Oliver's insights

Teflon share markets – 5 reasons they’re so resilient despite lots of worries

Over the last 18 months investment markets have faced a string of threats. Many of these have involved the US and President Trump’s policies - tariffs, a US/China trade war, Trump’s attacks on NATO allies, Trump’s attacks on the Fed, and the War with Iran and the associated oil supply shock.

6 min read

Key points

Despite lots of threats over the last 18 months share markets have proved to be remarkably resilient.

This likely reflects a combination of: President Trump’s desire for shares to rise; economic activity data right here right now has been okay; earnings growth has been helped by the AI spending boom; the global economy is awash in excess capital looking for a home; and policy makers have become more assertive in protecting their economies.

However, there is a danger in getting too swept along in positive market sentiment: the Iran War could flare up again; Trump will be less constrained after the mid-term elections; there is a risk that the AI boom is morphing into a bubble; inflation is proving sticky with global central banks starting to hike rates; & share market volatility is at the low end of its normal range which can be a sign of rising risk.

So, while the strong share run could continue for a while yet investors should resist the temptation to take on more risk.

Resilient share markets

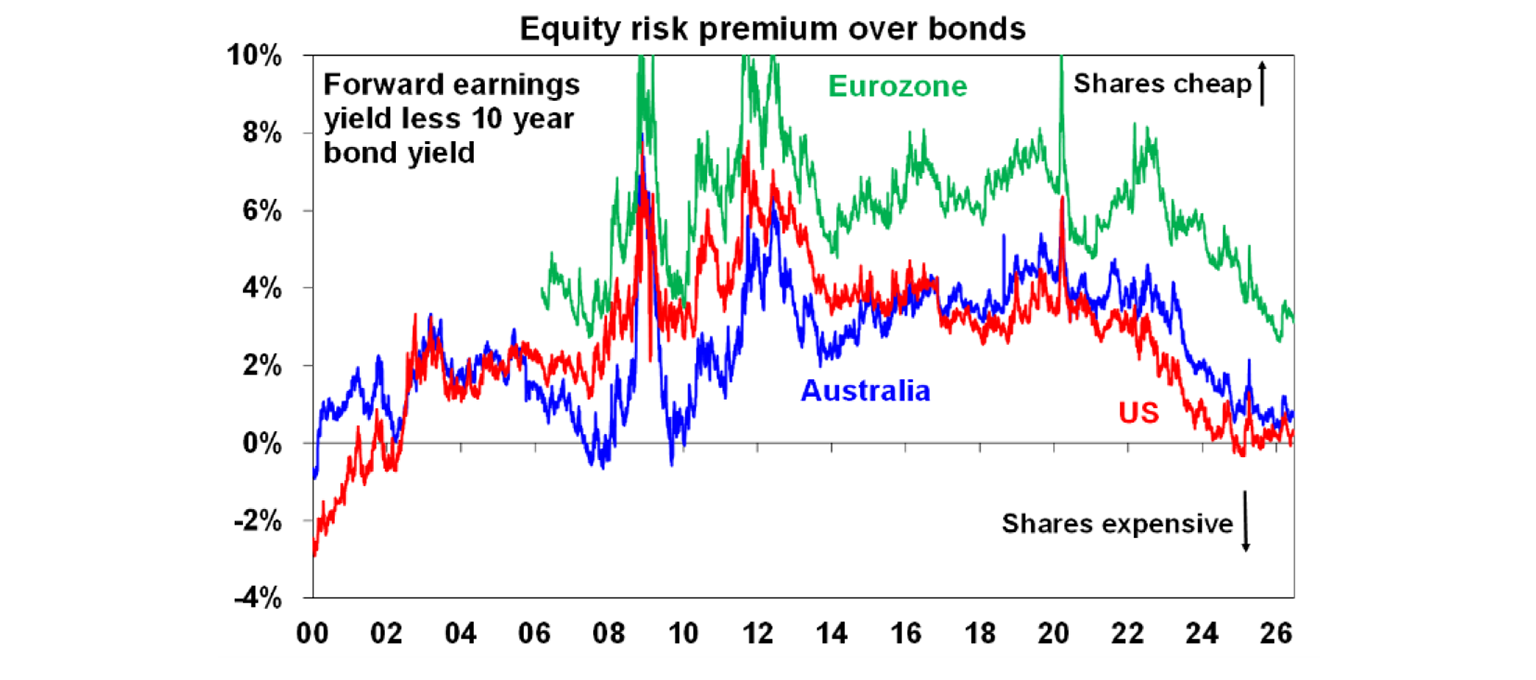

Over the last 18 months investment markets have faced a string of threats. Many of these have involved the US and President Trump’s policies - tariffs, a US/China trade war, Trump’s attacks on NATO allies, Trump’s attacks on the Fed, and the War with Iran and the associated oil supply shock. Even Trump’s erratic policy making itself would normally be seen as a concern. Added to this we have had sticky inflation with major central banks moving towards rate hikes, worries about higher levels of public debt and the continuing War in Ukraine. And this at a time when US and Australian share markets valuations were already stretched with high price to earnings ratios and offering close to zero risk premium over bonds - as measured by the gap between the forward earnings yield and 10-year bond yield. US shares since 2024 have been offering the lowest premium over bonds since the early 2000s and Australian shares have been offering their lowest premium over bonds since the late 2000s.

Sure, there has been corrections with 15-19% falls into April last year and a roughly 9% fall into March this year and Australian shares have been a relative underperformer. But global share markets have bounced back quickly, and returns have remained solid across a broad mix of share markets. Normally it would have been reasonable to expect a much bigger hit to share markets from the 15% or so net blow (after diversions) to oil production from the Iran War. It’s almost as if markets are coated in Teflon. So why the resilience? And can it be sustained?

Five reasons why markets have been resilient

It would be easy to say that investor sentiment is overly optimistic, and this has meant that investors are simply complacent in the face of all the worries. But investor sentiment on most measures is not at excessive levels so it’s clearly a bit more complicated than that. Basically, beyond the ability of the world to draw down oil reserves and so smooth the oil supply shock, there are five reasons markets have been so resilient:

Trump wants shares up and so will TACO when the going gets rough. One of the reasons we didn’t get too fussed about the outlook for share markets when Trump was re-elected was that he views shares as a KPI. He wants them to go up so he can say that “US shares are stronger than ever in the history of markets”. So consequently, whenever the US share market looked threatened last year with say the tariff escalation, he would back down. This of course gave rise to Trump Always Chickens Out (TACO) and with confirmation in relation to other events along the way (eg, in relation to ICE in Minneapolis and his attempt to effectively get control of the Fed) investors have naturally reasoned that the same would apply in relation to the Iran War, which in turn was confirmed from early in March with Trump constantly providing reassurance a deal would be reached. While this was tested along the way with various escalations its basically proved correct with Trump confirming that because he “didn’t want to see economic catastrophe” he sought and signed a peace deal with Iran.

The here and now has been okay. While “soft” economic data like consumer confidence surveys have taken a hit, “hard” data which measures actual spending and activity has remained okay. For example, global growth is still running around 3% which is around normal. The US economy has been growing solidly with strength in business investment offsetting a softer but still okay consumer. And in Australia final demand in the economy has been growing above 2%yoy. History tells us to worry if recession is on the way, but it’s not materialised and so investors have given up waiting.

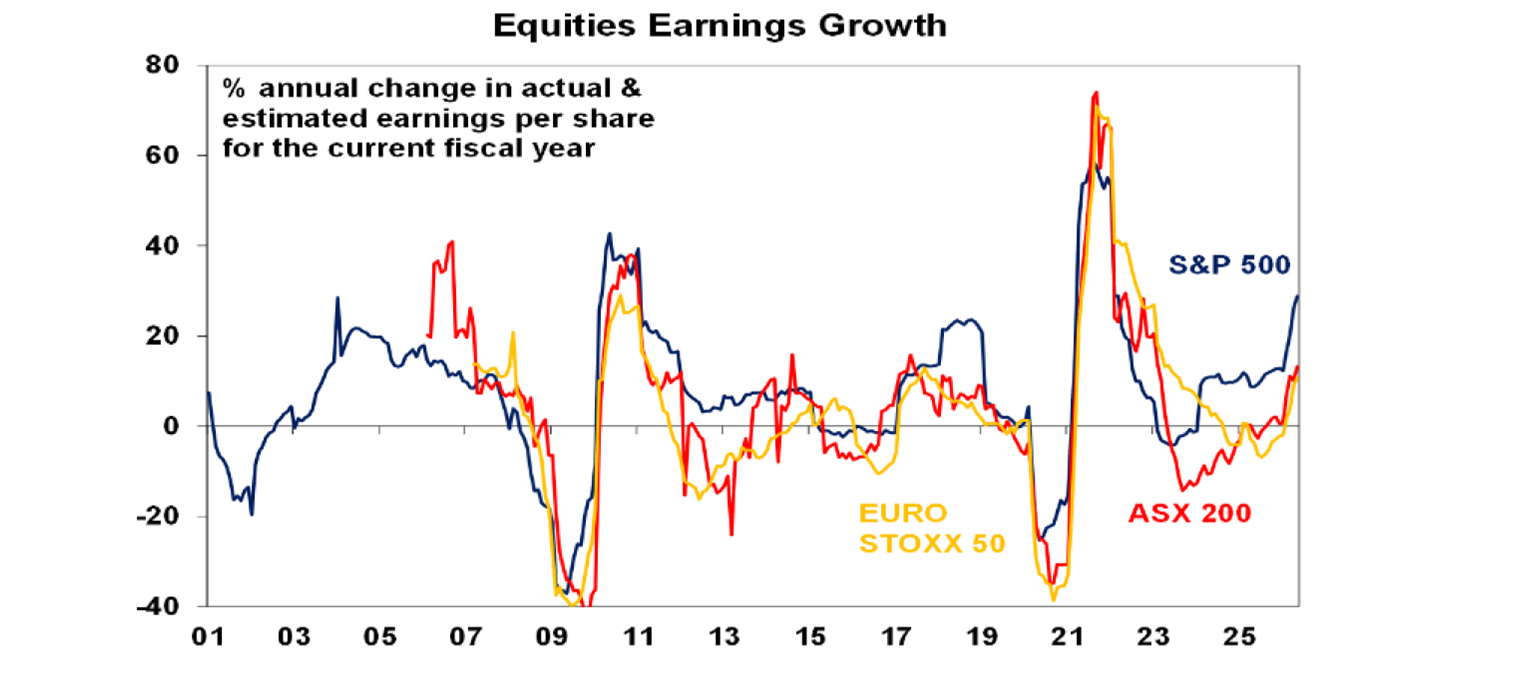

Partly related, to this earnings growth has been on the up. This has particularly been the case for the key direction setting US share market where March quarter earnings growth came in at 29%yoy, well up from initial expectations for around 14%yoy. Much of this owed to AI related demand fuelling growth in tech sector earnings of 61%yoy. Even profit growth in Australia has hooked up. This has been hard for investors to ignore even though political noise has been high.

4. Excess capital looking for a home. This is evident in strong flows into new asset classes like private debt a few years ago and the ease with which the US share market is absorbing record IPOs, although I am not so sure about SpaceX!

5. Policy makers will do whatever it takes to protect economies - and shares like that. This was seen through the GFC which saw big deficit spending and money printing, Eurozone crisis where the ECB and governments did whatever was required to protect the Euro and the pandemic where governments protected companies and citizens from the economic effects of lockdowns. If individuals are increasingly coming to regard government support as normal, then it makes sense that share market investors are doing the same.

The last two are reflected in Macquarie Global Strategist, Victor Shvets’ mantra that “if risk is everywhere, its nowhere”. In other words, while there may be lots of noise beneath the surface up top its relatively calm. In some ways this sounds a bit like the “Great Moderation” buzzword of the 2000s before the GFC came along which reflected the macro stability/ micro instability of the time amidst evidence that economic cycles had become less volatile with low and stable inflation.

Six reasons not to get too carried away

Of course, a big risk in this environment of relatively strong returns is that investors assume it will continue indefinitely and so increase their allocation to shares and thereby take on a higher allocation to riskier assets than originally planned setting up an eventual bubble. And it probably can go on for a while yet. But there are five reasons for caution.

Trump’s luck could run out. For example, his TACO on Iran may not work. It looks increasingly like Iran won – its navy and air force are gone but its regime is stronger, it still has missiles, it can still support its proxies, it nuclear program is yet to be resolved and who needs it anyway when they have shown they can block the Strait of Hormuz. The peace deal already looks fragile – maybe Hezbollah and Israel both have an interest in making it fail – and even if it does hold for a while it could all flare up again threatening global oil supply anew.

Related to this, Trump will likely be less constrained after the mid-terms and could go harder on foreign conflicts. If he just loses the House and retains the Senate, he may be motivated to do bi-partisan deals with the Democrats on domestic policies, eg, to tax billionaires and AI (well maybe!). But more broadly the Republicans’ likely loss of control of at least the House and maybe the Senate will see Trump focus more on foreign affairs as a lame duck president risking more flare ups including over Iran and maybe Greenland again or Cuba (which is less relevant directly but sends a signal to China that if the US can do whatever it wants in its backyard then maybe it can too).

Although we think it has further to go in the near term there is increasing risk that the AI phenomenon is morphing into a bubble. IPOs are surging and debt is surging to fund data centre capex.

While US, global and Australian economic data for growth and profits have been okay this may just be due to long lags. This is not our base case but it’s a risk. For example, its taken a decade for the full disruptive impacts of Brexit to become apparent for the UK.

Inflation globally is proving sticky and central banks are increasingly moving towards rate hikes. So far this decade, we have seen four global inflation shocks – the pandemic, Ukraine, the oil shock and the AI data centre boom - or five in the US with Trump’s tariffs. And deglobalisation, decarbonisation, increasing defence spending and bigger government suggest a more inflation prone world. The RBA led the charge to higher rates and other countries are starting to follow. All of which could threaten shares at some point.

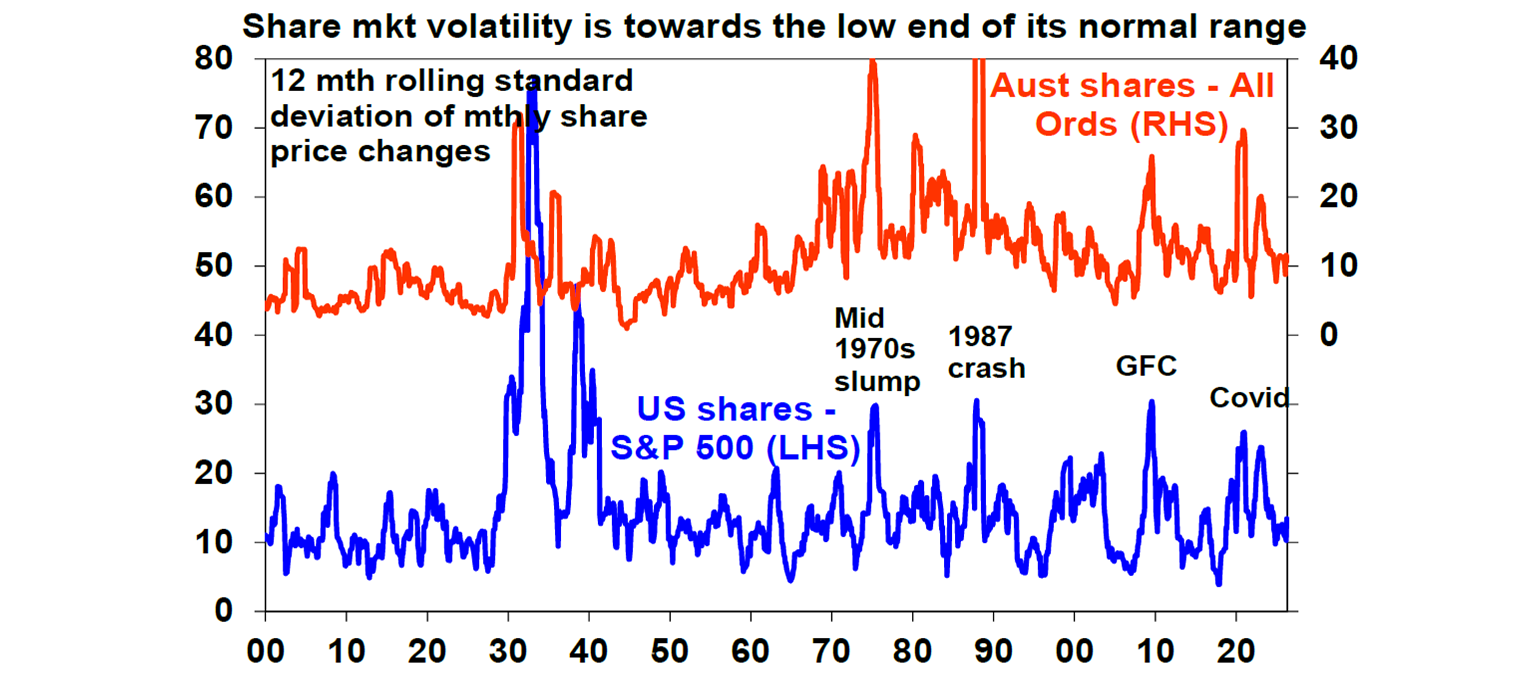

Finally, share market volatility is relatively low. While this period seems unusual with relatively resilient markets and solid average returns despite lots of things to worry about it’s not that unusual historically. In particular, share market volatility is not out of the normal range it’s been in for the last century or more in the US and Australia. However, it is at the low end of the range and long periods of low volatility can give way to periods of higher volatility – which in the past have been associated with share market falls.

Concluding comment

In short, history warns that it’s dangerous to assume that there is no cycle and no risk. As Howard Marks, co-founder and co-chair of Oaktree Capital Management observed “The riskiest thing in the world is the belief that there’s no risk.” The danger is that this can often lead to excessive exposure to shares which eventually leaves shares vulnerable to a fall.

This is not say we are there yet, but it’s not wise for investors to increase their allocation to shares just because of recent past strong gains. Given the difficulty in timing markets the best approach remains to adopt an appropriate long term investment strategy consistent with your wealth, income, spending requirements and risk tolerance and stick to it.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important note

While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.