Oliver's insights

Investment outlook Q&A – oil, bond yields, the Budget and the RBA

While there was much angst when the US/Israel War with Iran led to the closure of the Strait of Hormuz at the start of March with a surge in oil prices, falls in shares and talk of a stagflation/risk of global recession, the fallout so far has been modest.

9 min read

Key points

The oil supply shock remains a significant threat to economic growth and shares – particularly with the Strait of Hormuz remaining closed and oil reserves running down.

It’s contributing to rising bond yields and putting pressure on share market valuations.

The tax changes in the Budget will make shares and super relatively more attractive investments and favour high yielding over growth investments (ie, less risk taking).

The Budget contains good moves to deregulate, but little real tax reform with public spending remaining too high.

Introduction

This note takes a look at some of the main questions investors have in a simple Q&A format, particularly around the oil supply shock, global bonds, China, the Australian Federal Budget and the RBA.

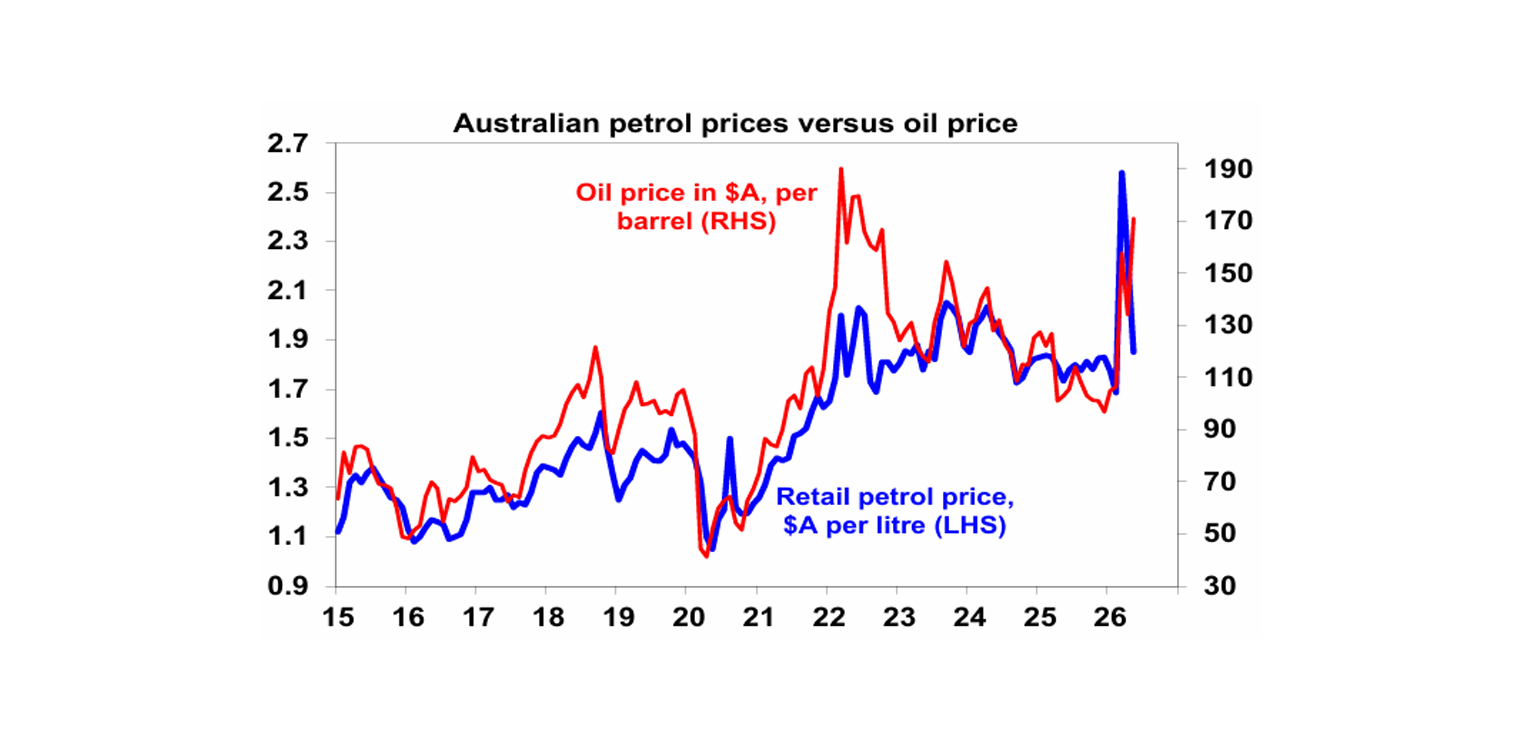

What happened to the oil supply shock?

While there was much angst when the US/Israel War with Iran led to the closure of the Strait of Hormuz at the start of March with a surge in oil prices, falls in shares and talk of a stagflation/risk of global recession, the fallout so far has been modest. In Australia, petrol prices are only just above where they were before the War began. What gives?

The global economy so far has been protected by the drawdown of oil stockpiles, the diversion of some fuel via other routes, fuel tax cuts, just in case buying, expectations that it will be temporary aided by Trump’s regular soothing comments to the effect it will soon be over and the AI boom in the US. However, the Strait is still closed, hopes for an imminent deal are fading and Trump is renewing his threats against Iran. Trump clearly wants to TACO but his threats have started to lose credibility. That’s always a risk when playing the “madman” in negotiations - and Iran looks happy to string it out. The trouble is that the world can’t keep running down oil stockpiles and sooner or later oil demand will have to adjust to a 10-15% reduction in global supply – with the International Energy Agency estimating global oil supply is down 13%. Rough estimates suggest this would require oil prices to rise to around $US150/barrel. Past experience tells us that oil crises impact oil prices, shares and economies with a long lag. For example, the full impact on oil prices unfolded over four months in the first oil shock in 1973 and over a year in the second oil shock in 1979. Hopefully, we are right and a deal is soon reached. If not, the risks of a much bigger boost to inflation/hit to growth will rise with a flow on to shares. The chart above shows that having overshot on the upside in March, Australian petrol prices have now overshot on the downside (even with the 32 cents fuel tax cut) & are at risk of rebounding.

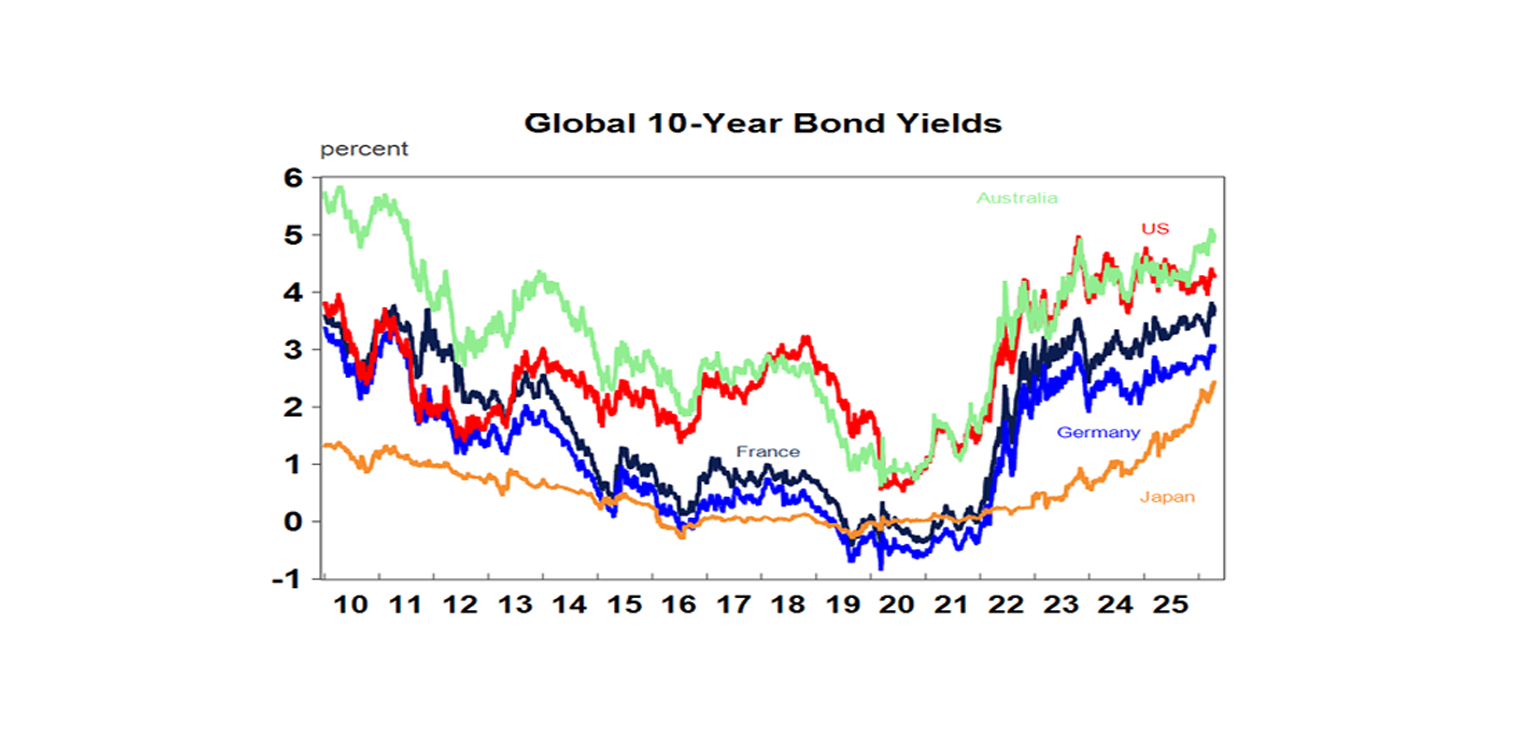

Why are bond yields rising?

Rising bond yields reflect worries that rising oil prices will boost inflation, central banks will have to raise rates, the US budget deficit is blowing out and US capex remains strong with data centre spending. This is boosting borrowing costs for corporates and US home buyers and to a lesser extent for Australian home buyers by rising fixed mortgage rates.

Are shares expensive or cheap?

The rising trend in bond yields at a time of relatively high price to earnings ratios, particularly for US shares, leaves share valuations stretched with both US and Australian shares offering little risk premium over bonds. This has been the case for the last two years now so it’s no guide to timing, but indicates shares remain vulnerable if the news flow turns more negative.

What happened to the threat from US tariffs?

US tariffs have taken a back seat lately but are still bubbling away. The Trump Administration is now starting to pay out refunds for the reciprocal and Fentanyl tariffs the US Supreme Court declared illegal which could amount to $US166bn. This will lead to a temporary fiscal stimulus and budget deficit blow out. Those tariffs were then replaced with a temporary 10% tariff (under section 122) from late February that will expire on 24th July, but these have also been ruled illegal by the US Trade Court which will likely lead to another round of appeals. In any case they will likely be replaced by more permanent section 301 tariffs taking them back to where they were before the Supreme Court decision. Meanwhile from a peak of nearly 12% the average effective US tariff rate has fallen back to below 10% thanks to import substitution. It’s still way up on where it was at the start of last year…so still adding to US costs and distorting trade. Though, worst case scenarios have been avoided because other countries decided last year to take the “high road” and avoid a trade war with the US. And the trade truce between the US and China - extended by the recent Trump/XI summit - has avoided a trade war between the world’s two biggest economies (although the underlying structural tensions remain).

What about China?

China continues to face big challenges: a falling population; trying to get consumer spending to take over as a key growth driver; and political tensions with the West. The return of Trump last year saw a renewed flare up in tensions, but they have been defused with the trade truce. In the meantime, China simply diverted its exports to other countries. Chinese economic activity data was weaker than expected in April, but this looks like payback from stronger than expected March quarter growth. However, Chinese growth is likely to continue to muddle along with growth this year expected to be around 4.5%.

What does the Australian Budget mean for investors?

Because of the removal of existing property purchases from negative gearing, the shift to taxing real capital gains for all assets with a 30% minimum rate and the new minimum tax rate of 30% on distributions from discretionary trusts the Budget is the most consequential for investors in years. At a high level for investors this will:

Reduce the after-tax return from investing in existing property.

Favour new home builds over existing property (which means a narrower and potentially more problematic choice set).

Boost the relative attractiveness of shares and commercial property relative to residential property as they can still be negatively geared.

Favour high rental yielding residential properties over lower rental yielding properties as these are less dependent on capital growth.

Favour high yielding assets over lower yielding growth investments.

Make fixed interest and bank deposits relatively more attractive

Make crypto and gold relatively less attractive as they are dependent on capital growth which will potentially now be taxed at a higher rate.

Boost the relative attractiveness of super – because it retains its concessional tax treatment.

Boost the attractiveness of the family home as it remains CGT free and could also be converted into a negatively geared investment property at some point. It could lead to more renovations.

Make high turnover investment trading strategies less attractive because of potentially higher capital gains tax bills.

In short, the tax changes are likely to drive an increased focus on high yielding investments at the expense of those more focussed on capital growth which could mean a decline in risk capital in Australia.

How does the Budget stack up against my wish list?

Prior to the Budget, I produced a “wishlist” of the top five things needed in the coming Budget. These were to limit any “cost of living” relief, cut spending, undertake serious tax reform, less red tape and more incentives to invest, and to reform the Charter of Budget Honesty. On each of these:

There wasn’t a lot of extra “cost-of-living” relief beyond the temporary fuel tax cut, with the $250 tax offsets more than two years away. This gets a tick.

However, there was nowhere near the Keating like reduction in public spending that is necessary - $100bn or 2% of GDP over four years – to free up spare capacity in the economy and take pressure off inflation. Sure, there were spending savings later this decade – but these are dependent on the savings to the NDIS occurring as promised, no boost to spending ahead of the next election and still leave Federal spending well above pre-COVID average levels. And there is actually increased spending in the near term, so this gets a cross.

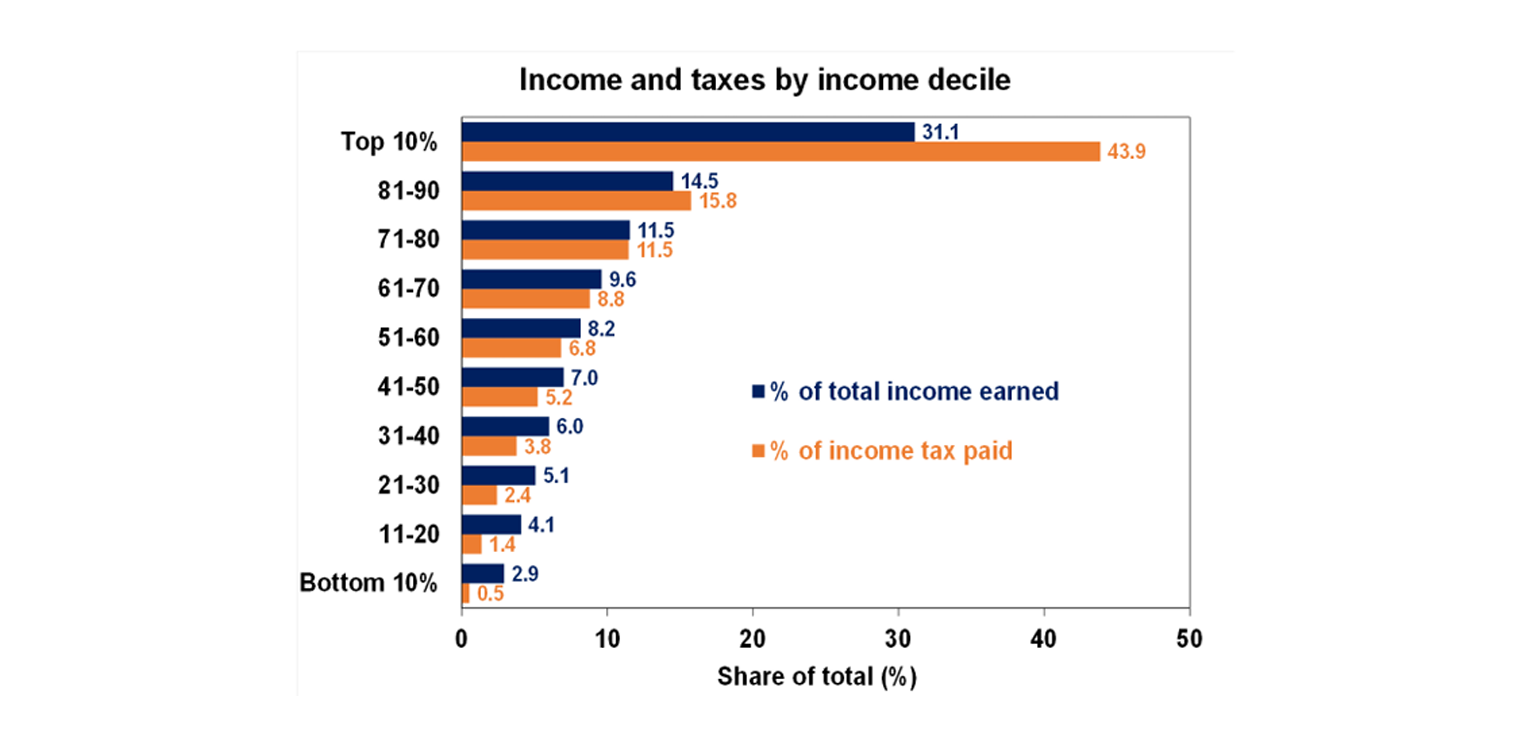

There was a tilt at some tax reform, but this was more about tax hikes than tax reform. The Australian tax system should be moving from a very high reliance on taxing income to a greater reliance on taxing consumer spending in order to boost incentive and improve intergenerational equity. The Australian income tax system is also very progressive compared to other countries with a high top marginal tax rate kicking in at a low multiple of average earnings leading to the top 20% of taxpayers accounting for 60% of income tax paid, even with various tax concessions. See the next chart.

This in turn has motivated a high use of the tax concessions but, with their curtailment, the already very progressive nature of the tax system will become even more so. That will lead to further disincentive and work against the aim of boosting productivity. This may be compounded if the CGT changes lead to less capital being available for startups, private capital and growth stocks. Ideally the curtailment of the tax concessions should have been matched by lower income tax rates. So, it’s hard to tick the tax reform box so far.

In terms of regulation and investment there were some good moves – with less red tape and moves to encourage investment mainly for small business. There was no move to unwind labour market re-regulation though. Overall, this gets a tentative tick

Finally, the Budget with its further boost to “off budget” spending – with actual budget deficit being $64.1bn more than double the $31.5bn underlying deficit that gets the focus - and an ongoing lack of fiscal rules continues to lack the discipline seen in times past.

Where does this leave the RBA?

The RBA is well aware that raising rates won’t make high oil prices go away but is rather responding to a pre-existing inflation problem in Australia - with underlying inflation around 3.3%yoy running well above target before the War – and seeking to make sure that the War does not make it a lot worse. The extra near-term stimulus in the Budget does not make the RBA’s job any easier but it’s not enough to change our prior expectations for the RBA to hike rates once more, probably in August. Through next year though, the RBA will probably be back to cutting rates.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Weekly market update - 07-08-2026 Shares at all time highs (again) despite Middle East War rollercoaster, Japanese yen & the Disneyland index, Aussie consumers still spending despite rate hikes, and RBA to hold rates but hike can still come later this year -

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.