Weekly market update

Investment markets and key developments

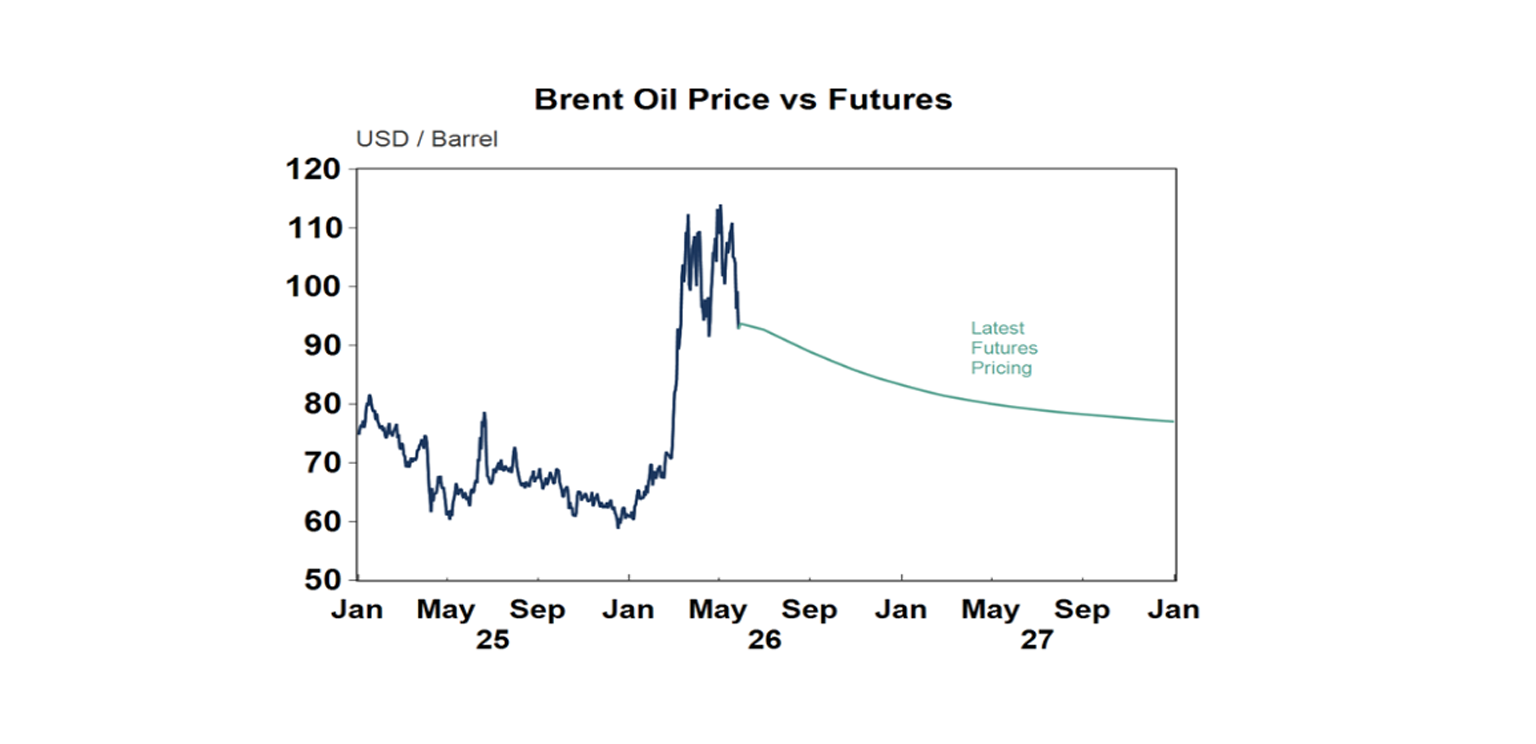

The week started on an optimistic note with Trump saying last weekend that “final aspects and details of the Deal are currently being discussed and will be announced shortly”. But this was followed by more military strikes on Iran and Trump saying he is “not satisfied” – so oil prices rebounded. But the indications are now that a tentative deal has been reached, pending Trump’s sign-off.

12 min read

The past week has been dominated by developments around a US/Iran peace deal – but despite some gyrations its looking like a deal is on the way. The week started optimistically with Trump saying “final aspects & details are…being discussed and will be announced shortly”. But this was followed by more strikes on Iran and Trump saying he is “not satisfied”. But the indications are now that a tentative deal has been reached, pending Trump’s sign-off with him saying he is making a “final determination”. This looks like it would reopen the Strait of Hormuz and extend the ceasefire for 60 days during which negotiations regarding Iran’s nuclear program will proceed. Of course, the deal could still collapse with both sides sending mixed messages. Iran’s desire to toll ships through the Strait, it’s enriched uranium, sanctions & Lebanon are sticking points. And a cynic might say the likely deal just leaves us where things were before the War with no progress on Iran’s nuclear ambitions so it could all flare up again.

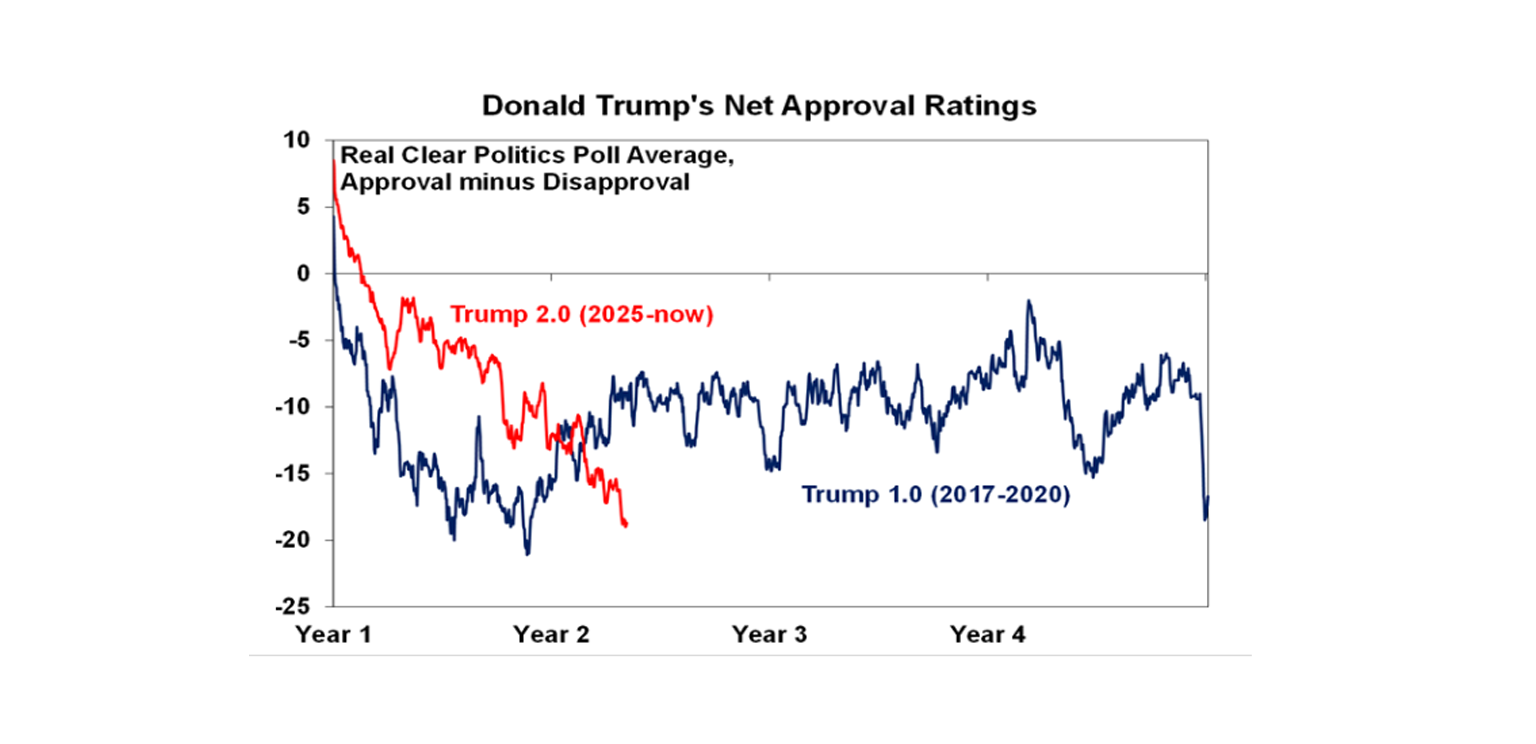

But the pressure on Trump to do a TACO and strike a deal is very high as his approval rating is continuing to collapse heading into the mid-terms. He has said it doesn’t matter but it likely matters to him bigly as the longer the Strait remains closed the more global oil reserves run down leaving the clock ticking on when the full impact of the roughly 12-13% cut to global oil production hits the global economy in full resulting in another spike in oil prices and even higher US gasoline prices – which US voters hate.

Of course, while Trump wants to TACO it requires Iran to provide the sauce.

With a deal likely nearing oil prices have fallen back to the lower end of the range they have been in since the War started. Oil futures are continuing to price a fall on the grounds that the Strait will be opened eventually but that prices will be above pre-War levels as it will take a while for oil and fuel production to ramp up again with a risk premium priced in to allow for the risk of a resumption of the conflict. This is in line with our own views.

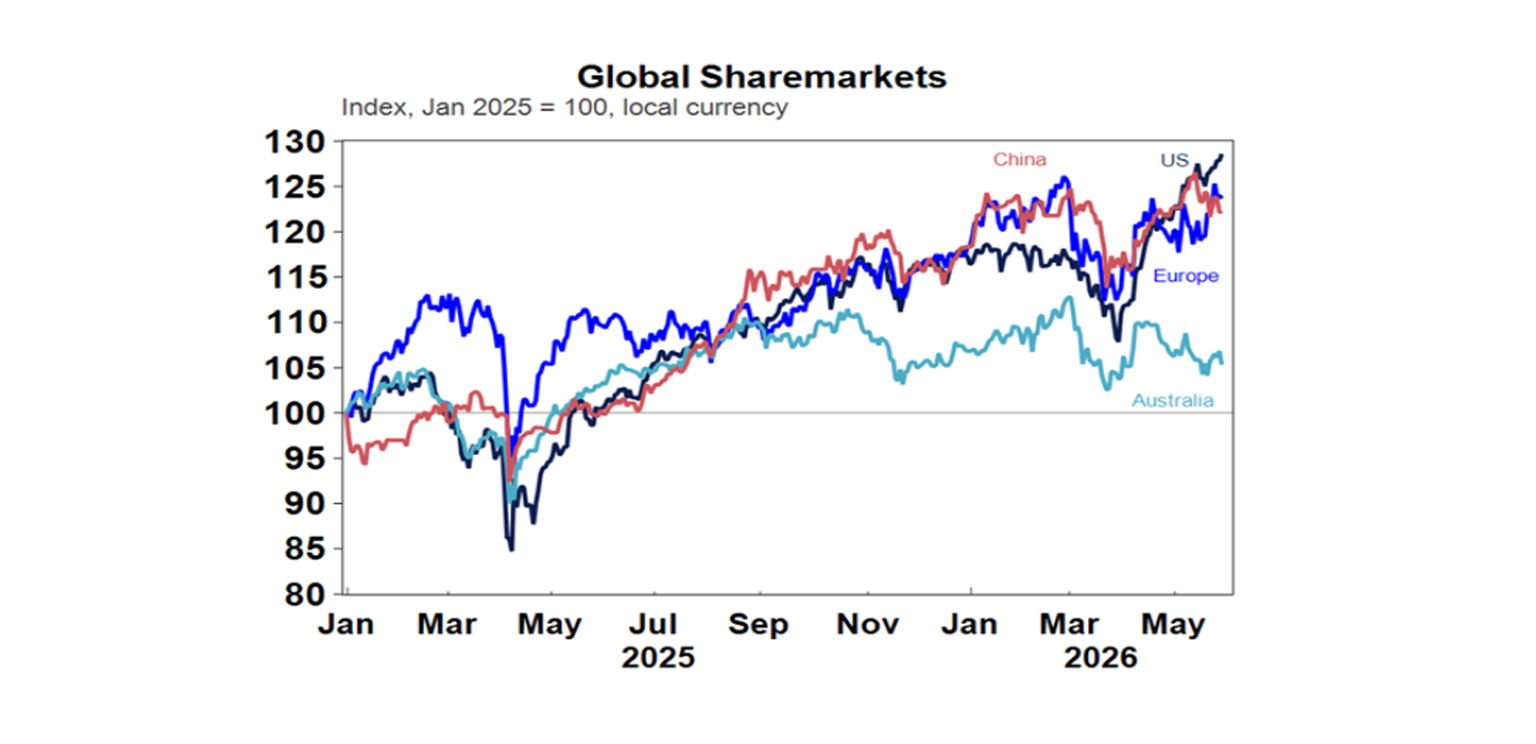

Helped along by the reports of a peace deal nearing agreement and ongoing optimism about the boost from AI related demand to profit growth, global share markets rose over the last week. US shares rose 1.8% to a new record high, Japanese shares rose 4.7% also to a new record high, Eurozone shares rose 0.5% and Chinese shares rose 0.9%. Australian shares rose 0.9% for the week, with gains in retailers and miners partly offset by falls in telcos and energy shares, but they remain significant underperformers. While the US share market has surged to new record highs helped also by very strong profit growth and still solid economic activity, the Australian share market has been continuing to struggle not far from its March lows in response to profit downgrades, three rate hikes from the RBA, capital gains tax changes and greater scepticism locally regarding a quick reopening of the Strait.

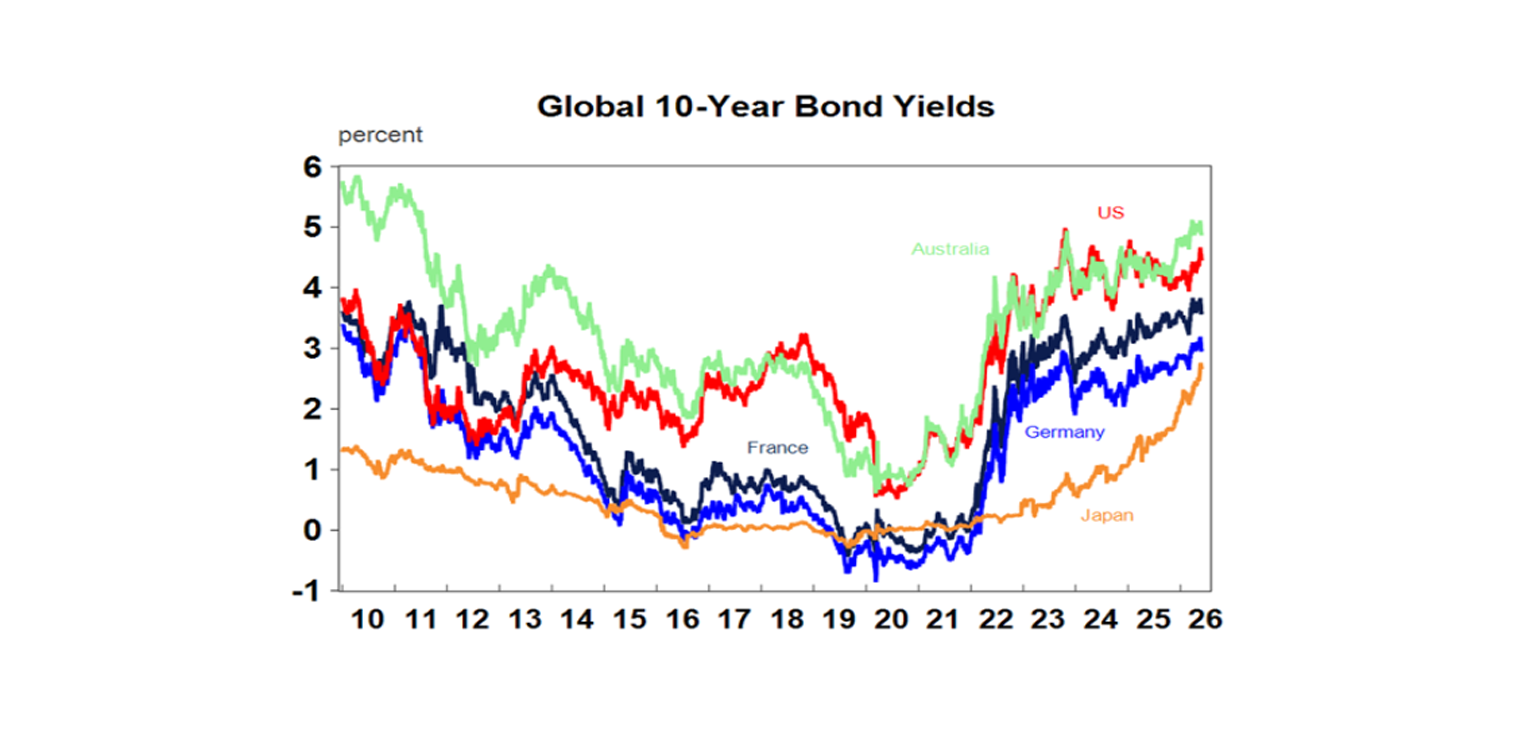

News of a peace deal saw bond yields fall on hopes for lower inflation with lower oil prices. Metal and gold prices rose over the week, but iron ore prices and Bitcoin fell. The $A rose slightly as the $US fell slightly.

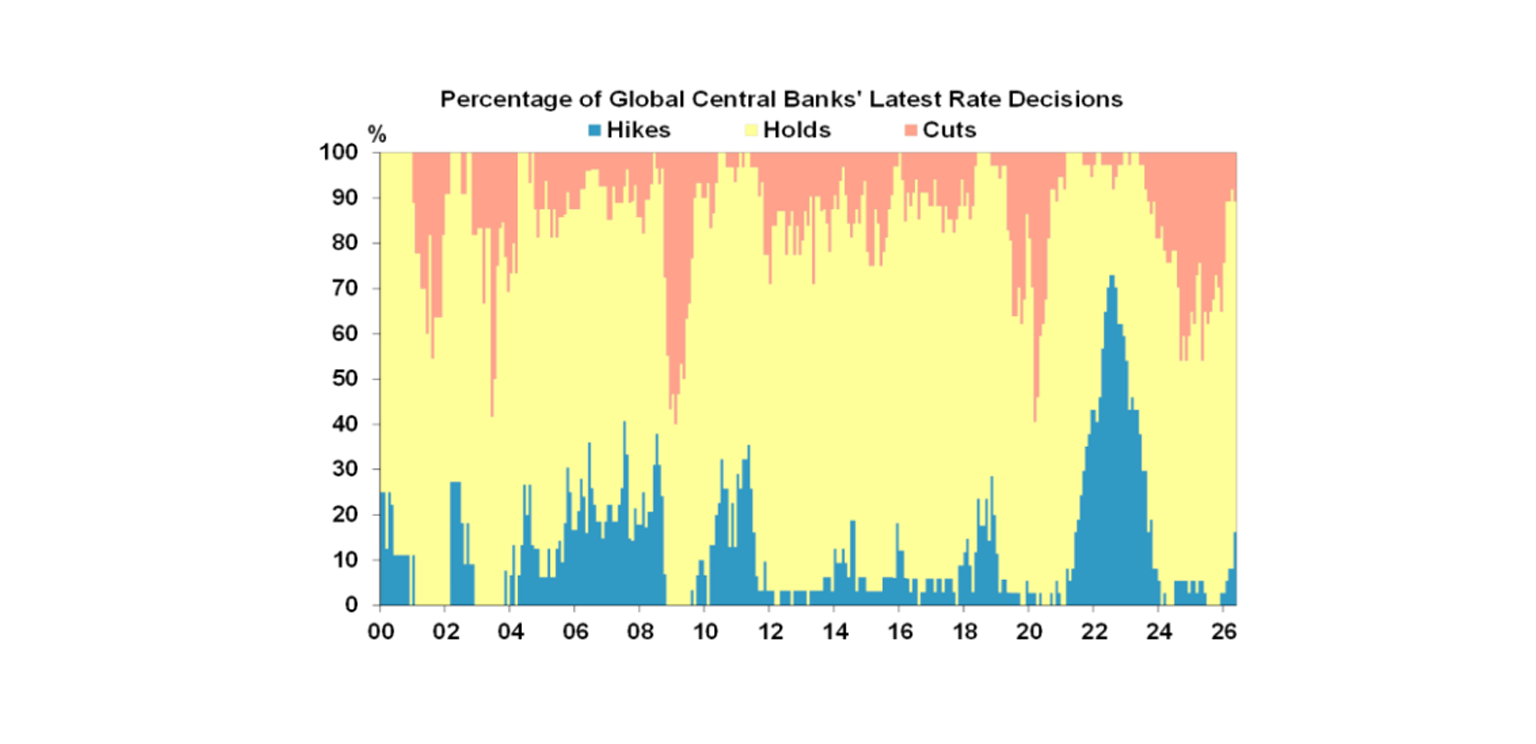

Despite optimism for lower oil prices, central banks continued to edge in the direction of higher interest rates over the last week. Another Fed Governor - Lisa Cook this week, Christopher Waller last week - came out warning of a rate hike if inflation doesn’t start to fall soon. And unfortunately, US core private final consumption inflation rose further in April to 3.3%yoy. And both the Bank of Korea and Reserve Bank of New Zealand while leaving rates on hold warned of rate hikes ahead. Its early days, but as can be seen in the next chart the percentage of global central banks hiking is hooking up.

The risk here is that expectations for higher inflation and rates could drive another leg higher in global bond yields which could put pressure on share markets. A quick reopening of the Strait could short-circuit this though.

In Australia though, mixed inflation data for April provided a bit of relief. The good news was that headline CPI inflation slowed more than expected to 4.2%yoy from 4.6%yoy with a bigger than expected fall in fuel prices (helped by the fuel tax cut) and free public transport in some states. Electricity prices fell 0.9%mom and the annual price ruling from the energy regulator points to falling prices from July helped by record output from wind farms and batteries. (So more clean energy can lower electricity prices!) The bad news was that underlying or trimmed mean inflation edged up further to 3.4%yoy from 3.3%yoy and appears to be tracking in line with the RBA’s forecast for a 0.95%qoq/3.8%yoy rise in the current quarter as a whole.

Some good news on the underlying inflation front was that the breadth of price rises has improved slightly with slightly more CPI items seeing inflation below 2%yoy than above 3%yoy. But against this the second round impacts from the oil supply shock to transport costs, plastics, food prices etc are yet to impact, housing costs are continuing accelerate with new dwelling prices up 0.7%mom and a rise in asking rents pointing to higher rents, business surveys continue to show a sharp rise in cost pressures and there is a high risk that an acceleration in minimum and award wage rises will contribute to stronger wages growth.

On balance the mixed inflation data for April, coming on the back of soft April jobs data, depressed confidence and signs of softening household spending will likely see the RBA leave rates on hold at its June meeting as it waits to see the impact from its three back to back rate hikes and how the oil supply shock pans out. However, we are continuing to pencil in a further and likely final rate hike in August as underlying inflation remains too high. The money is currently pricing zero chance of a rate hike in June and a 70% probability of a further hike by year end.

While some of the lyrics in Melting Pot are questionable and it doesn’t go down well with the identity politics and even multiculturalism of today – there is something naively appealing in the hippie sentiment of “what we need is a great big melting pot…and turn out coffee coloured people by the score” as way to a “get along scene”.

Major global economic events and implications

US economic data was mixed. Personal spending growth was soft but okay in April, the trend remains up in underlying capital goods orders and shipments – helped by the data centre boom - and jobless claims remain low. Against this though consumer confidence as measured by the Conference Board fell slightly, the falling savings rate is removing a source of support for US households, new home sales remain weak, and home prices fell slightly again in March. But while it’s mixed the Atlanta Fed’s GDPNow tracker for June quarter GDP has growth picking up to 3.8% annualised from just 1.6% in the March quarter.

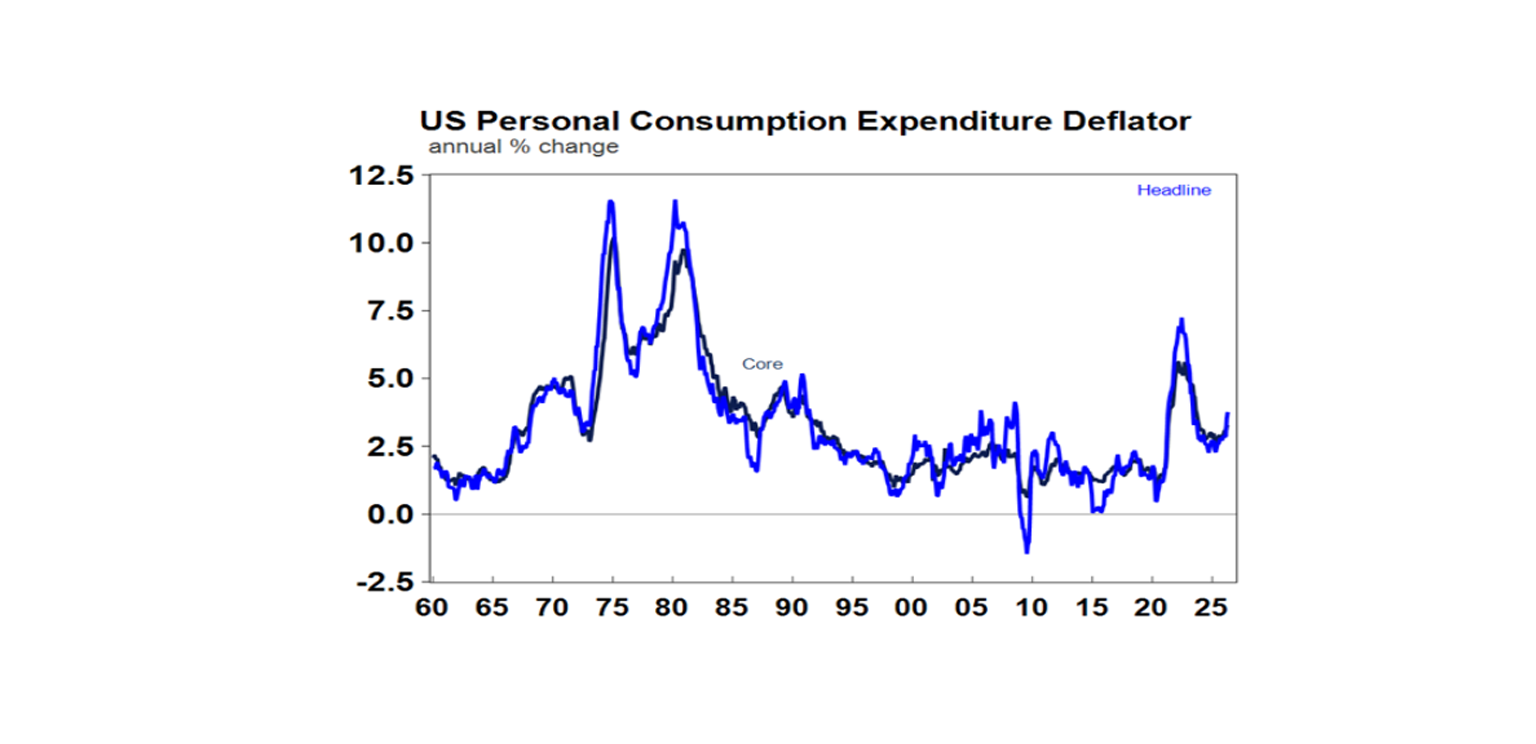

Meanwhile, the US core PCE measure of inflation rose to 3.3%yoy and is likely to rise further in the months ahead. While it wasn’t as high as feared its moving further away from the Fed’s 2% target and supporting concerns that the Fed may have to raise rates this year.

Japanese economic data was strong with industrial production and retail sales up strongly and unemployment down. Against this, Tokyo inflation fell to 1.4%yoy.

Australian economic events and implications

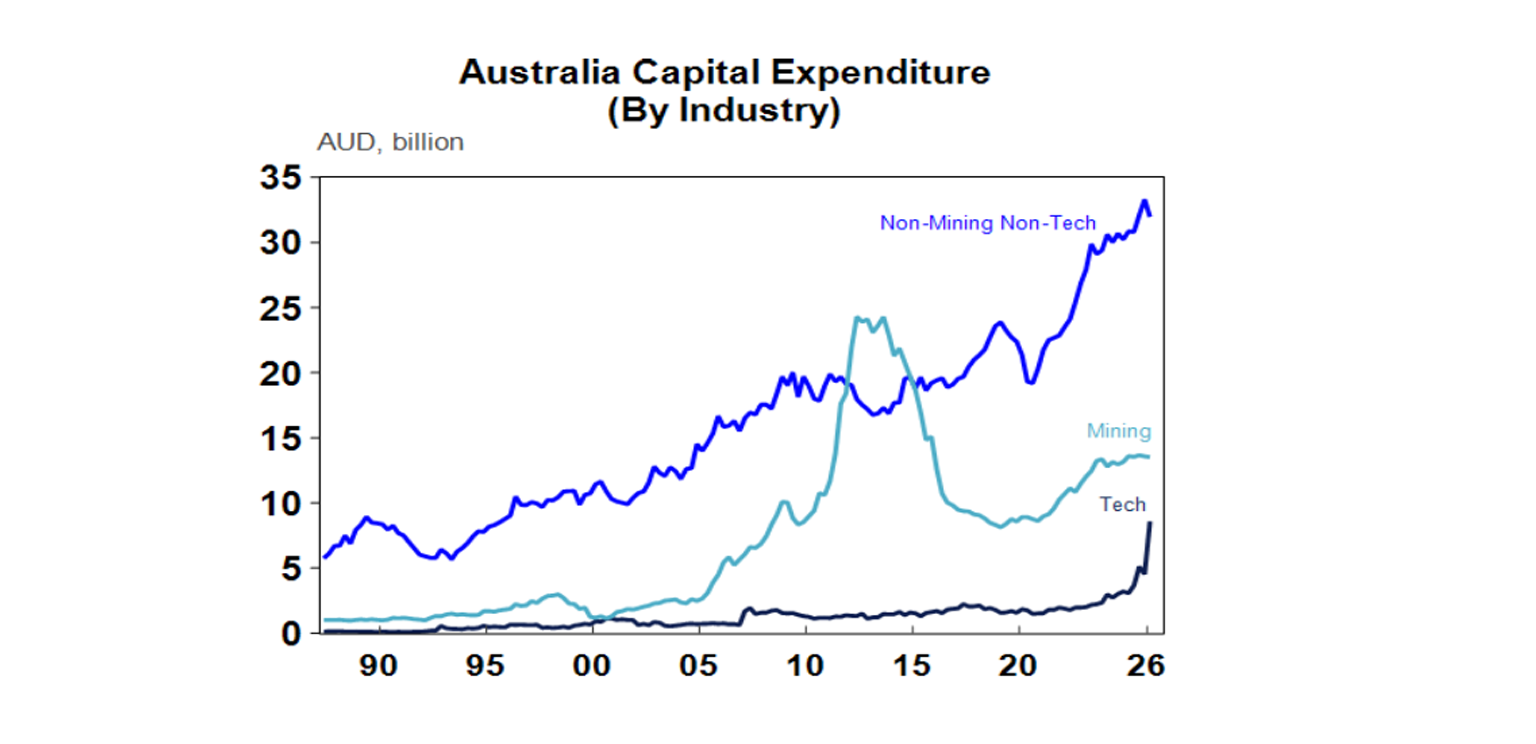

Australian business investment in the March quarter looks to have been strong helped by booming data centre investment. Real private capital spending (capex) rose 6.5%qoq in the March quarter reflecting an 18%qoq surge in plant and equipment investment driven by another big spike in IT investment in data centres. This may be great for the economy longer term but just bear in mind that a big chunk of it will be imported so it doesn’t necessarily mean a surge in March quarter GDP growth. Mining capex is trending sideways albeit at a solid level, and non-mining non-tech capex fell but it is in a rising trend.

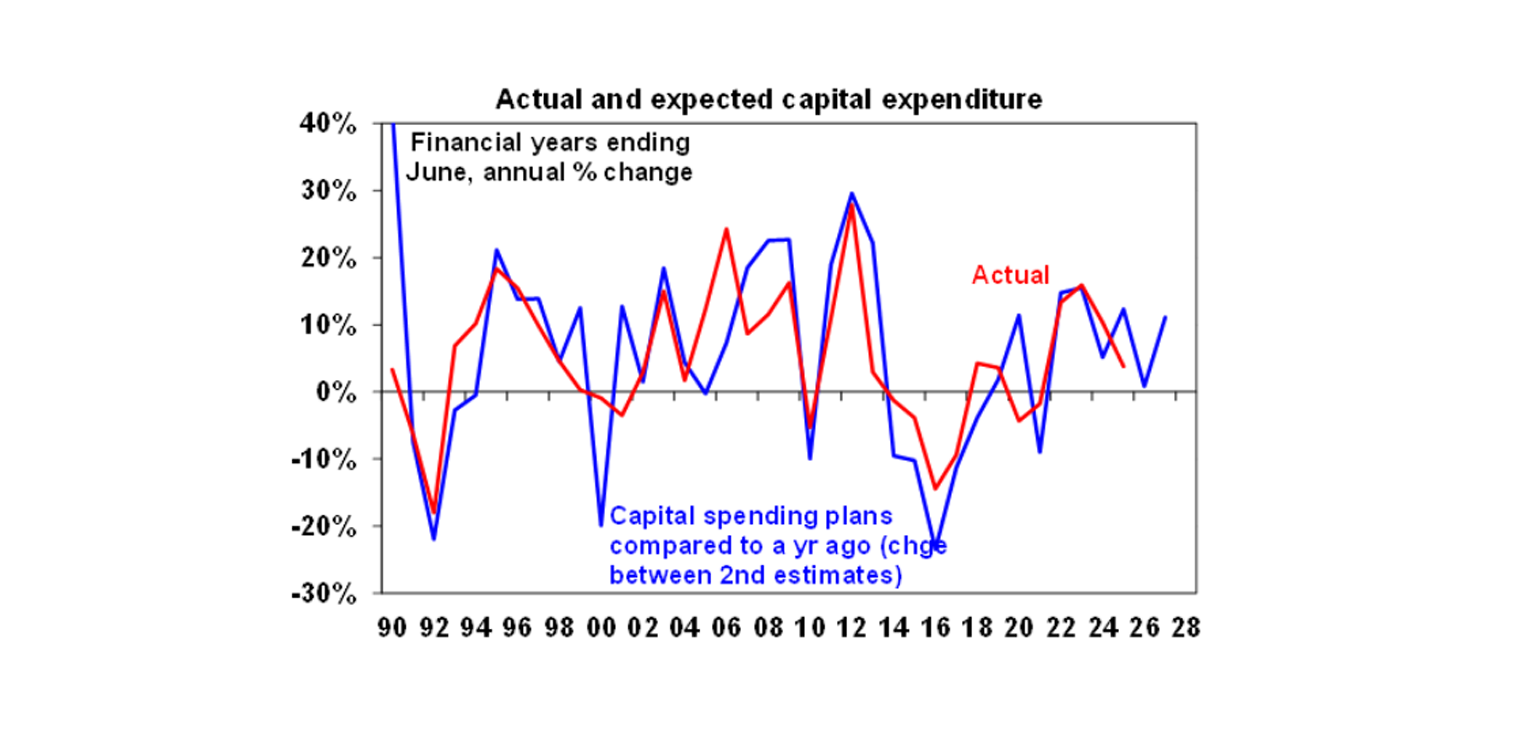

Business investment plans for the year ahead are for solid growth with capex plans 11% higher than a year ago.

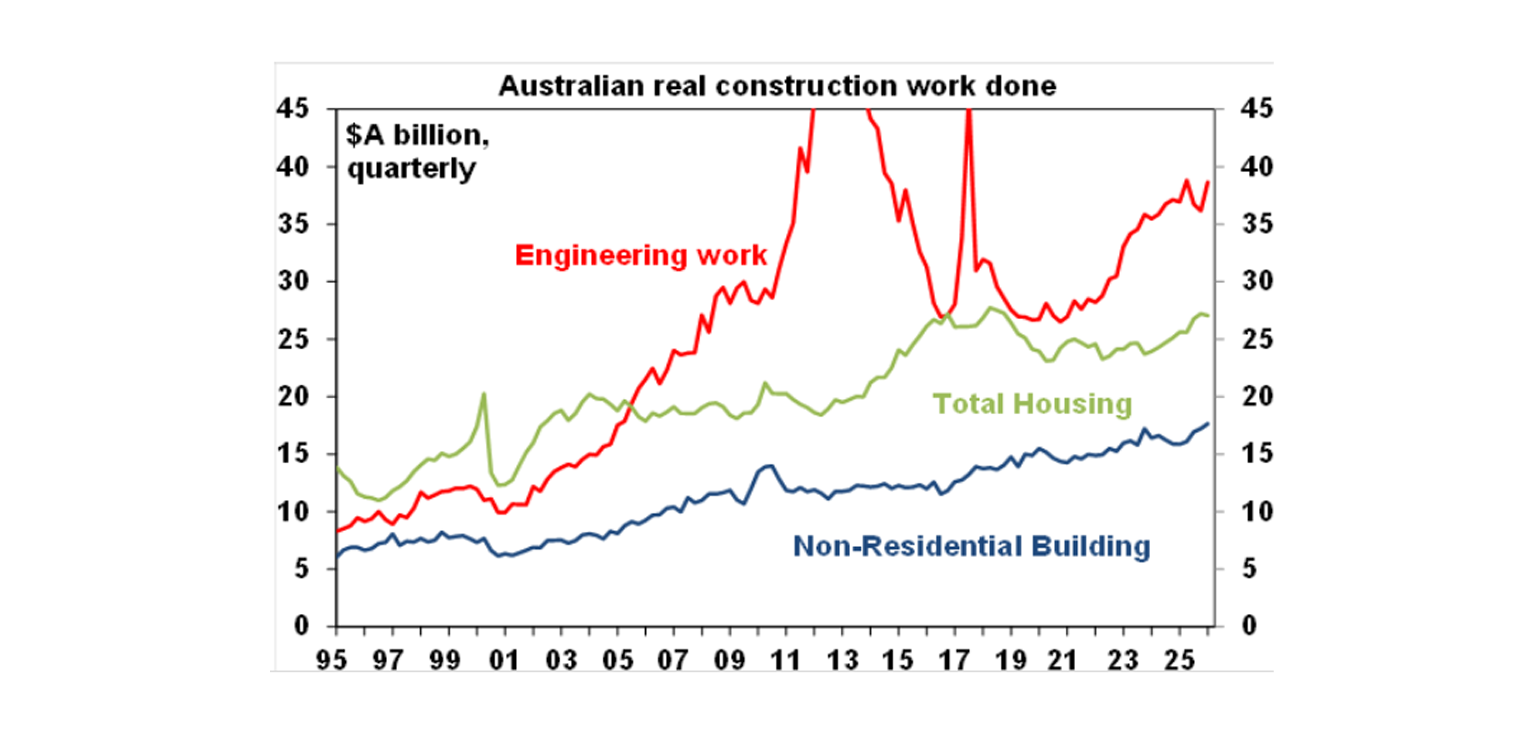

Construction work in the March quarter was also stronger than expected, up by 3.4%qoq. The upside surprise though was in engineering and narrowly concentrated in WA suggesting it was mining sector related. In terms of building – home building actually fell 0.6%qoq but non-residential building actually rose 2.5%qoq.

Household spending data for April was a bit less bright falling a greater than expected 1.1%mom and slowing to 4.9%yoy. The fall was largely driven by lower fuel prices, but spending was softer generally including in reduced travel. Real spending growth is still running around 2.5%yoy, but the slowing in April may be a tentative sign of flagging consumer demand with rate hikes and poor confidence.

What to watch over the next week?

In the US, expect the May manufacturing conditions ISM (Monday) and the services ISM (Wednesday) to both remain solid around 53, job openings and quits data for April (Tuesday) to show okay labour market conditions and May jobs data (Friday) to show a 90,000 gain in payrolls and a rise in unemployment to 4.4%.

Eurozone data is likely to show unemployment remaining around 6.2% (Monday) and CPI inflation around 3.3%yoy for May with core inflation rising to 2.4%yoy.

Chinese business conditions PMIs are expected to remain consistent with subdued but okay economic growth.

In Australia, the focus is likely to be on March quarter GDP data (Wednesday) which is expected to show a growth around 0.6%qoq or 2.7%yoy up slightly from 2.6%yoy in the December quarter with strong growth in business investment, moderate growth in consumer spending, a fall in housing and a detraction from trade. In other data, expect Cotality data to show a 0.1% fall in home prices in May (Monday) with further falls in Sydney and Melbourne and a further slowing in Adelaide, Brisbane and Perth as higher interest rates, poor buyer confidence and the Budget move to increase property taxes for investors depress demand. Building approvals for April (Tuesday) are likely to show a 2% bounce and the trade balance (Thursday) is likely to swing back into a $1.5bn surplus after a surge in imports of fuel and data centre related equipment resulted in a $1.8bn deficit in March.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction remains high given uncertainty around the flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Trump still likely to pivot to consumer-friendly policies and solid profit growth.

Bonds are likely to provide returns below running yield this year.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth this year is likely to slow to around flat with prices likely to fall over the year ahead due to poor affordability, RBA rate hikes, reduced investor demand flowing from the winding back of negative gearing and the capital gains tax discount and the hit to confidence from the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens. Fair value for the $A is around $US0.72.

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.