Econosights

The Economics of Taxing Natural Resources: Why it’s not just “tax gas more”

Australia is a major beneficiary of the natural resources trade, with mining exports alone contributing about 13% of the economy. The rise of China, alongside global population growth, urbanisation and industrialisation, has further increased our reliance on resource sales, particularly iron ore, coal, LNG, battery metals, and gold.

7 min read

Key points

Australia’s mining sector already pays substantial company income tax versus other industries, but royalties and rent taxes exist to capture public ownership of resources.

Across onshore mining, state royalties average ~6.4% of production value; given persistently higher mining profit margins, there’s a case to lift effective royalties.

Offshore gas doesn’t pay royalties; the Petroleum Resource Rent Tax is meant to tax economic rent, but design features (uplifted deductions, deductions timing, midpoint pricing for LNG) have kept collections low. So there is a need for reform, which can include tightening PRRT carry‑forward and deductible expense rules, making PRRT more progressive, while keeping an eye on broader tax reform and investment incentives.

Introduction

Australia is a major beneficiary of the natural resources trade, with mining exports alone contributing about 13% of the economy. The rise of China, alongside global population growth, urbanisation and industrialisation, has further increased our reliance on resource sales, particularly iron ore, coal, LNG, battery metals, and gold.

As the Federal budget returns to deficit in the foreseeable future and spending pressures rise from higher defence expenditure, reshoring of manufacturing, and an ageing population, there is a question for the government on how to optimise their revenue sources. An easy headline is “tax mining and gas more”, but the government seems to have ruled this out for the upcoming budget given current global shortage issues (though there is still potential for the tax to be reviewed in the future).

So, does the current system have merit? In other words, are mining companies already delivering an appropriate return to the community through taxes, or is the structure of resource taxation too generous?

The mining sector pays the most income taxes out of all industries

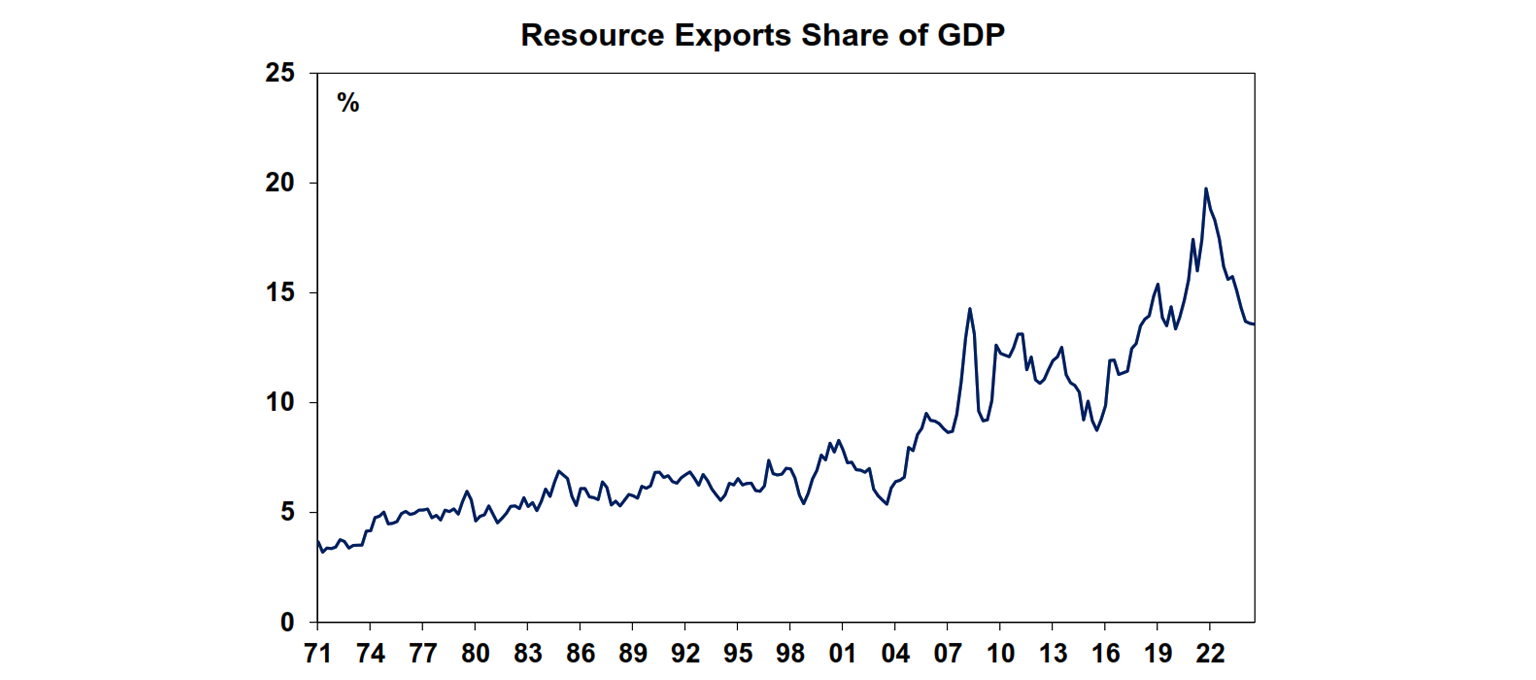

Mining accounts for more than 70% of Australian goods export revenues, and about 13% of Australia’s GDP, up from around 30% and 3% in the 1970s, respectively. A higher share of profits in mining doesn’t necessarily mean other sectors haven’t grown; it mostly reflects the supply/demand backdrop. For example, in the 1950s Australia’s biggest export was wool, not iron ore. Since then, stronger global demand for raw materials has lifted both volumes and prices, pushing up mining revenues and its share of GDP.

Mining and petroleum companies in most countries typically pay both taxes on production and income. Similar to other industries, Australian miners pay the standard corporate income tax of 30% of net profits (or 25% for small businesses with revenues under $50m), as well as capital gains tax at the same rate.

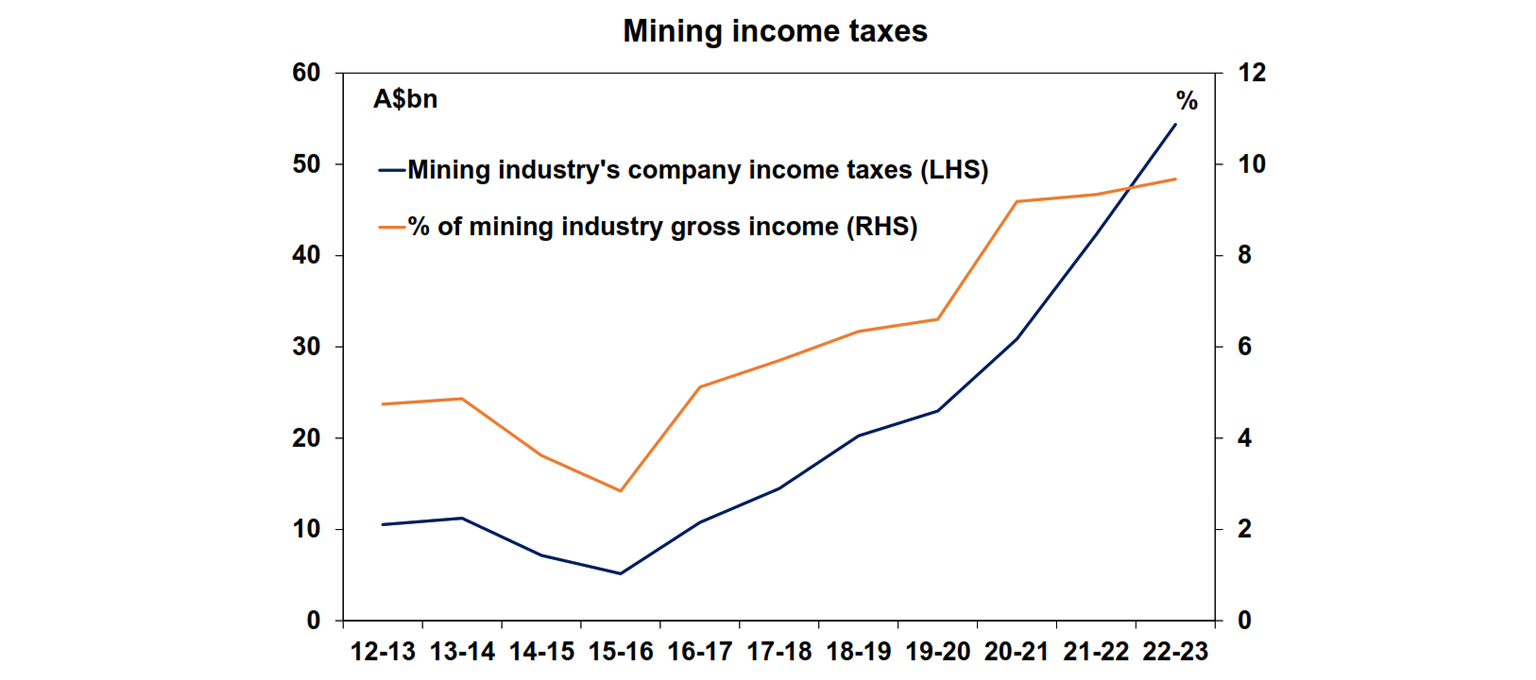

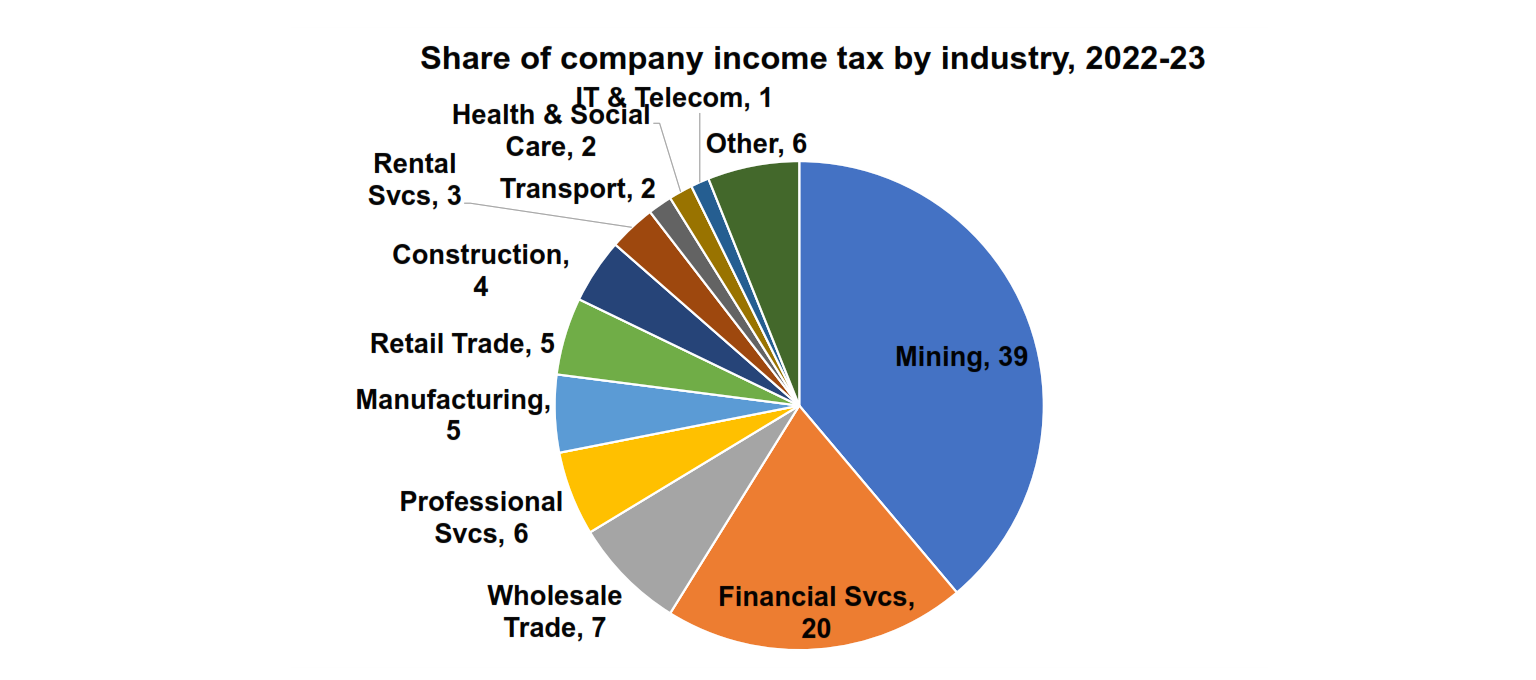

Income taxes paid by the mining sector have made up a large share of company tax in Australia. As the resources trade boomed, mining income taxes rose over time, in both nominal terms and as a share of production value. In 2022-23, mining company taxes totalled $54bn or 39% of federal company tax, the highest of any industry. Net mining company tax also came out at 27% of mining’s taxable income, above other industries at 22%. So, the booming minerals trade has significantly contributed to the federal budget over the years (and was a key contributor to the 2022–2024 surplus period). In other words, mining companies are not obviously underpaying company income tax to the federal government.

However, there is a need to pay additional prices on public resources

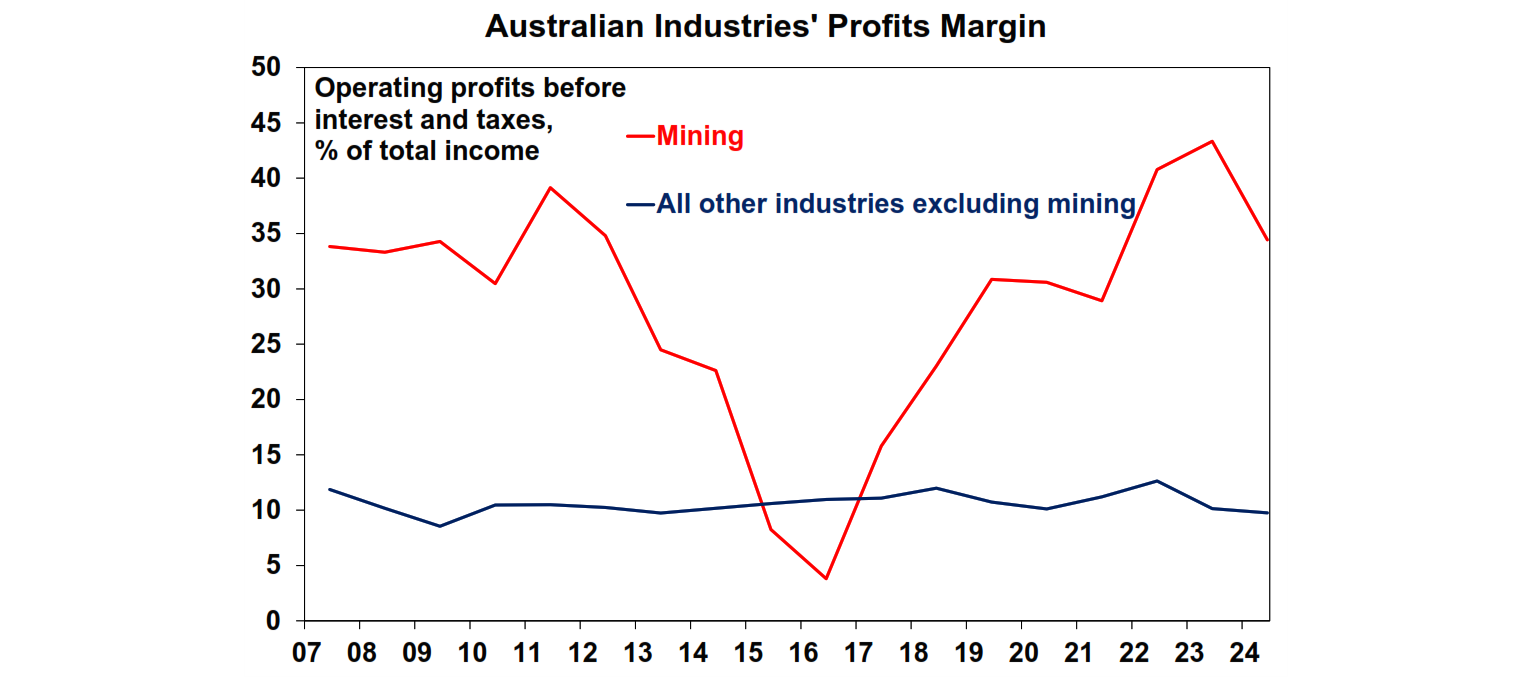

That being said, there is still a question of whether regular company income tax is sufficient, for three reasons. First, mining resources are owned by the Australian public, unlike industries such as agriculture, manufacturing, or construction, which sell products they create. Second, minerals are non‑renewable. While today’s generations receive income tax from mining, future generations inherit less resource wealth (or face higher extraction costs with lower reserves), so there should be additional taxes to address the intergenerational equity. Third, profits from extracting resources, even after accounting for depreciation of heavy plants and equipment, can be more lucrative than in other industries (see chart below). Mining profit margins have averaged ~28% since 2007 versus ~11% elsewhere (with the main exception in 2016, driven by high depreciation and amortisation rather than weak profits).

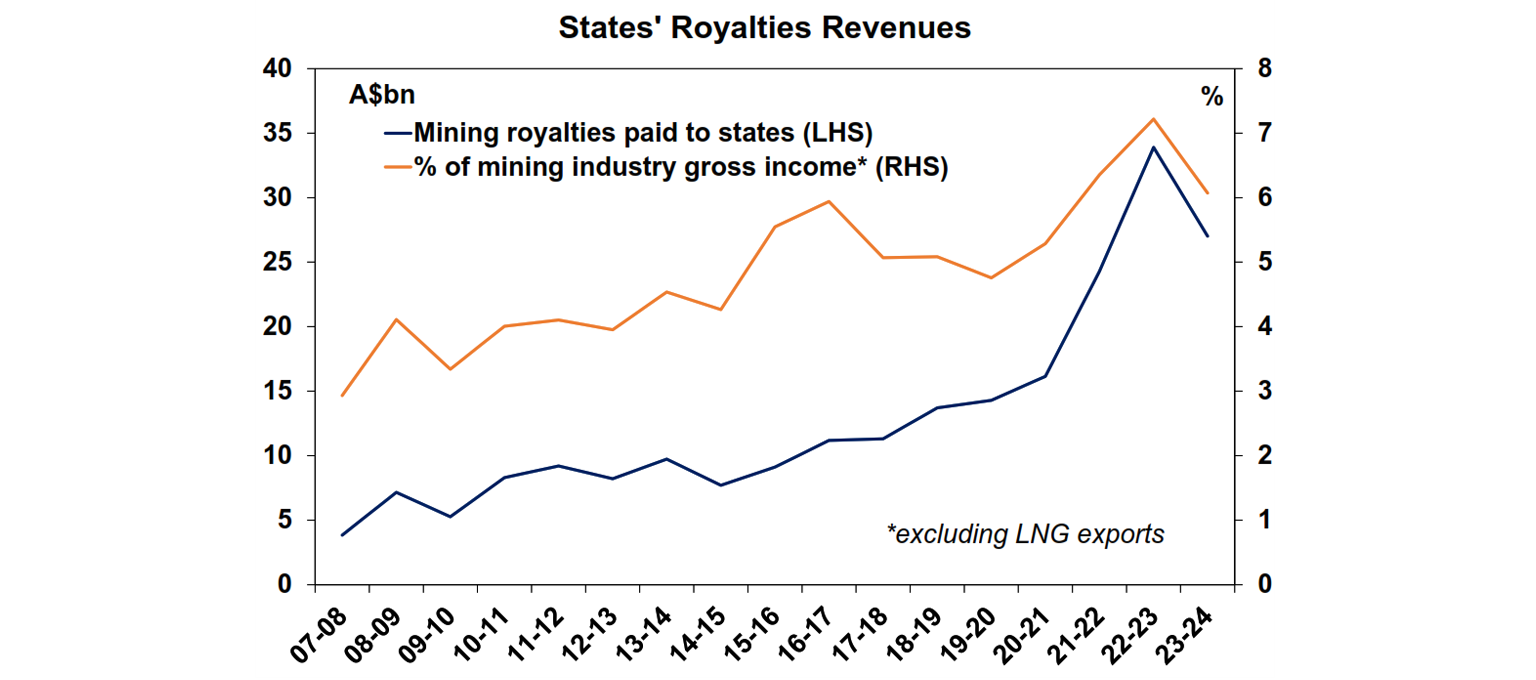

All of this points to a role for taxes on mining outside normal company income tax, which in Australia are largely implemented through production taxes (royalties). Royalties are paid to the state government where the resource is found and are typically calculated as a percentage of the value of extracted minerals.

In other words, state royalty revenues move with both production volumes and global commodity prices, regardless of whether a company is profitable at the time. This is still fair, because royalties are effectively the price a private company pays to “buy” a public resource, ensuring the community receives a return even when accounting profits are low or zero.

State royalty revenues have risen as production and commodity prices increased, but rates vary by commodity and state. For example, crushed iron ore royalties are 7.5% in WA versus 4% in NSW. Coal in QLD is charged at a progressive rate ranging from 7% to 40%, while in NSW coal rates vary by mine, around 8.8% to 10.8% of production value. Internationally, both coal and iron ore royalties in Australia sit around the middle of the pack (for example: coal royalty rates are typically ~2–10% in China, ~14% in India, and ~8–12.5% in the US; while iron ore is ~3.5% in Brazil versus ~15% in India).

One way to assess the royalty level is the effective royalty rate across all states and commodities, calculated as total royalty revenue divided by national mining production income. On this basis, the effective rate averages around 6.4%. But as shown above, mining companies have earned an average pre tax margin of ~28% versus ~11% for the rest of the economy, or a margin differential of roughly 16 percentage points, well above 6.4%. This suggests there’s a case to lift the effective royalty rate, as the sector has the capacity to absorb a higher royalty burden, while still earning returns well in excess of normal profits.

Royalties missing in offshore projects

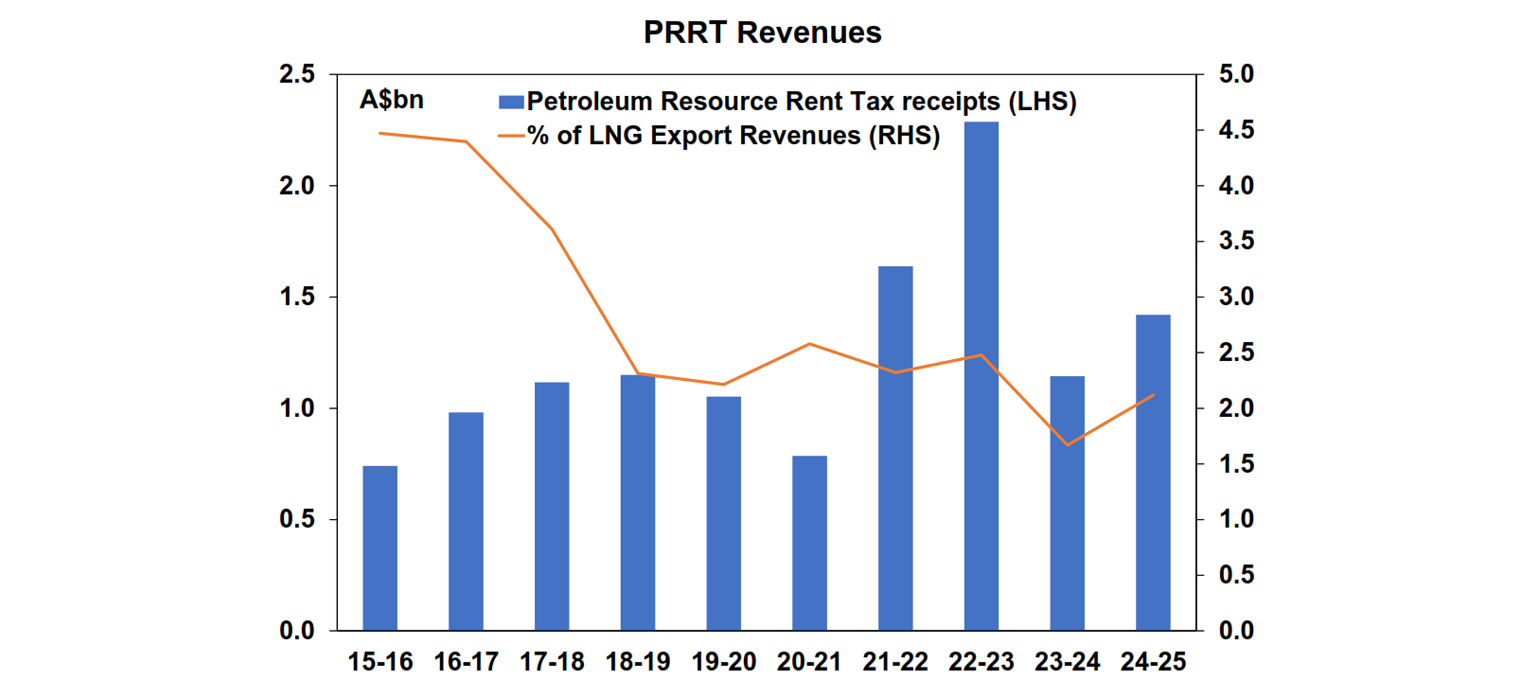

Royalties, however, don’t apply to offshore oil and gas projects, which account for about 73% of annual gas production in Australia. Because these projects are located in Commonwealth waters, they don’t pay production-based royalties to state governments. Instead, gas projects pay a special profit-based tax called the Petroleum Resource Rent Tax (PRRT), levied at 40% on profits after deducting exploration and development costs. But high construction costs and generous deductions (including full expensing of plants and equipment rather than depreciation over the years) have meant PRRT collections have stayed very low at around 2% of revenues, well below the ~6.4% effective royalty rate in onshore mining.

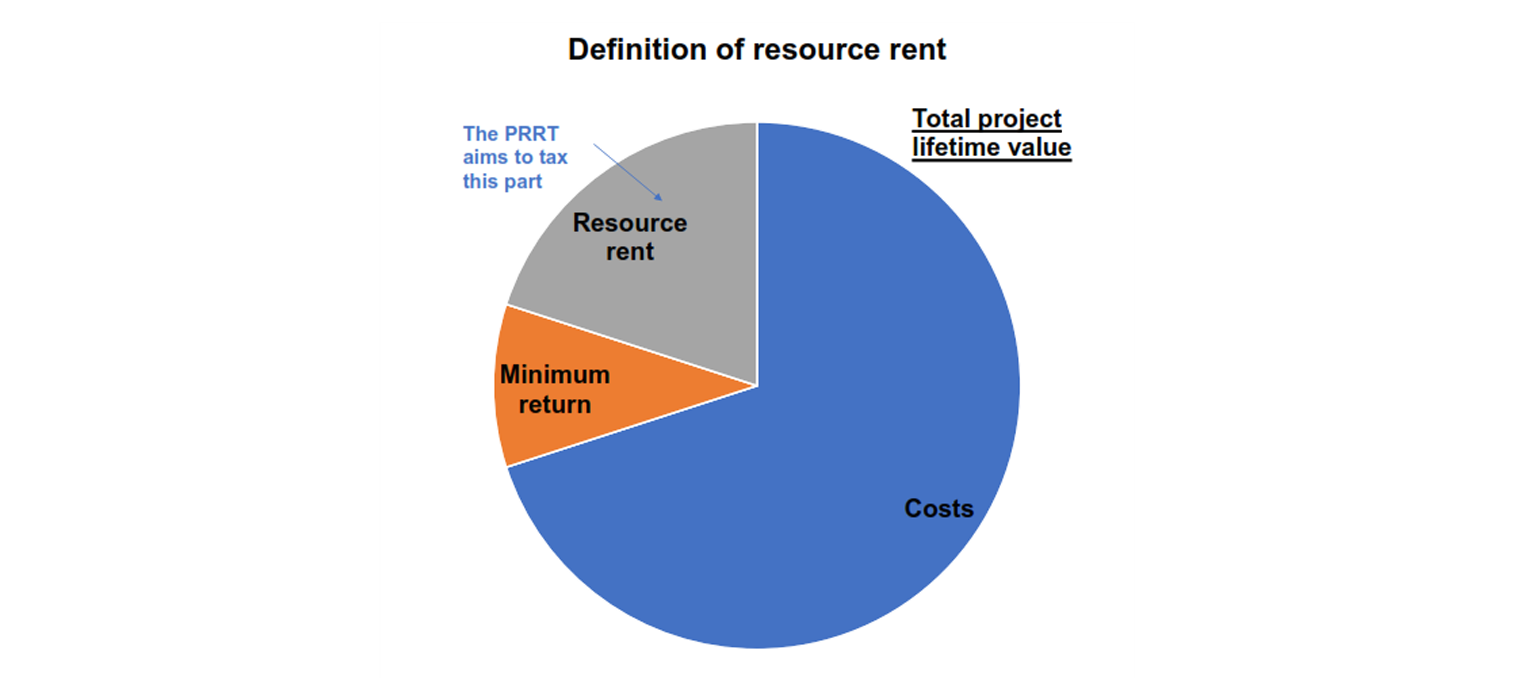

So, the question becomes: is the PRRT fair, and why does it exist instead of royalties? Economically, the goal of either royalties or PRRT (i.e., taxes outside standard income tax) is to capture abnormal returns above the usual rate. In theory, this is “economic rent”, defined as the excess project value added, after subtracting both costs and the minimum return on capital required by investors. This lets government share in windfall profits while still leaving investors a minimum return, in order to entice them to take on large projects with big upfront investments. In addition, only taxing the rent does not lower the pre-tax return for investors and avoids distortion in the investment decisions.

But working out the threshold at which a rent tax becomes payable (i.e., the minimum required return) is hard to pin down. In Australia, while the headline PRRT rate is 40% of project profits, the scheme allows losses and deductions to be carried forward across years (and, in some cases, across projects). Unused deductions are “uplifted” each year by specified rates (e.g., the long-term bond rate), which acts as a threshold of required return before the government takes its share. The uplift of deductions hence lowers tax liabilities.

While that sounds reasonable in theory, offshore gas projects typically have large exploration costs and major plant & equipment investment, which can be deducted upfront, even before production and sales begin. This differs from normal company income tax, where capex is generally deducted over time via depreciation and amortisation.

Secondly, because expenses can exceed revenues in the early years, deductions can be banked to carry forward and then continue to grow through the uplift rates. It’s reasonable that gas projects don’t pay much tax early on given multi‑year development costs even before entering production. This is no different to the ability to carry forward losses for any companies or individuals in Australia when paying income taxes. However, in the near future, gas projects are more likely to benefit from geopolitical-driven windfalls; and most importantly, they can also benefit from rapidly inflating carried‑forward PRRT deductions, which helps explain why actual PRRT paid has remained low. This issue is more problematic for gas projects rather than oil projects, because gas projects are much more capital intensive at the beginning, allowing for more deductions that are uplifted for many years.

Finally, PRRT applies only to upstream gas activity (exploration and extraction), not downstream activities like liquefaction, processing, or export. For oil projects or domestic gas, this is not an issue because the gas does not need to be converted to LNG. But in Australia, around 73% of gas is exported as LNG. For these exports, PRRT uses a “midpoint price,” which effectively taxes only part of the economic rent (more detailed explanation by the ANU here). This means many export projects experience leakage of taxable economic rent.

Is the system fair?

Is the current tax system fair? In practice, “fair” taxation design involves trade-offs between core principles, which the Parliamentary Budget Office summarises as simplicity, efficiency, and equity.US economic data was a mixed bag. Consumer confidence fell sharply in January on the Conference Board’s measure.

Arguably, resource rent taxes are more efficient, because they are designed not to distort investment and production decisions (while still allowing a minimum return), unlike royalties.

But the current system is not simple. Companies can end up paying well below headline rates because of deductions, pricing methods, and the ability to carry forward (and uplift) losses across years and projects.

Equity means a fair share of profits (after compensating companies for risk) should flow back to Australian citizens and compensate the public for environmental and social costs. This principle is particularly lacking in the PRRT, where the revenue share of taxes has drifted down since FY20–21.

While there is scope to increase onshore royalties higher, the most problematic issues are certainly concentrated in the PRRT for offshore gas projects, given effective rates remain well below the industry’s additional margin. This could be achieved via tighter carry‑forward rules and a stricter list of deductible expenses. A more progressive PRRT rate (like QLD’s coal royalty rates that rise with prices) could also better address equity.

However, we also need to avoid simply hiking mining taxes in isolation, which amount to a broader tax hike on the economy at a time when we need stronger private business investment overall. A more comprehensive tax reform which includes shifting revenue sources more broadly (as outlined by my colleague Shane Oliver’s budget wishlist) is likely needed keep the budget sustainable.

My Bui,

Economist, AMP

You may also like

-

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset. -

Weekly market update - 17-07-2026 Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.