Weekly market update

Investment markets and key developments

Australian shares are a key beneficiary of the rotation trade helped by the now concluded December half earnings reporting season confirming that listed company profits are rising again.

12 min read

While US shares fell over the last week as AI and tech related worries, including AI’s impact on private capital, along with the increasing risk of a war with Iran continued to impact, other global markets continued to benefit from the rotation trade away from tech to non-tech shares. For the week, US shares fell 0.4%, but Eurozone shares rose 0.3%, Japanese shares rose 3.6% and Chinese shares rose 1.1%. Australian shares had another strong week rising 1.3% to reach a new high helped by the rotation trade and a rebound in corporate profits. Gains were led by miners, consumer staple, IT and telco shares. Through February, global shares rose around 0.8% but the Australian share market rose 3.7%, the strongest February since 2019. Bond yields mostly fell including in Australia.

The rotation from tech to non-tech continues. This is evident in the continuing outperformance of the equal weighted US S&P 500 which is up 6.8% year to date compared to the tech heavy market cap weighted S&P 500 which is up just 0.5% and in the relative outperformance so far this year of non-US share markets with Eurozone shares up 6% and Japanese shares up 16.9%. Tech has a 32% weight in the US share market but its nearly 50% if tech like stocks are included..

Australian shares are a key beneficiary of the rotation trade helped by the now concluded December half earnings reporting season confirming that profits are rising again. So far this year the Australian share market is up 5.6% against 2.5% for global shares, which are dominated by the US with a 64% weight. Rich valuations, the hawkish RBA and global uncertainty around tech shares, US policies and geopolitics are the key constraints. But rising profits led by the miners and banks are propelling the market higher. Stronger profit growth and the rotation trade is likely to continue to help Australian shares, possibly now pushing the ASX200 above 9300 by year end. This of course assumes US tech stocks don’t fall too much, and we continue to see a 15% or so correction (like last year) along the way!

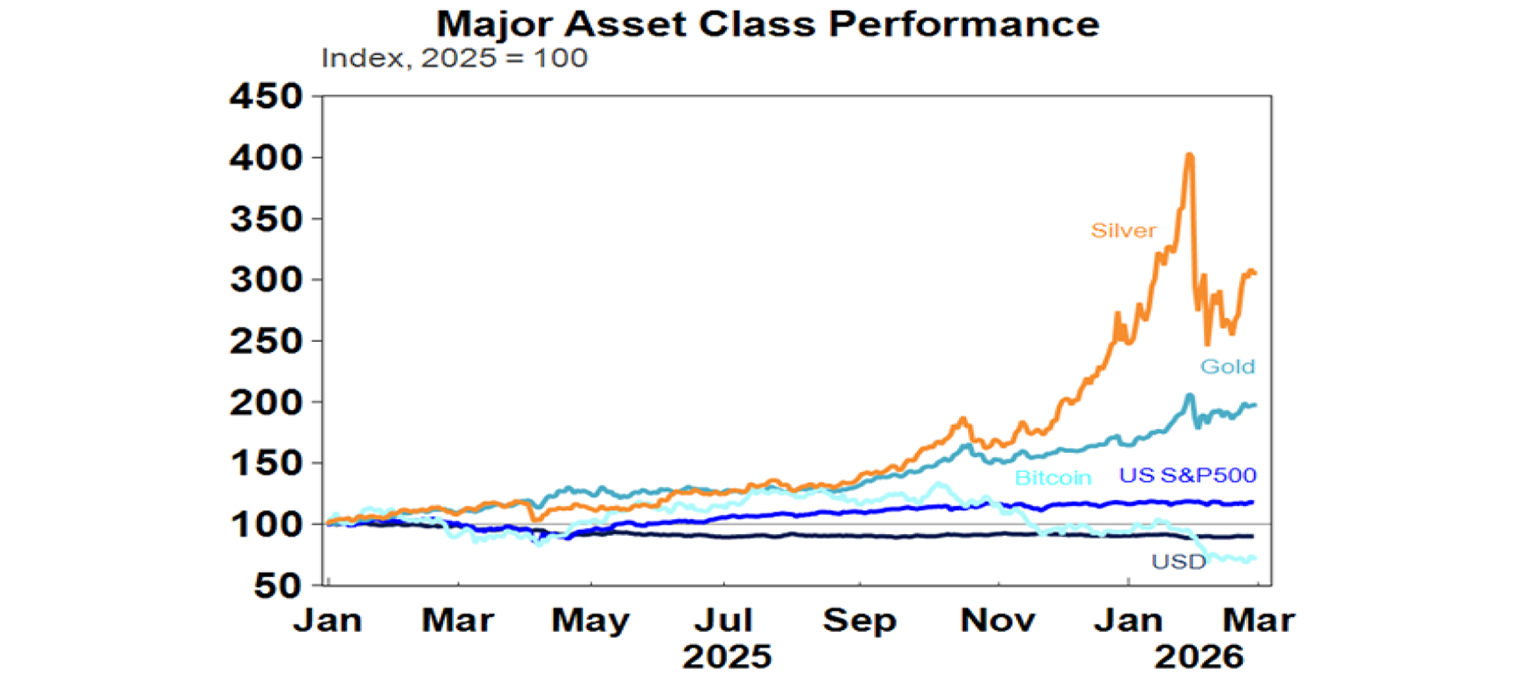

Gold (and silver) prices rose further on the back of geopolitical risk around Iran. Bitcoin remains in the dogbox though waiting for winter to end again. Metal and iron ore prices rose. Oil prices rose on increasing risks of another US/Iran conflict. The $A rose above $US0.71 again with the $US down slightly.

While most major share markets managed to rise over the last week worries remain around tariffs, AI and Iran.

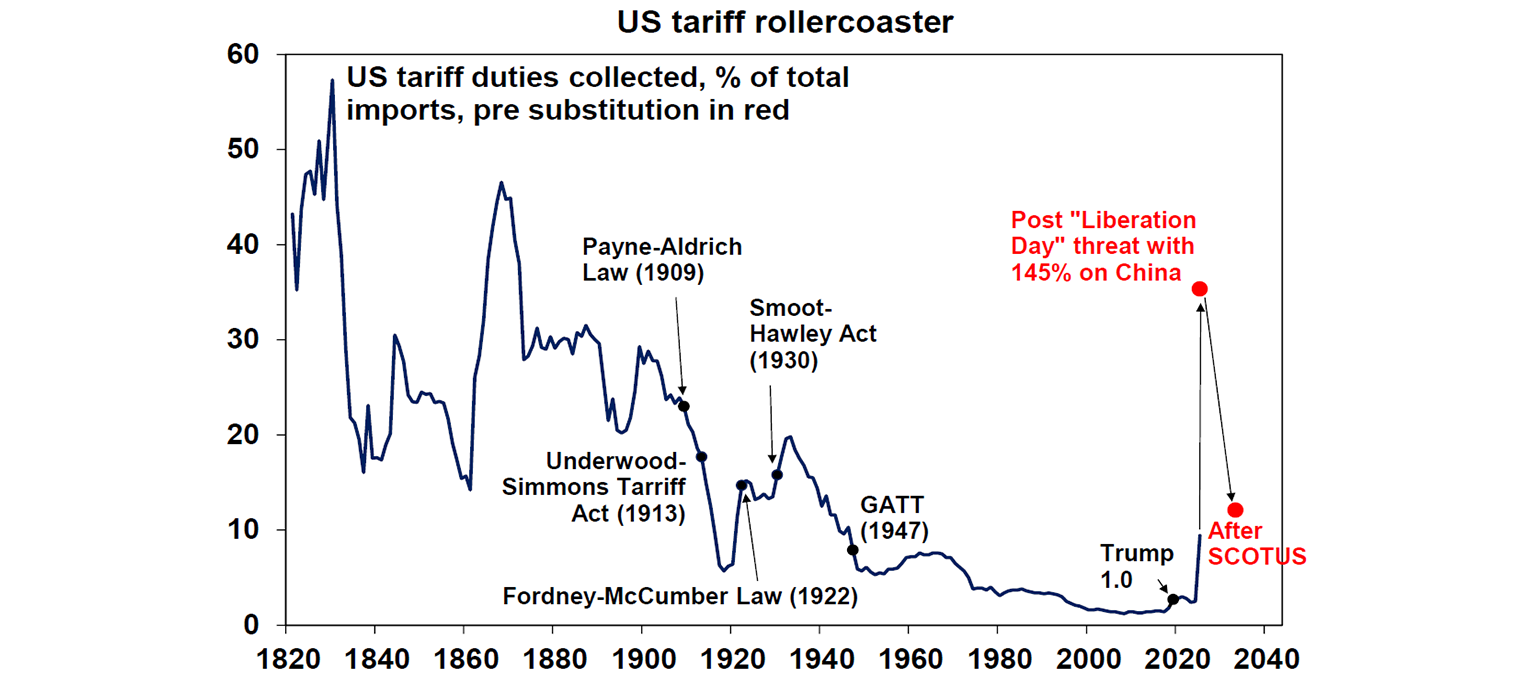

The US Supreme Court’s strike down of Trump’s emergency powers tariffs and Trump’s replacement strategy has added to uncertainty around US tariff policy. Our rough estimate is Trump’s 15% flat tariff rate (under section 122 of the Trade Act) combined with other tariffs that were not struck down will mean that the average US tariff rate will be around 12% and once section 301 trade reviews are undertaken it will move back to around 15% or so which is around where it was before the Supreme court decision. So ho-hum! But uncertainty remains around: whether the section 122 rate is 10% or 15% as only the former has been signed off, whether it will also survive legal challenges and what will happen to agreed deals. For Australia, the new replacement tariffs mean its worse off in the short term (now 15% versus 10% with no benefit versus other countries) but may be better off longer term as it will be hard to justify tariffs on Australia under s301. More broadly our view remains that the Supreme Court decision marginally reduced the risks around the US by reinforcing that it acts as a guardrail on Trump’s power and we have likely seen “peak Trump tariffs” for now as he refocusses on affordability issues ahead of the midterm elections.

Worries about AI valuations and disruption continue to throw shares around with a gloomy scenario report about AI’s impact on jobs and growth from Citrini Research combining with more reports about how AI can disrupt existing software and related jobs (eg WiseTech laying off 30% of its workforce and Block nearly 50%) along with a negative reaction to a solid beat by Nvidia (which saw sales up 73%yoy and earnings up 80%yoy). The gloomy Citrini scenario looks too negative though as it appears to ignore economy’s ability to adjust, the likely enduring desire for human engagement, likely limits to AI, no boost to the economy from higher AI and higher blue-collar income and no policy response. That said the sort of concerns we are now seeing and increasingly less favourable market responses to strong profit growth from AI related companies is the sort of thing you would expect to see going into a correction.

Finally, the risk of a US strike on Iran is very high. Once again there were claims of “significant progress” in US/Iran talks with more talks for the week ahead, but President Trump said he’s “not happy” with Iran and the US military build-up is continuing. Oil prices could spike above $US70 if there is a strike, which might add 5 cents a litre or so to Australian petrol prices. But if Iran retaliates by disrupting neighbouring countries oil exports or blocking the Strait of Hormuz through which 20% of global oil supplies flow, then a spike above $US100 would be likely which could add around 40 cents a litre or more to Australian petrol prices. And this would be taken badly by global share markets. Predicting this remains difficult though – it could be just another example of Trump’s “maximum pressure” negotiating approach and he is likely to be wary of anything that causes a sharp spike in oil prices ahead of the midterms.

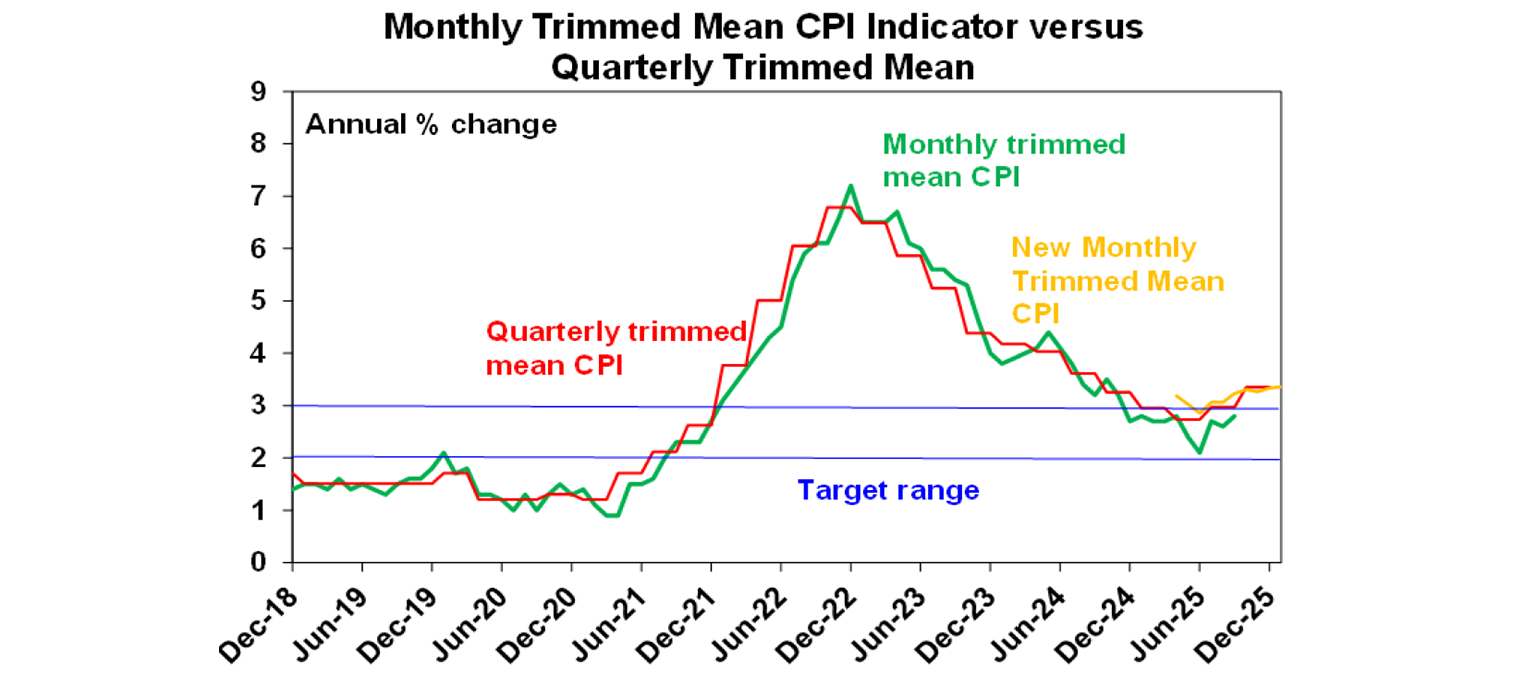

In Australia inflation surprised on the upside again in January – but we still see the RBA remaining on hold albeit the risk of another hike is very high. Contrary to expectations for a fall inflation remained at 3.8%yoy partly due to an 18.5%mom surge in measured electricity prices. And trimmed mean inflation rose further to 3.4%yoy with a 0.3%mom rise threatening to negate a possible downtrend in monthly increases since a spike last July. This in turn reinforces concerns about capacity constraints in the economy and increases the risk that the RBA could hike as early as its March meeting.

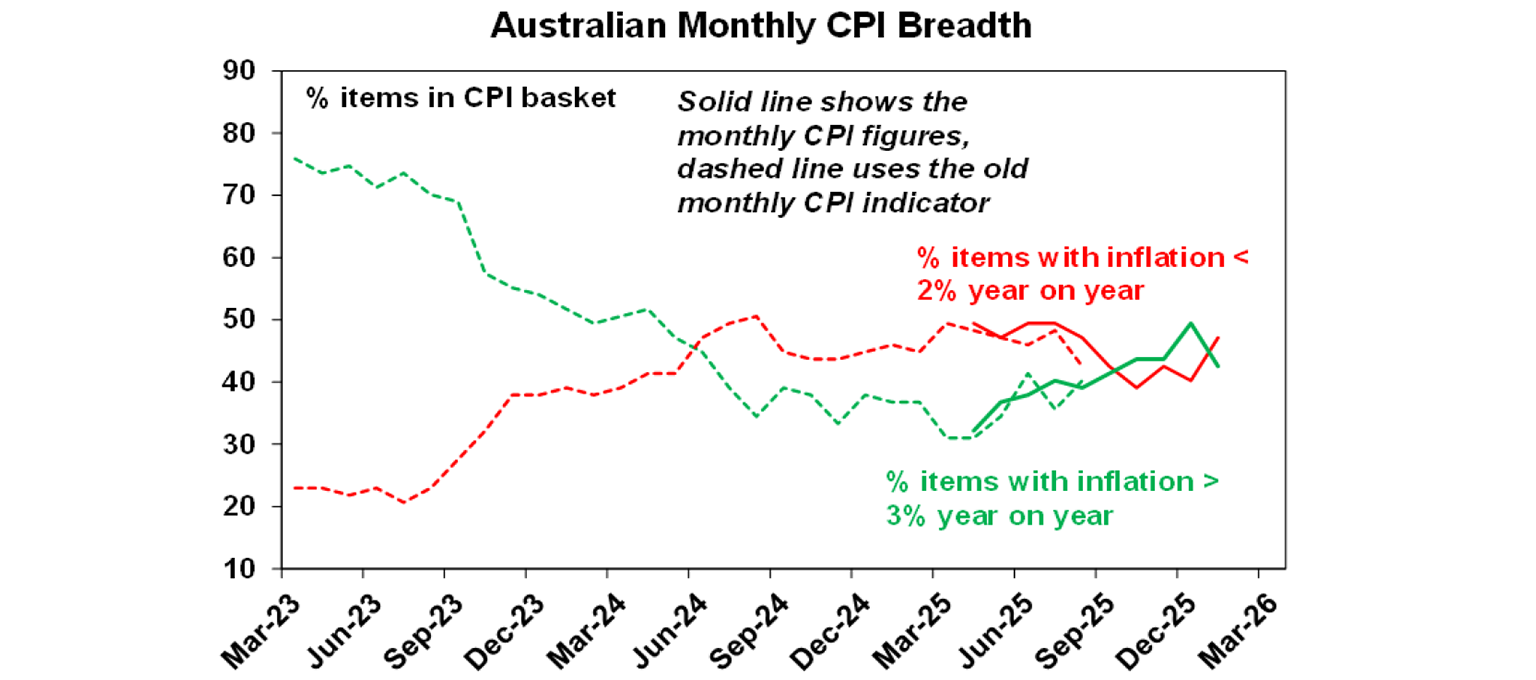

However, we expect the RBA to remain on hold for now. There are several reasons for this: for the first time in several months there were more items with annual inflation below 2%yoy than above 3%yoy; there is some tendency for new monthly trimmed mean to come in a bit stronger in the first month of each quarter; and so far it looks like inflation this month is coming in at or a bit below the RBA’s forecast for trimmed mean inflation for the March quarter of 0.9%qoq or 3.5%yoy. The RBA has continued to indicate that it will primarily focus on the quarterly inflation data and for these reasons it makes sense to do so now. RBA Governor Bullock’s comments after the inflation release – that “I don’t think it [inflation] is taking off again” and it’s not “very clear what we have to do” suggest that the RBA is in wait and see mode for now. The money market is putting the chance of a rate hike in March at just 11%, rising to 93% for May.

As we have noted in previous reports, the Australian Government can help the RBA in getting inflation down and enabling lower interest rates in three key ways: easing inflation in administered prices which are growing around 7%yoy; cutting government spending as it’s around a record high share of GDP which is making it hard for private spending to pick up without causing capacity constraints and hence inflation; and implementing policies to enhance productivity growth like deregulation and tax reform in order to boost the economy’s capacity to supply goods and services. So, reports that the May budget will contain a productivity package, a savings package and possibly tax reform are to be welcomed. The key is that the productivity reforms be hard-nosed and broad based, government spending is actually cut in real terms such that Federal Government spending falls back to 25% of GDP or less and that tax reform be more than just a cut to the capital gains tax discount - otherwise it will just be a tax hike.

Overall, our view remains that this year will see a volatile ride for investors on the back of geopolitical threats including around Iran, Trump related noise, the US midterm elections, interest rate uncertainty and worries around AI and tech valuation issues. So, we continue to expect a 15% or so correction in the next six months. But ultimately, we see it turning out okay for shares with reasonable returns on the back of good global economic and profit growth, Trump focussing on policies to help US households ahead of the midterms, the Fed cutting rates once or twice more, and profit growth turning positive in Australia.

Major global economic events and implications

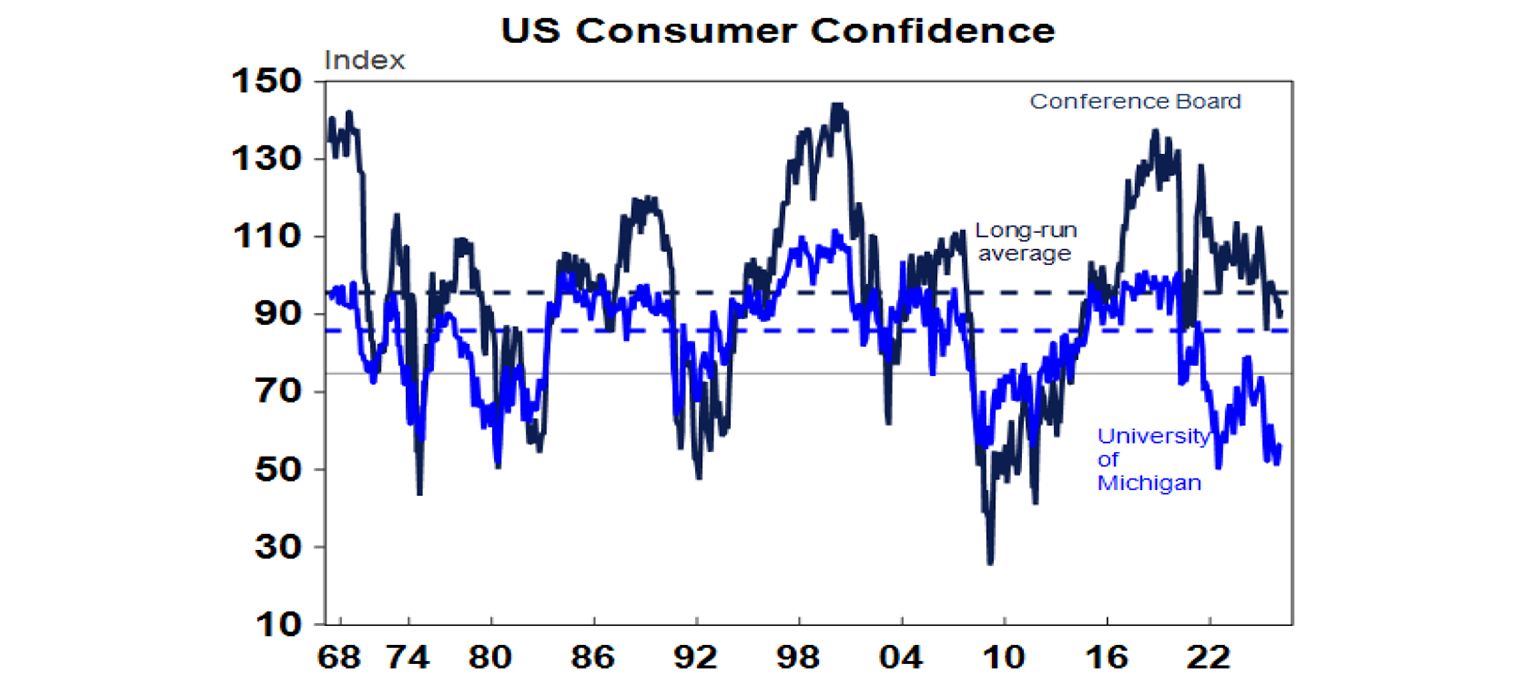

US data was pretty uneventful. Consumer confidence rose slightly in February according to the Conference Board survey but remains subdued. Home price growth came in stronger than expected in December.

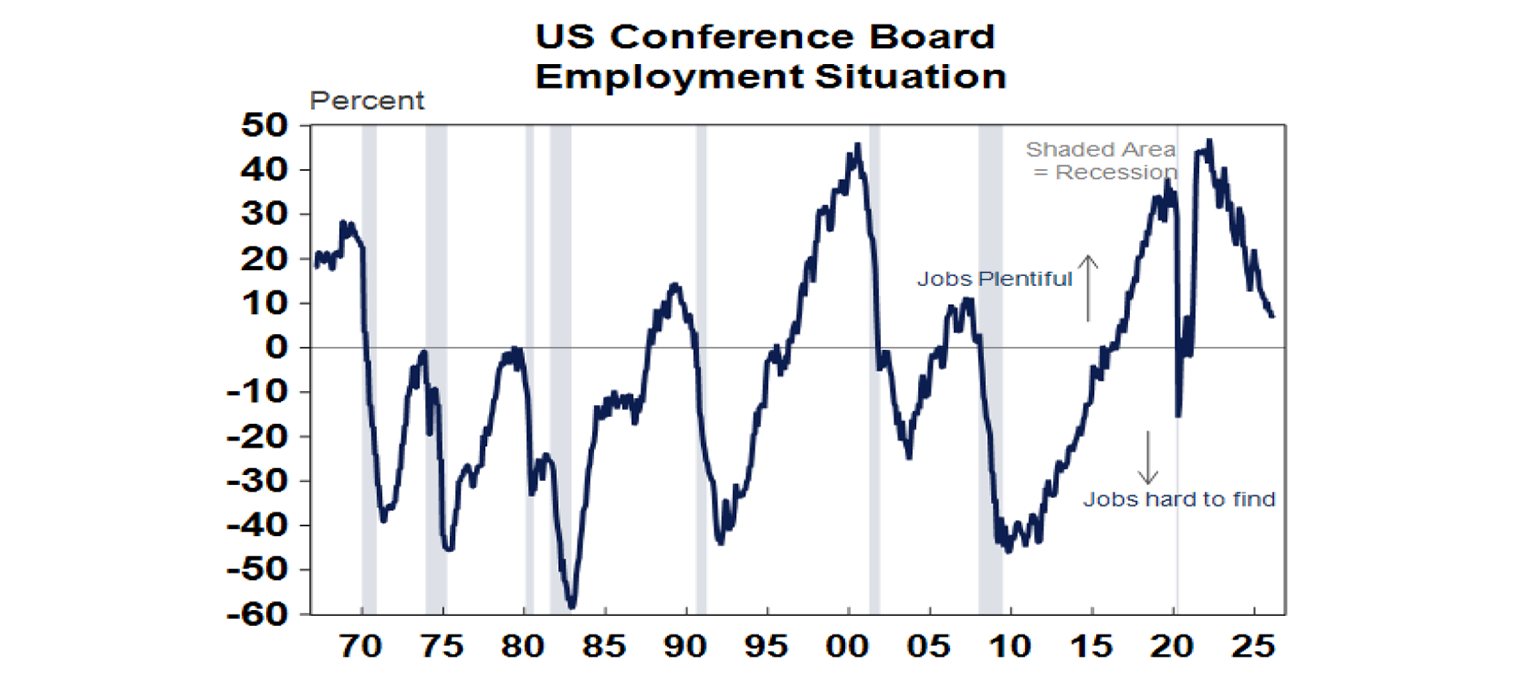

US jobs data was mixed. Consumers perceptions of whether jobs are plentiful or hard to find improved slightly but remains in a downtrend. Meanwhile, initial jobless claims remain low. The signs of a broader stabilisation or possible improvement in other jobs data is continuing to see the Fed shift in a less dovish/more hawkish direction with the two key doves at the Fed (Governors Waller and Miran) appearing to wind back their dovishness. Higher than expected producer price inflation for January pointing to a rise in core PCE inflation to 3.1%yoy and possibly more tariff pass through will also keep the Fed wary.

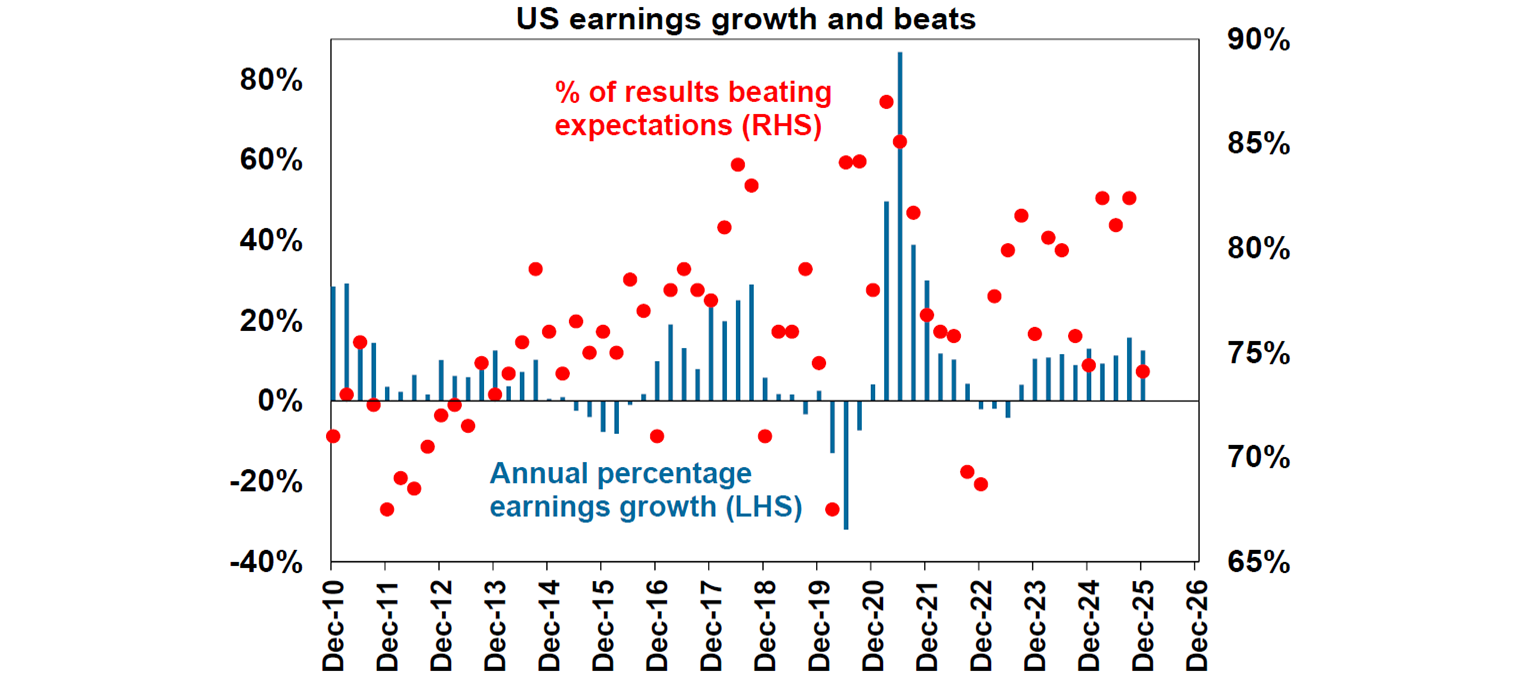

96% of S&P 500 companies have reported December quarter earnings, with 74.1% beating expectations, below the norm of 76.6%. Consensus earnings growth expectations are running at 12.6%yoy, up from an expectation of 8.8%yoy in late January. Tech saw earnings up 28%yoy, financials up 10%yoy and materials up 15%yoy.

Japanese data was mixed with industrial production up in January by less than expected, but retail sales rising strongly. Core inflation in Tokyo rose in February but only to 1.5%yoy. Overall, it’s consistent with the Bank of Japan remaining gradual in normalising interest rates.

Australian economic events and implications

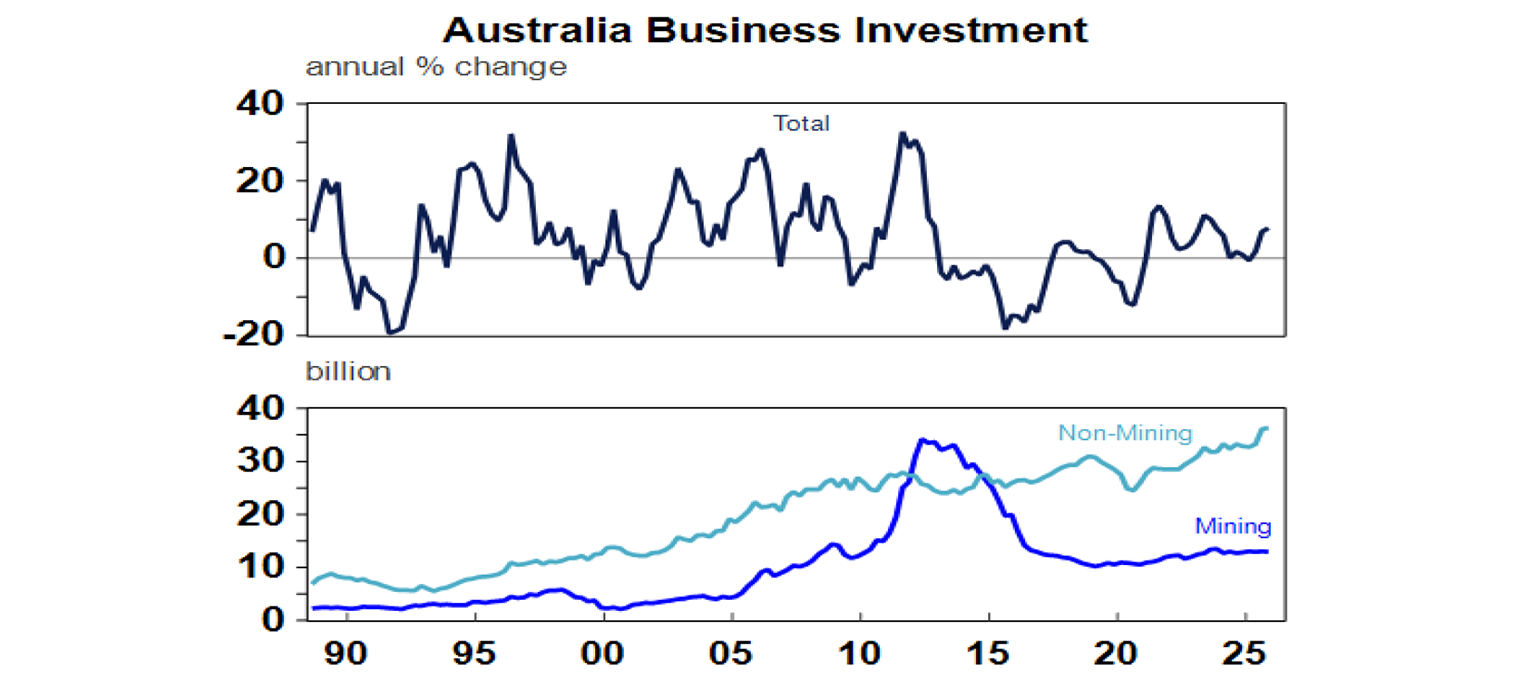

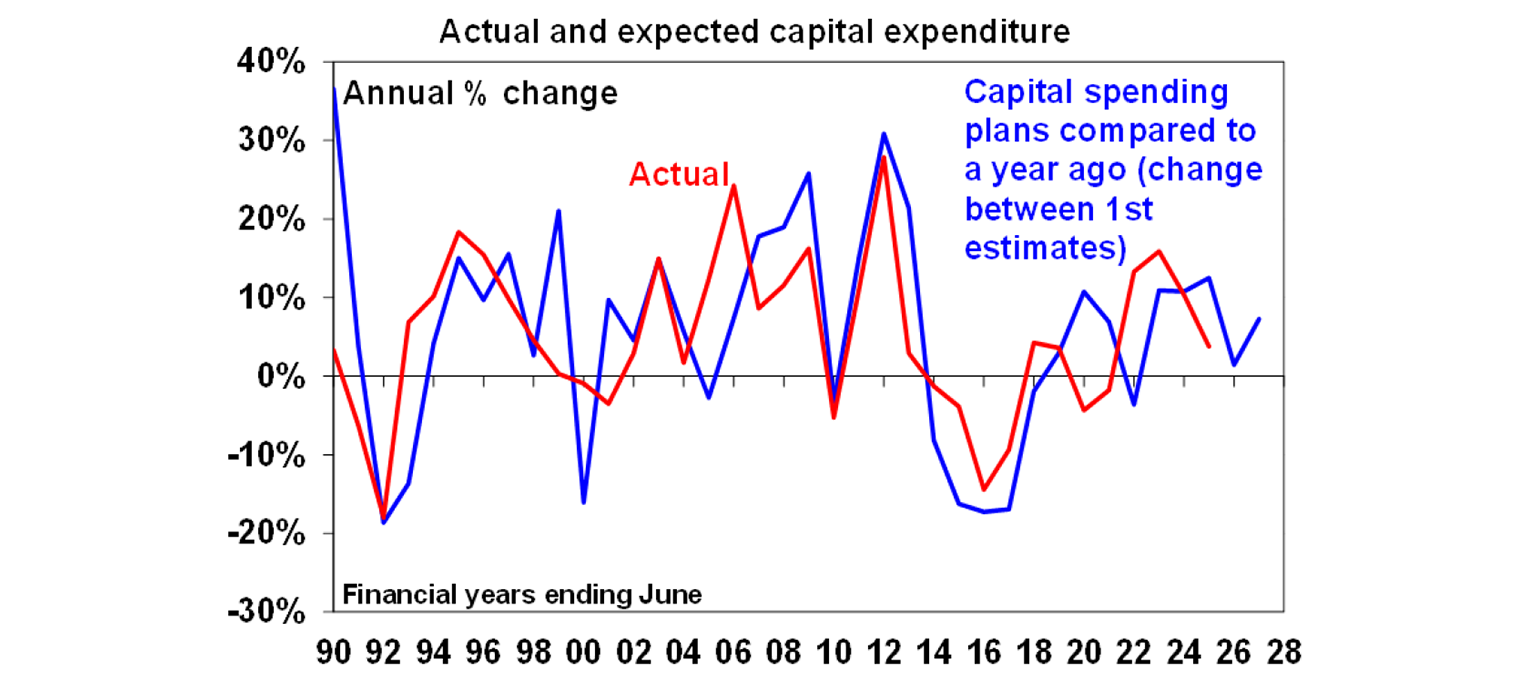

Australian business investment in the December quarter was soft. It rose 0.4%qoq with buildings up but plant & equipment down after a spike in IT data centre investment in the September quarter. While mining investment is flat non-mining investment is rising and annual growth is solid..

Investment spending plans remain solid pointing to a rise of around 8% this financial year and 7% next financial year.

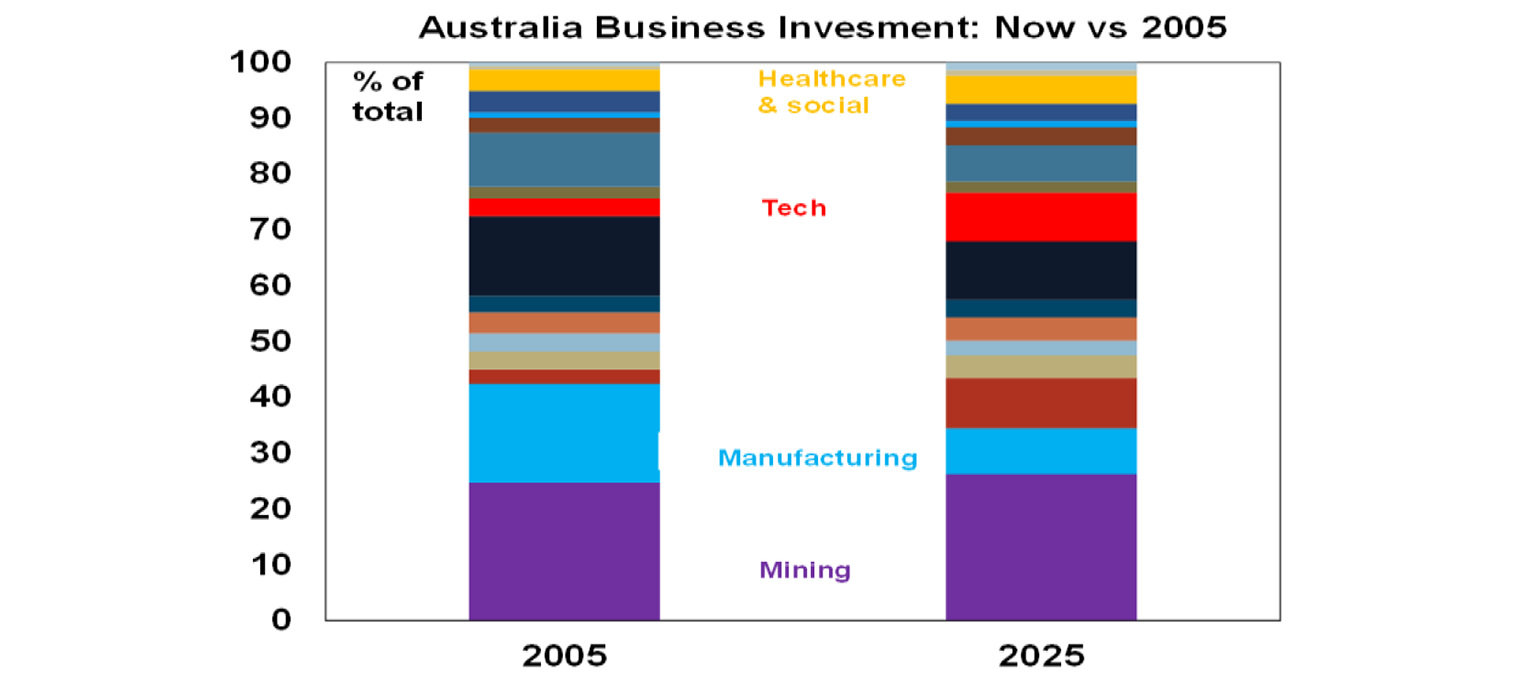

While IT investment fell back a bit in the December quarter its way up as a share of total compared to 2005 whereas manufacturing investment is way down.

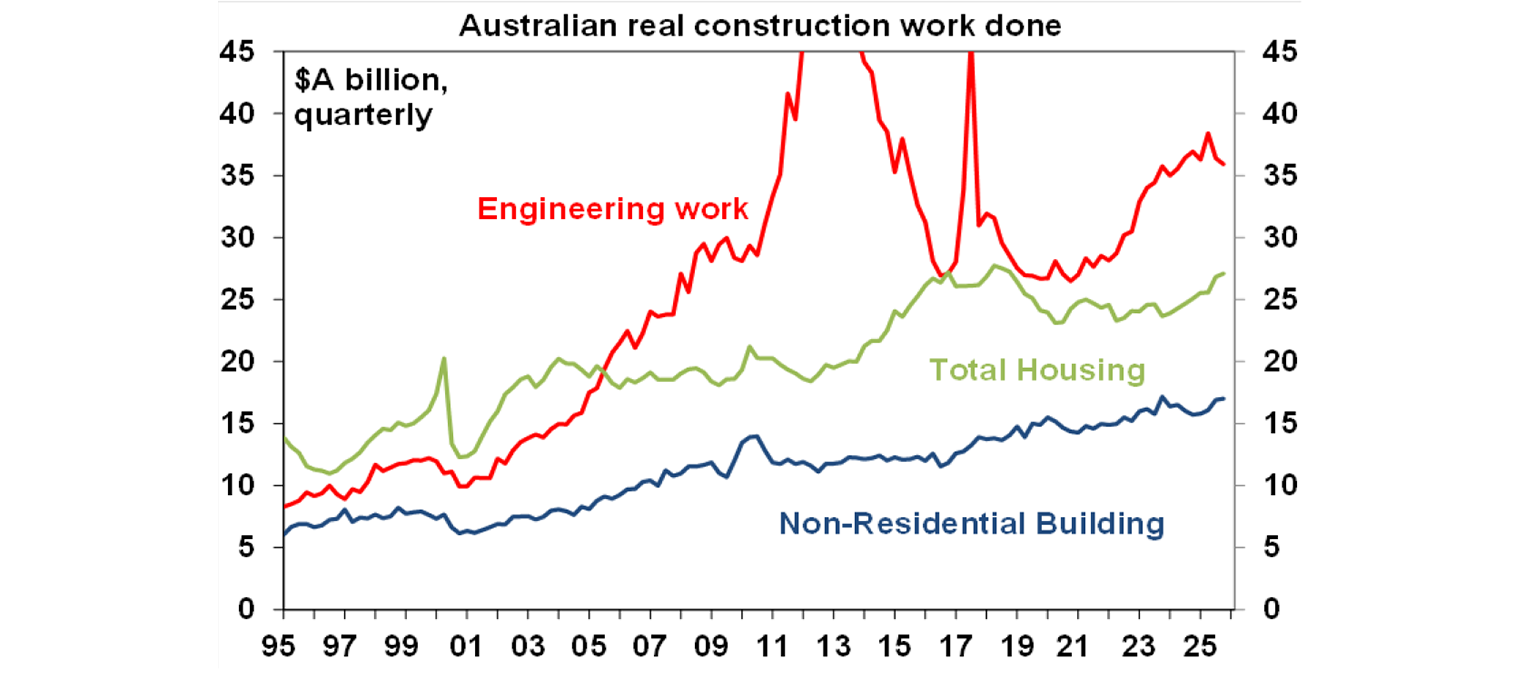

Construction spending fell 0.1% in the December quarter with housing investment continuing to trend up but engineering activity down.

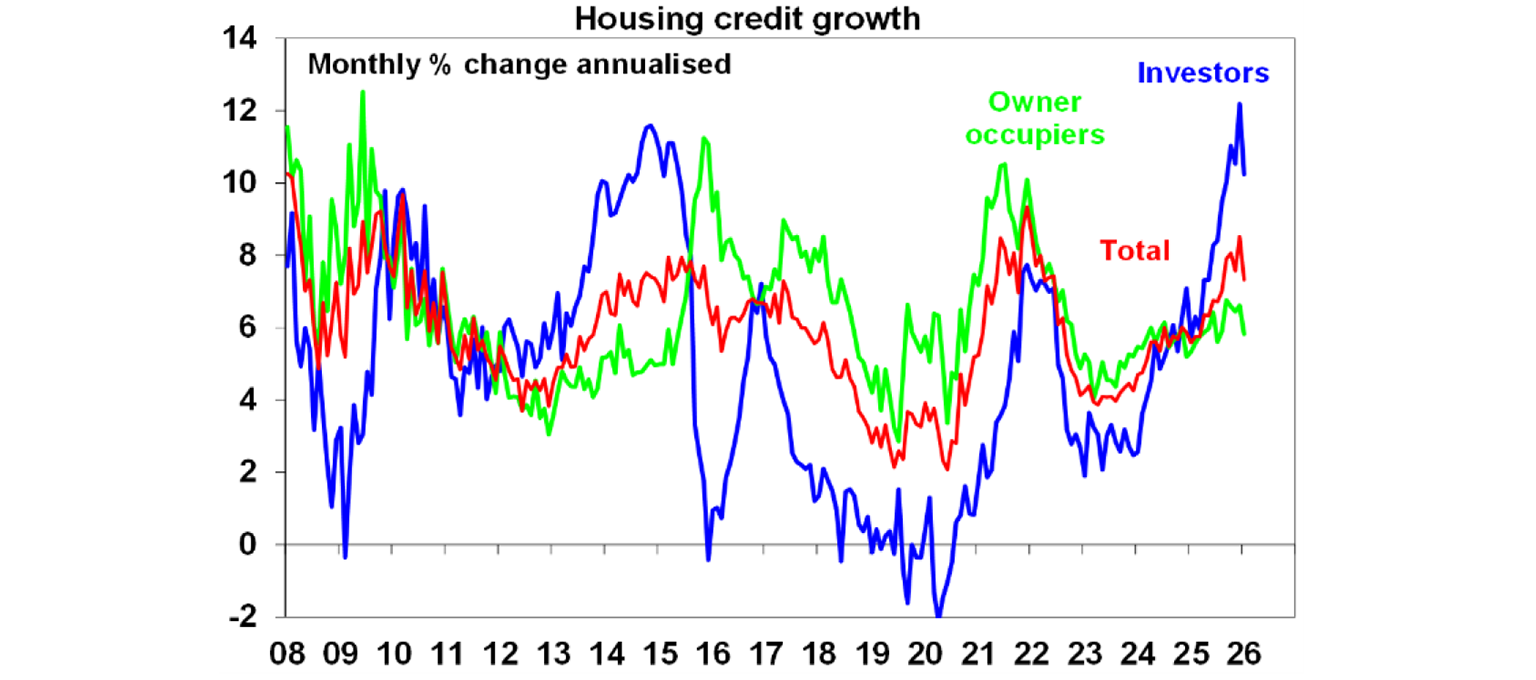

Private credit growth slowed slightly in January across housing, personal and business suggesting it could just be seasonal noise around December/January, but RBA rate hikes may start to impact in the months ahead. Investor housing credit growth is still around its prior 2014 high.

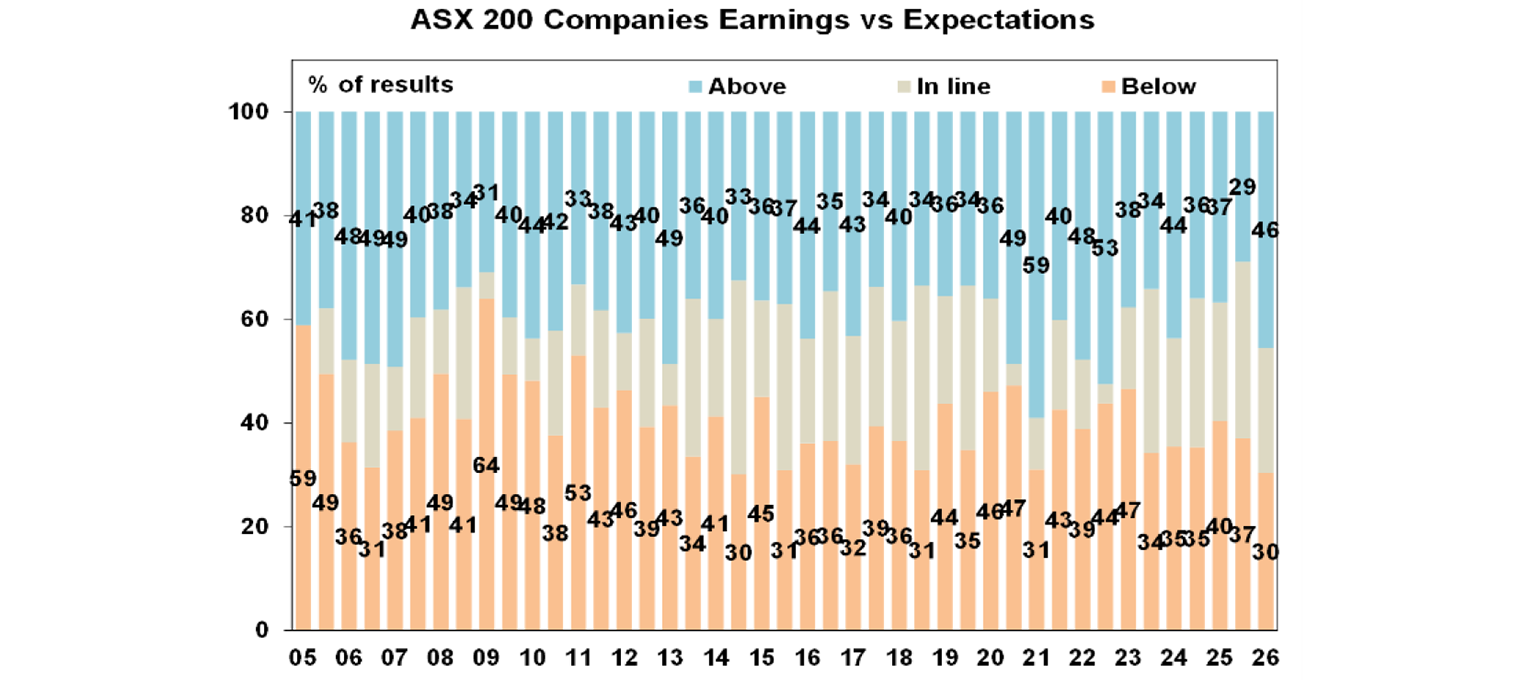

The Australian December half earnings reporting season is now complete and has confirmed a return to profit growth. As is often the case, the strength of results tailed off over the last week as more small caps reported. However, the consensus expectation for earnings growth for this financial year is now 13.6% which is up from 11.7% a few weeks ago and 7% in November. This follows three years of falling profits with the turnaround mainly driven by a 33% surge in mining profits, with banks seeing around 9% growth, energy seeing an 18% fall and the rest of the market seeing profit growth around 4%. Upside surprises surpassed downside surprises by 1.5 to 1 and the return to profit growth has been a key factor propelling the Australian share market higher this year.

46% of results surprised expectations on the upside, which is more than the norm of 40%, and 30% have surprised on the downside which is less than the norm of 41%. This is the best since the emergence from the pandemic.

56% of companies have seen earnings rise on a year ago which is a dip from the June half reporting season but still in line with the norm amidst a rising trend.

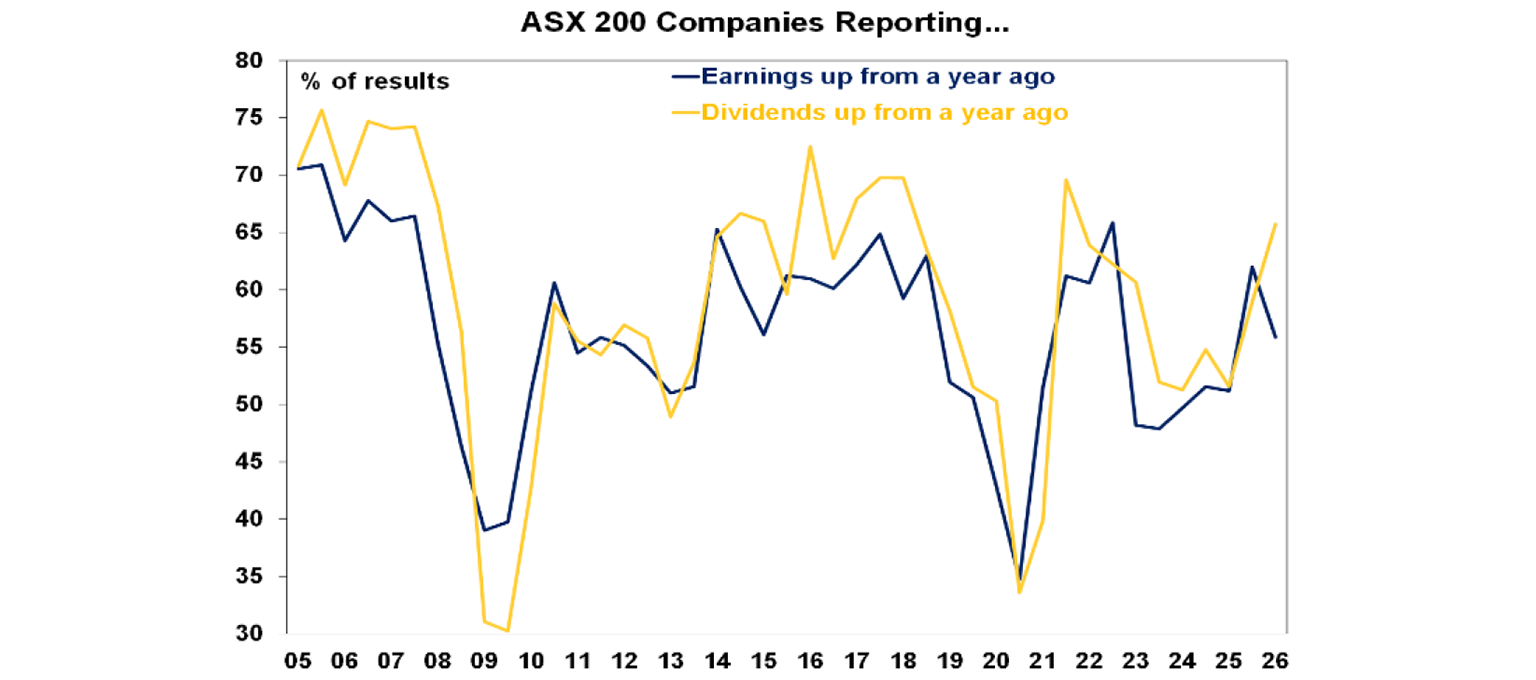

What’s more 66% of companies have increased their dividends, which was above the norm of 59%. Rising dividends are a sign of confidence that earnings will continue to rise.

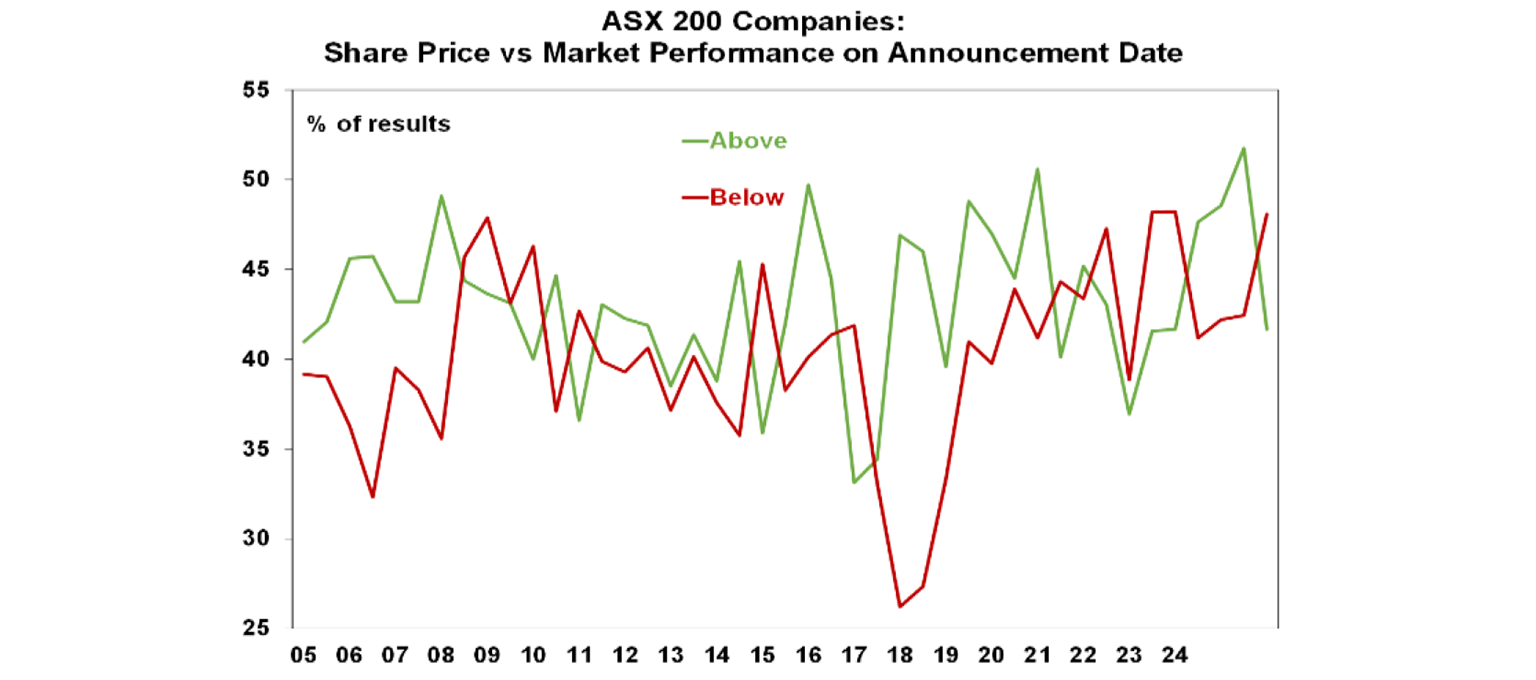

But with expectations running high there were some extreme reactions to results with some big falls in individual stocks even when they beat. In fact, this reporting season saw more companies see their share price underperform the market on the day they reported than outperform.

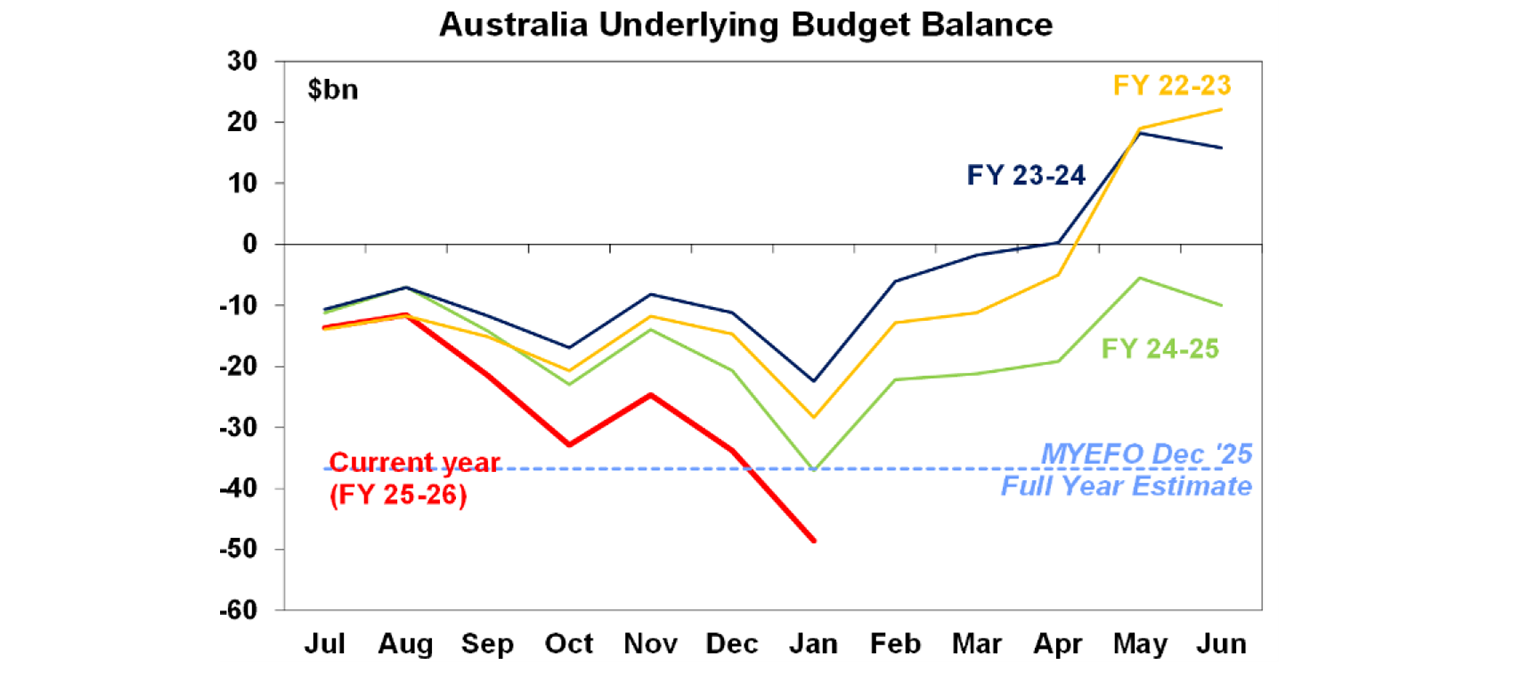

The budget deficit is sliding deeper into deficit but looks on track to come in about $5-10bn better than the MYEFO projection for $37bn. While government spending growth is very strong (running at 8%yoy or 14%yoy depending on how its defined), the “good luck” with stronger than expected corporate tax collections has continued resulting in the deficit running lower than expected.

What to watch over the next week?

In the US, the focus will be February jobs data (Friday) which are expected to show a fall back in jobs growth to around 60,000 and unemployment staying at 4.3%. In other data, expect the ISM manufacturing conditions index (Monday) to remain around an okay 52, the services ISM index (Wednesday) to remain around 54 and January retail sales (Friday) to be soft partly due to poor weather.

Eurozone inflation data for February (Tuesday) is expected to show core inflation around 2.2%yoy and January unemployment (Friday) is around 6.2%.

Chinese business conditions PMIs for February (Wednesday) are expected to remain in the same soft range they have been in for the last few years.

In Australia, December quarter GDP (Wednesday) is expected to show economic growth of 0.5%qoq or 2%yoy driven by solid consumer spending, a rise in dwelling investment and modest growth in business investment but with a slight detraction from trade. In other data, expect Cotality figures for February to show a further slowing in home price growth (Monday) to 0.6%qoq with Sydney and Melbourne showing prices flat, building approvals (Tuesday) showing a 10% bounce, household spending for January up 0.8%mom or 5.4%yoy and the trade surplus (both Thursday) is expected to remain around $3bn. Speeches and remarks by RBA Chief Economist Sarah Hunter (Monday), Governor Bullock (Tuesday) and Deputy Governor Hauser (Saturday) will be watched for any comments regarding the January jobs and inflation data and implications for interest rates.

Outlook for investment markets

Global and Australian share returns are expected to remain reasonable. Stretched valuations, political uncertainty associated with Trump & the midterm elections, AI bubble & tech valuation worries, and geopolitical risks are the main drags. But returns should still be positive thanks to Fed rate cuts, Trump’s consumer friendly pivot and solid profit growth. The return to profit growth should also support gains in Australian shares even though the RBA has increased rates and may do more. Another 15% or so correction in share markets is likely along the way though.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to 5% or less due to poor affordability, the RBA raising rates with talk of more to come and APRA’s move to ramp up macro prudential controls.

Cash and bank deposits are expected to provide returns around 3.85%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA holds or hikes. Fair value for the $A is around $US0.72.

You may also like

-

Weekly market update - 07-08-2026 Shares at all time highs (again) despite Middle East War rollercoaster, Japanese yen & the Disneyland index, Aussie consumers still spending despite rate hikes, and RBA to hold rates but hike can still come later this year -

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.