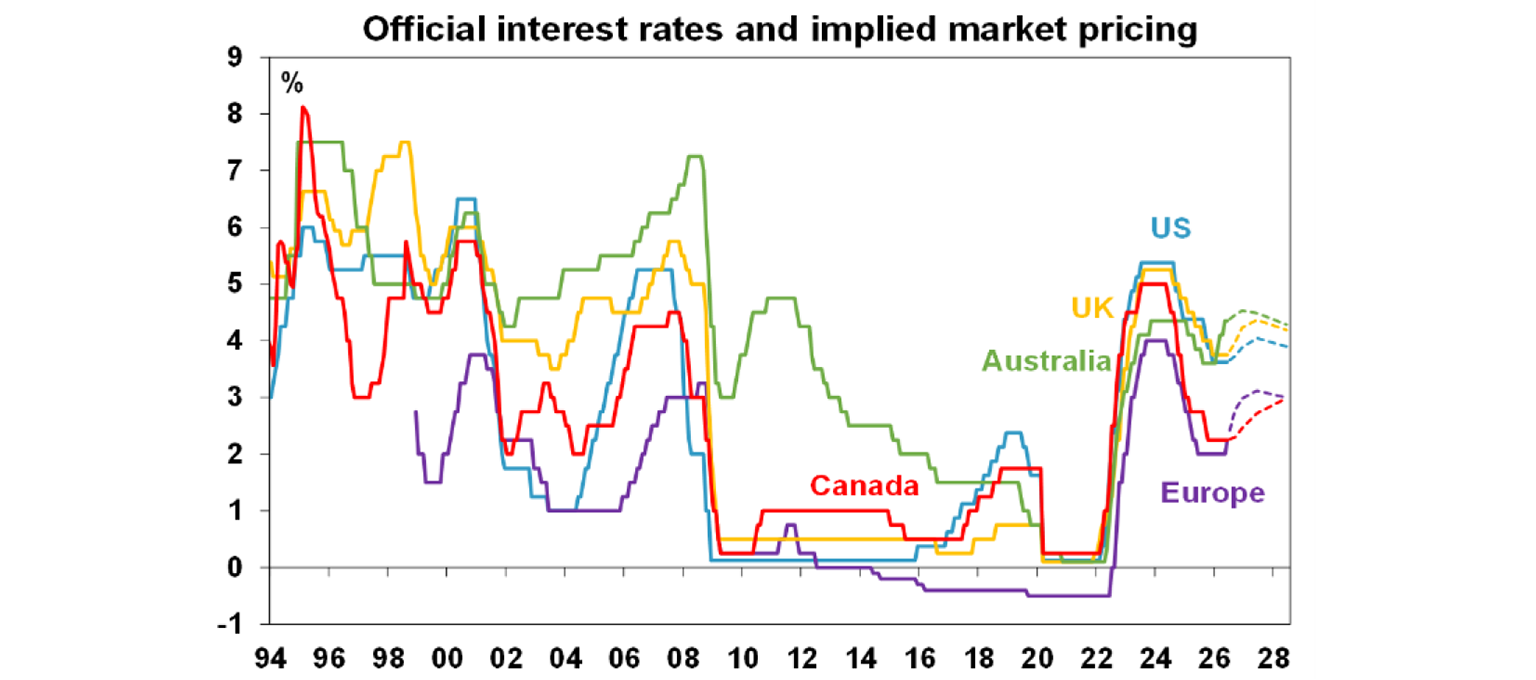

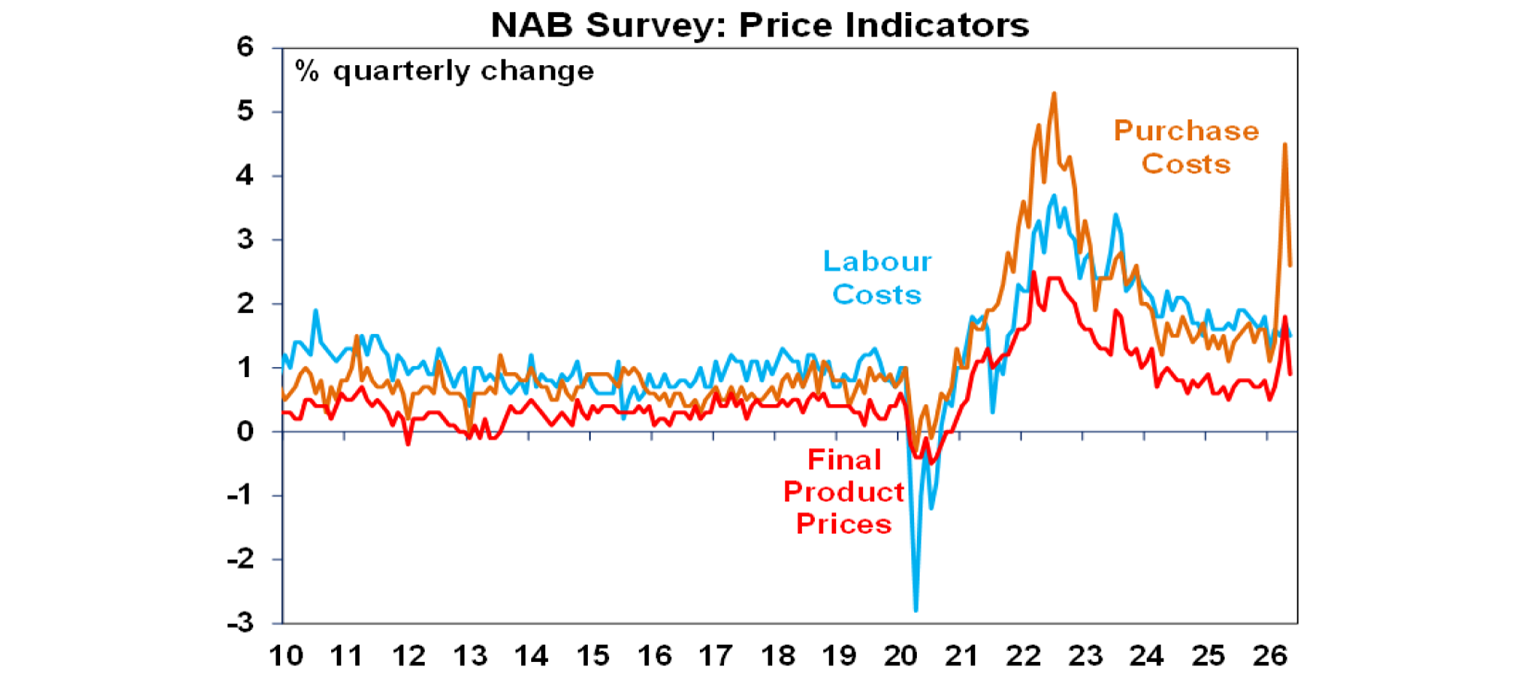

The past week also saw a continued drift towards higher interest rates by central banks. While the Bank of Canada left rates on hold, the European Central Bank hiked rates by 0.25% taking them to 2.25% with its commentary reinforcing expectations for more rate hikes ahead and the Bank of Indonesia raised rates for a second month in a row. The drift towards higher rates can be seen in the next chart.

US inflation likely keeps the Fed on hold for now but a hike later this year remains a high risk. CPI inflation rose further to 4.2% in May on the back of higher energy prices, and core CPI inflation also rose further to 2.9%yoy. The rise in core inflation was fractionally less than expected helped by softer readings in goods prices and likely leaves the Fed on hold in the week ahead. But elevated services inflation, the rising trend in core inflation with the AI boom stacking on top of the tariffs and the oil shock in adding to costs and core PCE inflation looking likely to come in around 3.4%yoy for May after hot components in the producer price index leaves the risk of a Fed rate hike later this year high.

The US money market is pricing in around an 80% chance of a rate hike by year end. Note that the ECB appears more hawkish than the Fed because of a lower starting point for interest rates and a greater exposure to the energy shock.

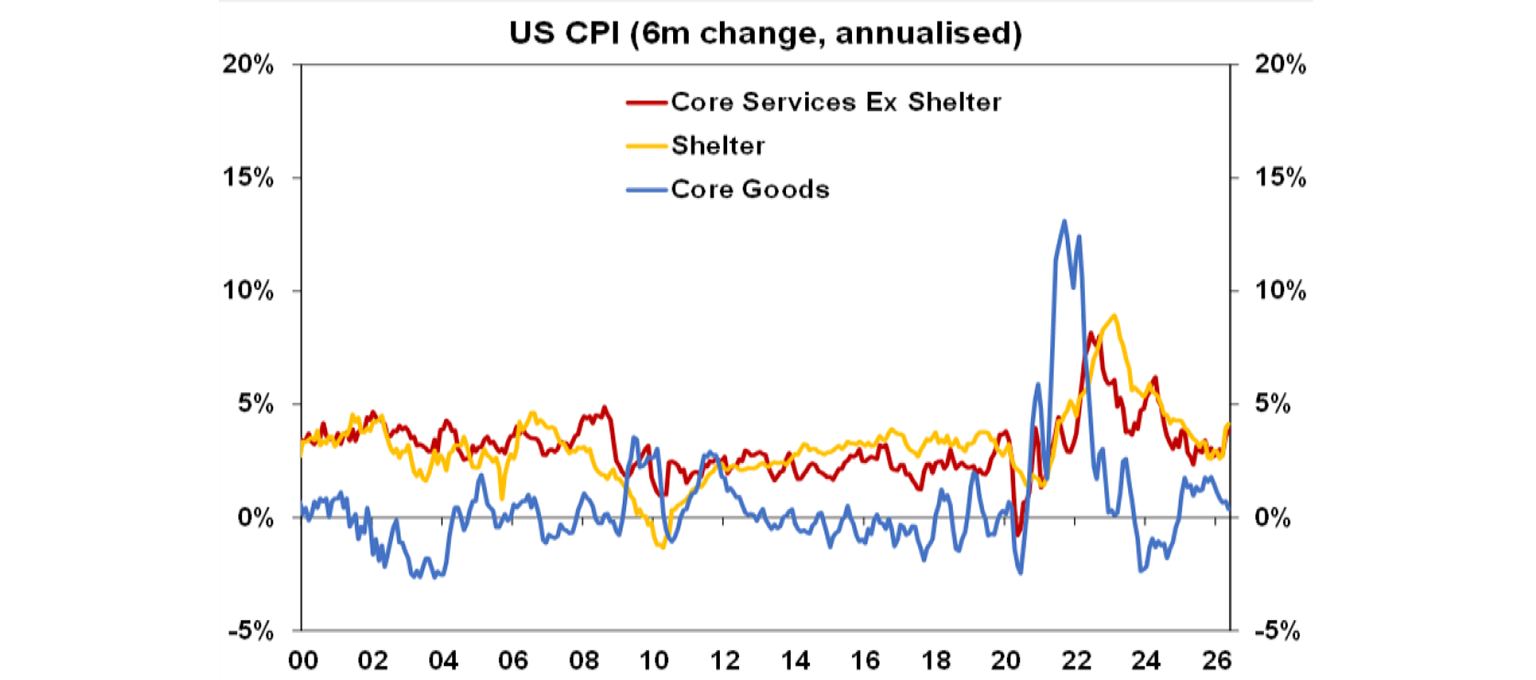

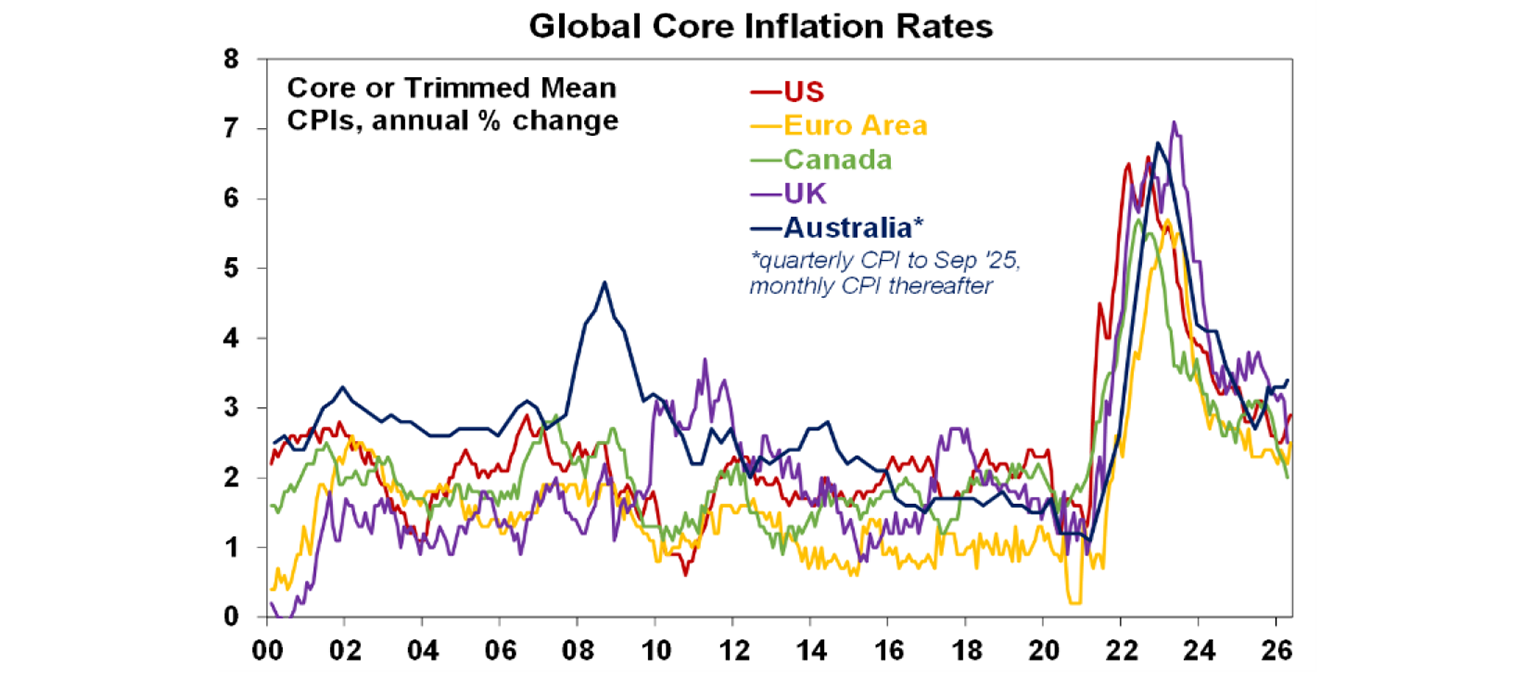

So Australia is seeming to be less of an outlier now on inflation and rates. Headline CPI inflation in the US at 4.2%yoy is now the same as in Australia. Unfortunately, we still look worse on an underlying basis though as can be seen in the next chart.

The RBA is expected to leave rates on hold at its June meeting this coming Tuesday, but it’s also likely to retain mild a tightening bias given concerns about inflation remaining above target for too long. The three rate hikes in a row this year have taken monetary policy from slightly easy to slightly tight and give the RBA some breathing space to wait and assess the impact of the hikes so far and the impact of the oil supply shock on the economy. The recent run of soft data for employment, household spending, home prices and confidence along with mixed April inflation data also support the case for a hold this month. That said, we expect that the RBA will maintain a tightening bias as underlying inflation is still trending up with business surveys and the stronger than expected award wage rise this year warn of ongoing cost and price pressures, posing a high risk that inflation expectations will move higher. As such we are continuing to allow for a further rise in interest rates with the next hike likely to come in August.

Major global economic events and implications

US economic data was soft. Small business optimism fell in May and existing home sales rose but remain weak. That said jobless claims remain low.

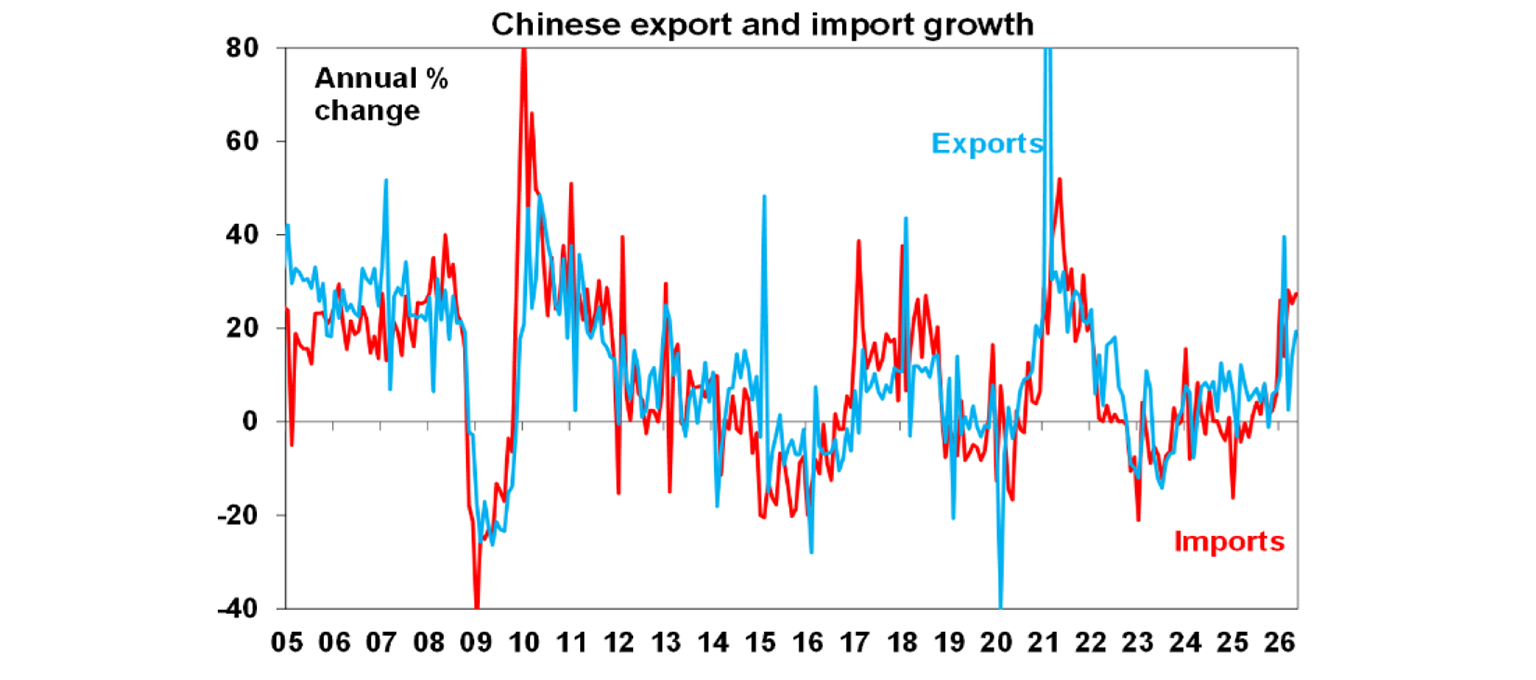

Chinese exports rose a stronger than expected 19%yoy in May helped by a rebound in exports to the US from the low base a year ago, the cut to US tariffs and AI related demand. Imports rose by more with a 27%yoy gain reflecting higher energy prices and suggesting stronger domestic demand.

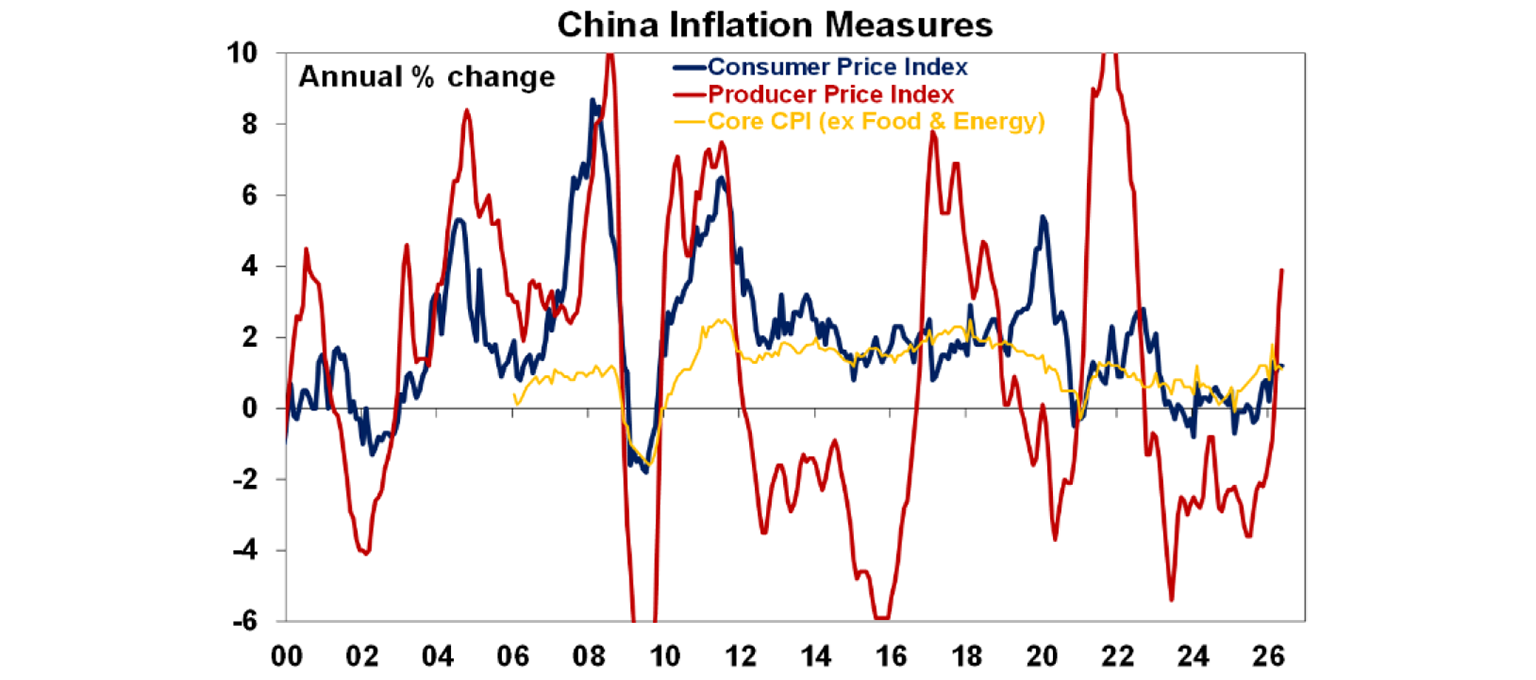

Chinese CPI inflation was unchanged in May at 1.2%yoy with core inflation slowing to 1.1%yoy, but a further rise in producer price inflation points to some further rise in consumer price inflation ahead. Meanwhile, Chinese credit growth slowed further to 7.7%yoy in May.

Australian economic events ad implications

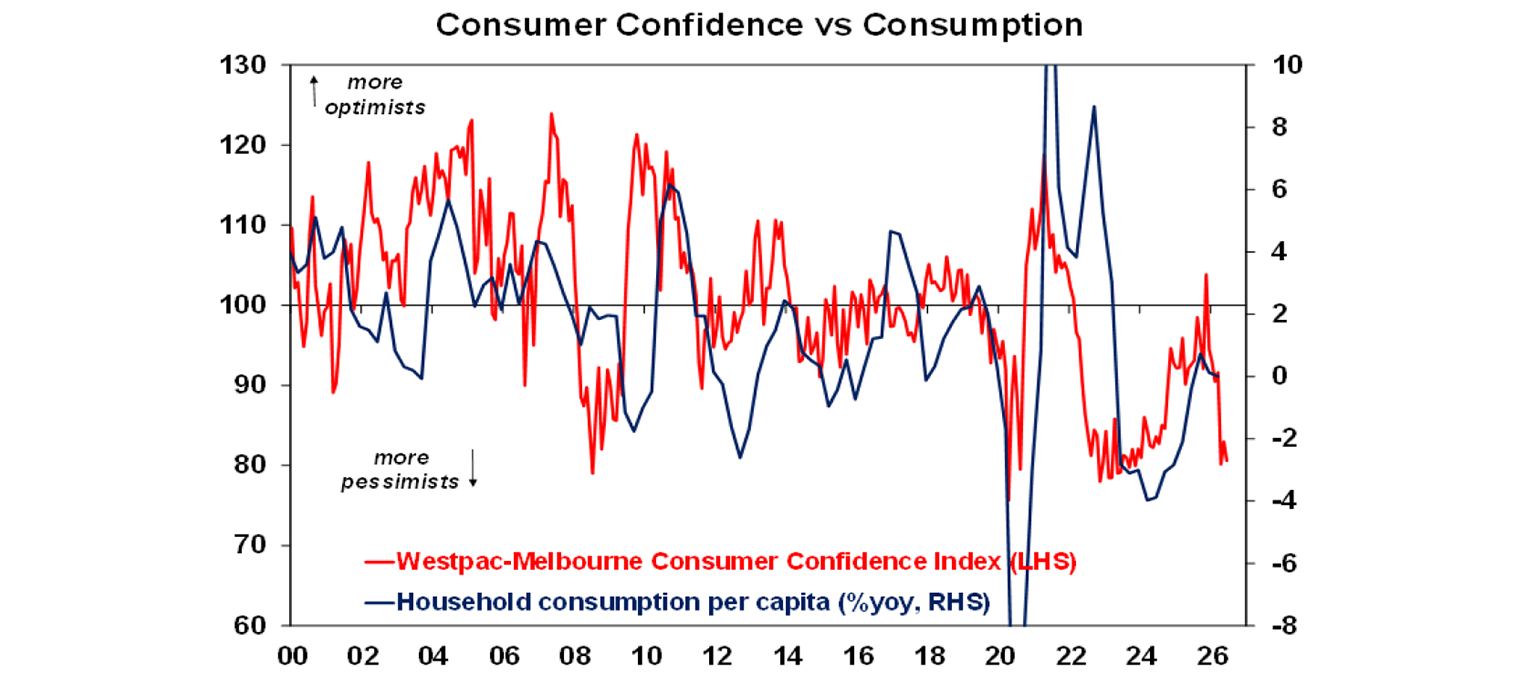

Consumer confidence fell back in June and remains at the low end of the range it’s been in for the last three decades or so with rate hikes, Budget tax hikes and the war continuing to depress consumers. The weakness in consumer confidence is warning of weaker spending ahead.

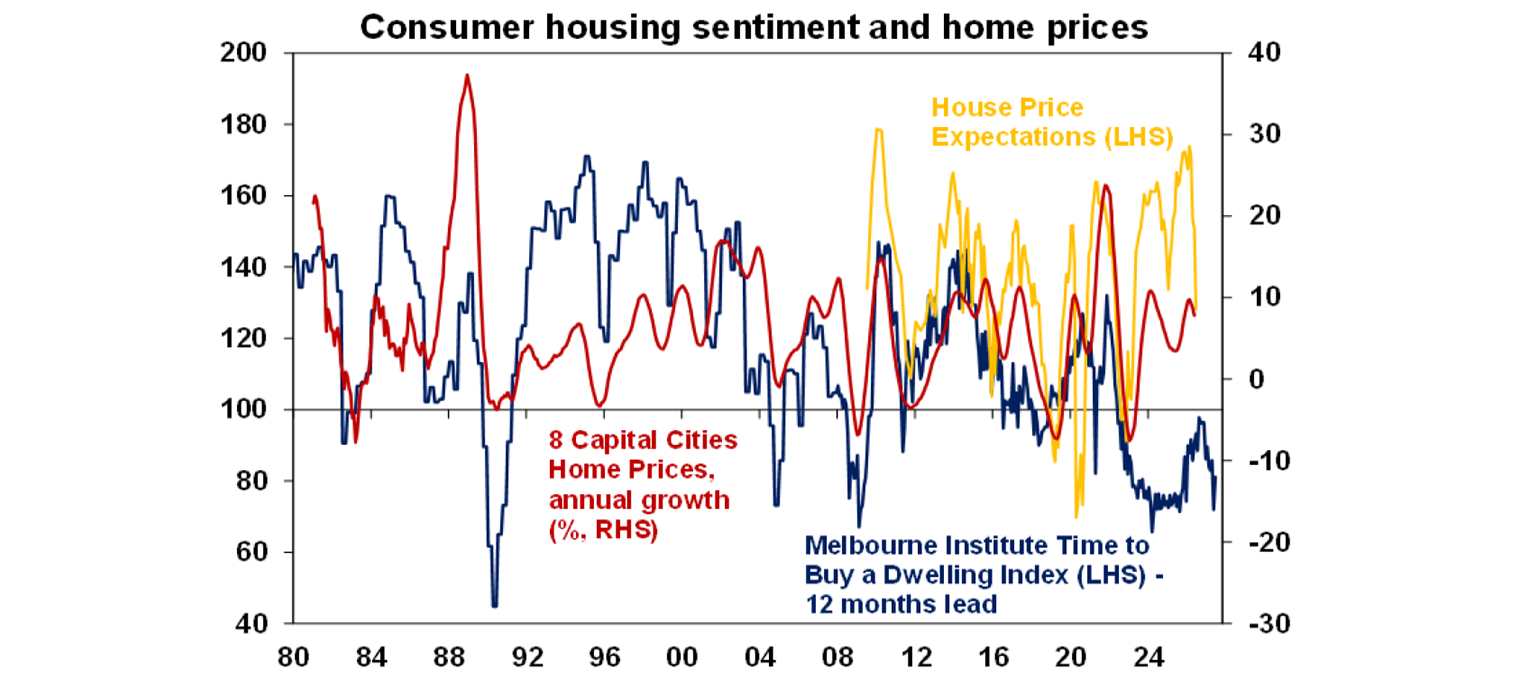

The Westpac/MI consumer survey showed a fall in home price expectations, and consumers continue to see now as a poor time to buy a dwelling.

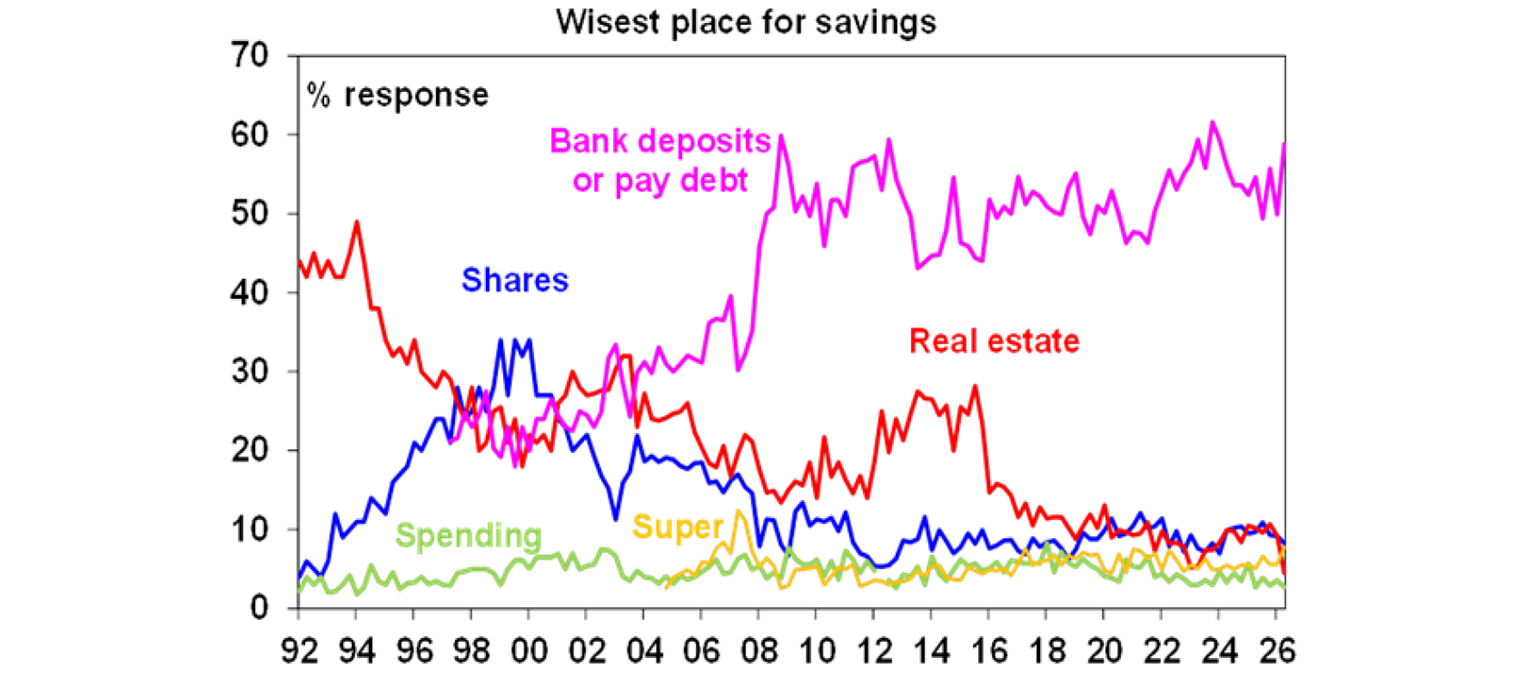

Consumers also moved a bit more cautious with their savings with an increased preference for bank deposits and paying down debt and less interest in shares and property with more interest in super. This likely partly reflects the tax changes in the Budget which make property and to a less extent shares relatively less attractive compared to super.

Consumer inflation expectations remained elevated at 5.5% in June which is down from their recent high but well above their pre pandemic norm of around 4%.

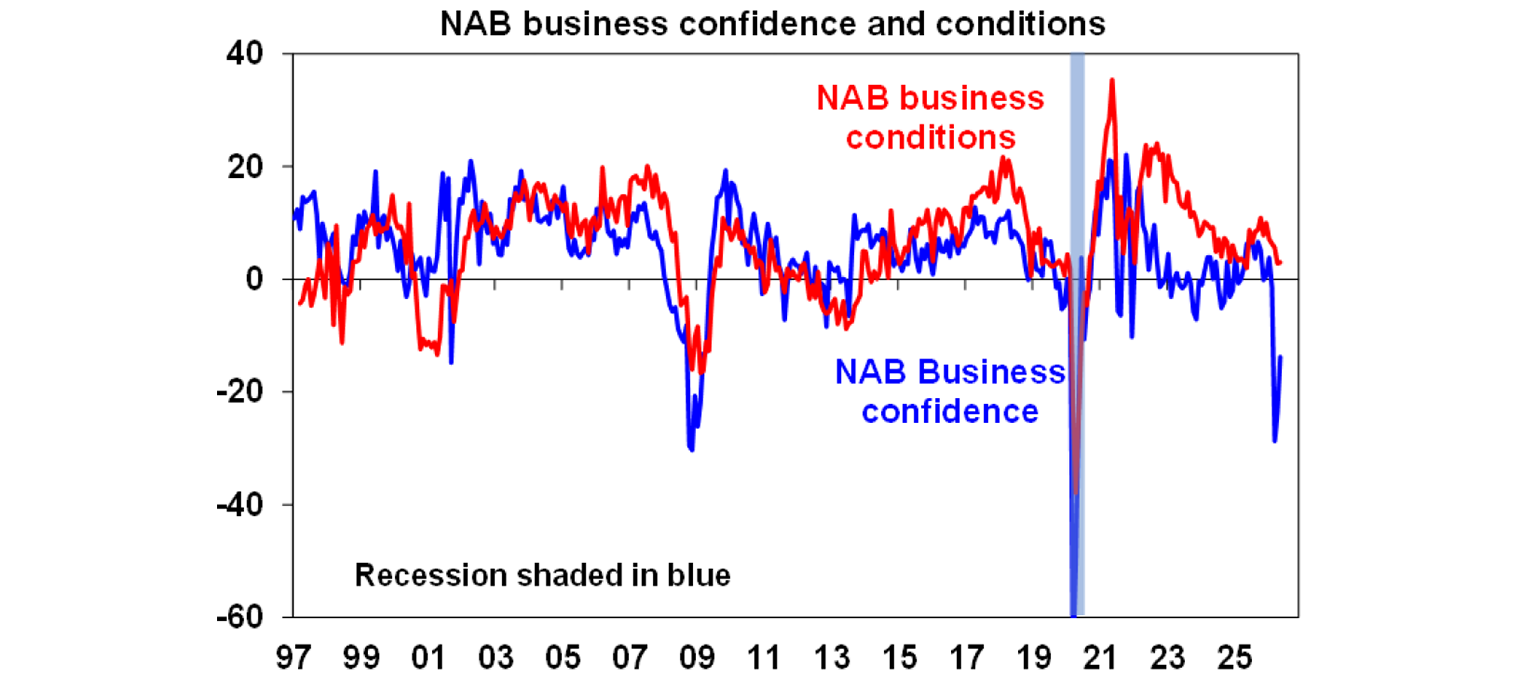

The May NAB business survey showed unchanged business conditions at below average levels, with a rebound in confidence but to still weak levels. Capacity utilisation fell suggesting a softening in demand though relative to supply which is something the RBA wants to see.

Cost and price pressures eased after the initial response to the oil supply shock but remain elevated continuing to warn of potential inflationary pressures ahead.

What to watch over the next week?

The week ahead is likely to be dominated by central banks with central banks in the US, UK, Sweden, Switzerland, Japan and Australia all meeting to consider interest rates..

In the US the Fed (Wednesday) is likely to leave interest rates on hold and remove its reference to an easing bias. While this will be Fed Chair Warsh's first meeting as Chair the rising trend in inflation and some improvement in jobs data will mean that he will find little support for a rate cut from Fed committee members with a majority now favouring removing the Fed's earing bias. Warsh may also move to reduce the amount of policy guidance from the Fed, possibly including discontinuing the "dot plot" of Fed officials' interest rate expectations, which had been flagging a rate cut this year and next. On the data front in the US expect a 0.2% rise in industrial production (Monday), home building conditions (Monday)) and housing starts (Tuesday) to remain weak and underlying retail sales (Wednesday) to show a solid 0.4%mom rise.

In Europe both the Swedish central bank (Wednesday) and Swiss central bank (Thursday) are expected to leave rates on hold at 1.75% and zero respectively although there is about a 30% chance of hike in Sweden.

The Bank of England (Thursday) is expected to hold at 3.75%, albeit with a tightening bias. British inflation data for May (Wednesday) is likely to remain around 2.8%yoy, with core around 2.5%yoy.

The Bank of Japan (Tuesday) is expected to hike by 0.25% taking its policy rate to 1% as it continues the gradual process of normalising interest rates. A report in the Nikkei indicates it will combine a rate hike with a decision not to further slow its bond buying beyond the March quarter next year. Inflation data for May (Friday) is expected to show a fall to 1.3%yoy though with core inflation around 1%yoy.

Chinese economic activity data for May (Tuesday) is likely to remain soft with retail sales expected to fall 0.6%yoy and investment to fall further.

In Australia the RBA (Tuesday) as noted earlier is expected to leave rates on hold but retain a tightening bias.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the oil shock if the flow of oil quickly resumes but the risk of further falls remains high given uncertainty around the flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and worries about the impact of AI. However, returns should still be positive for the year as a whole thanks to Trump still likely to pivot to consumer-friendly policies ahead of the mid-terms and solid profit growth.

Bonds are likely to provide returns below running yield this year.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

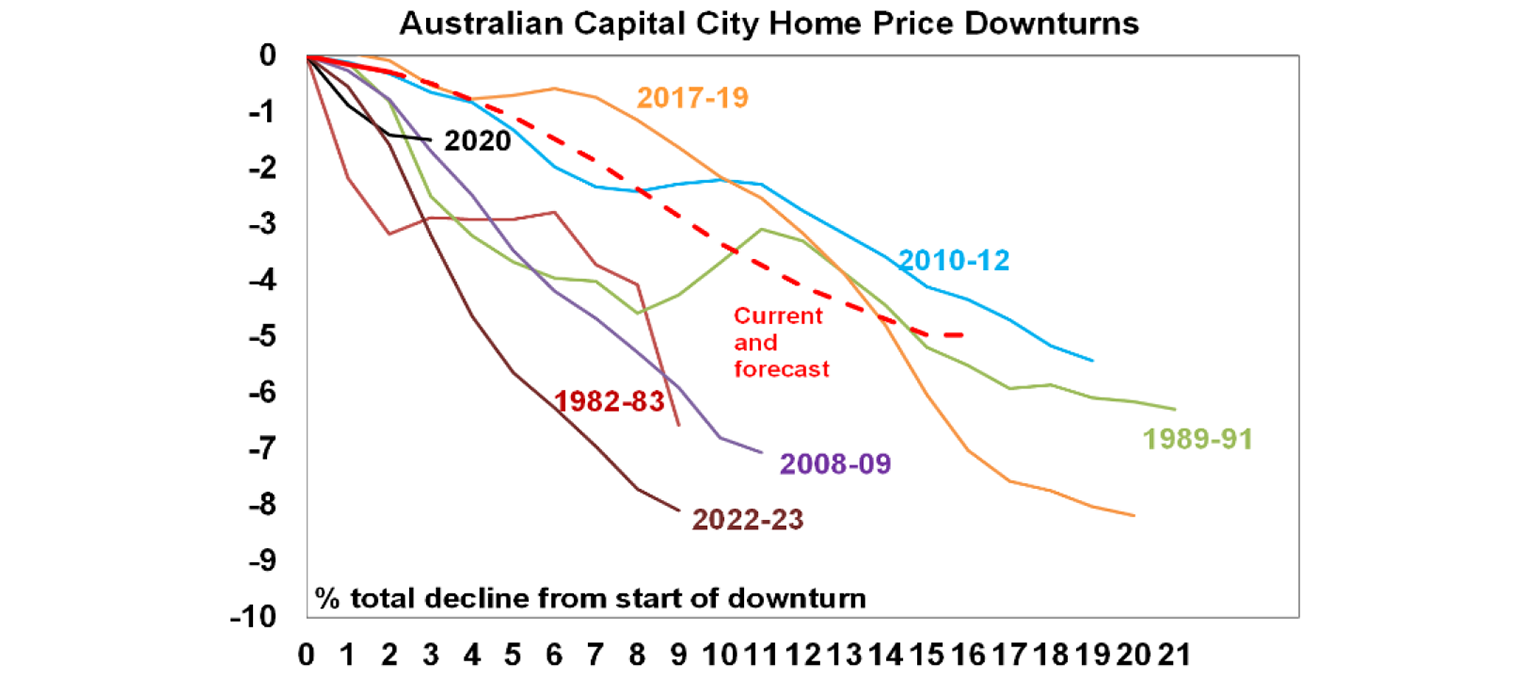

Australian home prices are expected to fall around 1% this year and by 5% over the next 12 months as a result of poor affordability, RBA rate hikes, reduced investor demand flowing from the winding back of negative gearing and the capital gains tax discount and the hit to confidence from the War. As can be seen in the next chart – which shows the percentage decline in property prices from the start of each downswing by month - a 5% fall is consistent with just another cyclical downswing of which there have been several over the last two decades.

Cash and bank deposits are expected to provide returns around 4.3%.

The $A is likely to rise as the interest rate differential in favour of Australia widens. Fair value for the $A is around $US0.72.

Diana Mousina

Deputy Chief Economist, AMP

You may also like

-

Weekly market update - 07-08-2026 Global shares had another ripper week with major share markets reaching new all-time highs, before retracing slightly on Thursday as the Iran “deal” seems further away than previously thought. -

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.