Weekly market update

Investment markets and key developments

The deal provided a boost for global share markets with US shares up 0.9% for the holiday shortened week to Thursday with a more hawkish Fed limiting the gains and US futures falling 0.2% on Friday due to a delay to the start of US/Iran talks towards a permanent deal.

9 min read

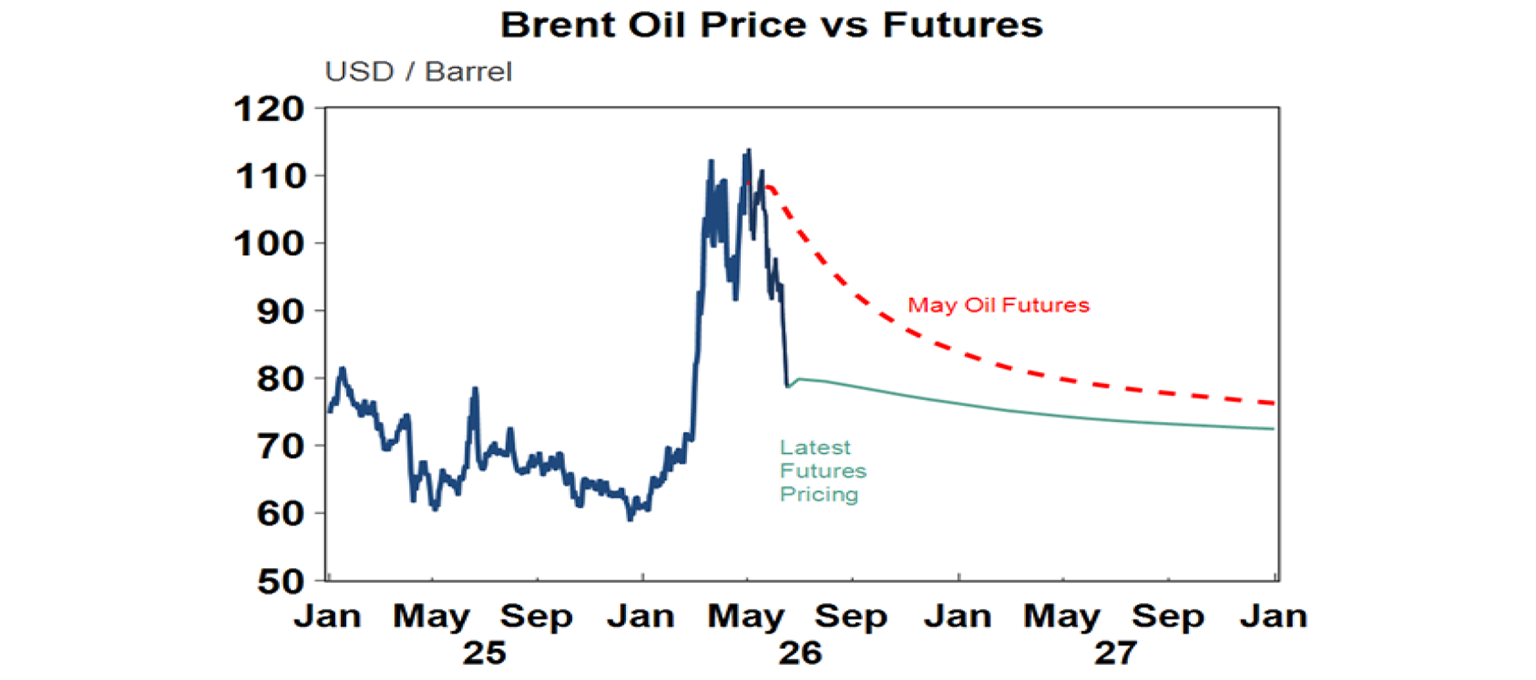

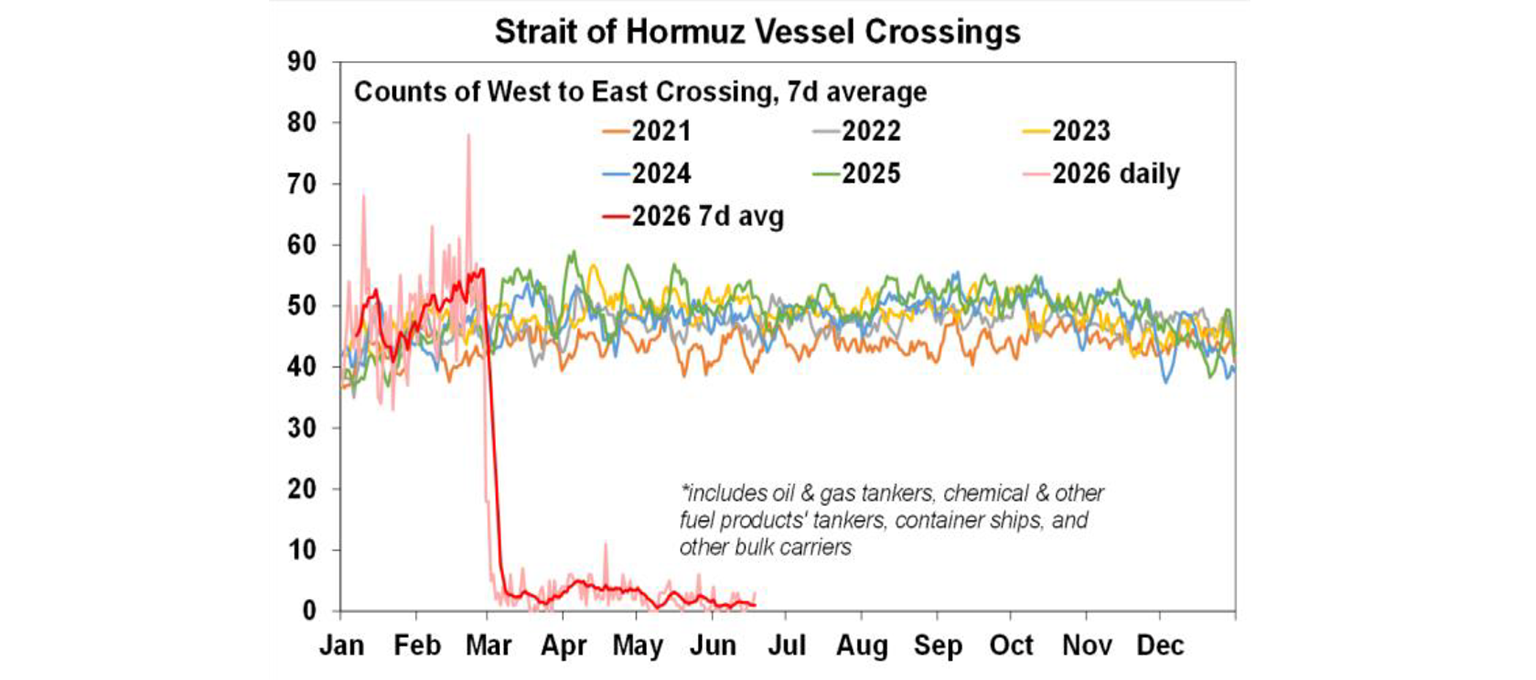

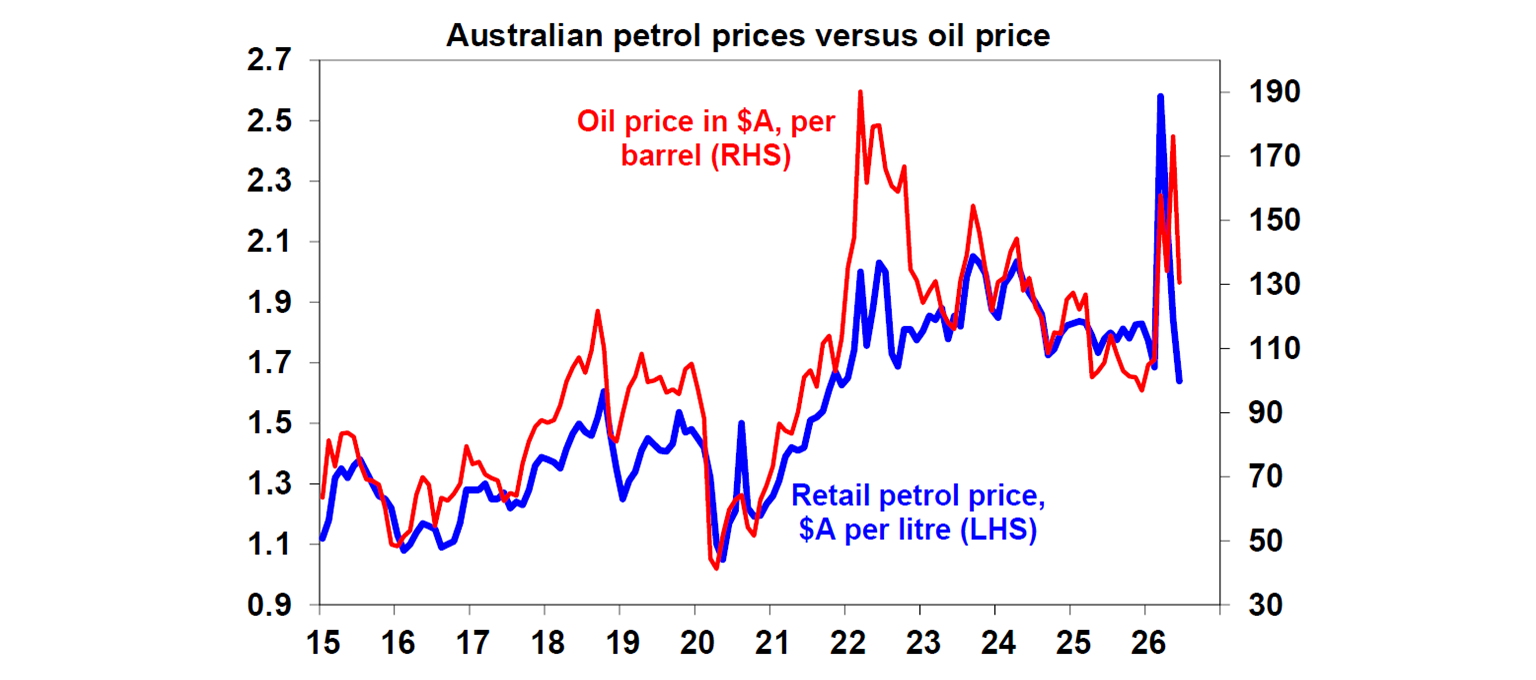

The past week saw good news with the US and Iran at last signing a peace deal that will, at least in theory, reopen the Strait of Hormuz. While a deal had already been anticipated its confirmation and reports that sanctions on Iranian oil would be lifted saw oil prices fall further taking them to around $US10 a barrel above where they were before the War started at the end of February, despite a slight set back on Friday.

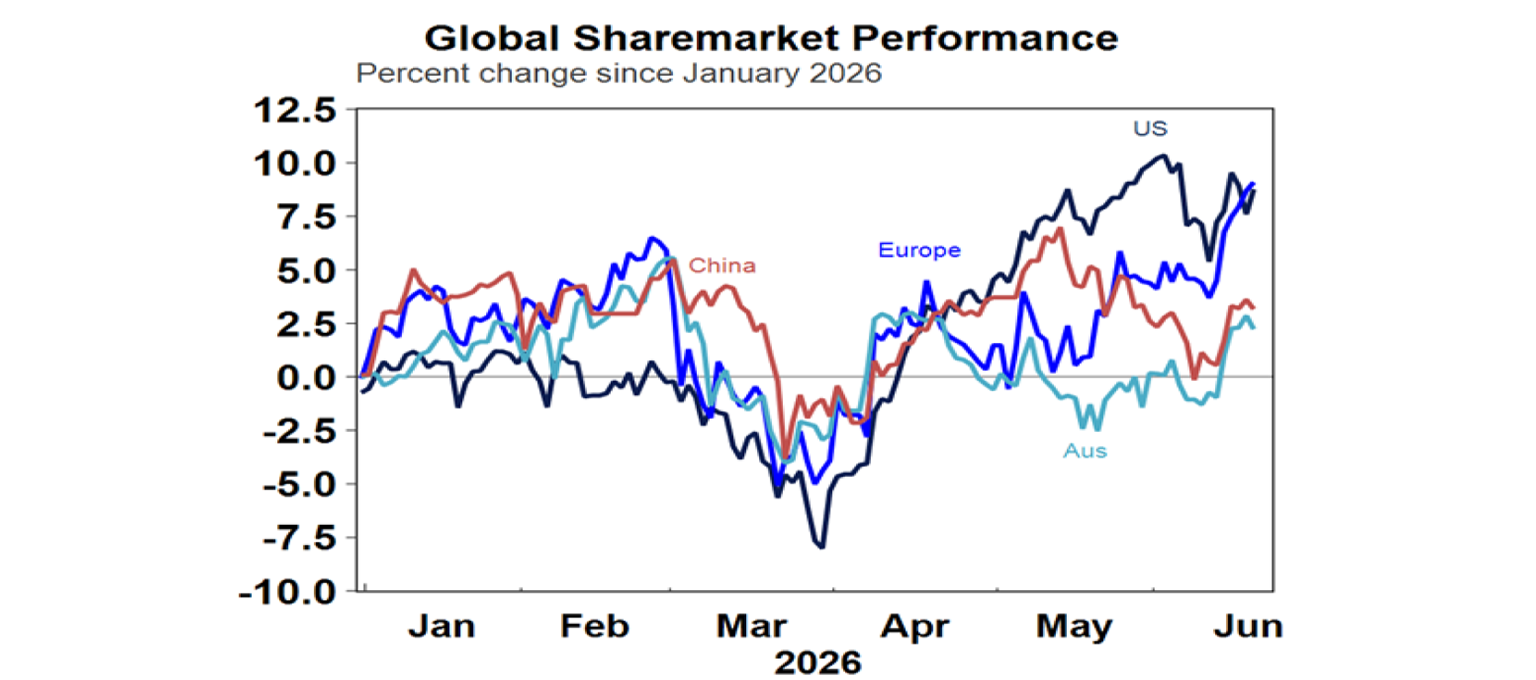

The deal provided a boost for global share markets with US shares up 0.9% for the holiday shortened week to Thursday with a more hawkish Fed limiting the gains and US futures falling 0.2% on Friday due to a delay to the start of US/Iran talks towards a permanent deal. Eurozone and Japanese shares reached new record highs with Eurozone shares up 1.4% for the week and Japanese shares up 7.9%. Chinese shares also rose with a gain of 3.4%. Australian shares were helped by the positive global lead but only rose 0.3% for the week not helped by a fall in BHP after it announced a project cost blow out. Gains on the ASX were led by health, finance and retail shares but these were largely offset by falls in energy, utility and telco shares. Australian shares remain relative underperformers so far this year as RBA rate hikes, worries about the impact of the Iran war and Budget tax changes have impacted.

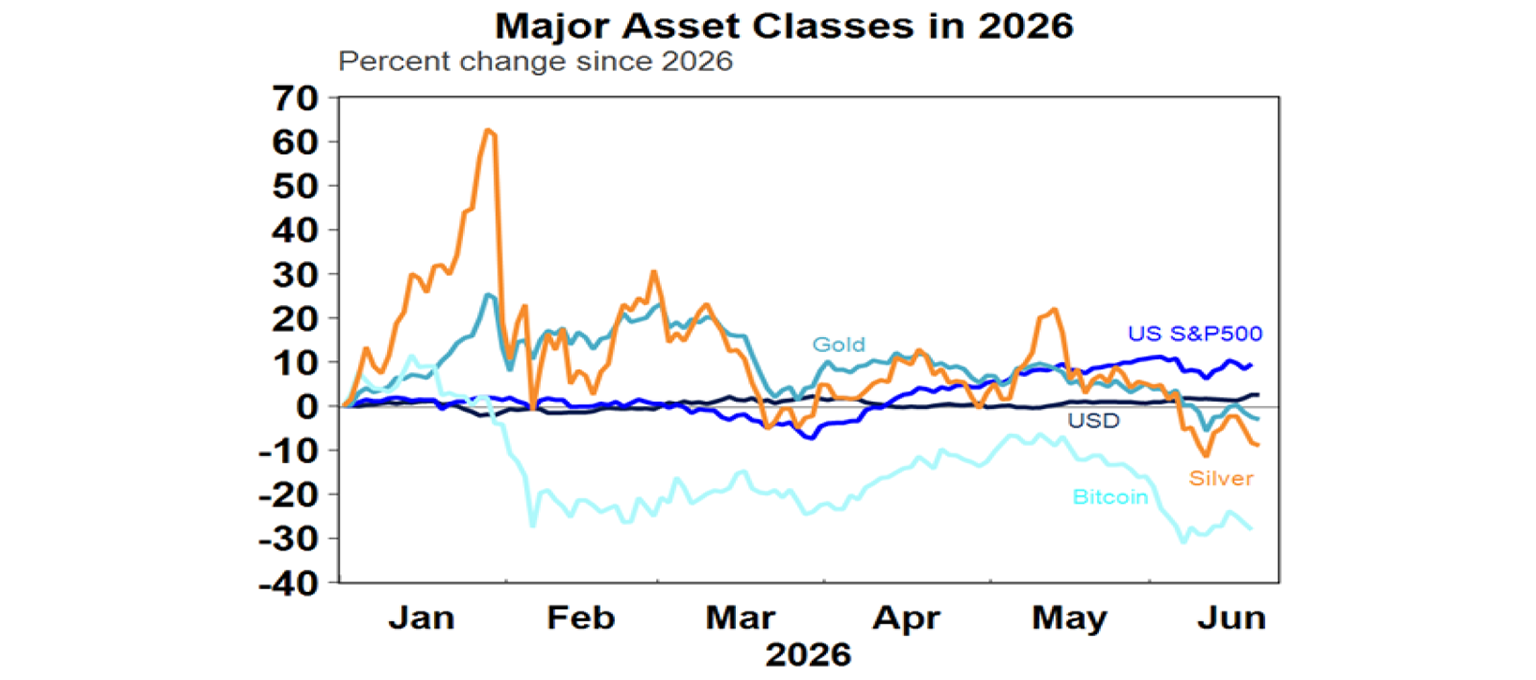

Bond yields initially fell in the last week helped by the further fall in oil prices but ended mixed with only small changes – down slightly in the US and Germany, flat in Australia and up slightly in Japan. Prices for copper, gold and iron ore fell as did Bitcoin and the $A, as the $US rose on the back of a more hawkish Fed.

The US/Iran deal is good news and likely removes a worst case stagflationary scenario, but it could all still flare up again. The deal basically extends the ceasefire by 60 days with flexibility to extend it further, with a phased reopening the Strait of Hormuz and removal of sanctions on Iranian oil with negotiations to commence towards a final agreement over Iran’s nuclear program in return for the release of frozen Iranian assets and establishment of a $US300bn rebuilding fund. Both sides have an incentive to support the deal – Trump to avoid high gasoline prices ahead of the mid-terms and Iran to avoid further bombing - and in the near term this supports lower oil prices and removes a big risk hanging over the global economy. However, Iran’s nuclear program is still not fully resolved (yes it reiterated that it will never produce nukes but its been saying that for years), it retains a large stockpile of missiles and retains an ability to support its regional proxies like Hezbollah and Hamas. All of which suggests that we are back where we were before the War started with nothing resolved. If anything, Iran is now stronger having shown it can easily stop ships through the Strait of Hormuz. So, it all begs the question – what has been achieved despite the huge cost of the War? It does look like Iran won. And its already looking very fragile with Iran delaying the start of talks towards a permanent deal due to fighting in southern Lebanon, although Israel and Hezbollah have reportedly since agreed to yet another ceasefire, and Iran is insisting that ships moving through the Strait will need its permission and “insurance” from it potentially setting up a disagreement about tolling. So, it could all flare up again, particularly after the mid-term elections are out of the way as political pressure on Trump to back down recedes!

The back down on Iran coming on top of the US back down in its trade war with China – highlights perceptions that it’s in relative decline and lacks the stomach to follow through to complete victory. Which in turn is consistent with increasing geopolitical instability as the US is in retreat as the world’s cop. But of course, that’s a separate issue!

Back to oil prices – in the short term further declines may be limited as a deal was largely already priced in and it will take a while for Middle East energy production and flows through the Strait to return to normal and markets are likely to price in a risk premium to allow for the risk it could all flare up again. So global central banks are likely to be wary of relaxing too much regarding the threat to inflation. However, past oil price shocks have eventually been followed by a big fall in prices as higher oil prices encourage more supply and kill more oil demand and this time is unlikely to be any different. But that’s more of an issue for 2027-28.

The peace deal may not necessarily lead to a further fall in Australian petrol prices just yet – much depends on what happens to the fuel tax cut. At around $1.64 a litre they are below where they were before the War started! This reflects the $0.32 fuel tax reduction that is scheduled to end this month, implying a rebound to around $1.96 a litre if the tax cut is reversed. But as the decline in global oil prices over the last month gradually flows through the petrol price is likely to settle around $US1.75. In other words, up from pre-War levels but not significantly so and in the range of the last few years. Of course, it the fuel tax cut is continued petrol prices could drift another 10-20 cents or a litre lower from here as the oil price fall flows through. Economics suggests that the fuel tax cut should end as scheduled – as it adds to the Budget deficit, will only boost spending when the RBA is trying to slow it and there are better ways to help those who need it. But the Government is under pressure from One Nation promising to halve fuel excise for 3 years.

While there was good news on the US/Iran conflict, the past week also saw a further drift towards higher interest rates by central banks.

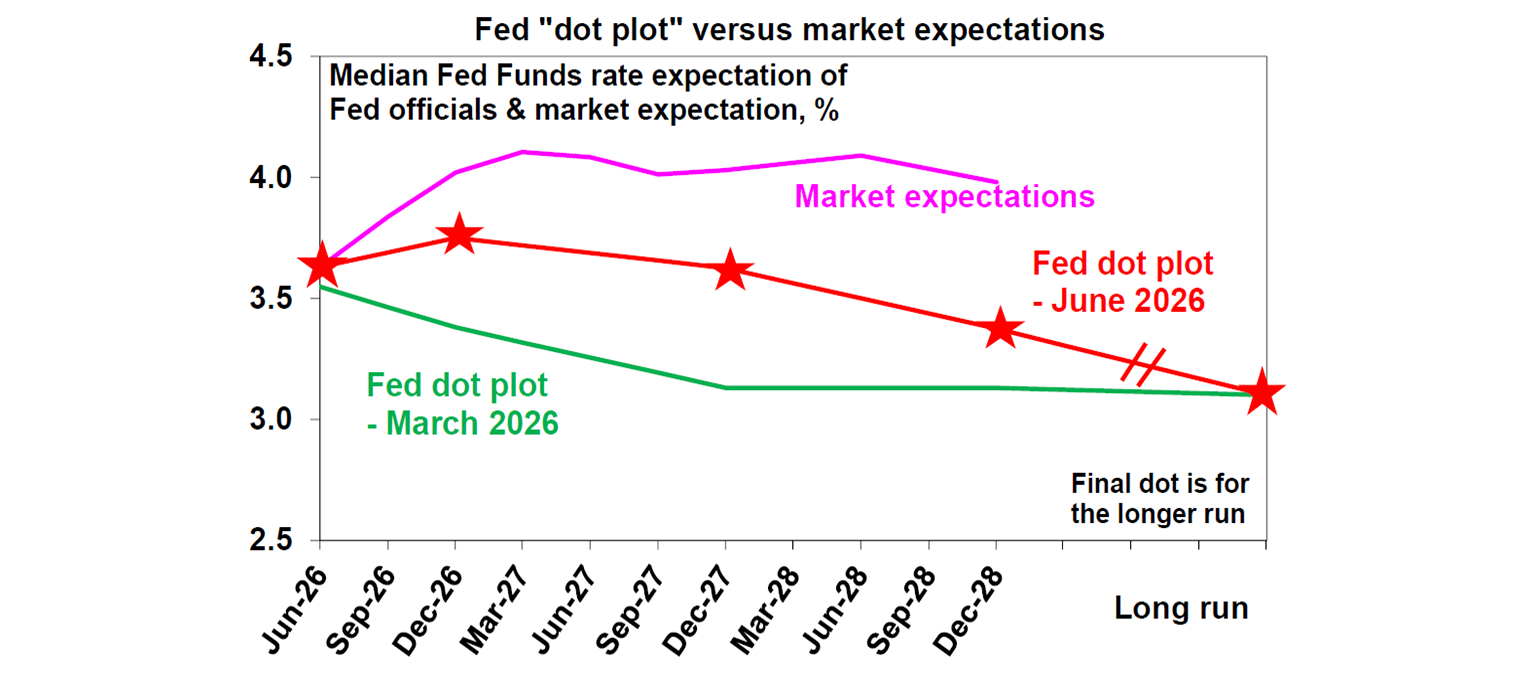

The Fed under new Chair Warsh left rates on hold at 3.5-3.75% as widely expected, but its message was clearly hawkish. The median dot plot of Fed officials interest rate expectations moved up with half now expecting a hike this year and half a hold, the easing bias was dropped from the post meeting statement, the Fed’s inflation forecasts were revised up to be well above target and the statement ended with a commitment to “deliver price stability.” As a result, the US money market now sees a hike by September and another one by April. So much for earlier expectations that Trump appointee Warsh might deliver on the President’s desire for a rate cut – that has been made impossible by the combination of the tariffs, the energy shock and policy stimulus leading to higher inflation making it impossible for Warsh to convince Fed committee members of the case for a cut even if he wanted to. Meanwhile, Warsh is implementing big changes at the Fed including a briefer statement and no clear guidance – which could mean increased volatility in money market expectations and financial markets as markets have to work it out for themselves.

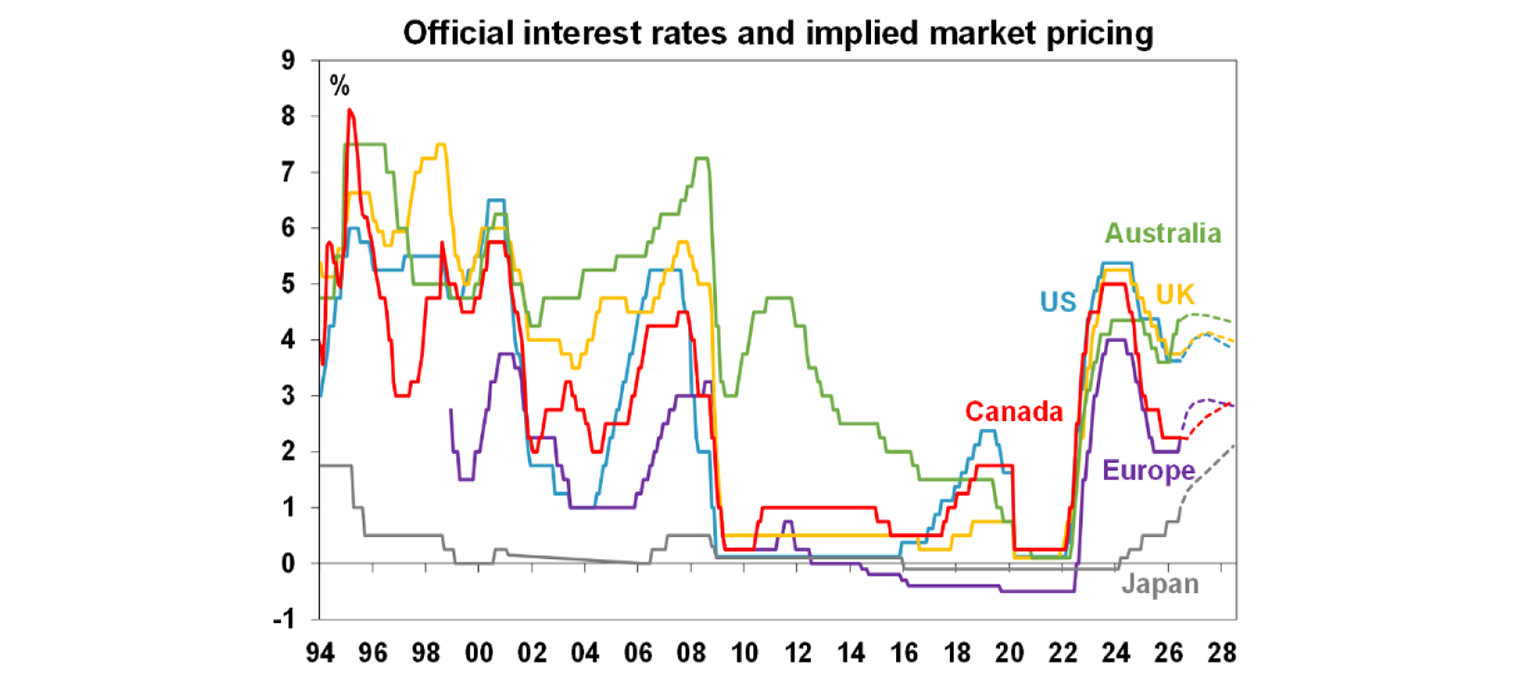

The Bank of England left rates on hold at 3.75% but with a 7/2 hold versus hike vote. Its commentary was hopeful of inflation returning to target without another hike, but the money market still sees a hike this year.

The Swiss, Swedish and Norwegian central banks all left rates on hold but the last two had a tightening bias.

Central banks in the Philippines and Indonesia raised their policy rates.

The Bank of Japan raised its policy rate by another 0.25% taking it to 1% and flagged more hikes ahead.

In Australia, the RBA provided no surprises and left rates on hold as three rate hikes in a row and signs of softer demand growth provided scope to pause and assess. However, this should not be seen as the top with the Reserve seeing the growth slowdown as what is needed, underlying inflation still rising in line with its forecasts, inflation still being too high and likely to remain so for some time and noting that its prepared to hike further if required. What’s more while the US/Iran peace deal is good news the RBA is likely to remain wary of the second-round flow through to inflation from the oil supply disruption that “will take some time to resolve”. We are continuing to allow for a further rate hike in August and have another one pencilled in for November reflecting the still rising trend in underlying inflation and risks that it will take longer to control.

Our view on shares hasn’t changed and we continue to see them providing positive returns this year, albeit with more volatility. The combination of sticky inflation, an upwards drift in central bank interest rates, worries about an AI bubble, huge US IPOs, political uncertainty around the US mid-terms and lingering Iran risks even with the deal are likely to continue to result in a volatile ride with a high risk of yet another correction. But continuing economic growth, solid profit growth and Trump likely to pivot somewhat to more consumer-friendly policies ahead of the mid-terms should result in okay overall returns.

In Australia, the Federal Government announced carve outs for its capital gains tax and trust changes. These basically increase the number of small businesses eligible for a 50% CGT concession by raising the revenue threshold from $2m to $10m, allow start ups meeting an “innovative business” definition with less than $50m revenue to retain the 50% discount, exempting donations from trusts from the 30% minimum tax and exempting testamentary trusts from the 30% minimum tax rate. The changes are welcome and should have been included in the Budget announcement to head off a lot of criticism. However, it’s debatable whether the changes go far enough. In particular the rules around innovative start-ups look very onerous with a cap on capital gains which looks too low – particularly once allowance is made for many such startups ultimately failing. And the change to CGT still apply in relation to share investing which by biasing share market investors towards income could mean less capital available for growth stocks. A failure to allow for the smoothing of capital gains for tax purposes unlike the old Keating model will also lead to inequitable outcomes where someone earning the same income as a salary earner but via a lumpy capital gain will end up paying a lot more tax.

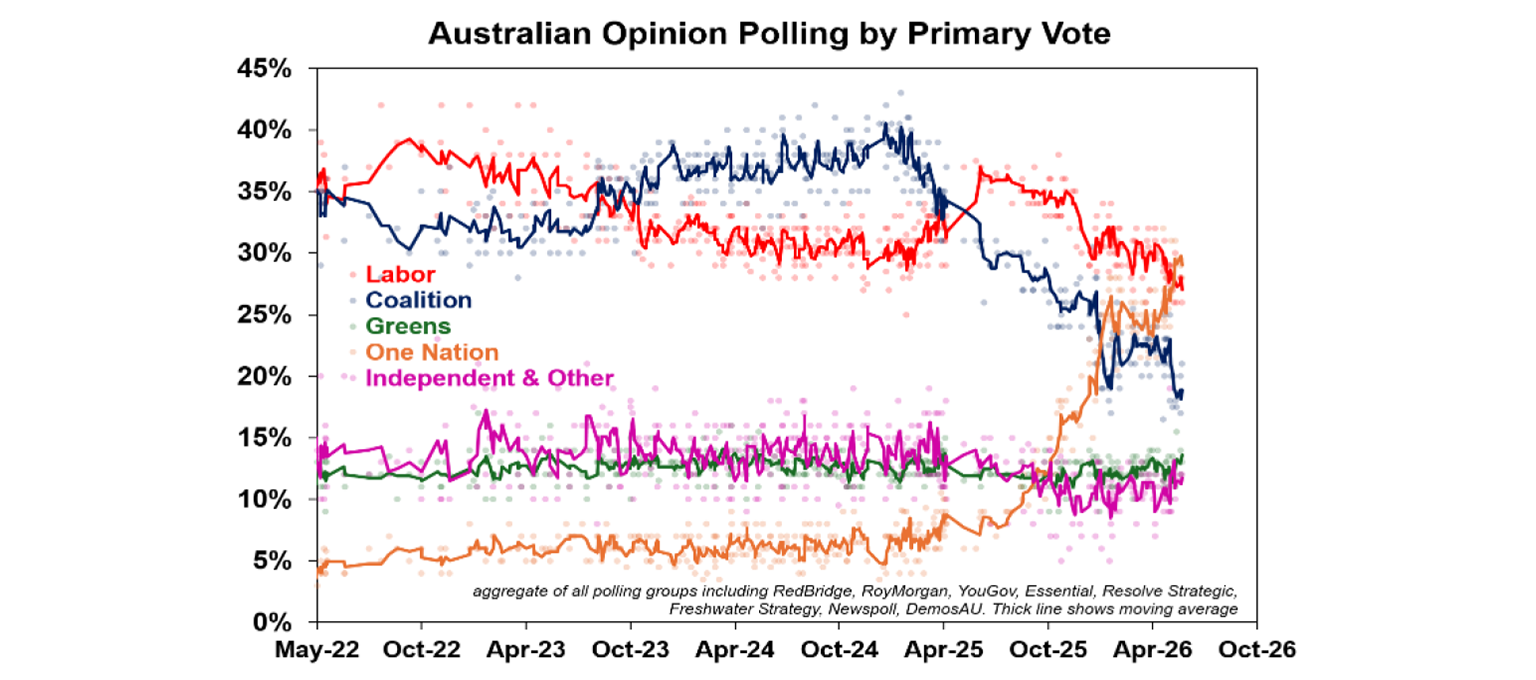

Populism taking off in Australia with the continuing surge of One Nation in opinion polls. It began as the Coalition imploded and then more recently has started to threaten Labor too. So, the rise of right-wing populism looks to be coming to Australia even though many thought it might pass us by! As in other countries its drivers appear to be a mix of cost-of-living pressures, perceptions of rising inequality and a feeling that mainstream parties aren’t delivering, all magnified by grievance driven social media for which the populist right and left seem made for. The danger is that many get attracted to simplistic solutions that might appear to be “common sense” only to find years later that they don’t work and only make the problem worse. Sure, immigration needs to be returned to more sustainable levels but cutting visas to just 130,000 a year risks negative population growth as annual departures are double that and going too far on immigration will lead to labour shortages, make it harder to deal with the aging population and decimate our fourth biggest export earner - education. Likewise, it’s common for populist parties to offer all sorts of tax cuts and tax breaks and say it will be financed by slashing government waste only to find that’s easier said than done (just think of DOGE in the US) which can then lead to worse budget deficit blowouts and often even worse inequality. And while it’s not really clear what exactly “monoculture” refers to – eg is it multiracial diversity but with everyone having the same values or really a desired return to a more anglo Australia? - returning to the sort of monoculture of my childhood in the black and white 1960s sounds kind of dull and unappealing after the diversity and dynamism that multiculturalism has brought. It would be a bit like trying to go back to things as they were in the first half of Pleasantville. Without multiculturalism its doubtful we would have a team like the Socceroos. A problem is that it’s hard to separate culture and ethnic background so Australia pushed down the multicultural path with bi-partisan support 50 years and global comparisons would suggest that it’s been very successful. Over the long term the rise of populism including populist responses to it by mainstream political parties risks a less favourable economic environment – less growth, more inflation and more volatility which could weigh on investment returns. See here for a deeper analysis.

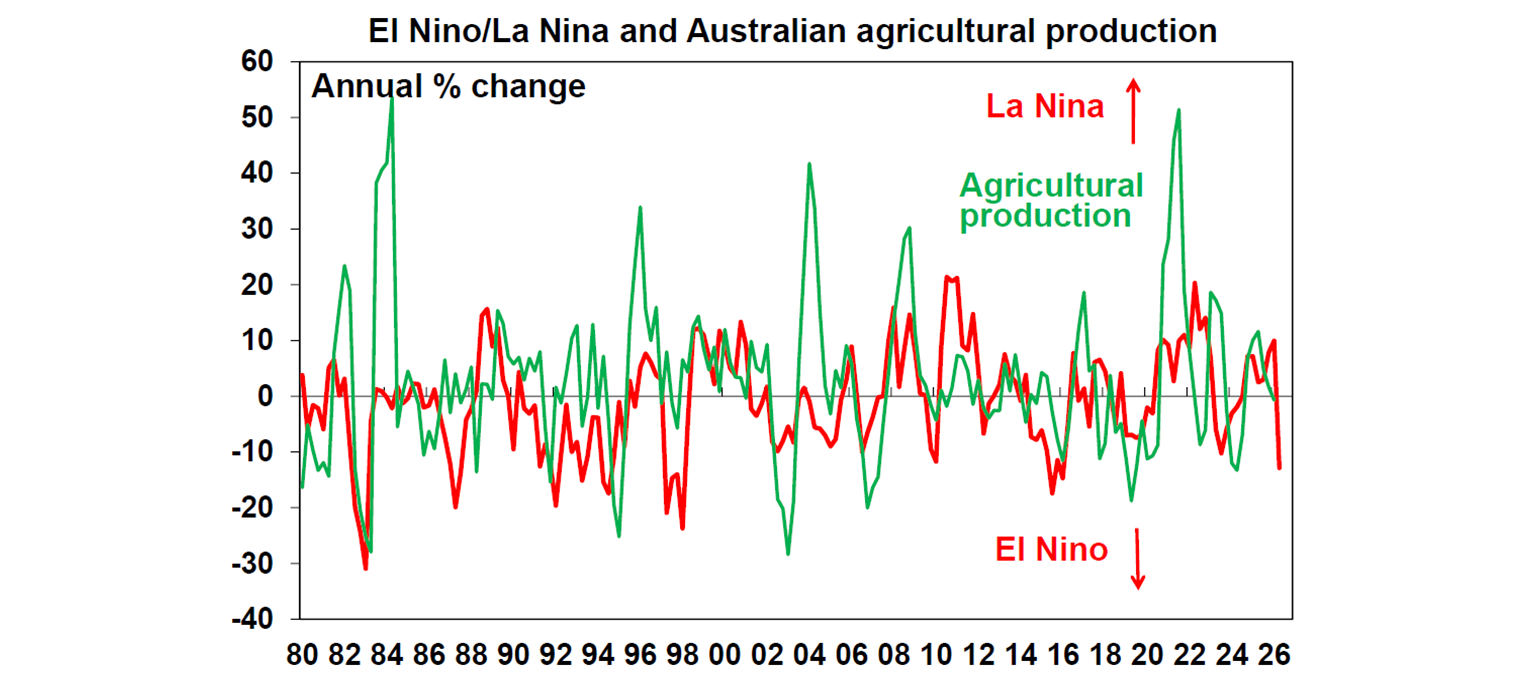

Another El Nino. In the last week the Bureau of Meteorology declared an El Nino weather event. This follows the Southern Oscillation Index – which tracks differences in surface air pressure across the Pacific – falling into El Nino territory. It tends to be associated with drier conditions down Australia’s east coast which can lead to higher food prices. But of course, this is not always case and its correlation with Australian agricultural production can be very hit and miss (outside the 1982-83 El Nino drought).

And for Juneteenth Day here’s Galveston – It’s one of the best anti-war songs but the arrival of Union troops there on 19th June 1865 was a special thing.

Major global economic events and implications

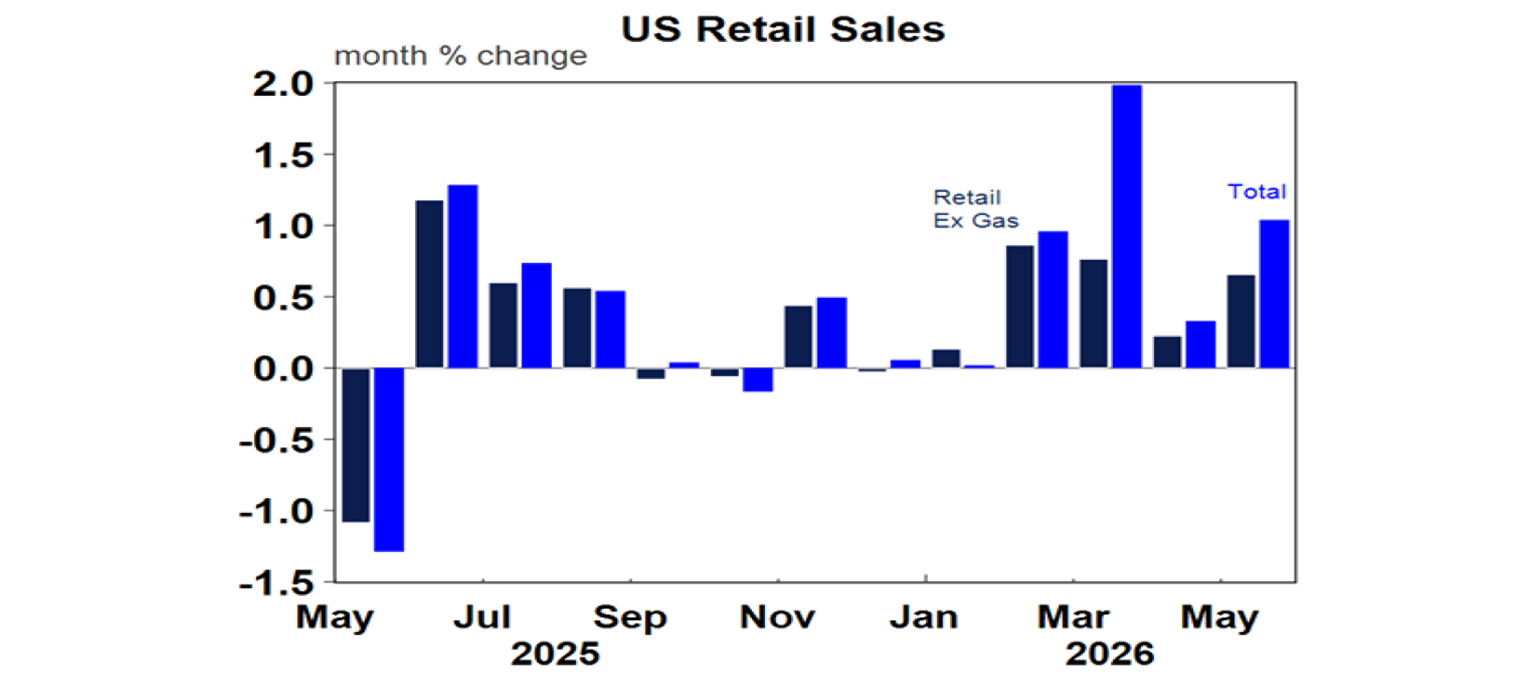

US economic data was mixed as it often is. Retail sales rose solidly in May, and jobless claims continue to remain low.

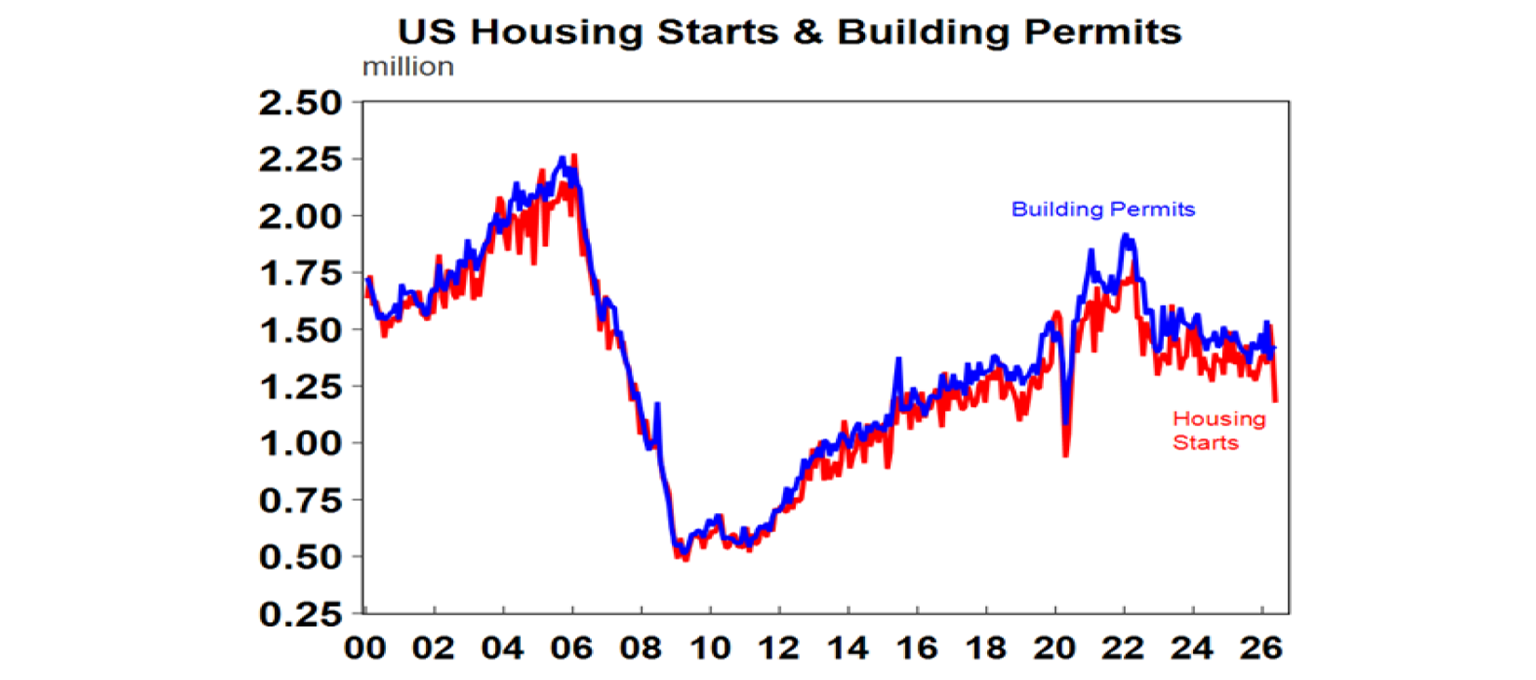

But US housing starts, permits to build new homes and home builder conditions were all weak.

UK inflation came in weaker than expected at 2.8%yoy in May, with core at 2.6%yoy helping take some pressure of the Bank of England for rate hikes. Against this though services inflation rose more than expected to 3.7%yoy and jobs and wages growth were a bit stronger than expected in the 3 months to April, with unemployment lower.

Japanese inflation rose to 1.5%yoy in May with core inflation remaining at 1.1%yoy.

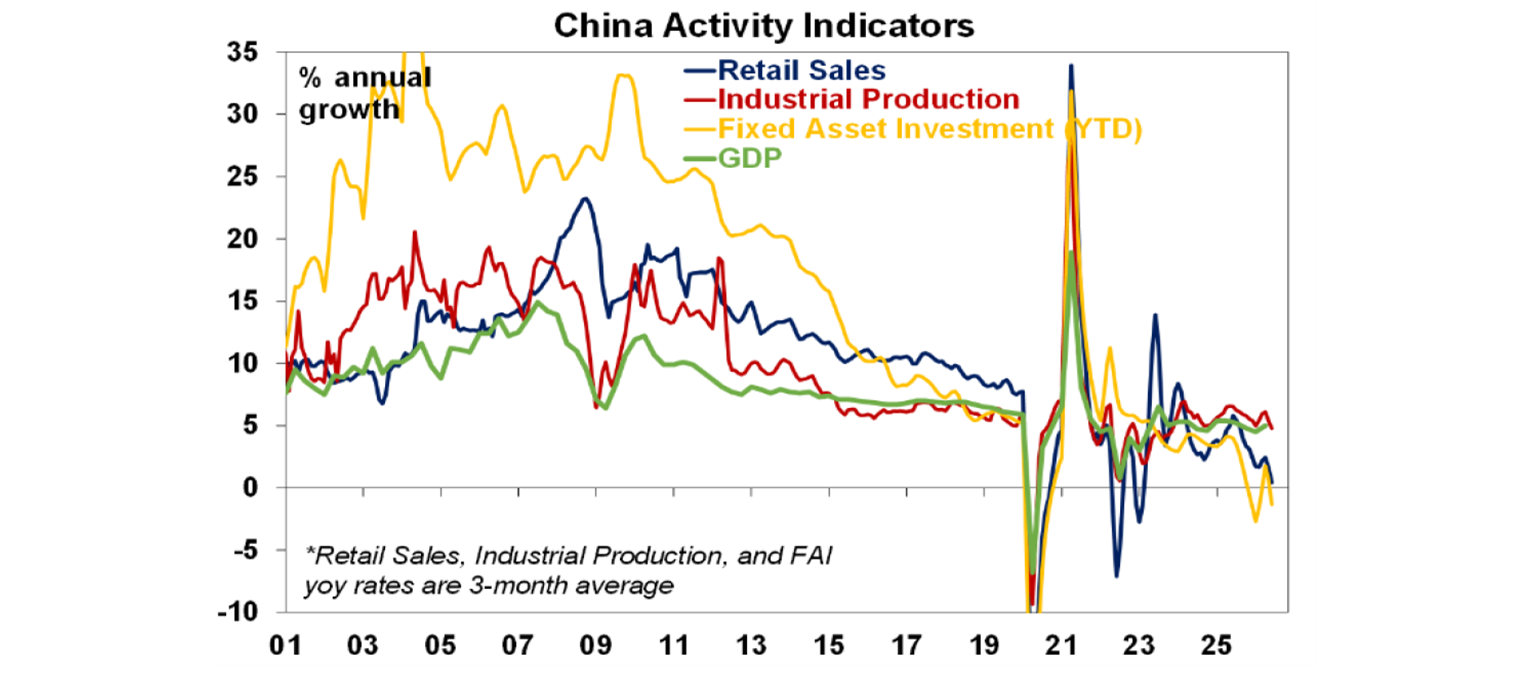

Chinese economic activity data for May was weak with falls in retail sales and investment along with ongoing falls in property investment, sales and home prices. Extra policy stimulus is likely to remain incremental though.

New Zealand March quarter GDP rose a solid 0.8%qoq or 1.5%yoy with solid in consumption & business investment, consistent with the RBNZ hiking rates next month.

Australian economic events and implications

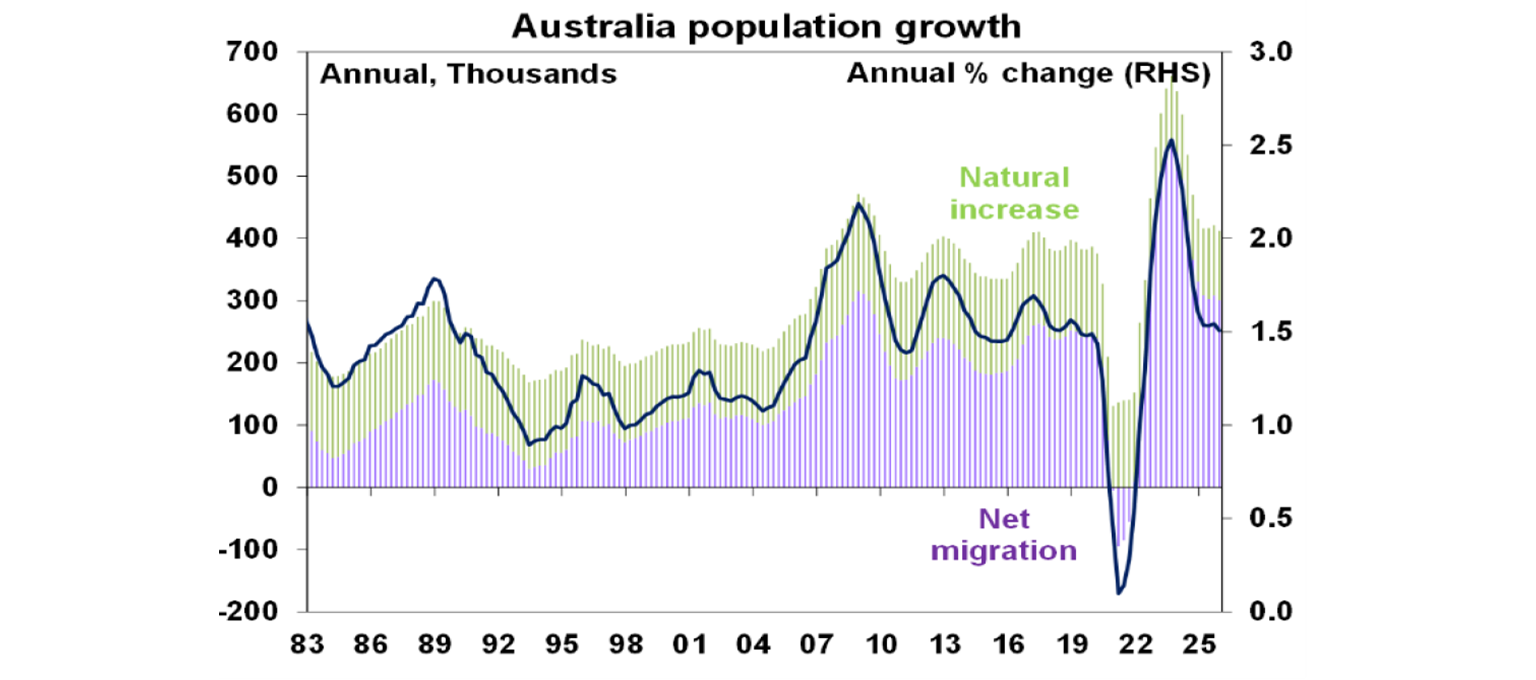

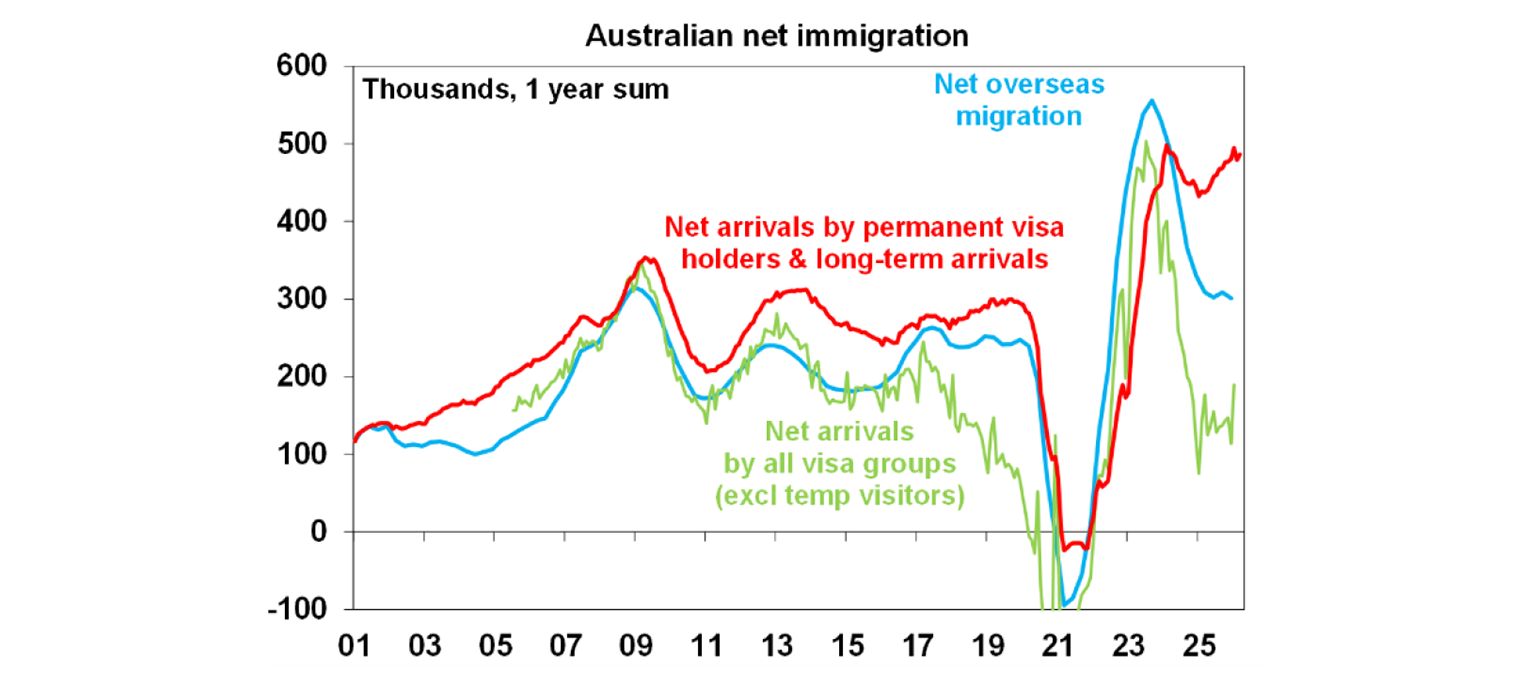

Population growth in the December quarter slowed to 1.5%yoy. This represents a 412,000 increase in the population over the last year, of which 301,000 was net migration. Net migration is down from the record 556,000 over the year to the September quarter 2023 but remains high. To meet annual new housing demand flowing from population growth and demolitions and rising demand for holiday homes we currently need new dwellings of around 200,000 a year but ideally need something like the Housing Accord’s 240,000 to reduce the accumulated undersupply as well – but we are currently only managing to build around 175,000. So, the housing shortfall will continue.

Taking an average of monthly data for visas and arrivals suggests net migration will remain relatively high for a while yet.

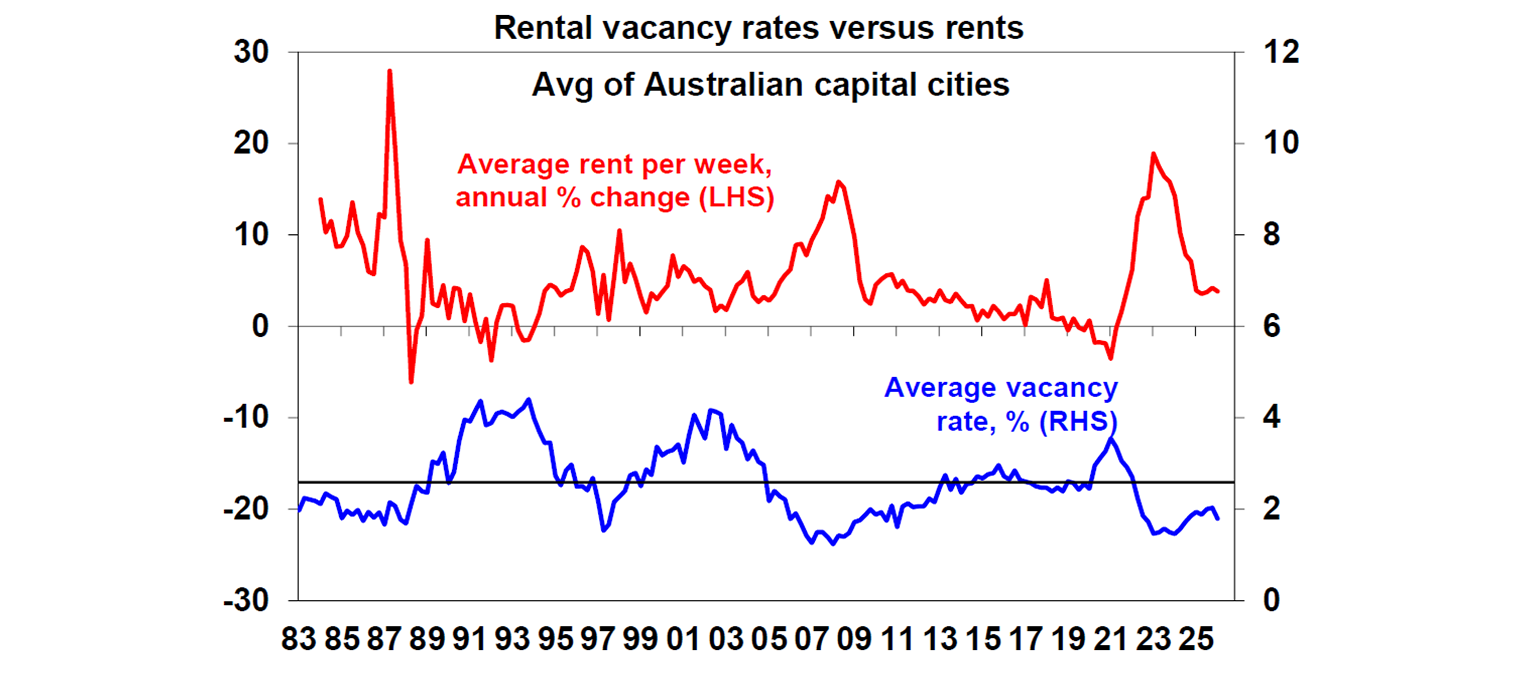

The housing shortage in Australia continues to be evident in very low rental vacancy rates, which points to a high risk of growth in average rents accelerating going forward.

What to watch over the next week?

Developed country business conditions PMIs for June will be released Tuesday and are likely to show some improvement in conditions reflecting the US/Iran peace deal and some pull back in price pressures.

In the US core private final consumption deflator inflation (Thursday) for May is likely to show a further rise to 3.4%yoy from 3.3% and underlying growth in capital goods orders and shipments (also Thursday) is likely to have remained solid.

Canadian inflation data for May (Monday) is likely to show core inflation remaining around 2.1%yoy.

In Australia, CPI inflation for May (Wednesday) is expected to fall 0.4%mom partly reflecting a 15% fall in fuel prices, but this will see annual inflation rise slightly to 4.3%yoy. Unfortunately trimmed mean inflation is expected to rise 0.3%mom taking it to 3.5%yoy from 3.4% partly reflecting second round effects from the oil shock. In other data expect a 35,000 rebound in employment for May with unemployment falling to 4.4% after oddly weak April data, a 1% fall in job vacancies over the 3 months to May and 0.1% fall in household spending for May (all due Thursday).

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the oil shock assuming the flow of oil quickly resumes but the risk of further falls remains high given uncertainty the peace deal with Iran, still stretched valuations, political uncertainty associated with Trump & the midterm elections and worries about the impact of AI. However, returns should still be positive for the year as a whole thanks to Trump still likely to pivot to consumer-friendly policies ahead of the mid-terms and solid profit growth.

Bonds are likely to provide returns below running yield this year.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home prices are expected to fall around 1% this year and by 5% over the next 12 months as a result of poor affordability, RBA rate hikes, reduced investor demand flowing from the winding back of negative gearing and the capital gains tax discount and poor confidence. A 5% fall is consistent with just another cyclical downswing of which there have been several over the last two decades.

Cash and bank deposits are expected to provide returns around 4.-5%.

The $A is likely to rise as the interest rate differential in favour of Australia widens, although a move to Fed hikes may limit this. Fair value for the $A is around $US0.72.

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.