Oliver's insights

The RBA undertakes a hawkish pause – we continue to expect a further rise in rates

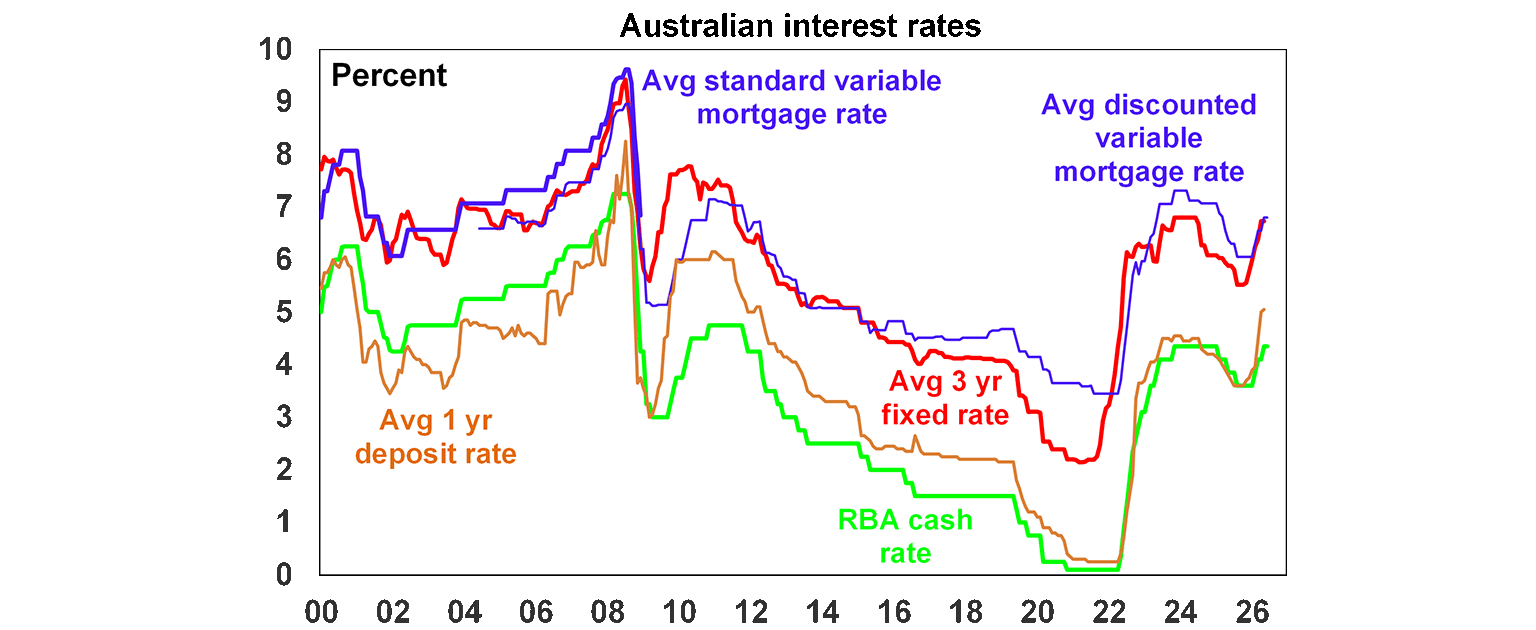

The RBA’s decision to leave rates on hold at 4.35% was no surprise with the money market pricing in no change ahead of the meeting and all 26 economists surveyed by Bloomberg expecting the same.

6 min read

Key points

After three consecutive rate hikes the RBA left rates on hold at 4.35% at its June meeting.

However, the RBA retained a tightening bias noting that inflation Is “still too high” and is likely to remain so for some time and that it will do whatever is necessary to achieve its mandate, “including increasing the cash rate further if required”, but with no reference to cutting it.

We are continuing to allow for a further rate hike in August and have another one pencilled in for November reflecting the still rising trend in underlying inflation and risks that it will take longer to bring it back under control.

The US/Iran peace deal likely heads off a worst-case scenario in terms of a further hit to inflation and growth – but the RBA is likely to remain wary of the second-round flow through to inflation from still high oil prices and the oil supply disruption that “will take some time to resolve”.

The RBA in wait and assess mode

The RBA’s decision to leave rates on hold at 4.35% was no surprise with the money market pricing in no change ahead of the meeting and all 26 economists surveyed by Bloomberg expecting the same. This followed three consecutive hikes which fully reversed last year’s cuts and taken the cash rate back to the level reached in 2023. The decision to hold was unanimous.

Why the RBA left rates on hold

In leaving rates on hold, the RBA noted that there are signs that the economy is slowing as expected (and required to cool inflation) and that it was appropriate to leave rates on hold as it assesses the response to the three previous rate hikes this year. In this regard it noted that financial conditions have tightened, consumer spending is showing signs of slowing and house prices are falling in some cities. Given all this, pausing to assess makes sense.

Against this though the RBA noted that while unemployment rose in April other labour market indicators are more resilient, business investment is strong, resolution of the War is at an early stage with oil supply issues likely taking time to resolve and maintaining upwards pressure on inflation and most importantly inflation is still too high and is likely to remain so for some time and that some firms are passing on cost increases. RBA Governor Bullock also noted that demand in the economy has to slow to get inflation down and that “unless we get inflation down then ultimately it will lead to higher unemployment.”

All of which suggests that while the RBA has paused its rate hikes, its primary concern remains excessive inflation. This was highlighted in the final paragraph in the RBA’s post meeting Statement where it noted that it will be “attentive to the data” as always but that “it will do what it considers necessary” to deliver on its dual price stability and full employment mandate, “including increasing the cash rate further if required.” Its omission of any reference to cutting the cash rate taken in context with its ongoing concerns about inflation indicate that it retains an inclination to raise rates further.

So, this month’s pause should not be taken as a sign that we are necessarily at the top on rates.

Governor Bullock’s press conference comments basically reinforced the Bank’s concerns about inflation and left the door open for further interest rate hikes if needed.

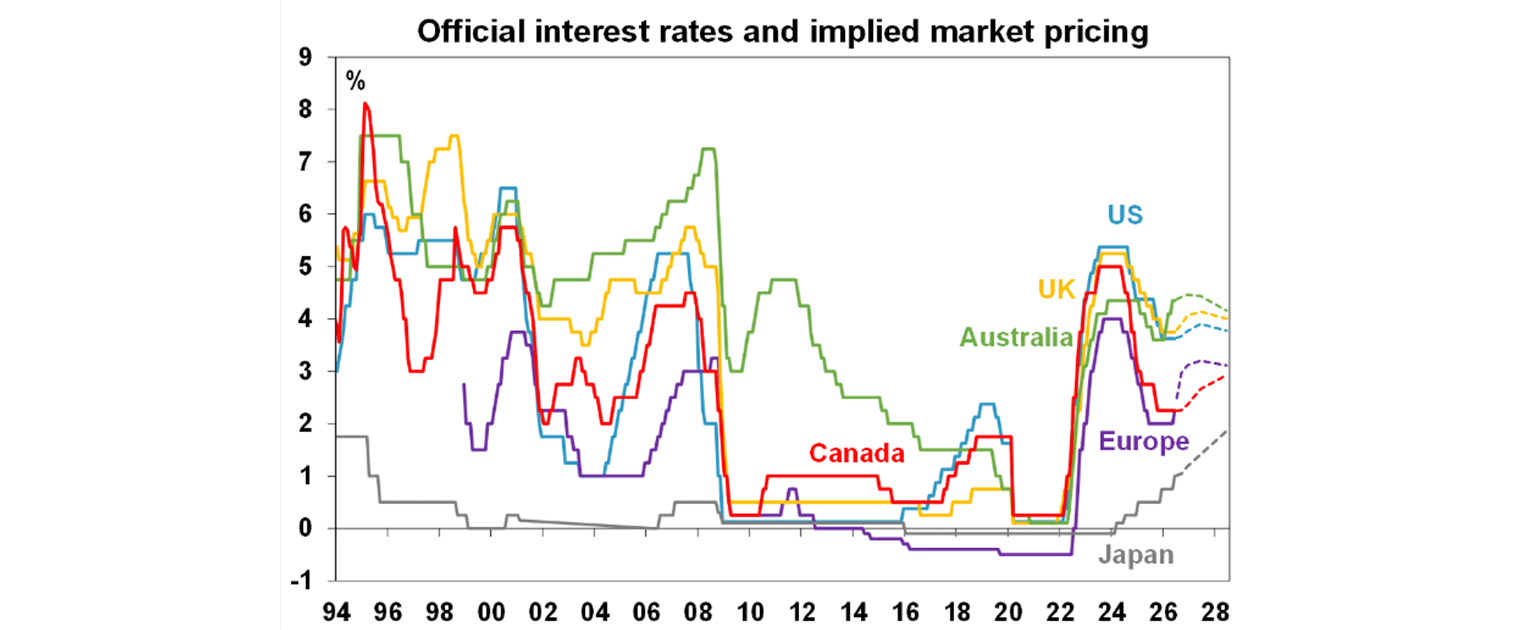

The money market is still expecting around a 55% probability of another hike in Australia by year end with Australian interest rates expected to remain higher compared to other major countries. This reflects other major countries mostly having inflation much closer to target before the War started, whereas Australia already had an inflation problem which the oil shock has threatened to exacerbate.

We continue to expect a further rise in interest rates

We are continuing to allow for a further rise in interest rates with the next hike likely to come in August as underlying inflation is still trending up with business surveys and the stronger than expected award wage rise this year warning of ongoing cost and price pressures, posing a high risk that inflation expectations will move higher.

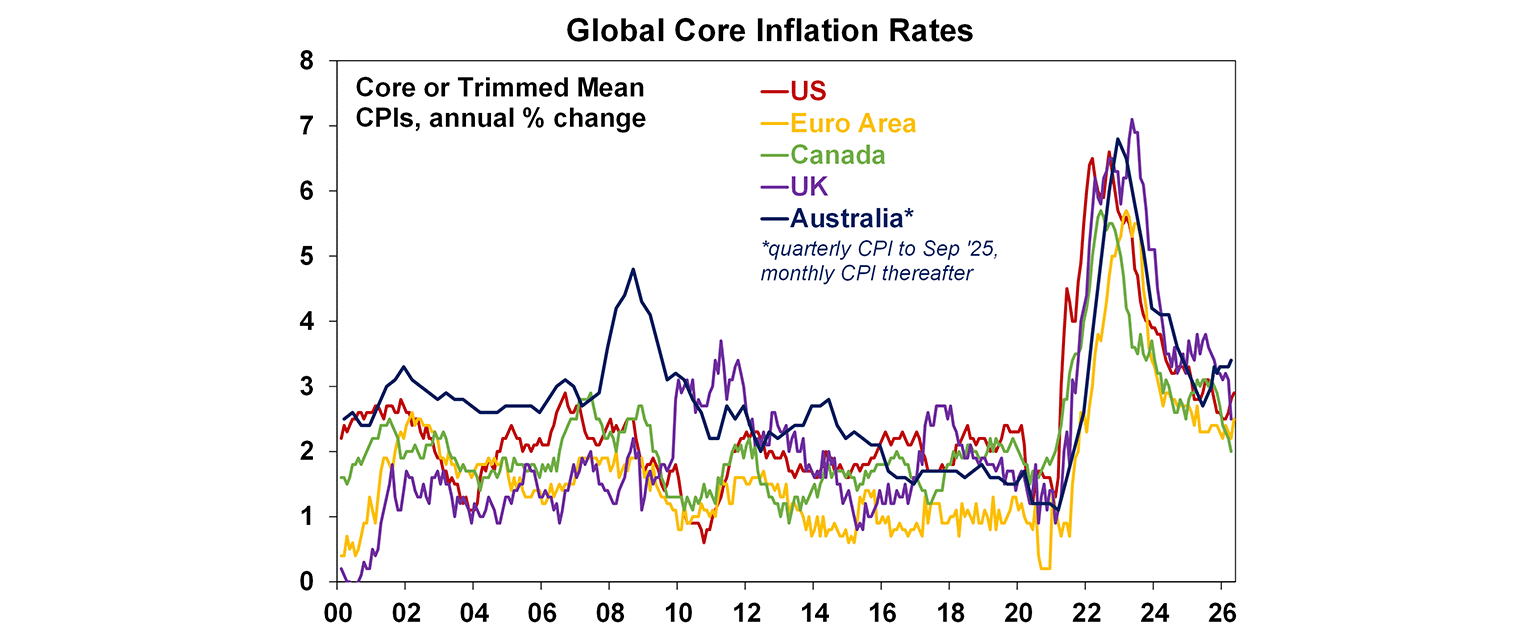

Trimmed mean inflation rose to 3.4%yoy in April and appears on track with the RBA’s forecast for a 0.95% rise in the June quarter taking it to 3.8%yoy. RBA Governor Bullock confirmed this in here press conference.

The Fair Work Commission’s granting of a 4.75% increase in award wages and 6% increase in the minimum wage from July – impacting around 21% of the workforce - was a higher-than-expected acceleration from last year’s 3.5% increase and along with its influencing effect on other wages points to an acceleration in wages growth this year. As its unsupported by productivity growth which is running around 0.3%yoy, it points to a further acceleration in cost pressures.

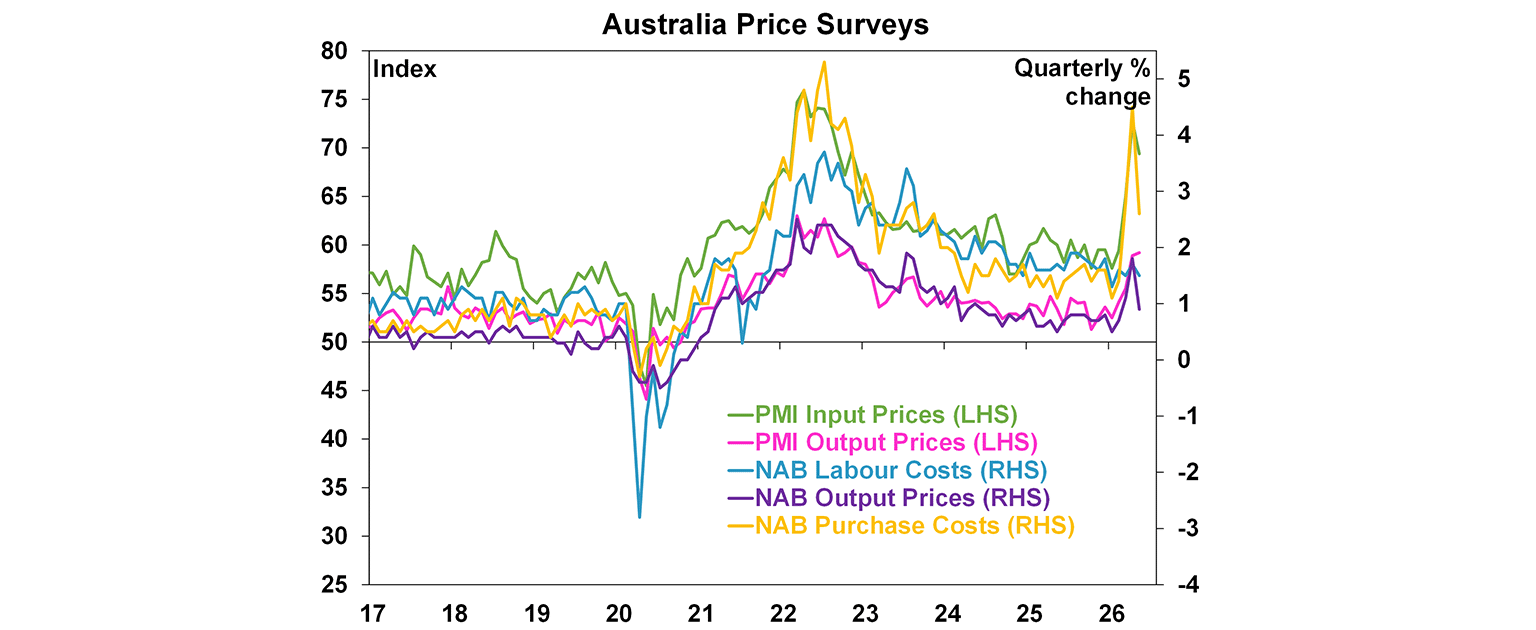

While the NAB business survey and PMI for May showed some easing in cost and price pressures, both show them remaining elevated and running well above pre-pandemic levels.

The US/Iran peace deal – assuming it’s delivered upon and leads to a reopening of the Strait of Hormuz – is good news but the RBA is likely to remain wary. The deal likely heads off a worst-case scenario in terms of a stagflationary further boost to inflation and hit to growth and should see energy prices fall further. But the fall is likely to be gradual, and the RBA is likely to remain concerned of the second-round flow through to underlying inflation from the supply disruption that will take a while to return to resolve.

The oil supply shock coming on the back of the 2022 pandemic and Ukraine related supply shocks risks locking in higher inflation expectations. The combination of bigger government, deglobalisation, decarbonisation, increasing defence spending and aging populations are all making the global and Australian economies more inflation prone and the run of supply shocks is only adding to this. Inflation expectations tend to be backward looking, and the longer inflation stays above target - and it now looks like doing so for five of the last six years including the present year - the more people will expect it to stay above target and so for inflation expectations to rise. In the last five years Australia’s headline inflation rate has been above 3% for 44 months or 73% of the time and trimmed mean inflation has been above 3% for 51 months or 77% of the time. The longer this continues the less Australians’ will have faith in the 2-3% target. This will show up in faster wage demands and businesses more inclined to put through price rises more regularly. All of which risk making it harder for the RBA to get inflation back down

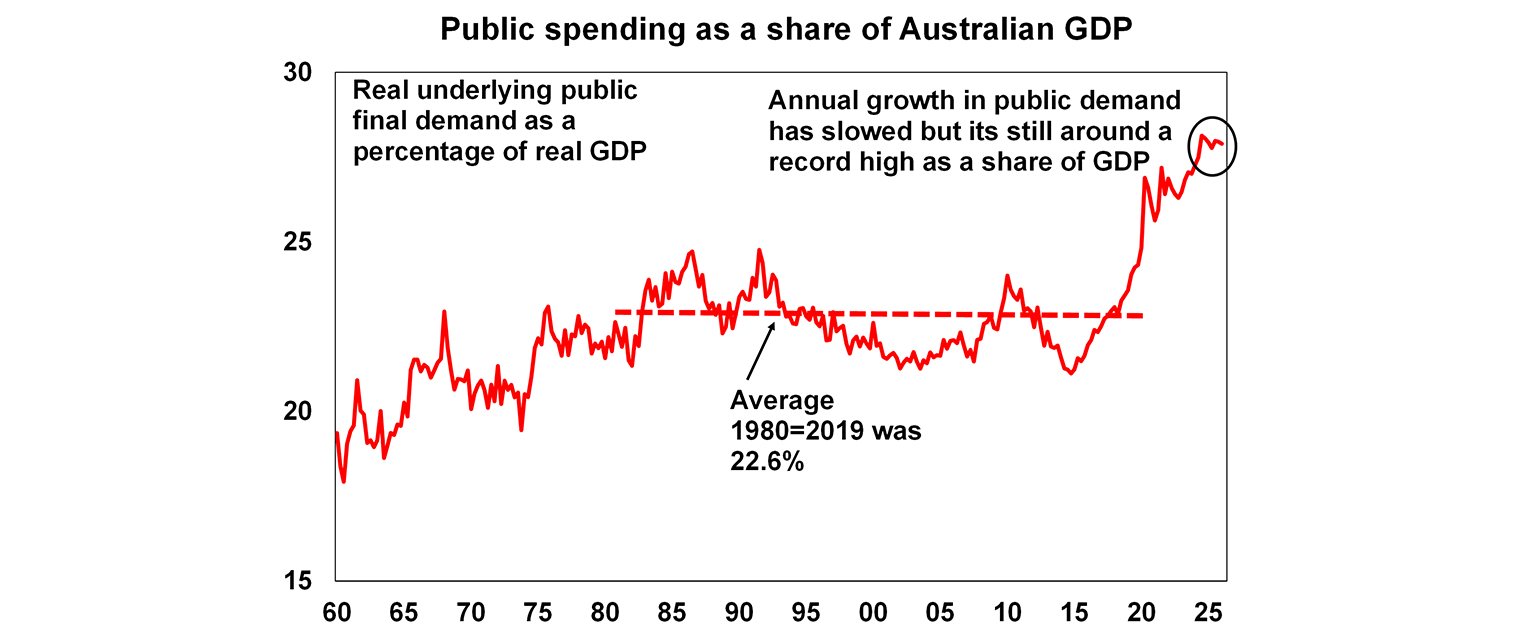

Ideally, the Government could have taken pressure off the RBA in the May Budget by cutting back spending for the year ahead in order to free up capacity in the economy and doing more to help boost productivity. Unfortunately, though Federal spending is projected to remain around 27% of GDP for the next few years, which is well above pre-pandemic levels and in turn implies that public spending overall will remain around 28% of GDP, which is also well above pre-pandemic levels. There were some good moves to deregulate in the May Budget but these will take years to bear fruit and the wind back of tax concessions - around negative gearing, capital gains and trust - amounting to a tax hike will likely be neutral to slightly negative for productivity.

So, to provide confidence that underlying inflation will come back to target in a reasonable time frame and that inflation expectations will remain consistent with the target we are continuing to allow for a further rise in rates, with the next hike likely to come in August and another one pencilled in for November.

Failure to bring inflation back to target in a timely manner will only mean more pain for Australians - but particularly low-income households - facing ongoing cost of living pressures and stagnant/weak growth in living standards. On this I completely agree with the RBA.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset. -

Weekly market update - 17-07-2026 Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation.

Important note

While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.