Oliver's insights

Why have Australian living standards “fallen” and how do we fix it?

For the last few years there has been much talk of a “cost-of-living” crisis in Australia and of “falling living standards”. This has flared up again lately with the pickup in inflation resulting in a renewed fall in real wages.

6 min read

Key points

Falling real wages and a surge in tax and interest payments over the last five years have led to a slump in Australians’ living standards.

But a broader driver of the malaise in living standards has been a slump in productivity growth from over 2% pa in the 1990s to near zero since 2016.

Amongst other things this has led to a worse growth/inflation trade-off than was the case prior to the pandemic and higher than otherwise RBA interest rates.

Key policies to boost productivity growth include: tax reform; reducing the size of the public sector; deregulation; greater incentives to invest; and competition reforms.

Introduction

For the last few years there has been much talk of a “cost-of-living” crisis in Australia and of “falling living standards”. This has flared up again lately with the pickup in inflation resulting in a renewed fall in real wages. And in the last week the OECD noted that: a 5% fall in real wages over the last five years was amongst the worst in OECD countries; Deloitte Access Economics noted that on its growth forecasts for the next two years Australia was heading for its worst stretch of growth below 2% since the early 1990s; and the media reported that Australia’s underlying rate of inflation was around the highest in developed countries.

This of course is a far cry from what we were used to in the decades prior to the pandemic. In the 1980s a collapse in national income following years of stagflation, i.e., poor growth and high inflation, galvanised the Hawke/Keating Labor Government to undertake supply side productivity enhancing economic reforms to get the economy back on track. These were continued in the Howard/Costello years and Australians saw rapidly rising material living standards. This in part contributed to the IMF referring to “Australian Exceptionalism” given its strong performance compared to other developed countries and was highlighted in a 2018 cover story in The Economist magazine titled “Aussie Rules…what Australia can teach the world” and referred to “the wonder down under”. Unfortunately, this turned out to be another example of the tendency for magazine covers to jump on to something just when it’s about to reverse!

In fact, to borrow from journalist Paul Kelly’s new book, Australian Exceptionalism had by then already entered the “twilight zone” as since the late 2000s the wheels fell off the reform agenda and productivity started to suffer but it had been masked by strong export earnings so no one really worried. Since the pandemic, though, the malaise has become clearly apparent. So, what went wrong and how do we fix it?

Weaker living standards

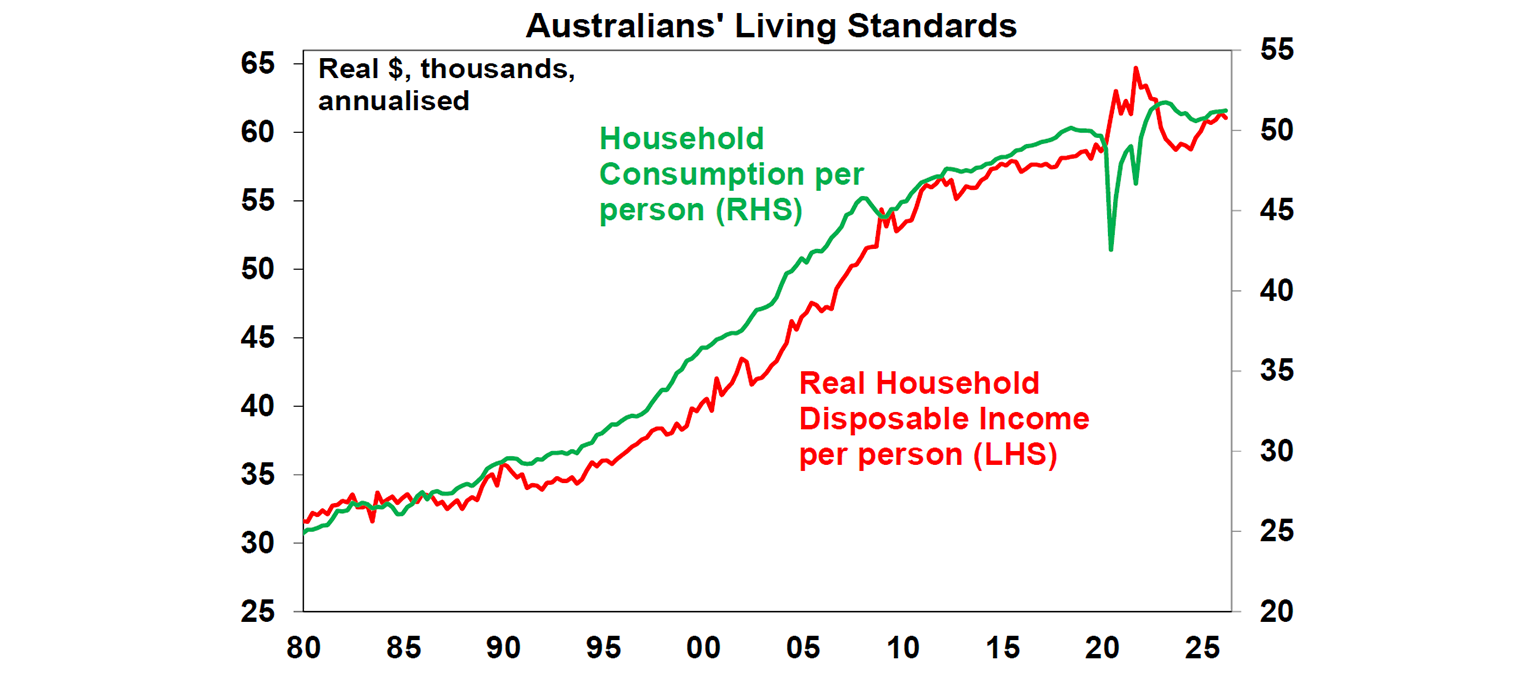

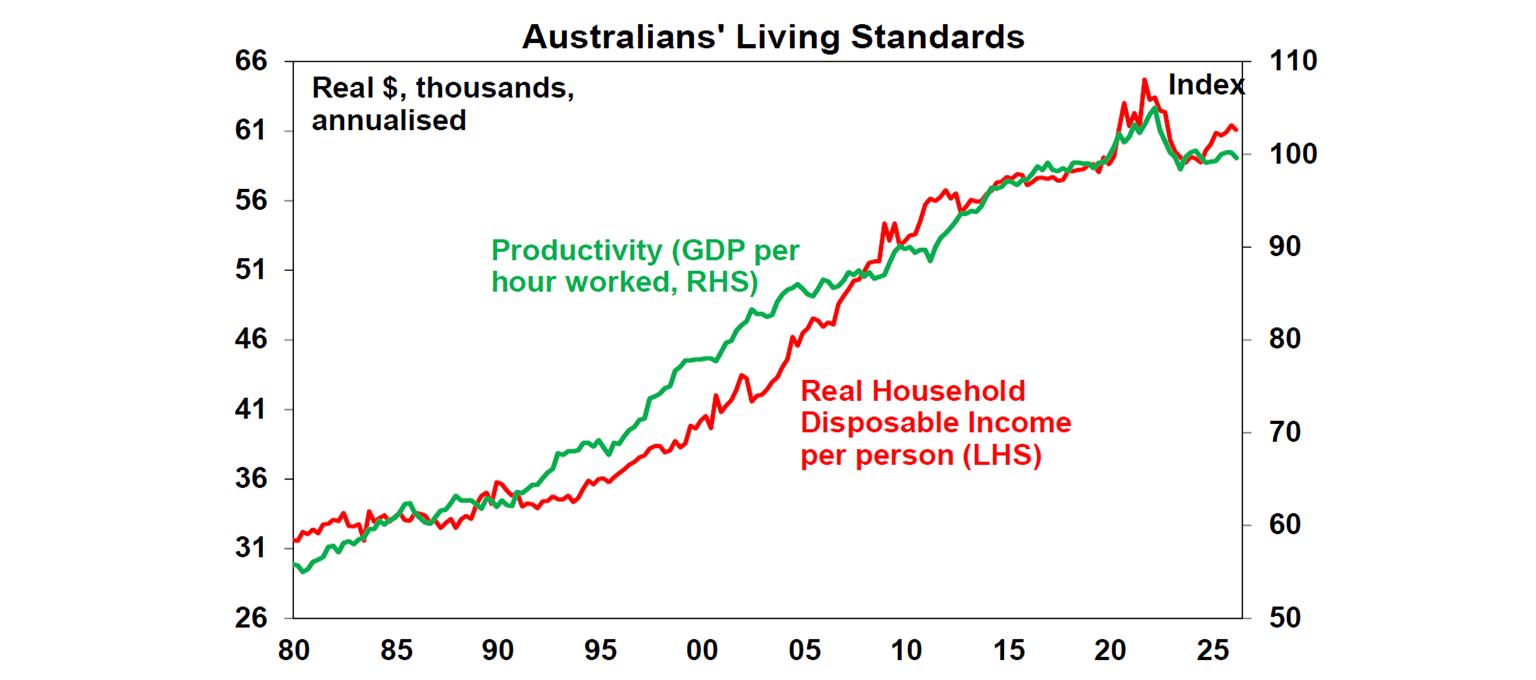

The deterioration in living standards can be seen in various indicators. Often referred to in the last few years has been the slump in real household disposable income per capita which shows the value of incomes after allowing for tax, mortgage debt payments and inflation. It’s a far broader measure of household income than just wages. See the red line in the next chart.

This of course is a far cry from what we were used to in the decades prior to the pandemic. In the 1980s a collapse in national income following years of stagflation, i.e., poor growth and high inflation, galvanised the Hawke/Keating Labor Government to undertake supply side productivity enhancing economic reforms to get the economy back on track. These were continued in the Howard/Costello years and Australians saw rapidly rising material living standards. This in part contributed to the IMF referring to “Australian Exceptionalism” given its strong performance compared to other developed countries and was highlighted in a 2018 cover story in The Economist magazine titled “Aussie Rules…what Australia can teach the world” and referred to “the wonder down under”. Unfortunately, this turned out to be another example of the tendency for magazine covers to jump on to something just when it’s about to reverse!

In fact, to borrow from journalist Paul Kelly’s new book, Australian Exceptionalism had by then already entered the “twilight zone” as since the late 2000s the wheels fell off the reform agenda and productivity started to suffer but it had been masked by strong export earnings so no one really worried. Since the pandemic, though, the malaise has become clearly apparent. So, what went wrong and how do we fix it?

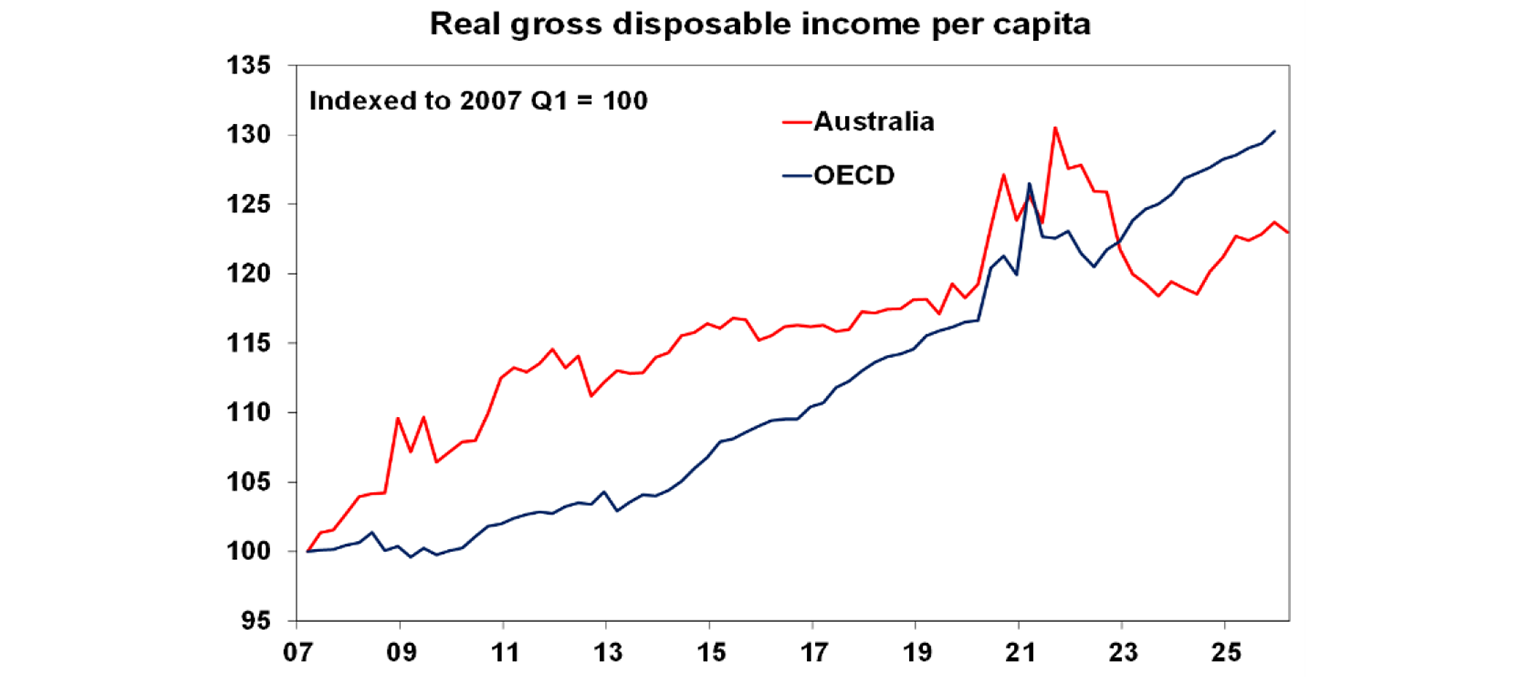

Since its high point in 2021, it fell more than 9% into 2023-24. It’s still 5.6% below its high, and is now showing signs of slowing again. Of course, the slump was exaggerated because it came off the back of a surge through the pandemic due to payments like Job Keeper. But even allowing for that, real disposable income per person is up only 0.6% pa over the last decade, compared to 2.3% pa growth over the prior 20 years. This in turn has resulted in even slower growth in real consumer spending per person. And real disposable income has been much weaker here than across OECD countries, where on average its risen above the highs reached in the pandemic.

So, what’s gone wrong?

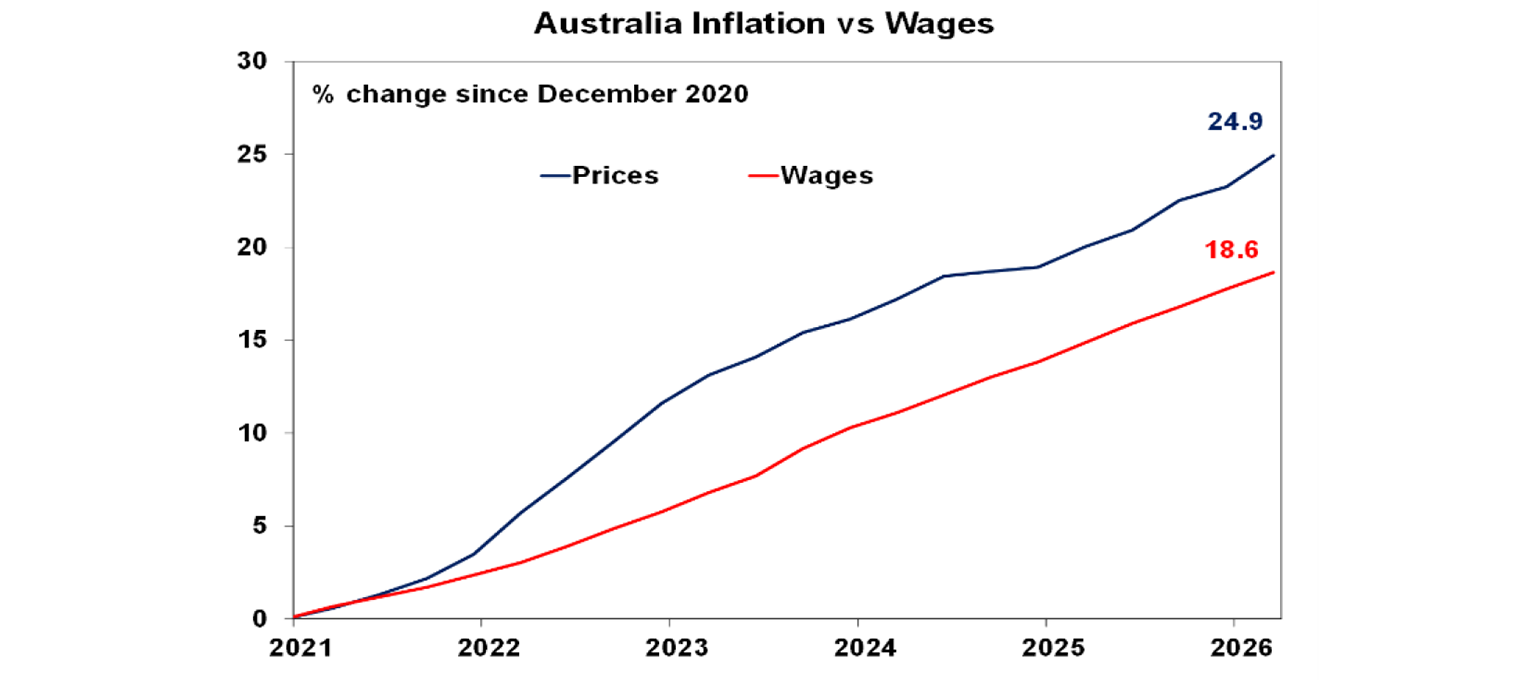

The poor performance in real household income reflects a combination of factors. First, wages have not kept up with inflation since 2021. Since the end of 2020 average consumer prices are up 25%, but average wages have only gone up 19%. So real wages have fallen 6%.

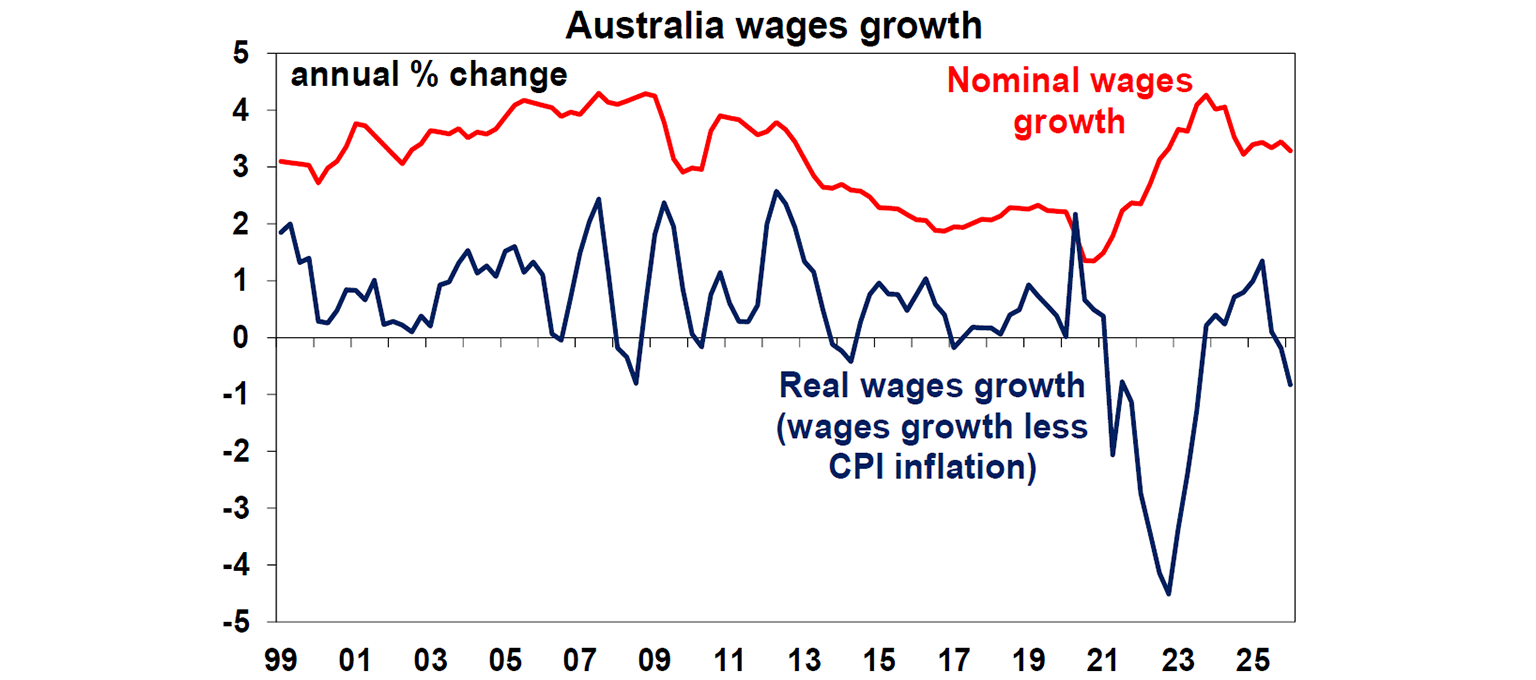

Before the pandemic real wages rose of the time. They did start to rise

again in 2024 and into 2025, but are now reversing again due to the rebound in

inflation

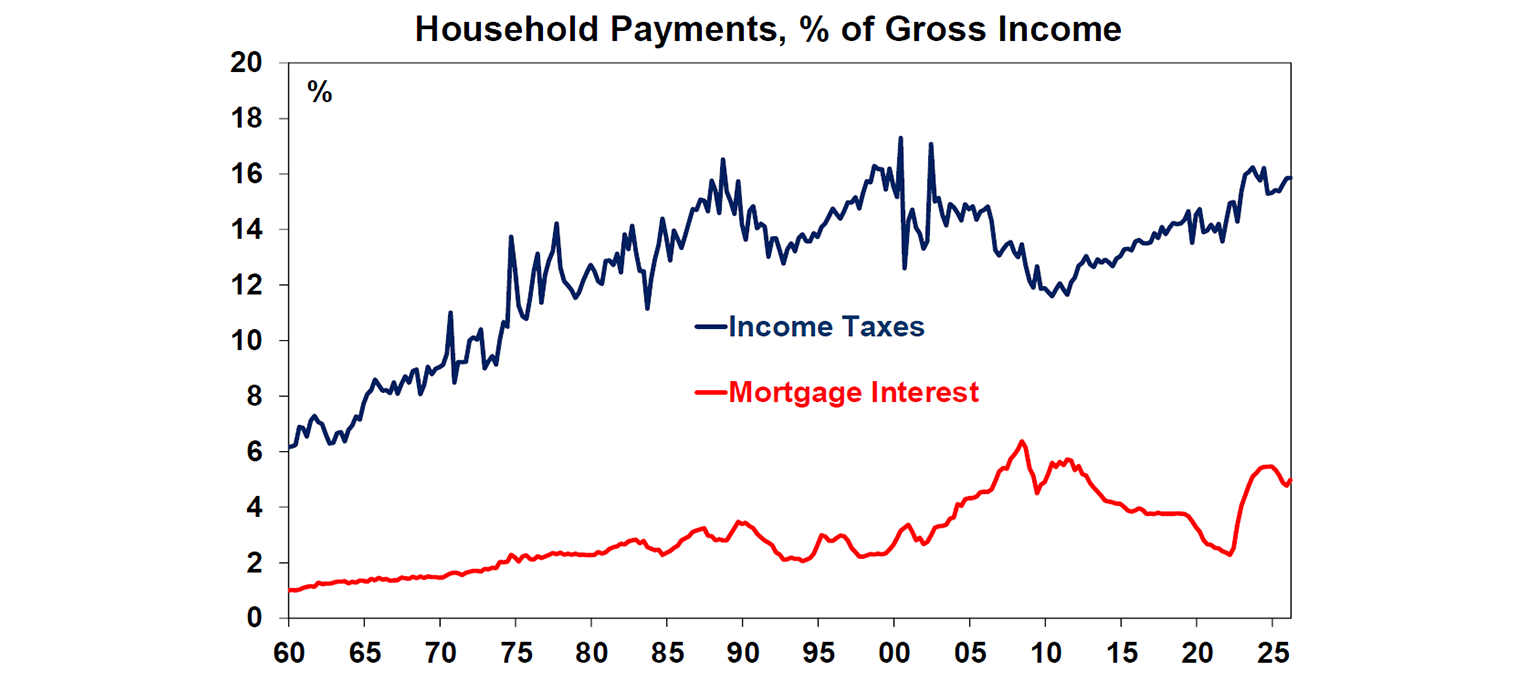

Second, the rise in interest rates since early 2022 saw a big rise in mortgage interest payments relative to income. There was a brief decline last year, but this is now reversing again.

Thirdly, bracket creep has driven income tax payments to a near record high as a share of income further reducing disposable income. The July 2024 income tax cuts provided some relieve but the rising trend has resumed.

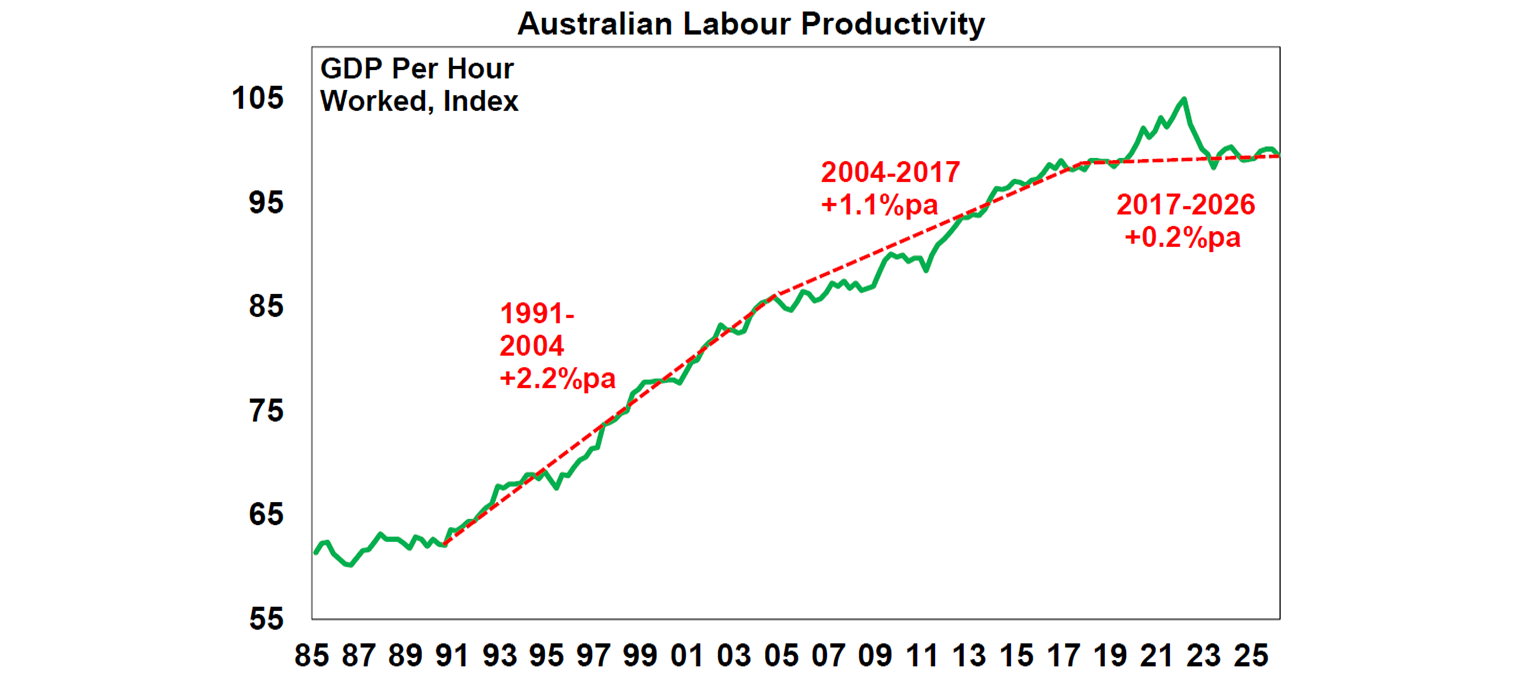

However, a more fundamental driver of the malaise is poor productivity growth. Productivity is often thought of in terms of labour productivity, i.e. GDP per hour worked. It rises when we boost our skills, use more capital like machines or AI or arrange our efforts more efficiently all of which enables us to work smarter and so produce more, which can then be rewarded with rising real incomes. While productivity growth was strong in the 1990s and into the 2000s it slowed from the mid-2000s and has slowed to a crawl since 2016.

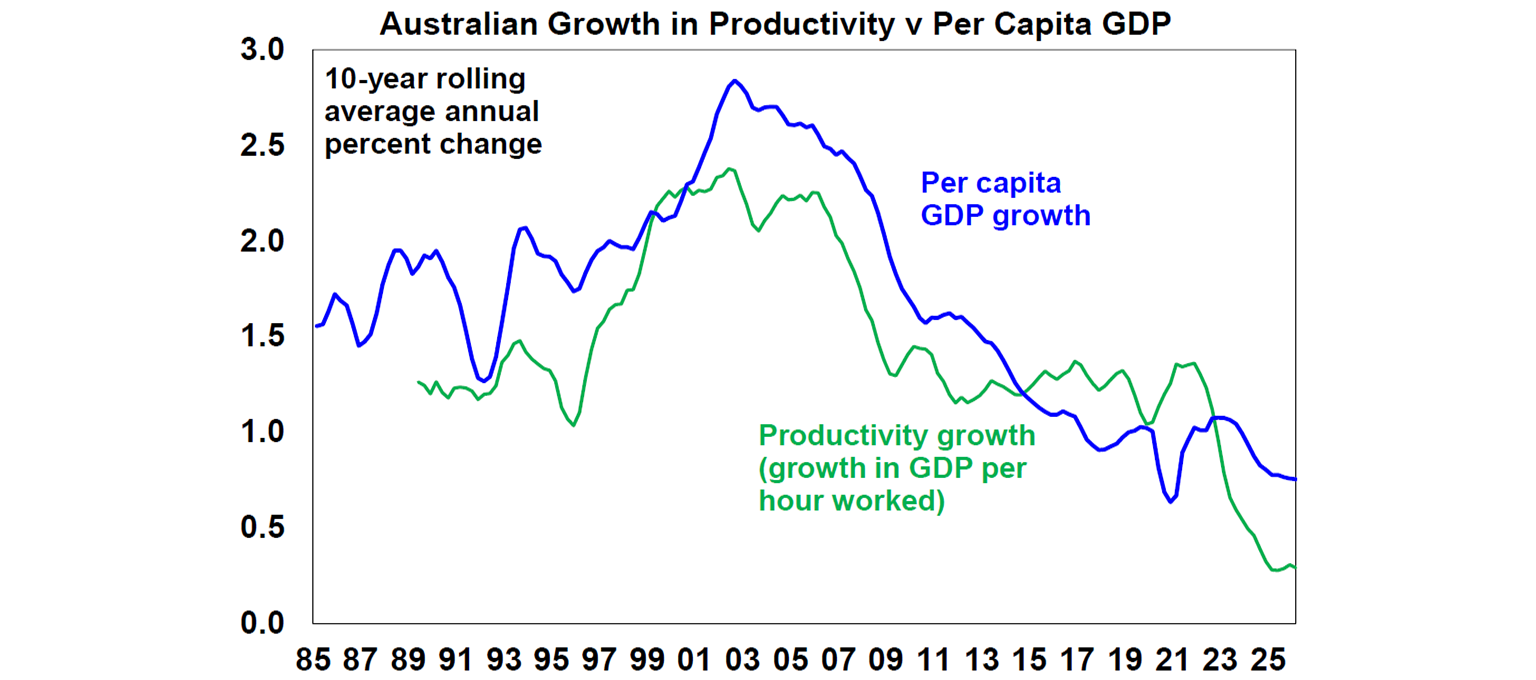

Productivity growth is the main driver of material living standards over long periods. As can be seen in the next two charts, the slowdown in productivity points to ongoing softness in per capita GDP growth…

…and slower growth in household incomes and by implication consumer spending.

We can make up for this by faster population growth, but this doesn’t help living standards per person. Likewise, it can be masked by strong commodity prices and hence national income but medium-term threats to Chinese growth mean we cannot rely on that. Lower productivity growth makes it harder to boost the supply side of the economy to keep inflation down and results in lower real wages growth, slower growth in profits and a reduced ability for the government to provide services.

So, why has productivity growth stalled?

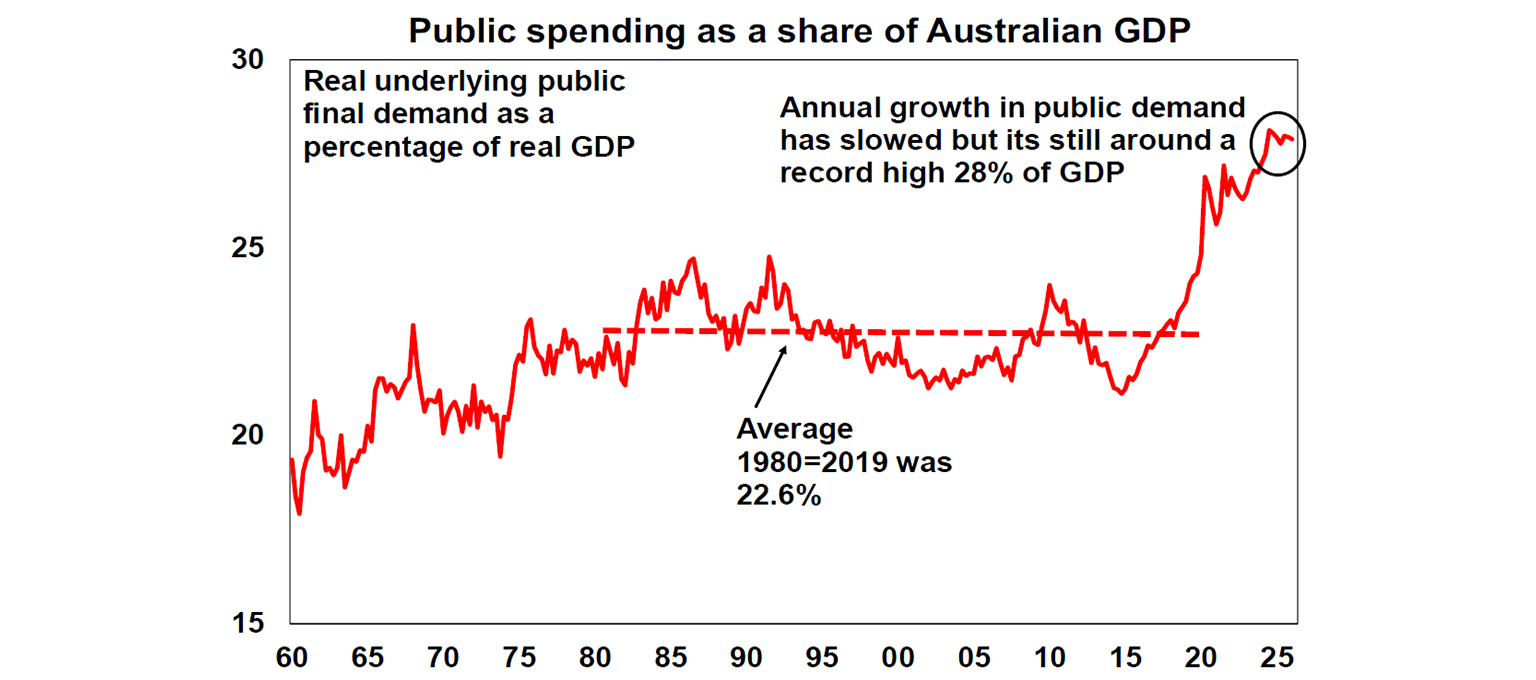

As noted in the introduction, after the malaise of the 1970s and a collapse in export earnings, there was a focus in the 1980s under Hawke and Keating, and then continued under Howard and Costello, on supply side economic reforms designed to improve productivity growth by making the economy more flexible and competitive, improving incentives and improving skills. This saw productivity growth surge through the 1990s into the 2000s and expanded the capacity of the economy to grow without causing inflation. But since then, a range of factors have contributed to slower productivity growth, including: no big new reforms since the GST in 2000 and some backsliding, e.g. with reregulation in industrial relations; very strong population growth has led to urban congestion and poor housing affordability; growth in business investment stalled in the 2010s; market concentration has increased, reducing competition; confusion regarding climate policies contributed to underinvestment in power supply and higher energy costs; and a huge expansion in public spending has taken resources from the more efficient private sector. A good example of the latter has been out of control growth in the NDIS which saw public sector employment rise dramatically over the last few years and health employment as a share of the labour force rise nearly 2 percentage points above its long-term trend.

The surge in public final demand – which is now running around 28% of GDP compared to an average of around 22.6% over the previous 40 years – is particularly significant as the required shift in resources from the private sector to the public sector has been bad news for productivity. That is because public (or non-market) sector productivity is invariably lower than that in the private (or market) sector and because public spending has been squeezing out private business investment, which has weakened private sector productivity.

This has meant a worse growth inflation trade-off

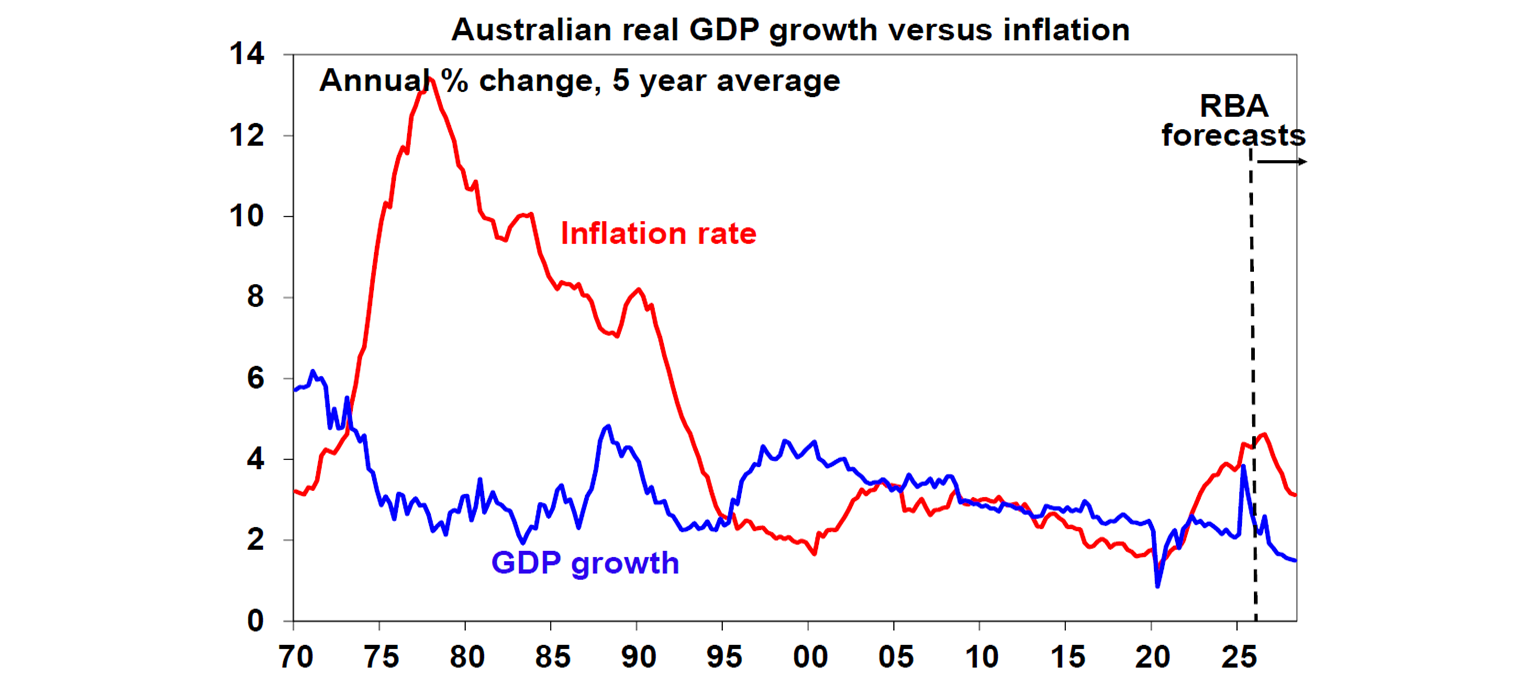

The deterioration in productivity growth has effectively led to a worse growth/inflation trade off. In other words, because the economy is no longer as efficient as it uses to be in boosting the supply of goods and services to meet any pick up in demand (or spending) in the economy – as we saw last year when private sector demand picked up – an acceleration in growth is more likely to result in a higher rate of inflation than used to be the case for any given level of GDP growth. This can be seen in the next chart where the five-year average rate of GDP growth has been trending down (abstracting from pandemic distortions) but the five-year average inflation rate (the red line) has been trending up so far this decade. Of course, this is nowhere near as bad as the 1970s. However, it’s still necessitating higher RBA interest rates and ultimately lower economic growth to tame inflation than would have been the case prior to the pandemic. Hence the observation by Deloitte Access Economics referred to earlier & it’s also evident in the RBA’s own growth & inflation forecasts.

In other words, households with a mortgage are paying for higher levels of public spending via higher mortgage rates. All Australians our paying for the slump in productivity growth with weaker than otherwise living standards.

How to sustainably boost growth in living standards?

If we want to boost living standards and enable sustained real wage growth consistent with the 2-3% inflation target there are no quick fixes. At the risk of sounding like a broken record, the only sustainable way to do it is to boost productivity so we can expand the supply side of the economy and take pressure off inflation. Fortunately, this has been debated for a long time so there are plenty of good ideas out there, including these seven key measures:

Tax reform to rebalance from direct tax to a broader GST, compensate those adversely affected, index the income tax thresholds to inflation and remove nuisance taxes like stamp duty to incentivise work effort and investment and better allocate resources. The Government did move to curtail property tax concessions in the last Federal Budget but with no real cuts to income tax this was more of a tax hike than tax reform and the capital gains tax changes threaten startups and hence productivity.

Put a limit on the size of government spending below 25% of GDP. If we want more government services, we need to find other government spending to cut. Unfortunately, the Budget saw no significant cut to government spending.

Deregulate product and labour markets to remove red tape and boost labour market flexibility, for instance, to make it easier to build new homes. There was a bit of this in the last Budget but much rests with the states and the Government has ruled out industrial relations deregulation.

Provide more incentives to boost investment and adopt new technology. There was a bit of this in the Budget but it was modest and the capital gains tax changes are likely to be a disincentive for some.

Undertake competition reforms to reduce market concentration.

6 .Match population growth to the ability to supply new homes and make it easier for people to live away from congested cities.

7. Reduce climate policy uncertainty and rely more on market signals as to how best to transition to net zero.

While the Economic Reform Roundtable last August and the lead up to the Federal Budget this year offered the hope of the more sustained focus on boosting productivity, this has yet to be really delivered upon. For a deeper look at the productivity malaise and solutions see here.

What’s stopping us?

The problem is that since the GFC, and reinforced by the pandemic, the political pendulum has been swinging in favour of bigger more interventionist government. There is now an expectation that government is the solution to most problems. The economic rationalist policies of Reagan, Thatcher, Hawke/Keating and Howard/Costello are out of fashion. Populist policies are in. Even in the US under Trump.

In the absence of a crisis, it’s hard to see Australian governments undertaking the sort of hardnosed economic rationalist reforms required. Hopefully the “cost-of-living” crisis and the living standard malaise will start to put more pressure on for sensible reforms. We may have a way to go yet though.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important note

While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.