Weekly market update

Investment markets and key developments

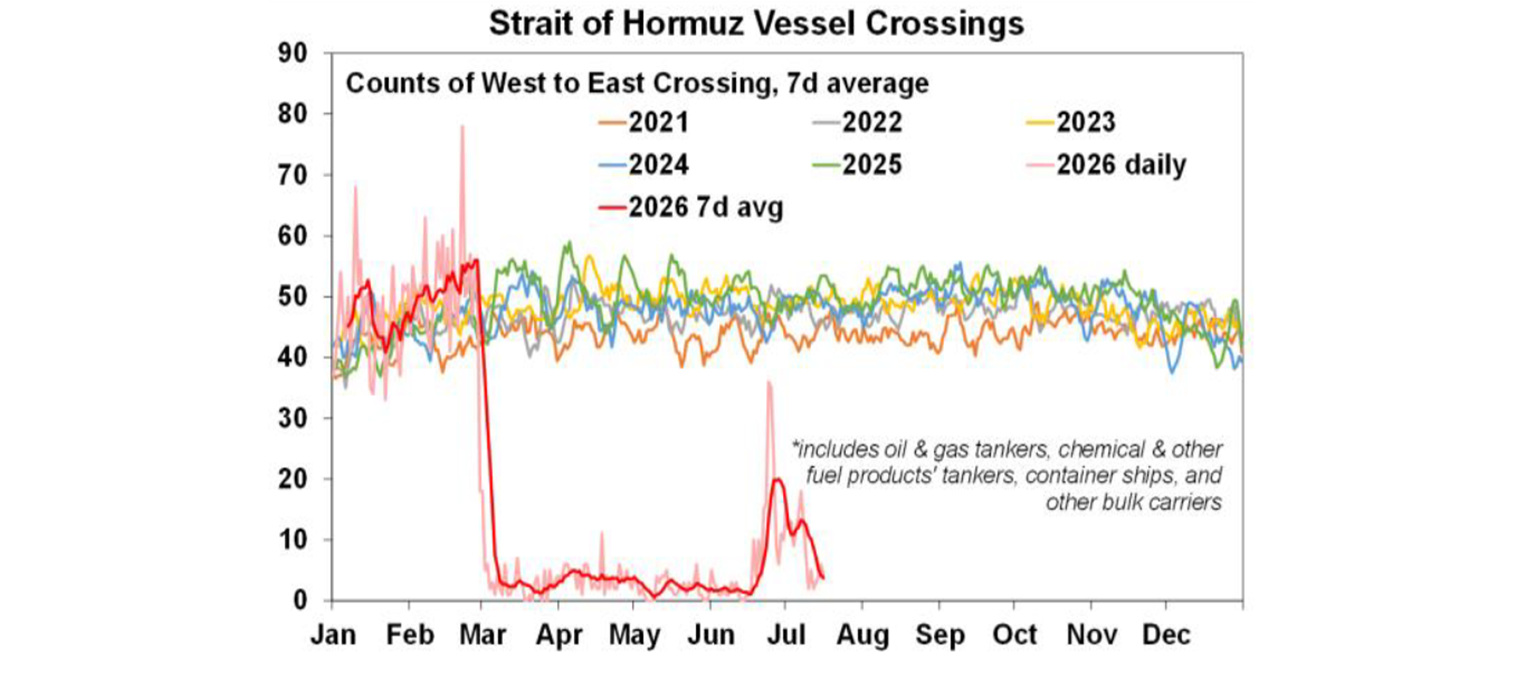

Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation.

11 min read

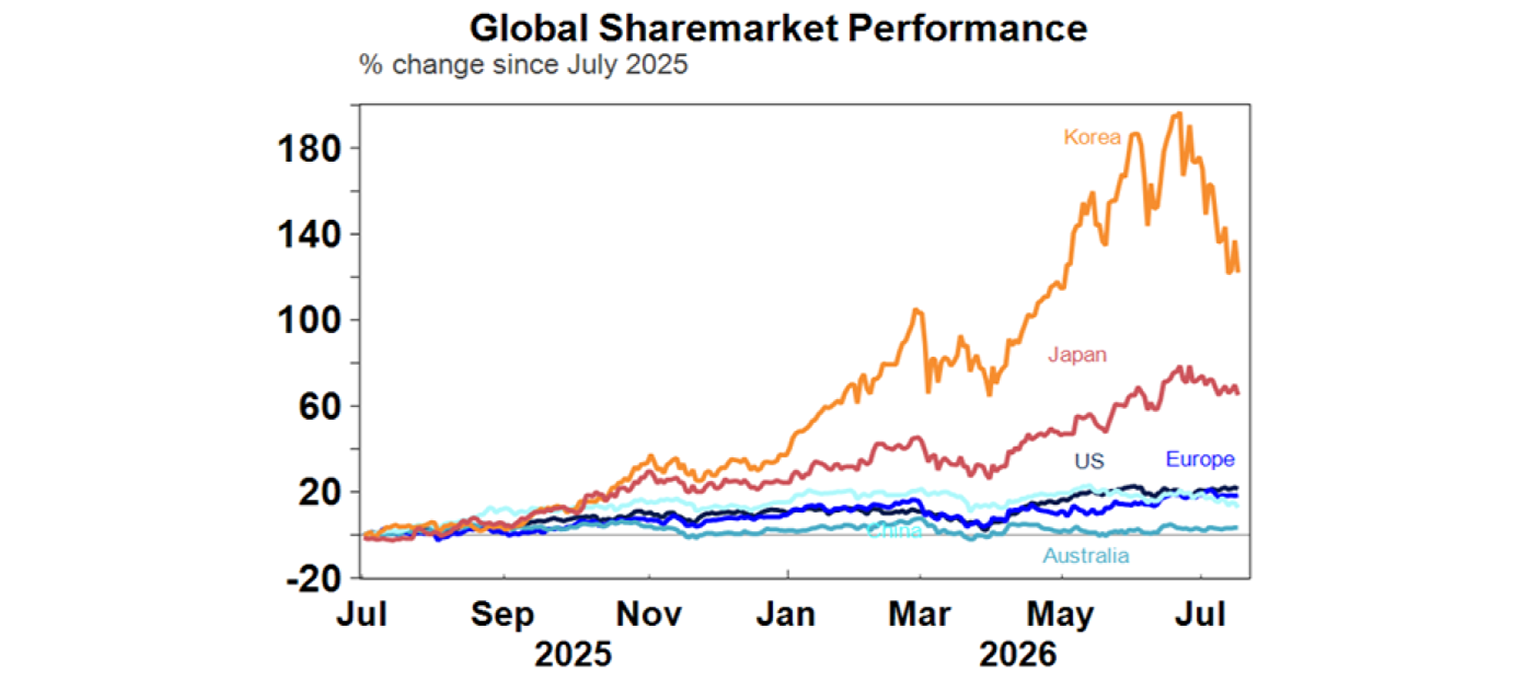

Global shares fell over the last week as the Iran War escalated again with oil prices up and IT shares were hit with a rout in chipmakers on worries that about the sustainability of AI related earnings and valuations. This intensified on Friday when Chinese AI company Moonshot unveiled a new AI model, Kimi K3, claimed to offer similar performance to top Anthropic and Open AI models at a lower cost leading to fears of another “DeepSeek moment”. For the week US shares fell 1.6%, Eurozone shares fell 0.7%, Japanese shares fell 6.4% (reflecting its exposure to tech and higher oil prices) and Chinese shares fell 5.3%. The renewed surge in the oil price along with a fall in BHP shares on the back of a weak production outlook for copper and a strike at Port Hedland saw the Australian share market fall but only by 0.1%. The relative underperformance of the Australian share market since the March lows and its low exposure to AI tech companies could leave it relatively less vulnerable compared to other global markets.

Pressure remained on Korean shares which are down 25% from their high on worries about an AI bubble weighing on Korean chipmakers, profit taking after Korean shares more than doubled year to date, heavily leveraged retail investors closing positions, tightened regulations around buying single stock leveraged ETFs and not helped by the Bank of Korea raising rates with more hikes likely. With surging earnings the forward PE is now around 6-7 times, but Dr Kospi may be sending a warning signal about the outlook for AI related tech shares.!

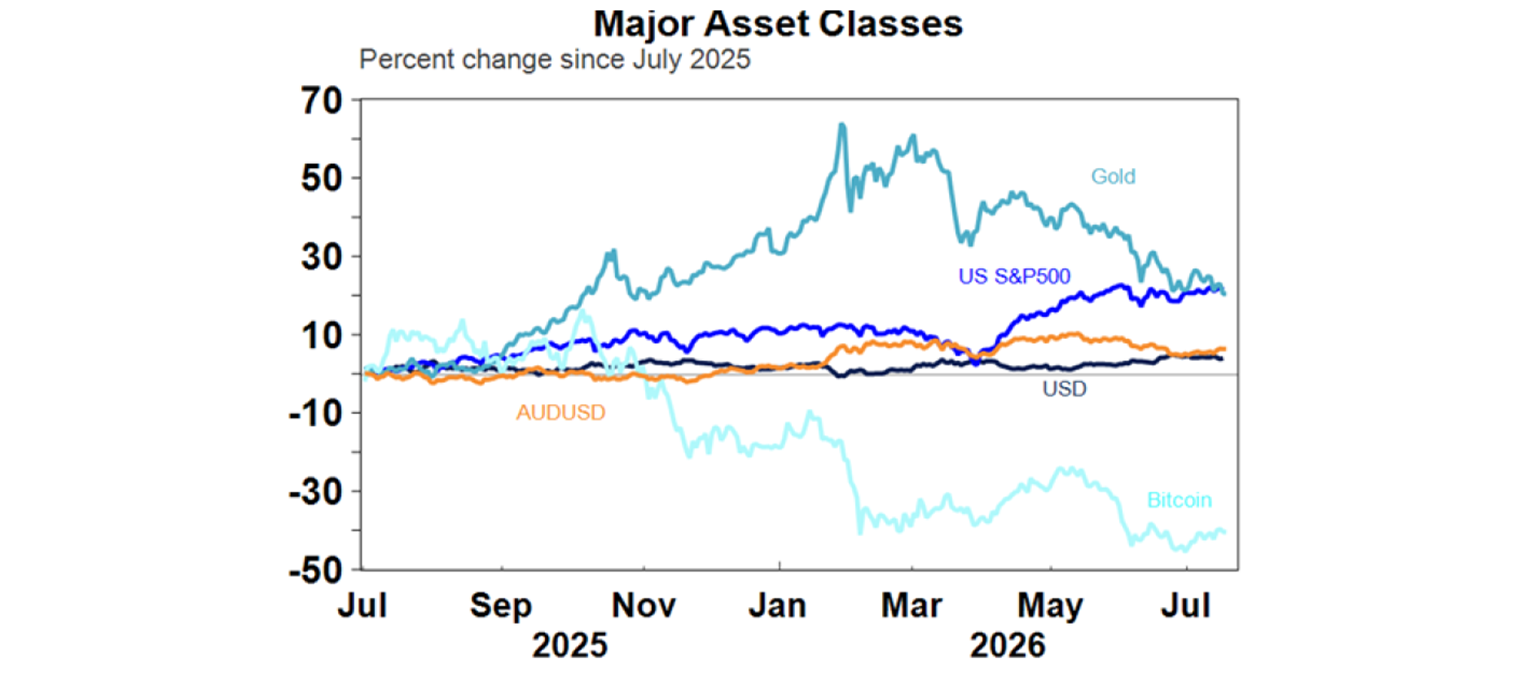

Bond yields were mixed over the last week – up in Europe and Australia but down in the US and Japan. The $A rose slightly to around $US0.70 as the $US was little changed. The iron ore price rose slightly but remains around $US100 a tonne, but copper, gold and Bitcoin fell. Bitcoin continues to hold above technical support around $US60,000 but has so far failed to rise above its 50 day moving average and looks weak like its still in a “crypto winter”.

Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation. Trump at one stage added to confusion with a plan to impose a 20% fee on the value of cargo on ships transiting the Strait but that ridiculous idea was quickly dropped.

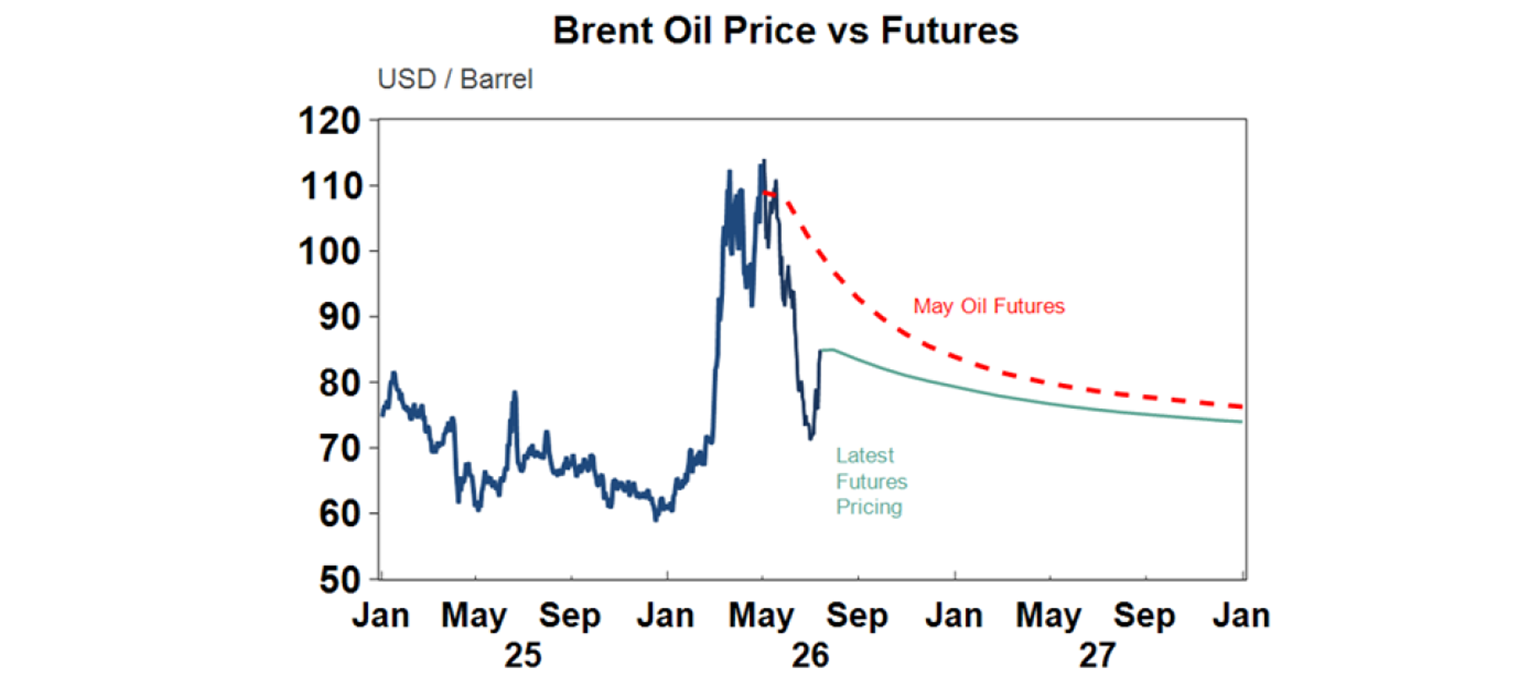

This in turn has seen oil prices rebound, although they are well below their highs – note that intra day Brent and West Texas spiked to around $US1.20 a barrel earlier in the War.

The resumption of the War begs the question of what has been achieved? Iran is arguably now stronger having proved it can block the Strait, its government is more hardline, there is no resolution to its nuclear ambitions, and it still has missiles and drones! There are parallels with the Ukraine and Vietnam wars which showed a superior military power can be challenged – but of course they did not threaten the global economy to the same degree!!

So far, the response in both oil prices and share markets has been relatively moderate and a long way from the panic seen back in March. This likely reflects the relatively benign experience since the War started and the assumption that the same will continue to apply. In particular:

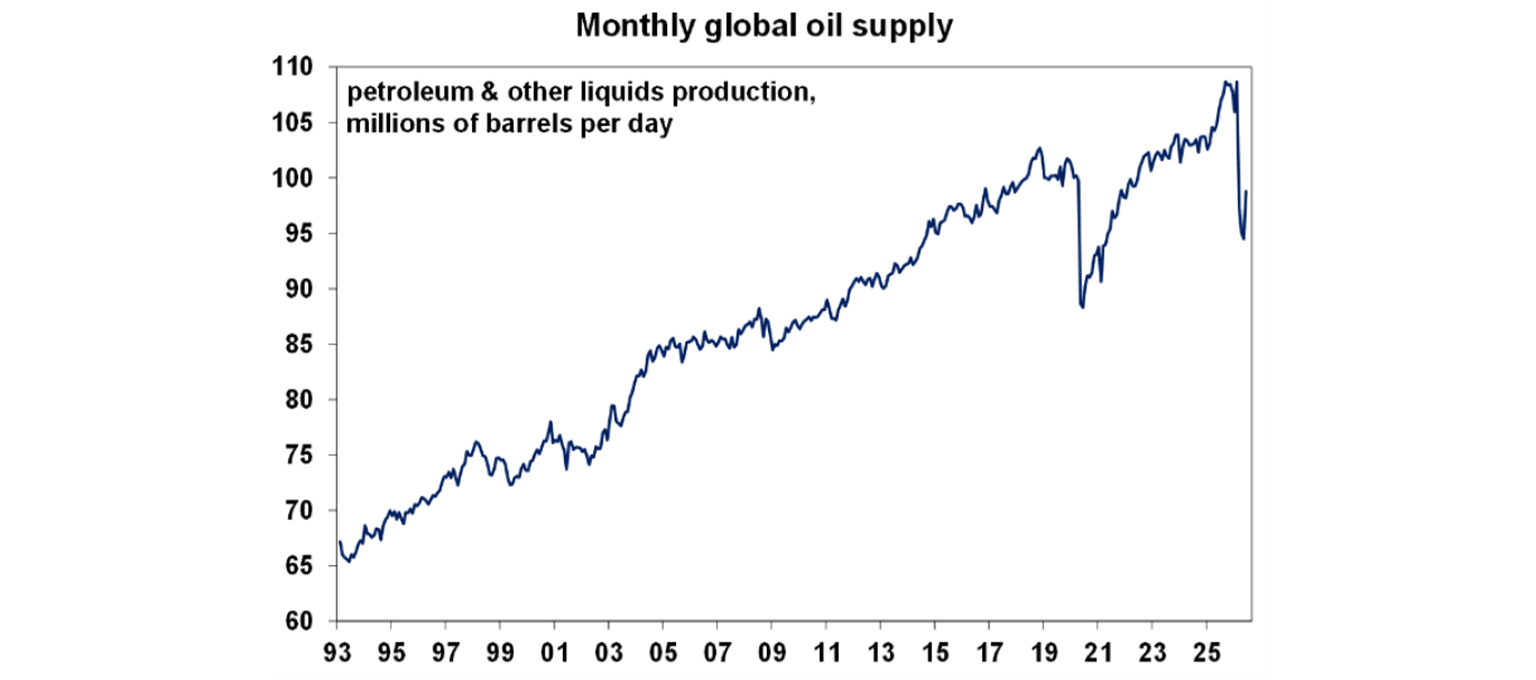

The hit to global oil production has been less than implied by the blockage of the Strait (which would normally mean a 20% hit to oil and gas supplies – ie a 20 million barrels a day reducton in oil supplies) as some was able to bypass the Strait by flowing through the Saudi East-West pipeline to the Red Sea (which has 7 million barrels per day of capacity) and the UAE’s Fujairah pipeline (1.5-2 mbd capacity) and production picked up in other countries. So the hit to production is more like 12-13mbd rather than 20mbd. And the fall in production as seen in the next chart was from a spike higher through last year which led to a reserve build up.

Global oil demand has fallen around 5% (or 5mbd) as a result of efficiencies and an increase in demand for EVs. See the Australian data section below.

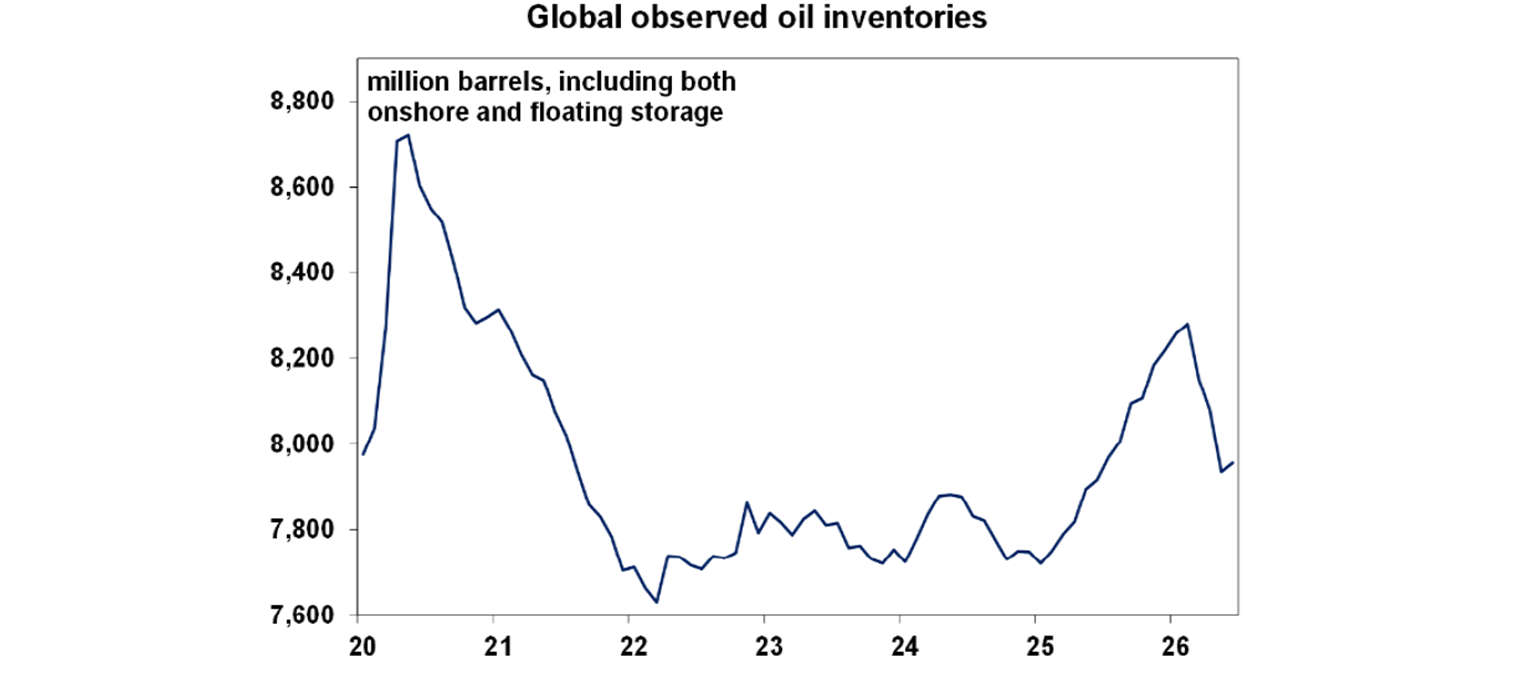

The world has been able to run down oil reserves which had been built up ahead of the War. The next chart may understate the rundown – which could have taken us back to around the 2022 lows. But this is what the International Energy Agency’s data says.

Despite a hit to confidence economic data has mostly held up pretty well and expected profit growth remains strong, helped by the AI boom of course.

Investors are assuming another TACO as there are constraints on both the US – with Trump’s approval rating likely to collapse anew and lead to Republicans losing both the House and Senate in the midterms if the gasoline price surges again – and on Iran - which wants to keep pressure on Trump but not so much he decides to wipe out its government. Trump has been claiming that Iran wants to talk peace again..which usually means he wants a deal!

The final point may suggest some sort of range for oil prices, maybe around $US70-90, with another TACO “peace” deal if we get to the high end. Well hopefully!

But the risk is now high for the global economy and share markets as oil reserves head even lower threatening a renewed rise in oil prices above $US100 a barrel. The strikes on Iran and its retaliatory strikes are intensifying and if really pushed it may attack the UAE port of Fujairah again and could fire up the Houthi’s to block the Bab el-Mandeb Strait out of the Red Sea. Which would severely disrupt the oil bypass routes. So we are back to where we were before the peace deal in that the longer the Strait remains closed and the War escalates the greater the risk that oil prices will have to rise to around $US150/barrel to bring demand down to match the hit to supply. This is not our base case but it’s a high risk again. This leaves US and hence global and Australian shares at high risk of another correction in the seasonally weak months of August and September. Particularly, if AI earnings and valuation worries really intensify. Of course, just as Australian shares didn’t get much benefit on the way up in the AI boom they may not fall as much if and when it does really start to unwind.

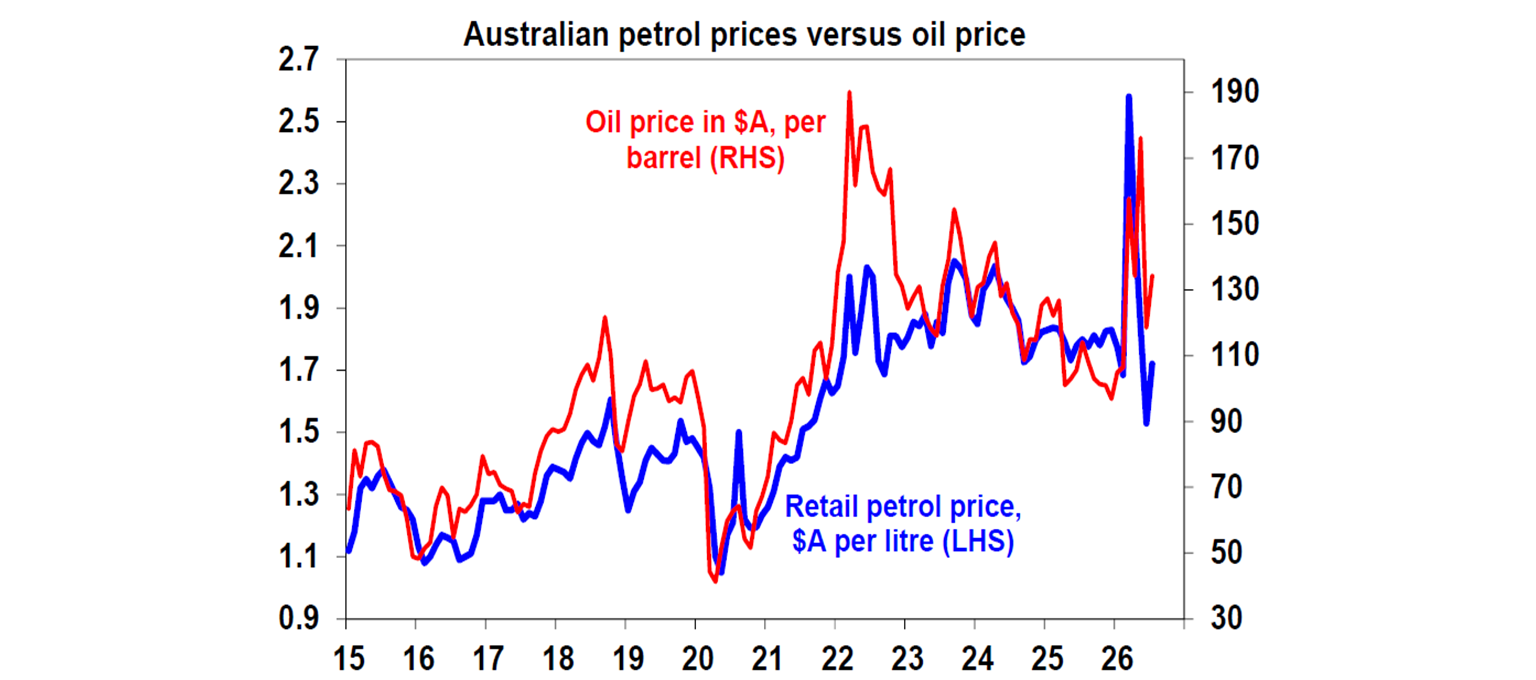

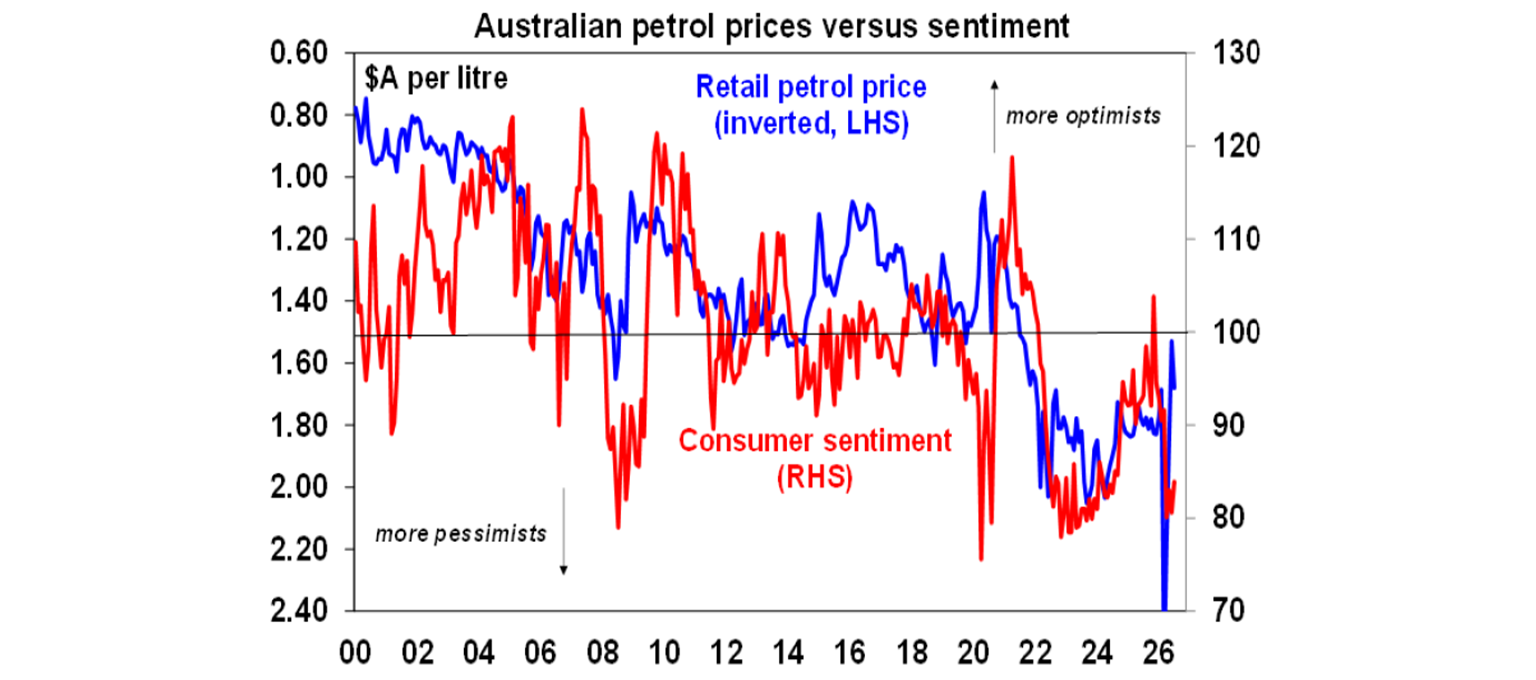

In Australia, petrol prices have risen from the 30 June low of around $1.53 a litre to now around $1.73. This reflects the halving of the 32 cents a litre fuel tax cut from 1 July and some flow through of the rebound in oil prices. But the rebound in oil prices is yet to fully flow through and could add around another 10 cents a litre to petrol prices. It’s likely that the Government will delay the removal of the remaining 16 cent a litre fuel cut beyond 2 August.

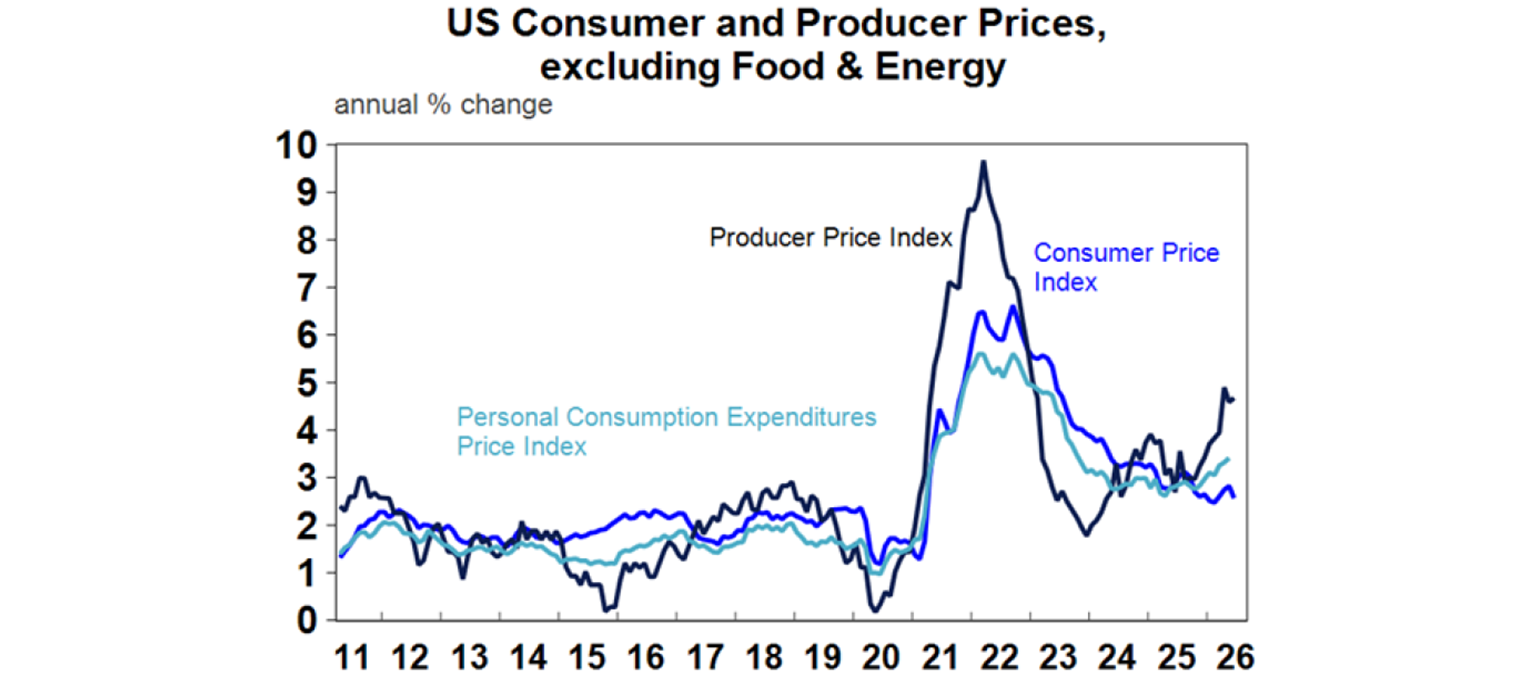

While the rebound in oil prices boosted concerns that central banks might have to raise interest rates, this was partly offset in the US by weaker than expected June inflation data. Thanks to lower energy prices last month the headline CPI actually fell in June seeing its annual rate of increase drop back to 3.5%yoy and core inflation was flat leading to a drop to 2.6%yoy from 2.8%yoy. Producer price inflation has also moderated. This in turn points to June annual core private final consumption deflator inflation, which the Fed targets, dropping to 3.3%yoy from 3.4%yoy.

The softer inflation readings for June give the Fed a bit of breathing space for its July meeting to leave rates on hold. While Chair Warsh sounded hawkish in Congressional testimony, he offered little in terms of how he will get inflation back to target but he did reiterate his view that AI will ultimately push inflation down and for now he has a bit of leeway given the softer inflation readings for June. Influential NY Fed President Williams also indicated that he thinks inflation has likely peaked. A risk for the US though is that the inflation relief proves short lived as the rebound in oil prices persists and as the AI boom continues to boost tech related prices in the near term. On this front it’s noteworthy that Fed Governors Waller and Cook indicated they are losing patience with inflation and some regional presidents look to supporting a hike in rates. So, while the Fed is likely to leave rates on hold this month there are likely to be some dissents in favour of a hike and a September move is a close call. The US money market still expects at least one hike by year end.

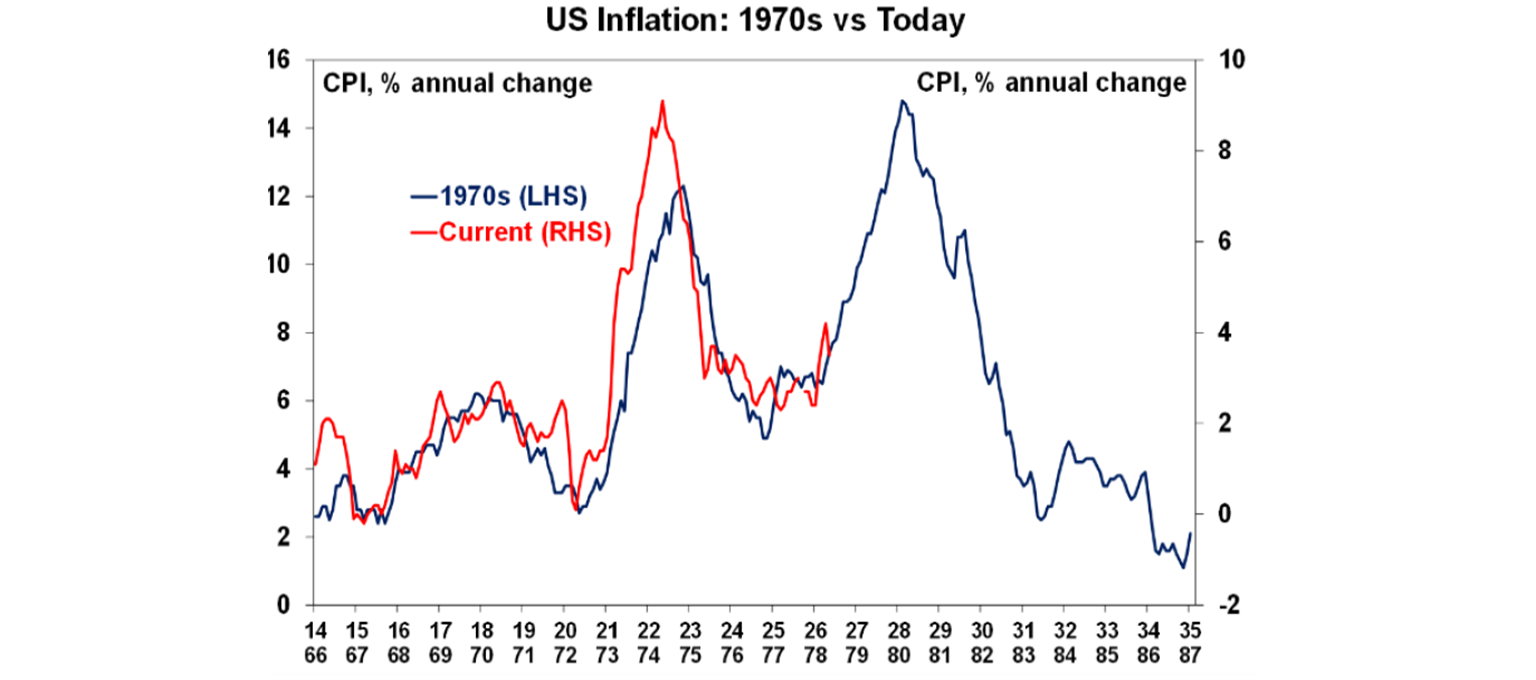

I am not a great fan of historical overlay charts like the next one for US inflation – but the US and the global economy does seem to have become more inflation prone (thanks to deglobalisation, rising defence spending, bigger government, etc). So, the risk of another up wave in inflation can’t be ignored if central banks get too relaxed.

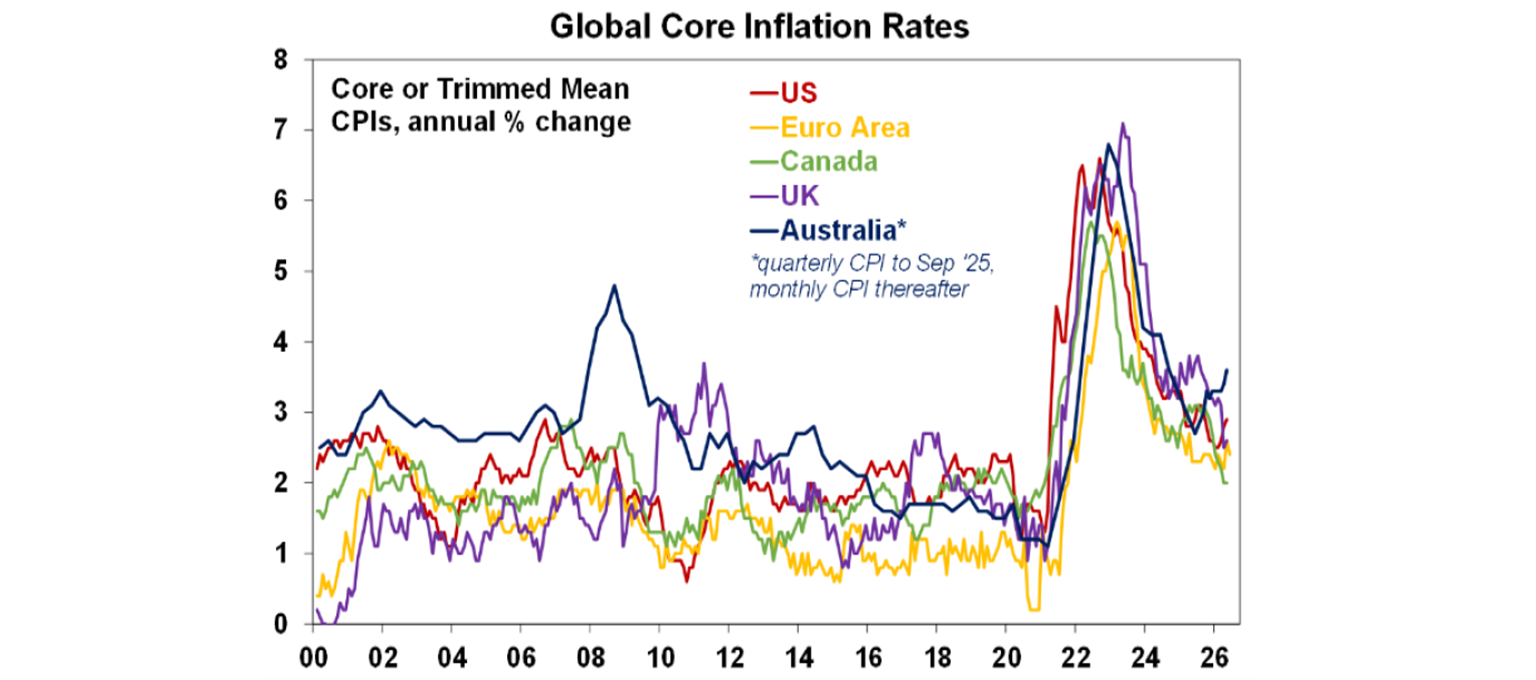

Unfortunately, Australia remains a standout in terms of core or underlying inflation, highlighting why we continue to see the RBA raising rates further this year. The rebound in oil prices with a likely flow on to underlying inflation adds to the risk of the further rate hikes this year with the money market now seeing a 65% chance of a hike by year end.

A Little Less Conversation (A Little More Action) first appeared in Elvis’ 1968 rom-com Live a Little, Love a Little but was remixed by JXL in 2002 reaching No 1 in Australia. Nearly 60 years after the original here’s a brand-new Josh Wildfire remix of it. It’s what we need in terms of economic reform to get living standards sustainably rising again!

Major global economic events and implications

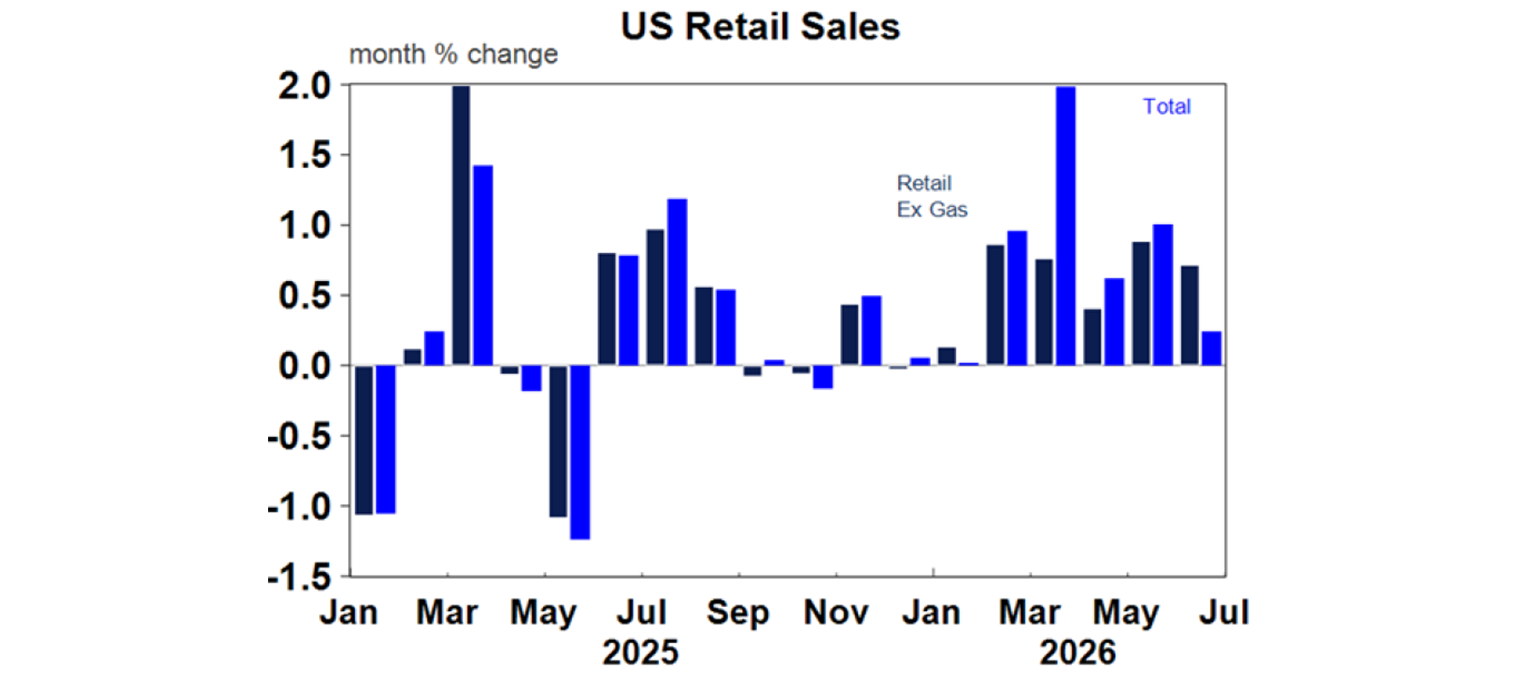

US economic data was mostly solid. Consumer spending looks to be remaining solid with strong underlying retail sales growth in June, jobless claims remain low and business conditions in the New York and Philadelphia regions are strong in July. Against this the July NAHB home builders’ conditions index remained weak. Meanwhile, the Fed’s Beige Book of anecdotal evidence reported a slight upgrade in growth to “slight to moderate” and that price pressures are still elevated but may have moderated, albeit this may be dated given the renewed escalation in oil prices.

The Bank of Canada left rates on hold at 2.25%. This reflects underlying inflation running around its 2% target and unemployment at 6.5%. With underlying inflation around target its likely to be on hold for a while yet.

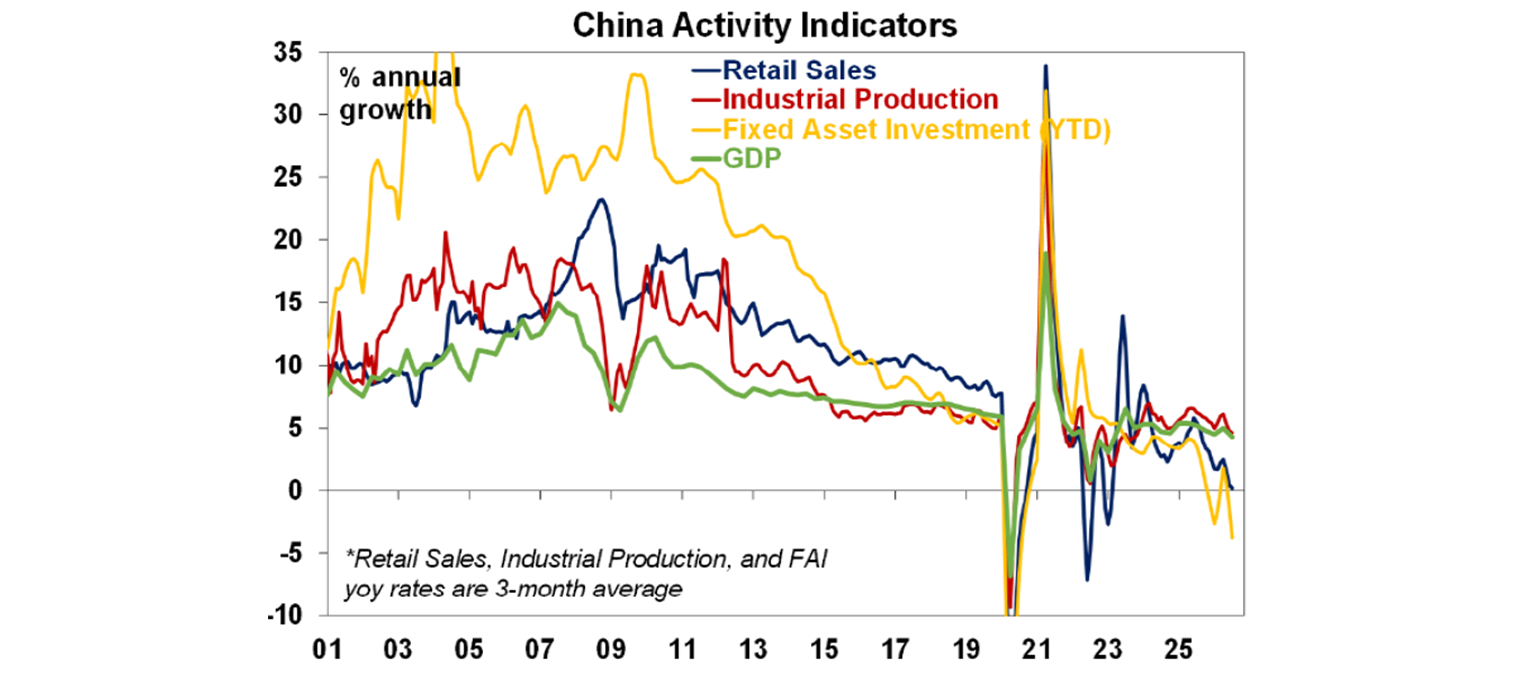

China’s economy slowed more than expected. June quarter GDP rose 0.9%qoq or 4.3%yoy, down from 5%yoy. This likely reflected the impact from the oil supply shock, slower public spending and bad weather. However, June data was mixed with a fall in investment, an ongoing property slump and slowing credit growth, but industrial production and retail sales growth picked up a bit. Policy measures are still needed to boost consumer spending and the housing sector, but are likely to remain incremental unless the oil shock goes on for several more months.

Australian economic events and implications

Consumer confidence bounced 4% in July helped by the fall in petrol prices and talk that interest rates might have peaked. The renewed rise in oil prices and its flow through to petrol prices suggest that the bounce may be short lived..

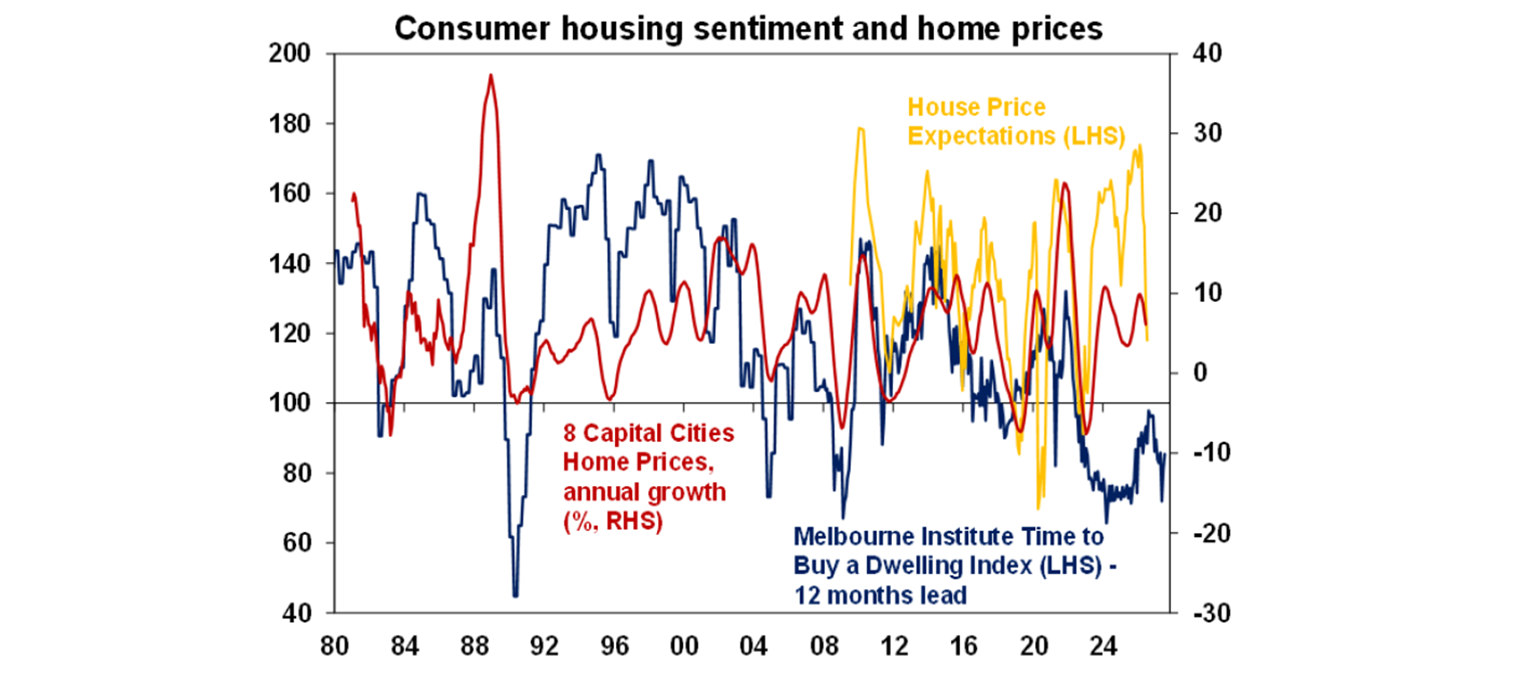

The Westpac/MI consumer survey showed a further fall in home price expectations, and consumers still see now as a poor time to buy a dwelling although it’s up slightly.

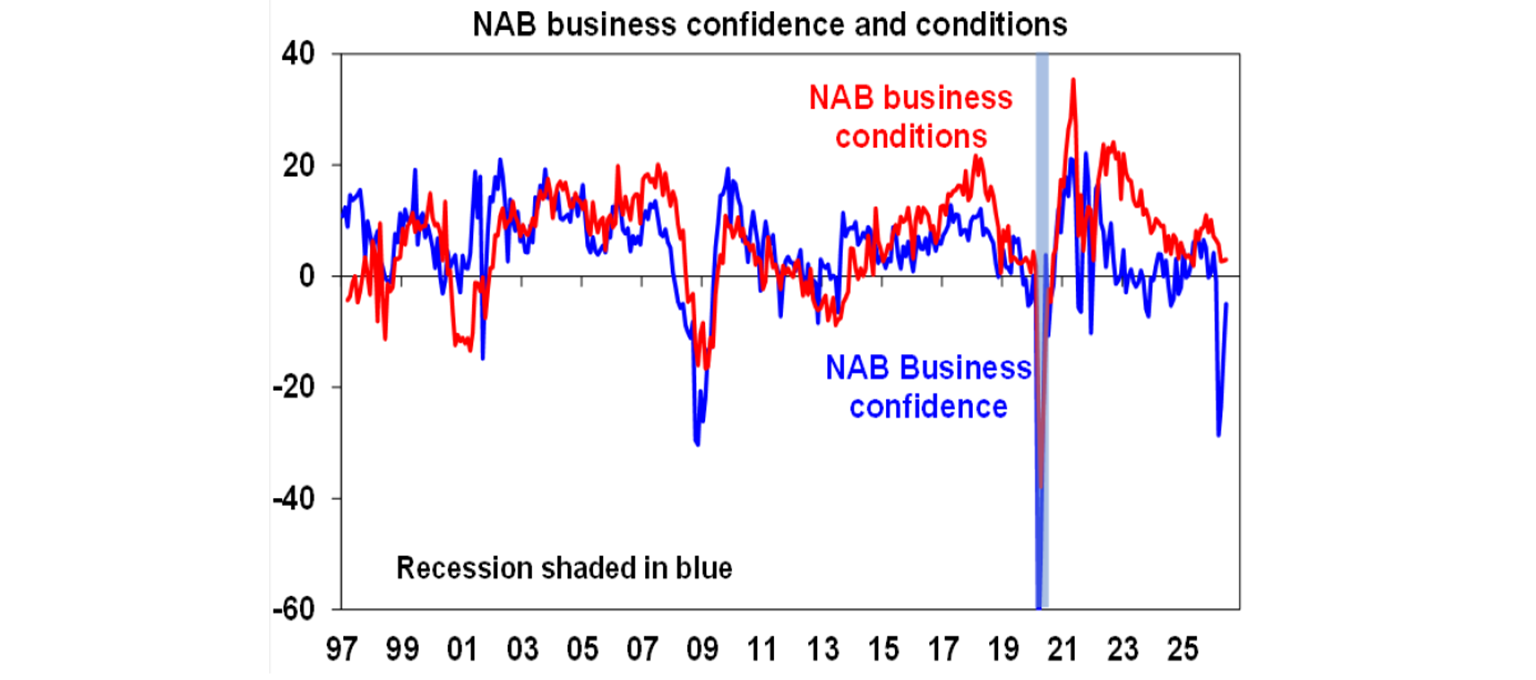

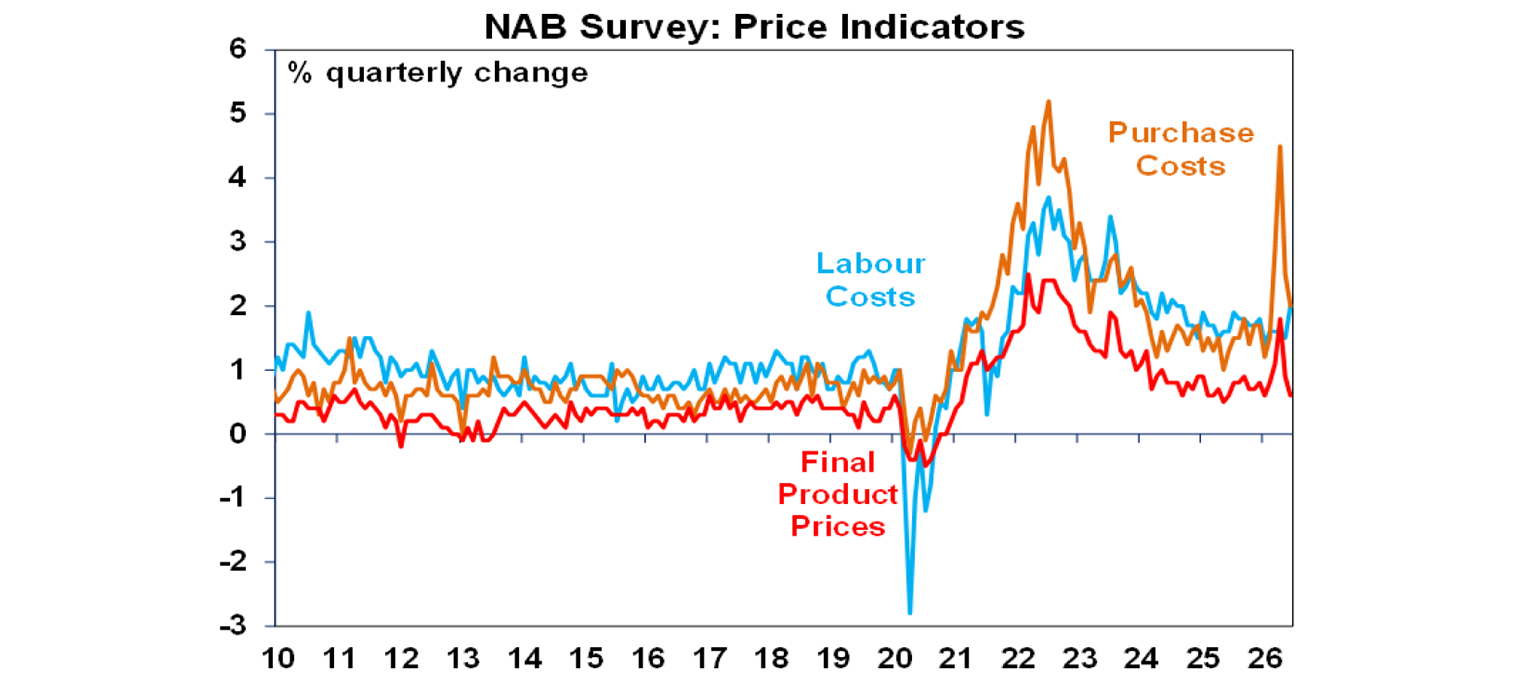

The June NAB business survey showed unchanged business conditions at below average levels, with a rebound in confidence helped by the fall in fuel prices but to still weak levels.

Labour cost pressures increased on the back of the rise in minimum and award wages, but purchase costs and final product price pressures fell further. This is good news and on its own would support the RBA leaving rates on hold, but its vulnerable to the latest rebound in oil prices.

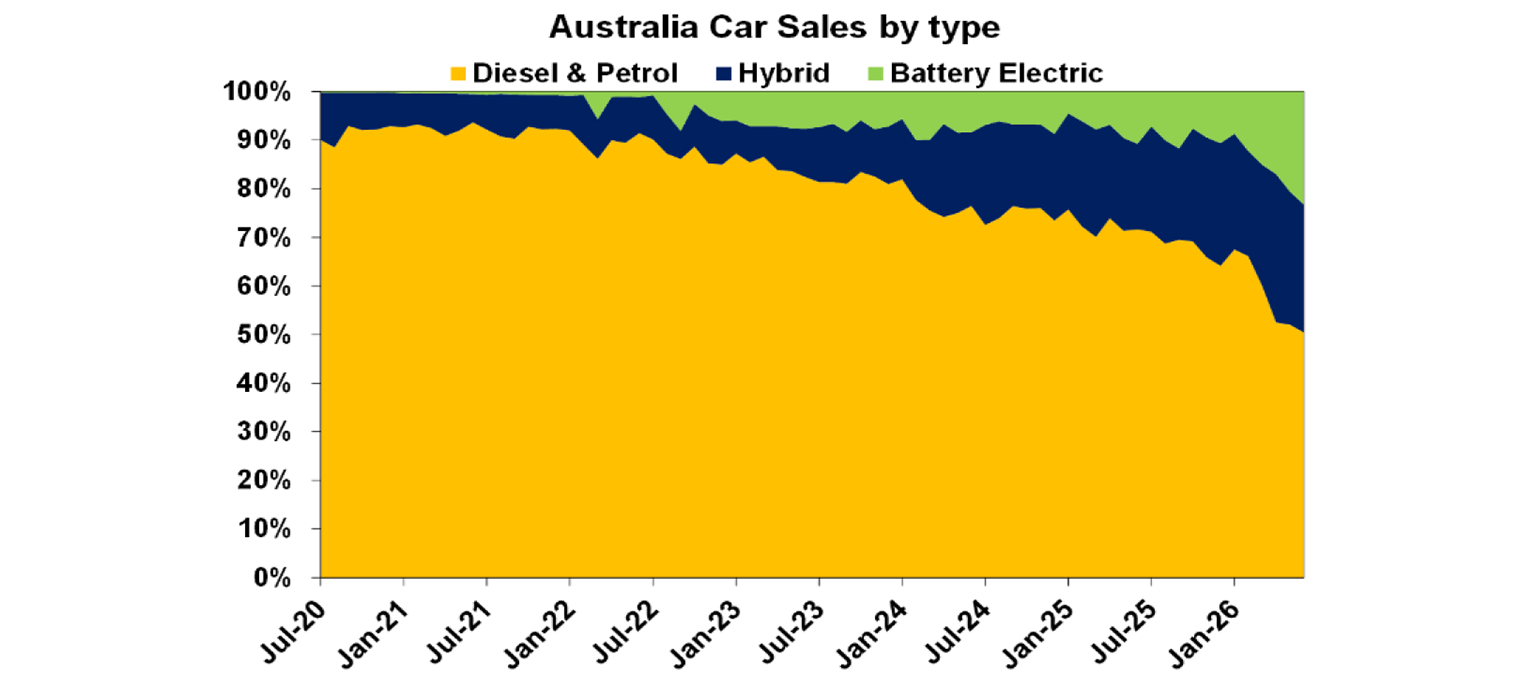

The impact from the oil supply shock can be seen in the next chart. EVs are now over 20% of new car sales and together with hybrids are nearly 50%.

What to watch over the week ahead?

Business conditions PMIs for developed countries will be released Friday and are likely to show some deterioration and rise in cost pressures reflecting the breakdown in the US/Iran peace deal and rebound in oil prices. They are likely to remain in the same rnge as recently though consistent with global growth around 3%.

The US June quarter earnings reporting season will ramp up with the consensus expecting growth around 24%yoy, after 29% in the March quarter. Key to watch will be the AI capex boom and price pressures. Growth is expected to have been led by energy and tech companies.

In the US the temporary Section 122 10% tariff imposed after the reciprocal tariffs were struck down in February expires this coming Friday. They are likely to be replaced by permanent Section 301 tariffs levied on a country, sector and issue specific basis (like the new 25% tariff on Brazil and the forced labour tariff proposed a few months ago) which will likely see the effective tariff rate (after exemptions and substitution) settle around 10% - down from above 30% after Liberation Day but above the pre-2025 level of around 3%. Announcements are likely in the next week but there could be a gap between the Section 122 expiry and the startup of some Section 301 tariffs – so there may be a brief tariff free period. The key is that US tariffs will remain a longer-term threat to global trade and US costs and efficiency but a new short-term disruption is unlikely. The proposed (and laughable!) 12.5% forced labour tariff on Australia will hopefully be lowered back to 10% - but either way the impact on Australia will be mild.

Canadian inflation for June (Monday) is likely to have fallen to 3%yoy with the core measures staying around 2%.

The ECB (Thursday) is expected to leave rates on hold at 2.25% after hiking at its last meeting with core inflation close to target but it’s likely to retain a tightening bias.

Japanese inflation for June (Friday) is likely to have risen to 1.7%yoy, with core inflation rising slightly to 1.4%yoy.

New Zealand June quarter inflation (Tuesday) is likely to rise to 4%yoy.

In Australia, expect June jobs data (Thursday) to show an 18,000 rise in employment with unemployment at 4.4%.

Outlook for investment markets

Global and Australian share markets are likely to remain volatile with the risk of another correction given the resumption of the Iran War and blockage of the Strait of Hormuz, stretched valuations, sticky inflation, political uncertainty associated with Trump & the midterm elections and worries about the impact of AI and whether there is an AI bubble. However, returns should still be positive for the next 12 months as a whole thanks to continuing economic growth with recession avoided and solid profit growth.

Bonds are likely to see returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home prices are expected to fall around 2% this year and by 6% over the next 12 months as a result of poor affordability, RBA rate hikes, reduced investor demand flowing from the winding back of negative gearing and the capital gains tax discount and poor confidence. This will mean roughly a 7% top to bottom fall.

Cash and bank deposits are expected to provide returns around 4-5%.

The $A is likely to rise reflecting the wider interest rate differential to the US, although a move to Fed hikes may limit this. Fair value for the $A is around $US0.72.

Dr. Shane Oliver,

Head of Invesment Strategy and Chief Economist, AMP

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.