Weekly market update

Investment markets and key developments

Global share markets mostly rose over the last week with ongoing hopes for a deal to unblock the Strait of Hormuz and strong earnings data. This was despite worries about a more hawkish Fed and concerns about the inflationary consequences of the War.

9 min read

Global share markets mostly rose over the last week with ongoing hopes for a deal to unblock the Strait of Hormuz and US strong earnings data. This was despite worries about a more hawkish Fed and concerns about the inflationary consequences of the War. For the week US shares rose 0.9%, Eurozone shares rose 2.9% and Japanese shares rose 3.1%. Chinese shares were an exception though and they fell 0.3%. Helped along by the positive global lead the Australian share market also rose but only by 0.3%, with ongoing concerns about the impact of the Budgetary tax hikes on investing weighing. Strong gains in consumer and financial shares on the ASX were partly offset by sharp falls in utilities and industrials.

Metal prices rose slightly over the last week but gold and Bitcoin fell with $A and $US little changed.

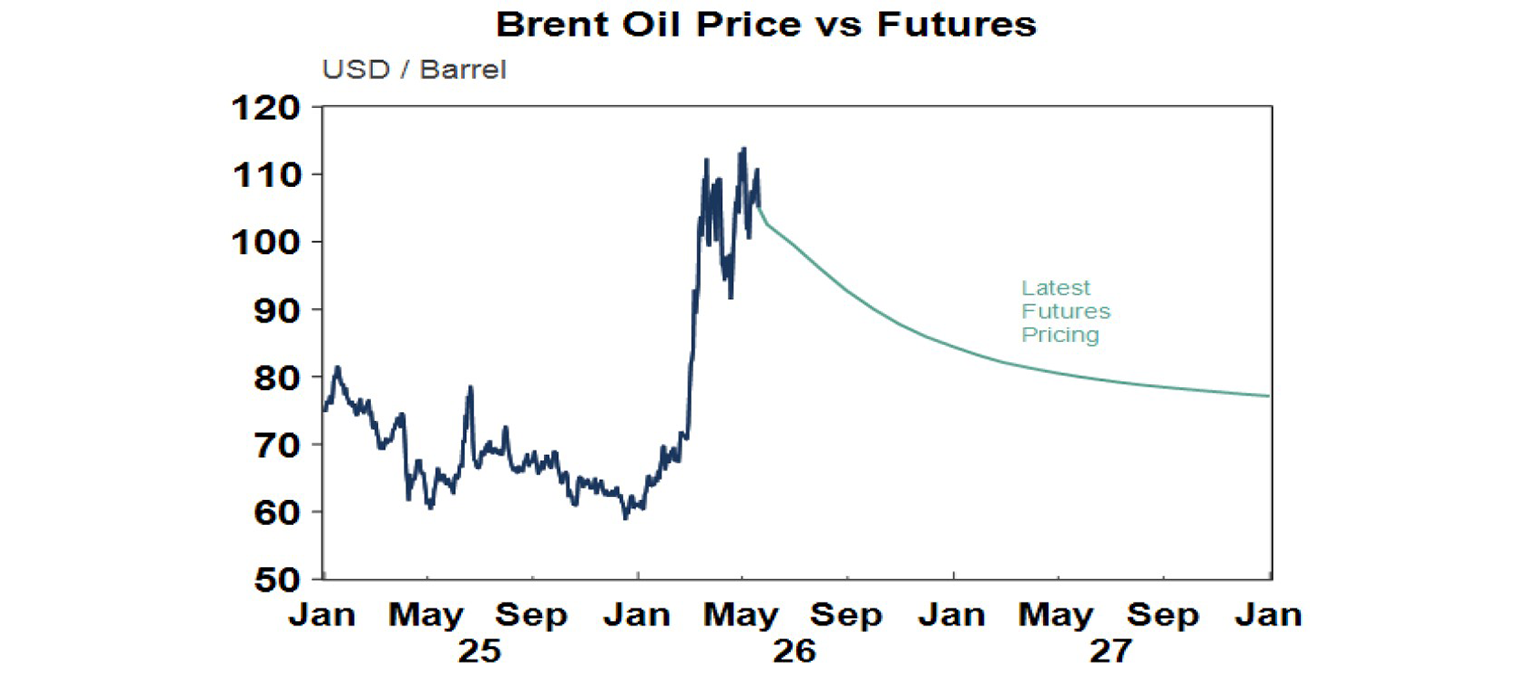

The past week saw more of the same in relation to the Iran War – more threats from Trump followed by soothing words about “very big discussions” with Iran. While a few ships got through, the Strait remains effectively closed maintaining a roughly 12 or 13% hit to global oil supplies. The upshot is that Trump wants to TACO but Iran is still not willing to provide the salsa with uranium and transit tolls through the Strait remaining sticking points. So, the standoff continues, posing bigger risks to the global and Australian economies the longer it goes on. This is leaving oil prices range bound, but with oil futures pricing in a fall on the grounds that a deal will be reached eventually. This remains our base case and Trump has been showing some signs of shifting focus to Greenland and Cuba lately!

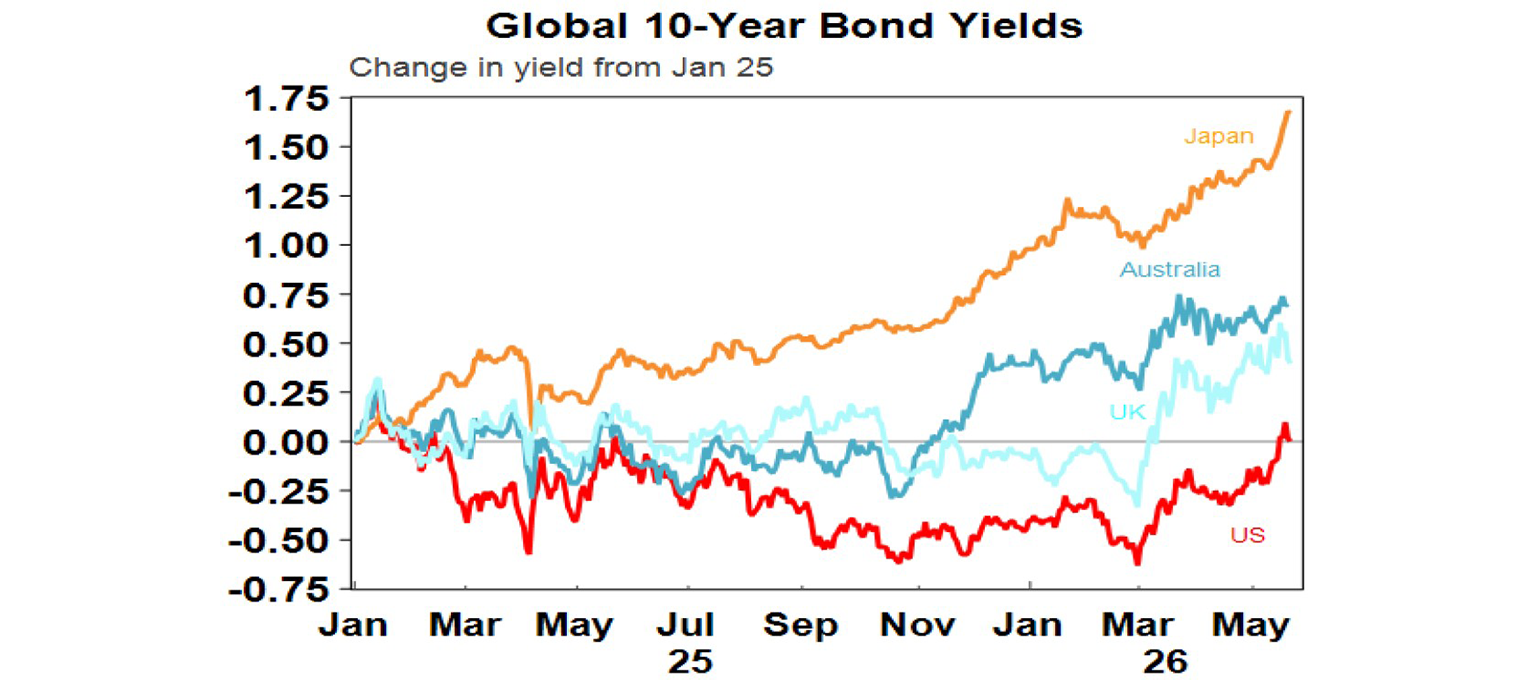

Meanwhile, the ongoing impacts of the Strait blockage have added to concern that inflation and inflation expectations will rise further. Inflation data for the UK, Canada and Japan was better than expected, but the minutes from the Fed leaned hawkish with “many” Fed officials preferring to remove language indicating an easing bias and a “majority” indicating that a rate hike would be appropriate if inflation remained above target. This was reinforced by Fed Governor Waller, who is a Trump appointee, noting that “inflation is not heading in the right direction” and that he would “support removing the easing bias.” The US money market has now removed expectations for a rate cut this year and now sees a 95% probability of a hike. Meanwhile, some emerging country central banks are coming under pressure to raise rates with the Bank of Indonesia hiking by 0.5% in the last week. This is all combining to maintain upwards pressure on bond yields.

The RBA has “space” to be in wait and see mode but remains hawkish. The minutes from the last meeting noted that financial conditions are probably now a bit restrictive and that the three hikes this year give the RBA space to see how the War develops and impacts the economy. Soft jobs data for April – the last to be released before the RBA meeting next month – adds to the likelihood that the RBA will leave rates on hold in June. But the overall message from the RBA remains somewhat hawkish. This was highlighted in comments by RBA Assistant Governor Hunter who noted that a combination of factors meant that the boost to inflation from the oil supply shock could be “faster and more extensive” because of the starting point for the Australian economy of capacity constraints and already high inflation and with RBA research finding that price changes become more frequent when inflation is high which can lead to underestimating future inflation. The RBA is right to be concerned about a flow on to inflation expectations because five of the six years up until this year will have seen inflation above the 2-3% target, which risks increasing scepticism that the target will be met going forward which in turns risks a step up in wage demands and price rises. With the release of UK and Canadian inflation data in the past week it is clear that Australia sticks out like a sore thumb, both in headline inflation and in underlying inflation despite the latter yet to really show much impact from the War. As a result, the RBA has had to hike rates this year when other central banks have held and has to continue to remain relatively hawkish. Unfortunately, the Budget did not make the RBA’s job any easier. While we expect the RBA to leave rates on hold at its June meeting as it waits to assess things, we continue to expect another hike in August. The money market sees just a 2% chance of a hike next month, but continues to expect a hike by year end.

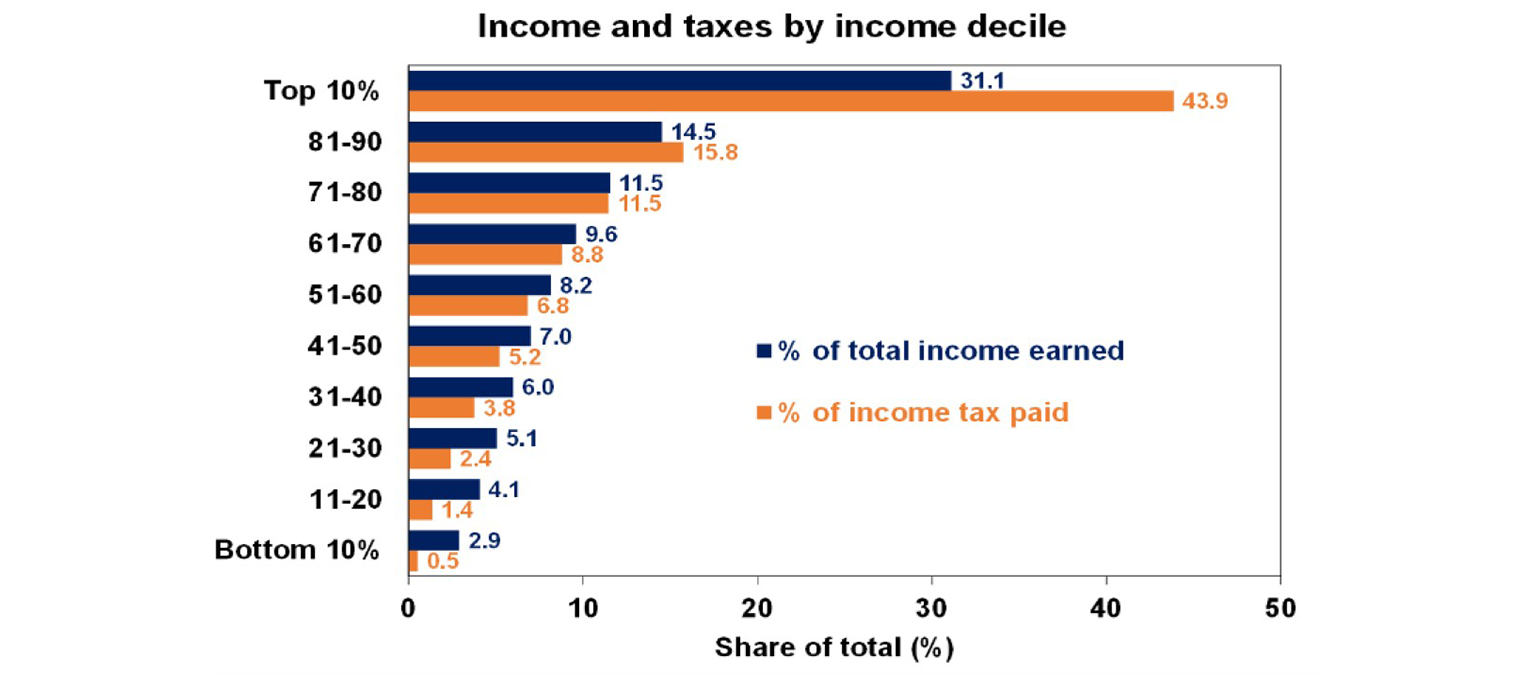

The changes to negative gearing, the capital gains tax discount and the taxation of family trusts have received a lot attention, but a disappointing aspect of the Budget was that the changes were not assessed in the context of the overall income tax system. Even with access to these concessions the Australian income tax system was highly progressive with the top 10% of income earners paying 44% of income tax revenue being raised by Canberra and the top 20% accounting for 60%. The tax system should be progressive because the more you earn the more you should be able to contribute as a share of your income. But there is a danger in pushing it too far in that it risks creating a disincentive to work, form new businesses and expand to employ more people. And now with the concessions wound back it will become even more progressive adding to these disincentives risking weaker productivity growth and living standards. This risk is particularly high for start ups and small businesses and even if they are excluded from the CGT change the risk could remain in relation to less capital being available for growth stocks on the share market.

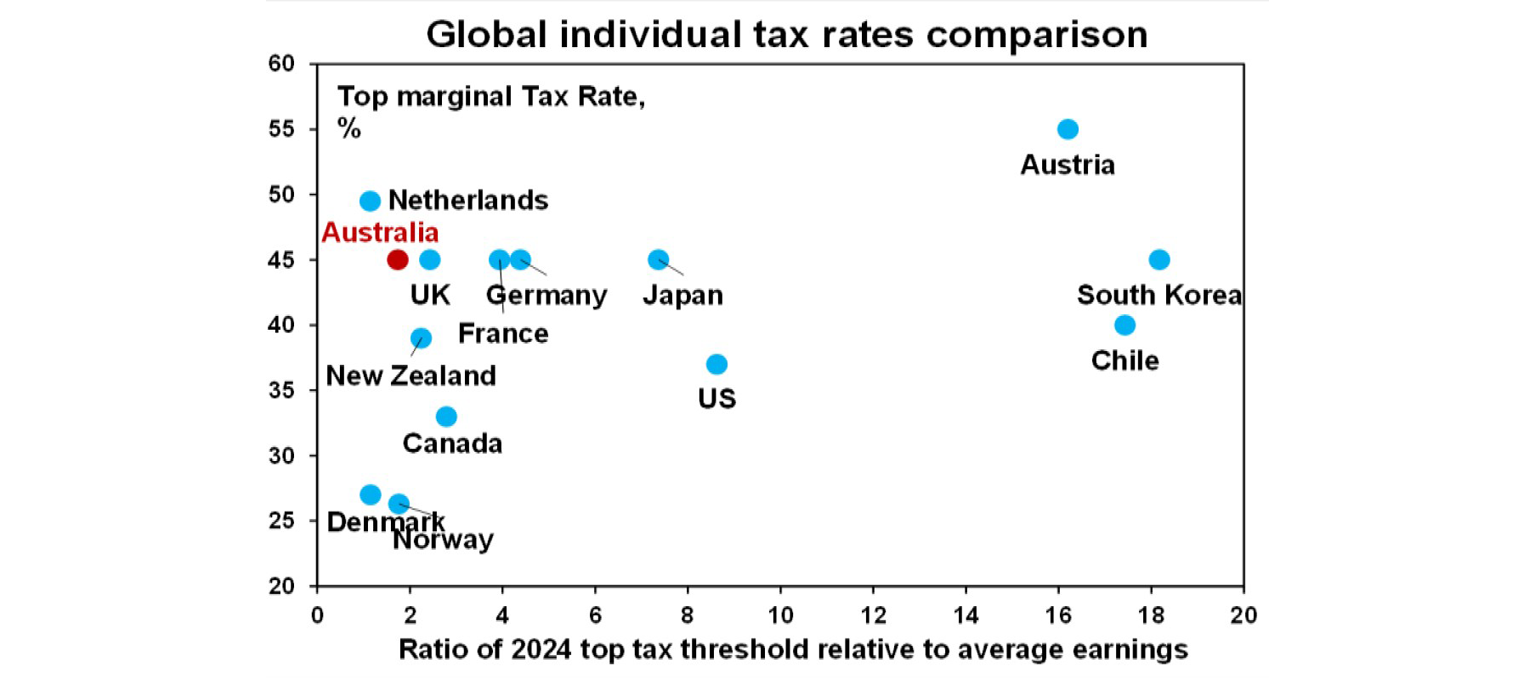

In short, the curtailment of the tax concessions should have been accompanied by income tax cuts or at the very least a commitment to indexing the tax scales to inflation. This is particularly the case with the top tax rate being above that in many other comparable countries and kicking in at a relatively low multiple of average wages. See the next chart. If the top tax threshold had been indexed to inflation since it was last significantly raised in 2008-09 it would now be $280,000 and not $190,000, which means far more taxpayers today are now paying the top rate than was originally intended for them.

It’s a bit sad that Australia missed out on winning Eurovision (again) as Delta had such a good song – better than Bangaranga. Here is La La La, the winner from 1968 which came from Spain – apparently the original singer of the song was Catalan and was switched out for Massiel at the last minute because he insisted on singing in Catalan which might not have gone down well with President Franco. This is covered in The Song Contest on SBS. It’s also amazing to see that Eurovision had a full orchestra back then. This was mandatory until 1998 – but it then went electronic and pre-produced.

Major global economic events and implications

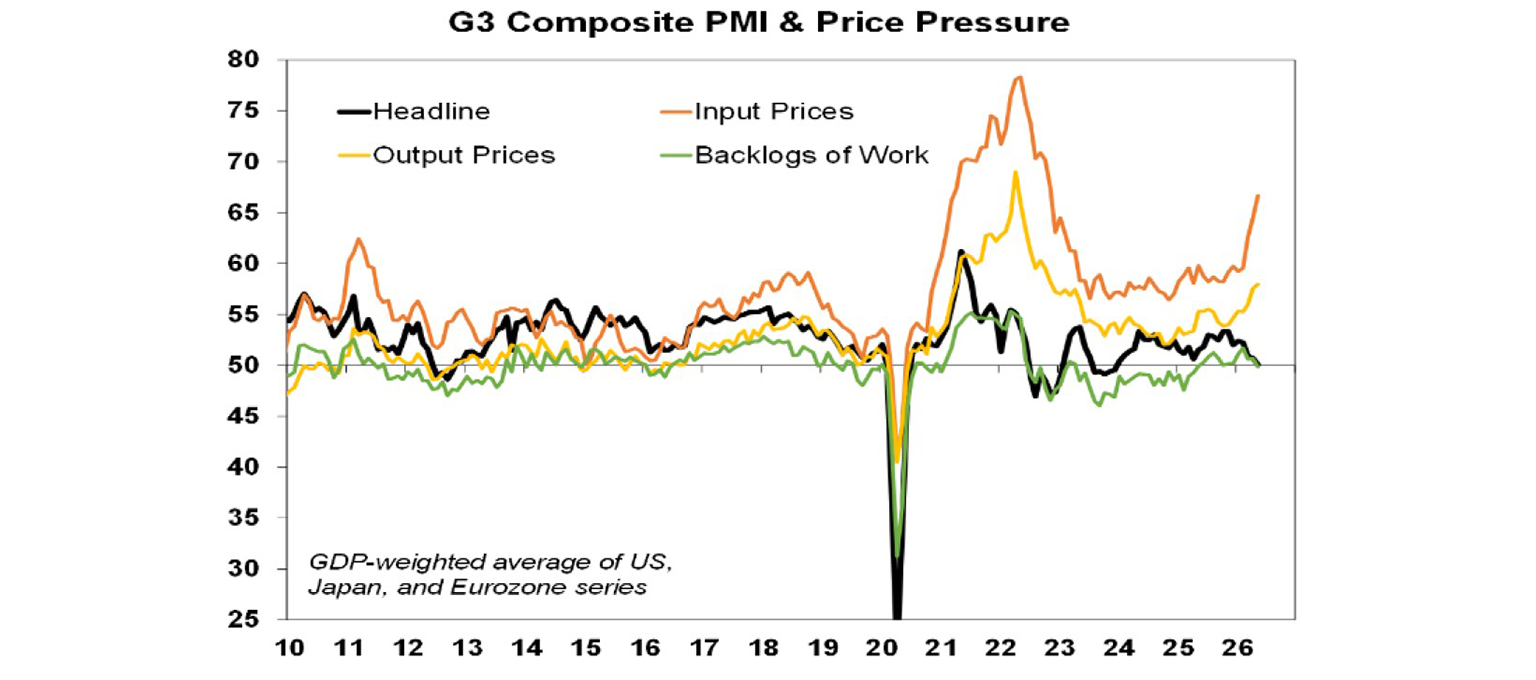

Developed country PMIs for May showed a further whiff of stagflation with slightly weaker business conditions and higher price pressures. The weakness in activity was concentrated in Europe and Japan, but with manufacturing holding up and services down.

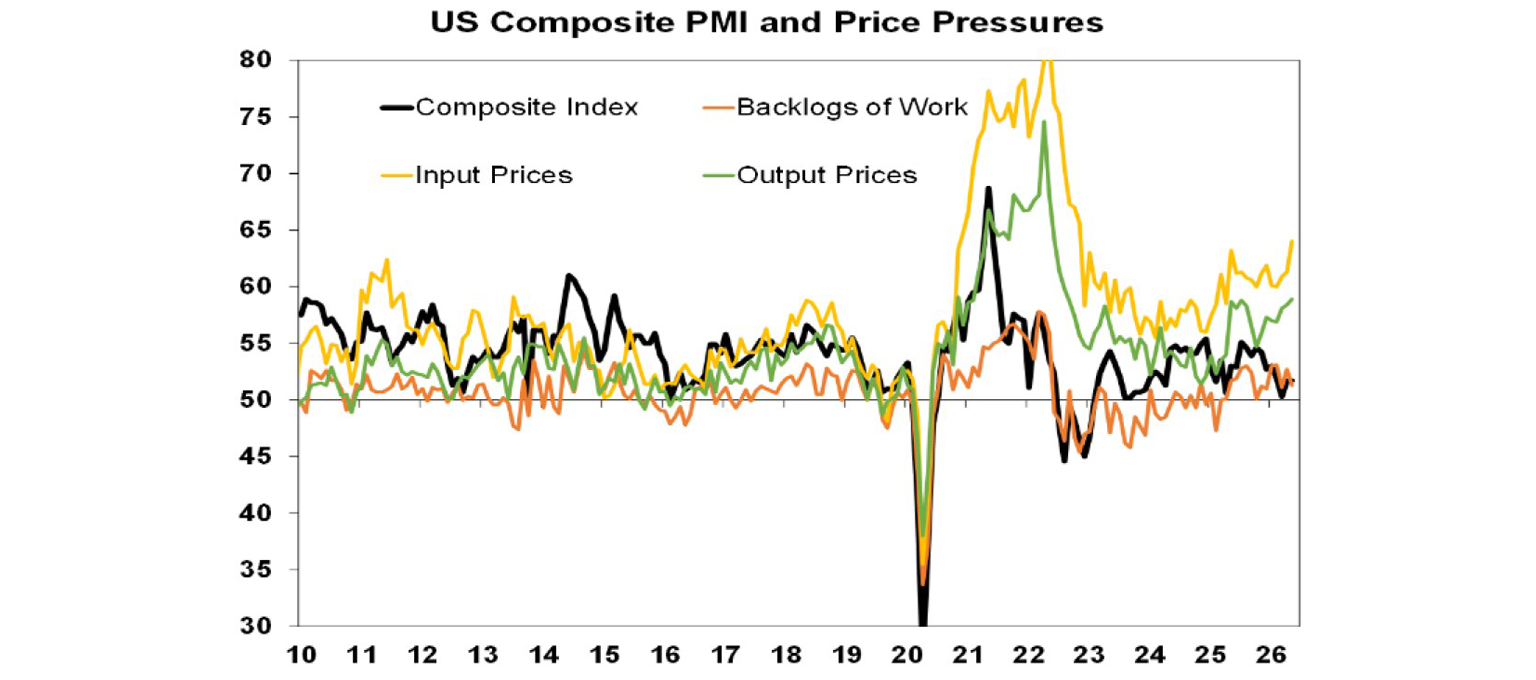

The US composite PMI is continuing to hold up a bit better – helped by the US’ status as a net oil exporter - but high & still rising price indicators are a problem for the Fed.

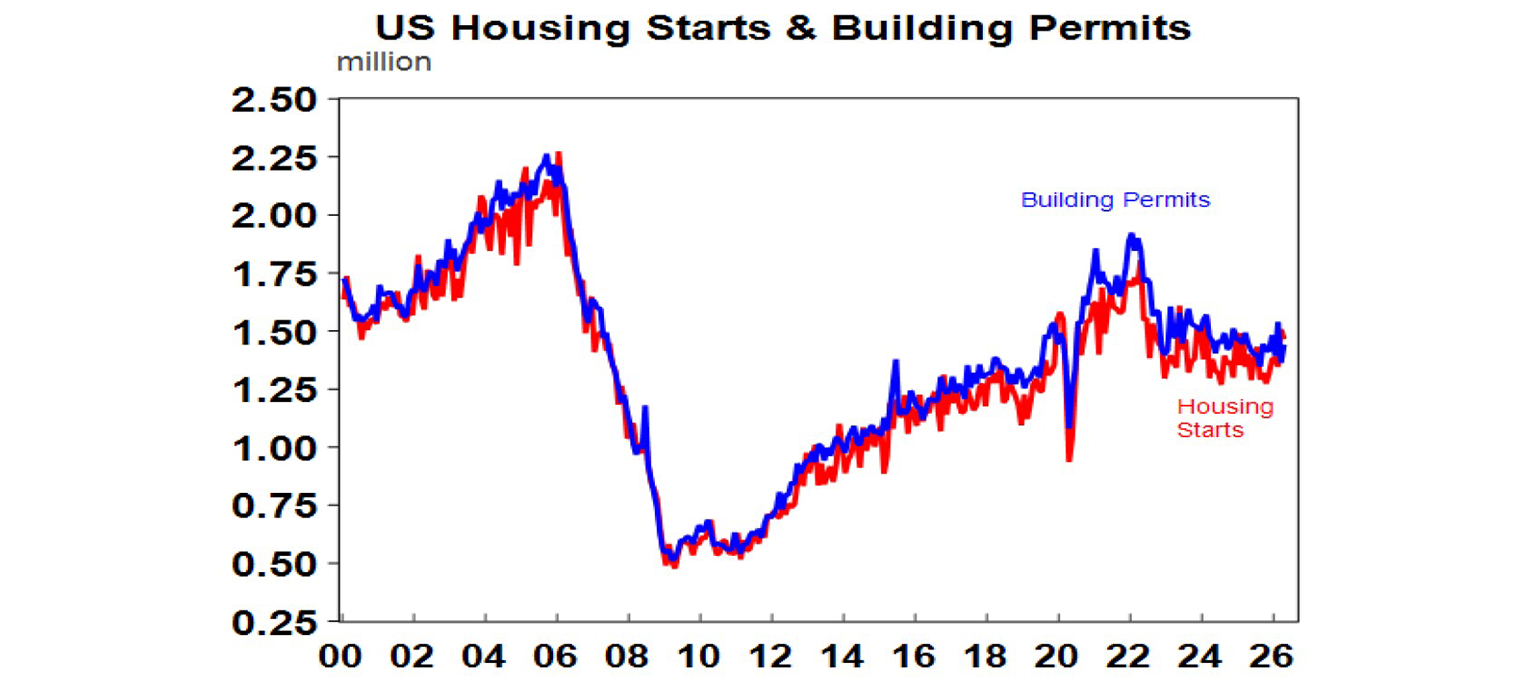

Other US economic data was mixed. In contrast to the PMI, manufacturing conditions in the Philadelphia region fell in May and consumer sentiment fell to a new low. While home builder conditions rose in May and housing starts rose in April, permits fell and all remain soft not helped by the ongoing rise in mortgage rates. Meanwhile, jobless claims remain low. The University of Michigan consumer survey showed 5-10 year ahead inflation expectations rising to 3.9% and they seem to be ranging well above levels seen before President Trump’s return – which is a concern for the Fed.

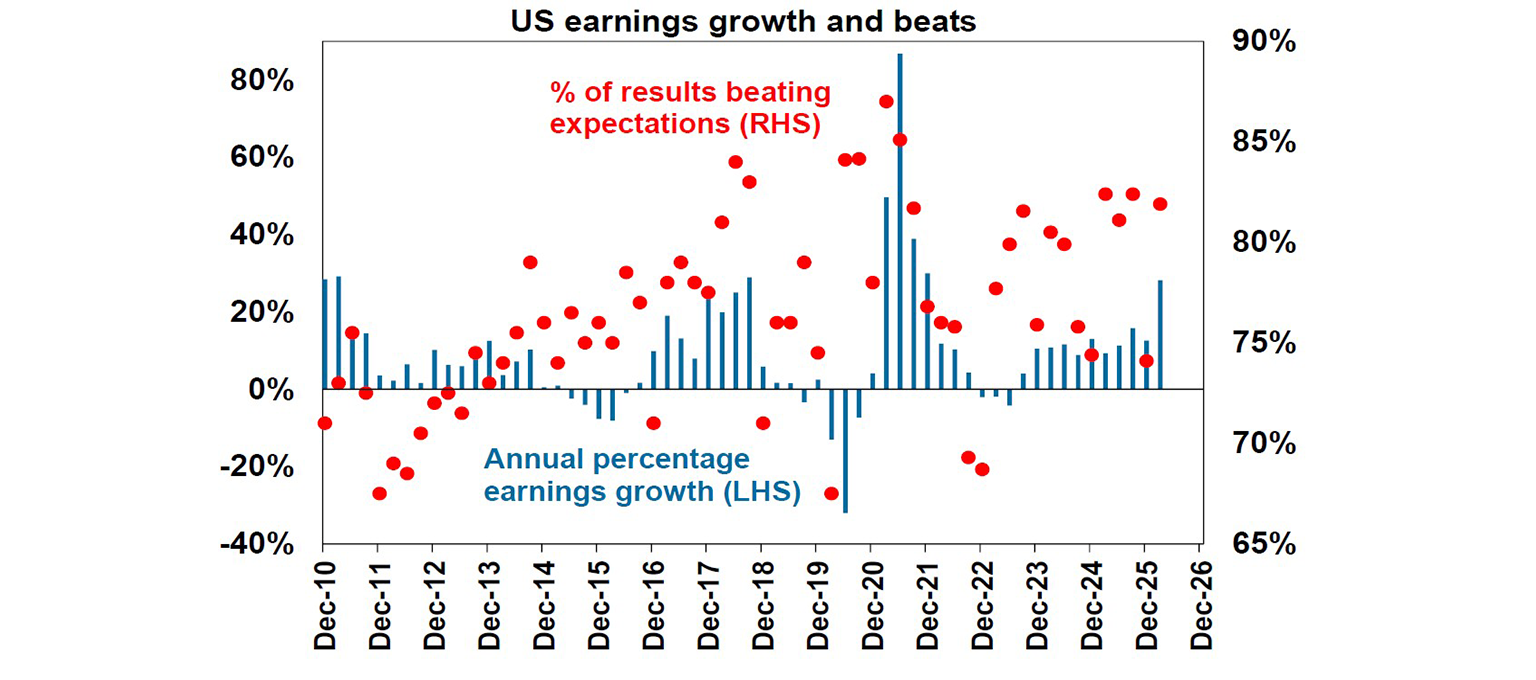

With Nvidia having reported, the US March quarter earnings reporting season is now largely over and profits have boomed. 95% of S&P 500 companies have now reported with 82.1% beating expectations and earnings growth for the quarter has now moved up to 29%yoy, up consensus estimates for a 14%yoy rise at the start of the reporting season. This is the strongest pace since 2021. Tech has led the charge with earnings growth around 61%yoy. Nvidia reported sales growth of 85%yoy and earnings growth of 129%yoy, both of which beat expectations but the market was hoping for more with its shares down 1.8% after reporting.

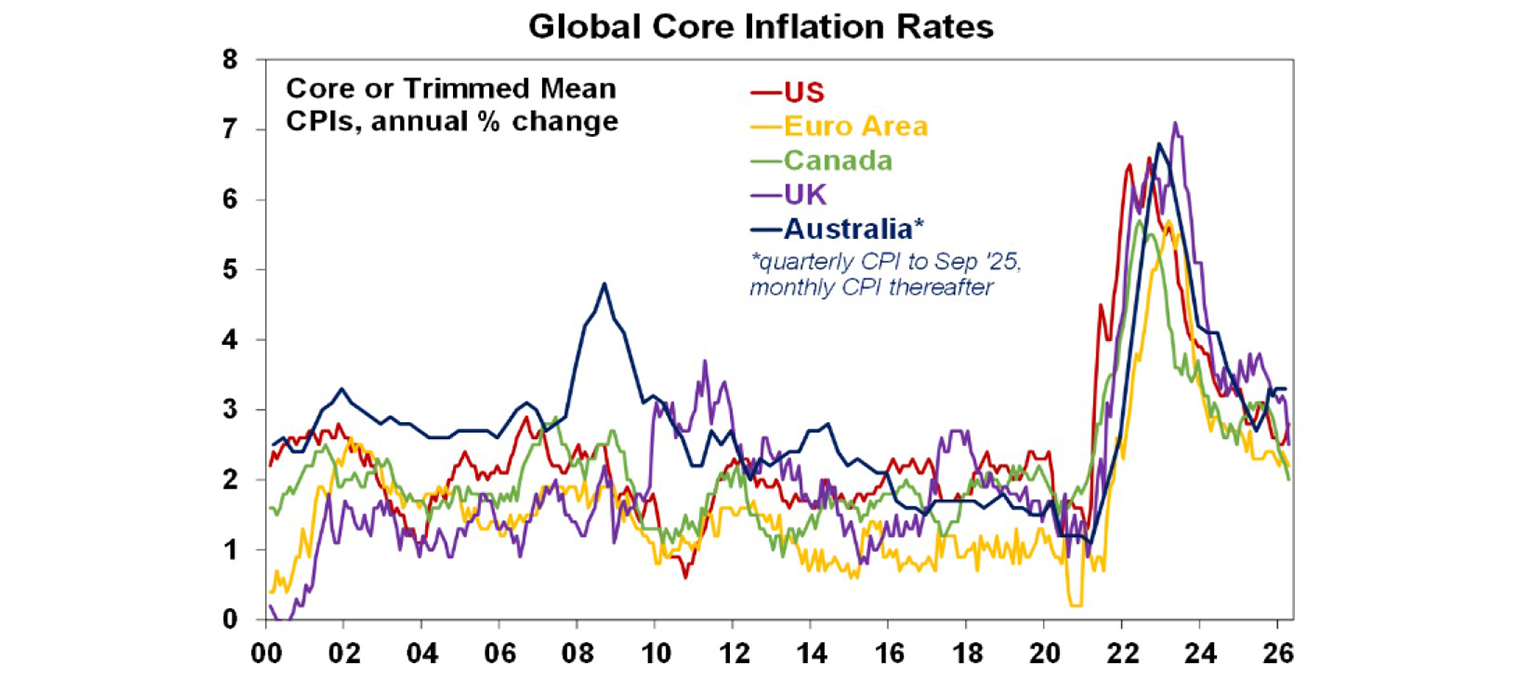

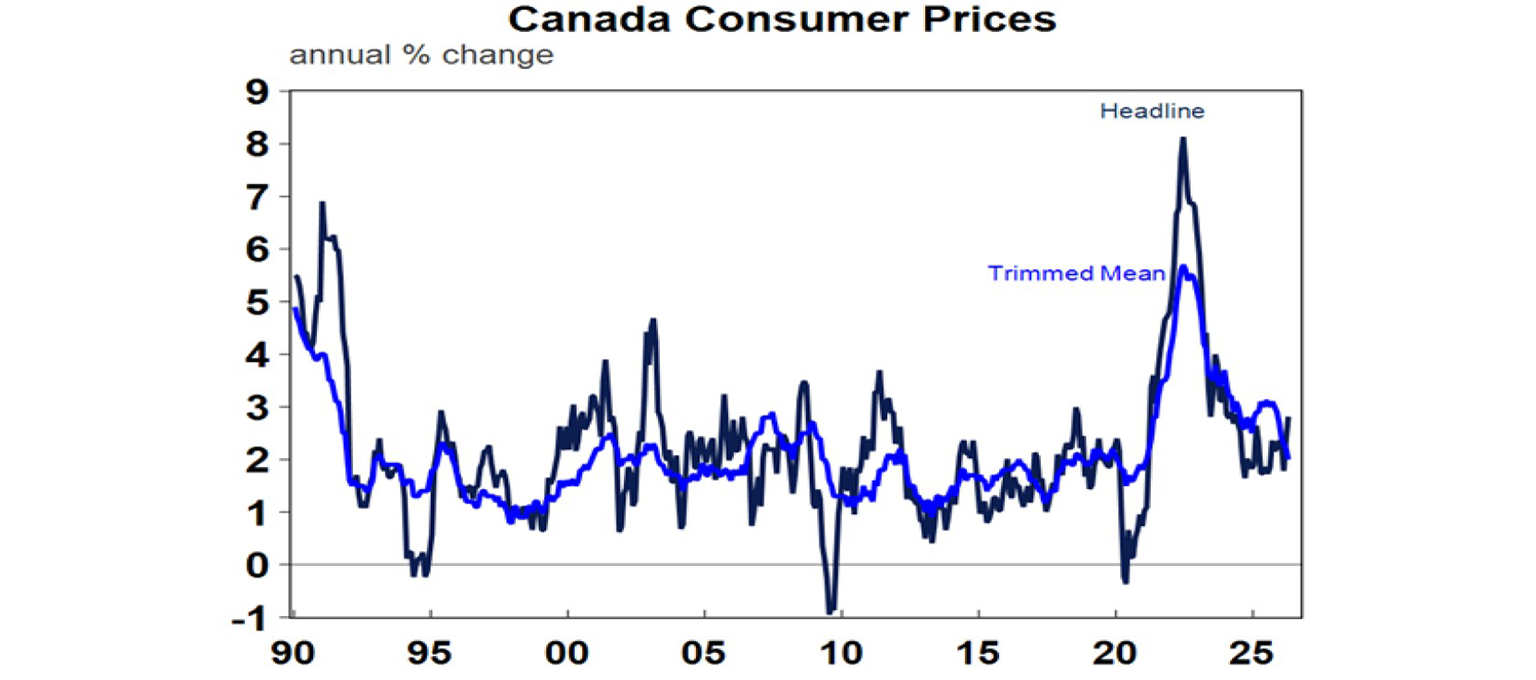

Canadian inflation rose less than expected to 2.8%yoy in April with the underlying measures around 2%yoy. This likely leaves the BoC in no hurry to raise interest rates from 2.25%. This contrasts dramatically with the situation facing Australia which has much higher inflation but note that Canada’s unemployment rate is 6.9%, well above Australia.

Similarly UK inflation in April was also less than expected falling to 2.8%yoy at the headline level with core inflation falling to 2.5%. As with the BoC this likely leaves the BoE in no hurry to hike, particularly with unemployment at 5%.

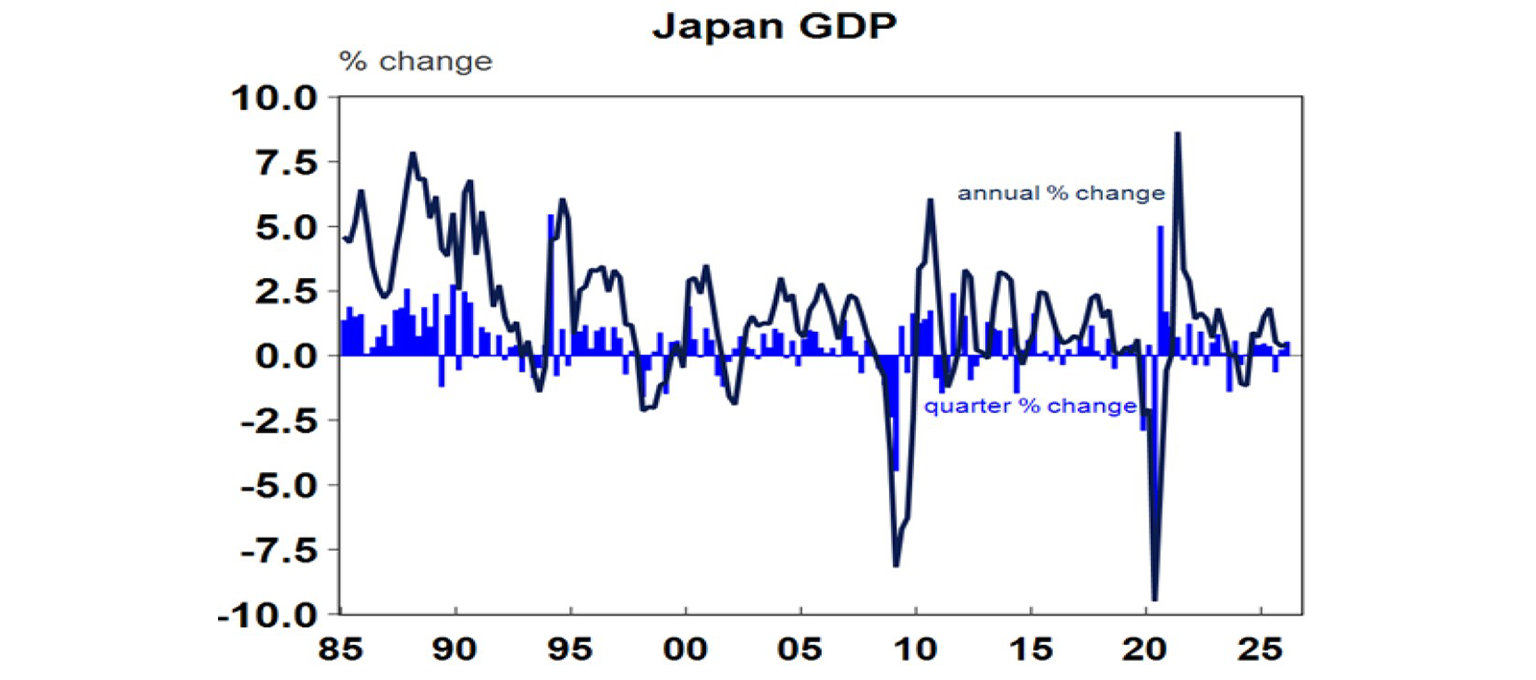

Japanese March quarter GDP was stronger than expected at 0.5%qoq with modest increases in consumption and business investment and a strong contribution from trade. Japanese inflation slowed to 1.4%yoy in April with broad based softness and core inflation slowing to 1.1%yoy which should keep the BoJ gradual in hiking.

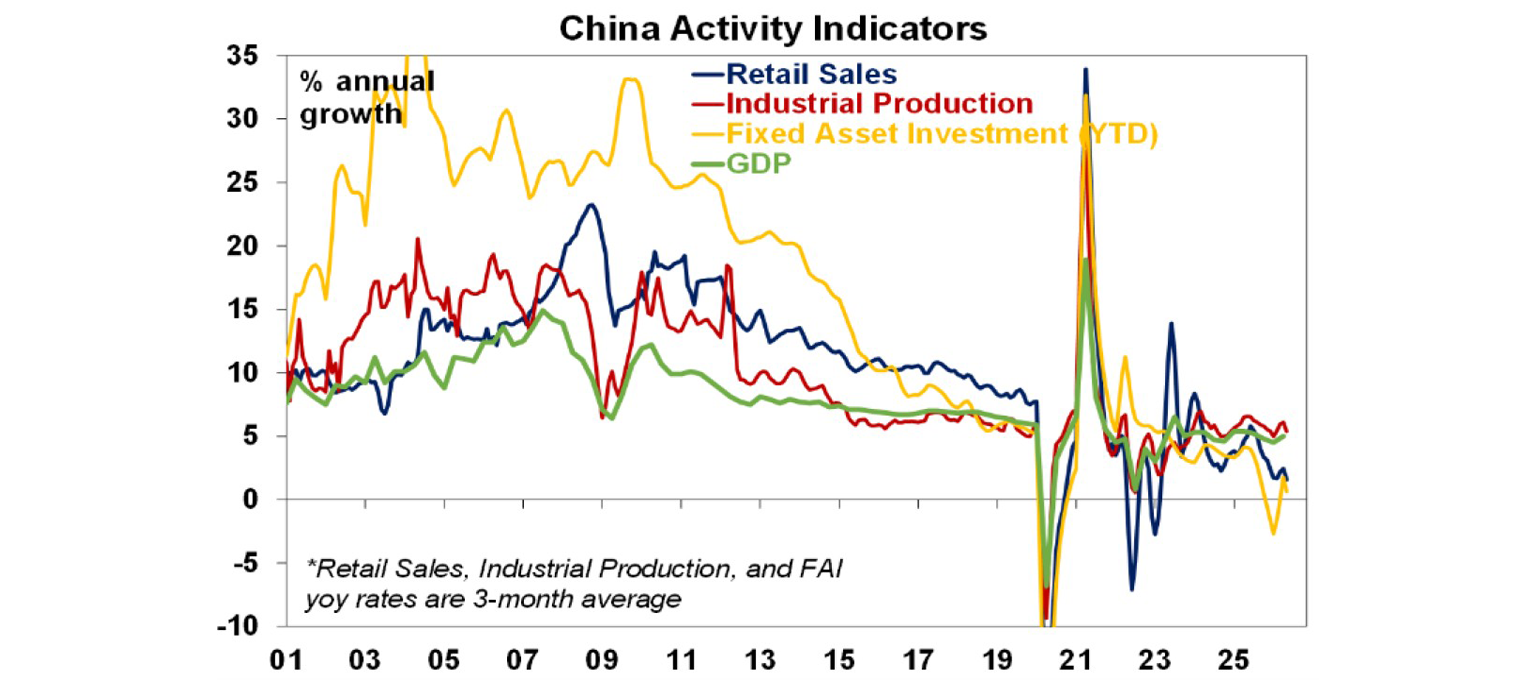

China’s economic activity softened across the board in April. Retail sales growth slowed to just 0.2%yoy with a sharp fall in gold and jewellery sales, and the end of subsidies impacting the sale of household appliances. Property investment and sales continue to fall but at least the pace of decline in home prices slowed. The slowdown appears to reflect a payback after a strong March quarter and some policy tightening but the Government is likely to keep growth muddling along around 4.5%yoy.

Australian economic events and implications

Jobs data for April was soft but may have been distorted. Employment fell by 18,600, with unemployment rising to 4.5% its highest since 2021 and participation fell. However, it wasn’t all weak with hours worked up strongly and it may have been distorted by Easter and school holidays and a new data collection method by the ABS. What’s more female employment fell by 32,000 with the fall concentrated in Queensland where unemployment spiked from 3.7% to 4.2% which looks dodgy and subject to reversal next month. The softness in April may be a sign of a softening jobs market on the back of rate hikes and the oil shock, and we expect a further rise in unemployment but the weakness in April could just be statistical noise and so we will need to see May’s data to get a clearer picture..

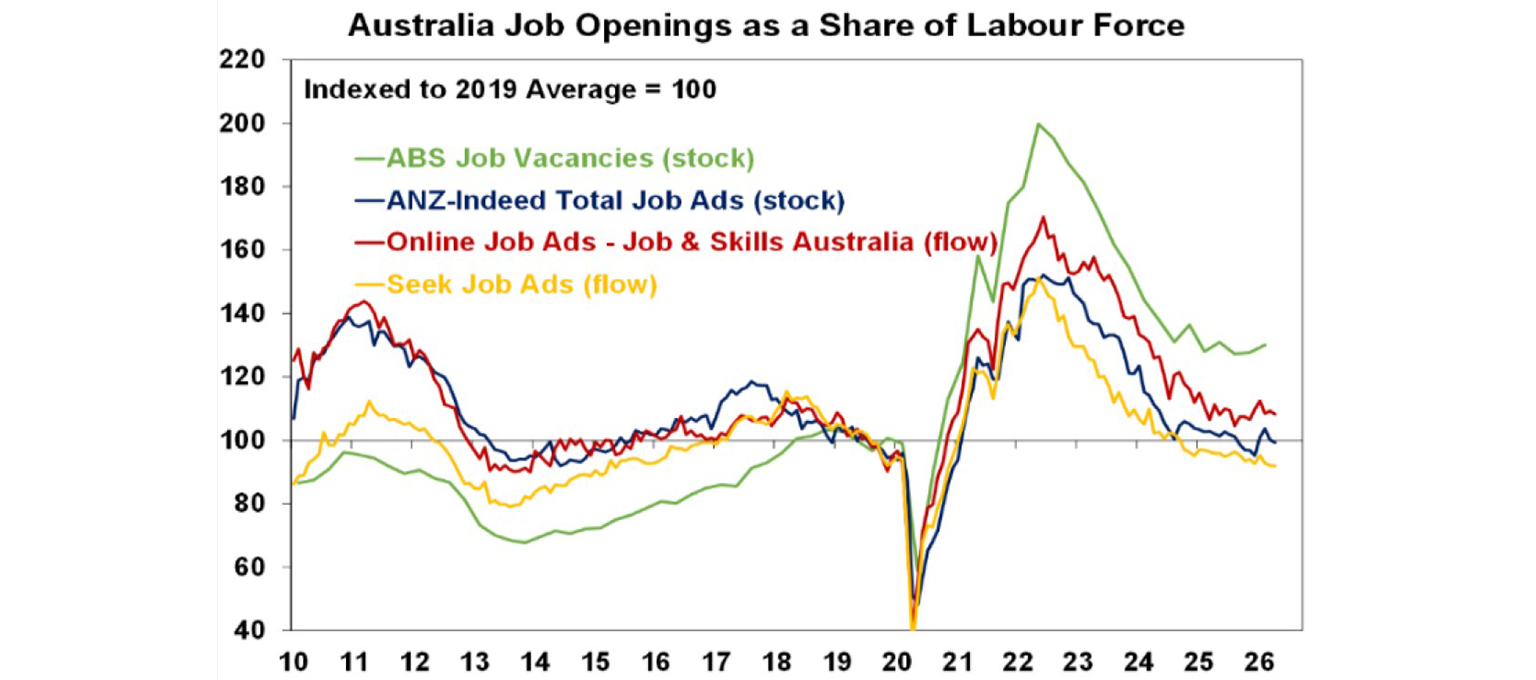

Job vacancies are down from their highs but are at okay levels and may have been starting to bottom. So the RBA is likely to continue to characterise the jobs market as slightly tight.

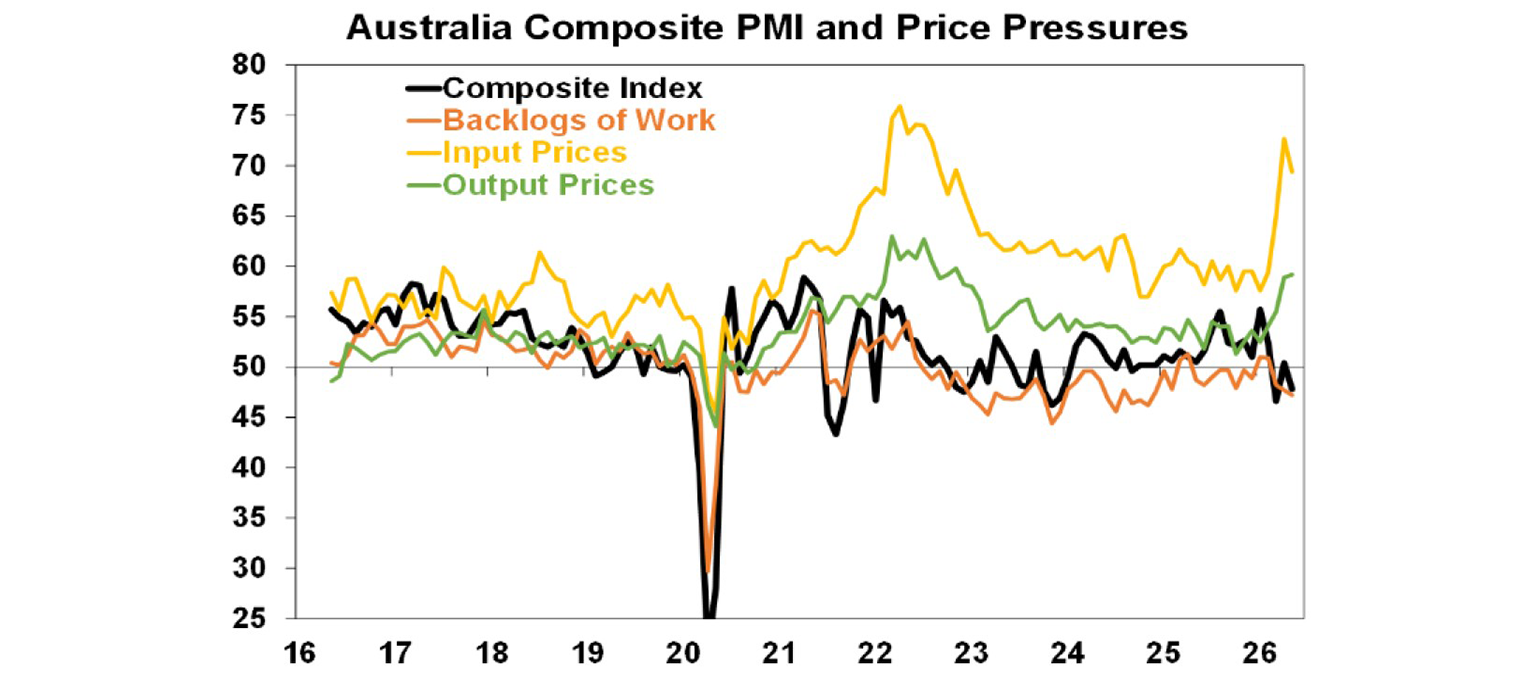

Australian business conditions PMIs for May continued to show weak economic conditions as rate hikes and the oil supply shock impact. New orders and employment were both down sharply. At the same time the input and output price indicators remain around 2022 levels.

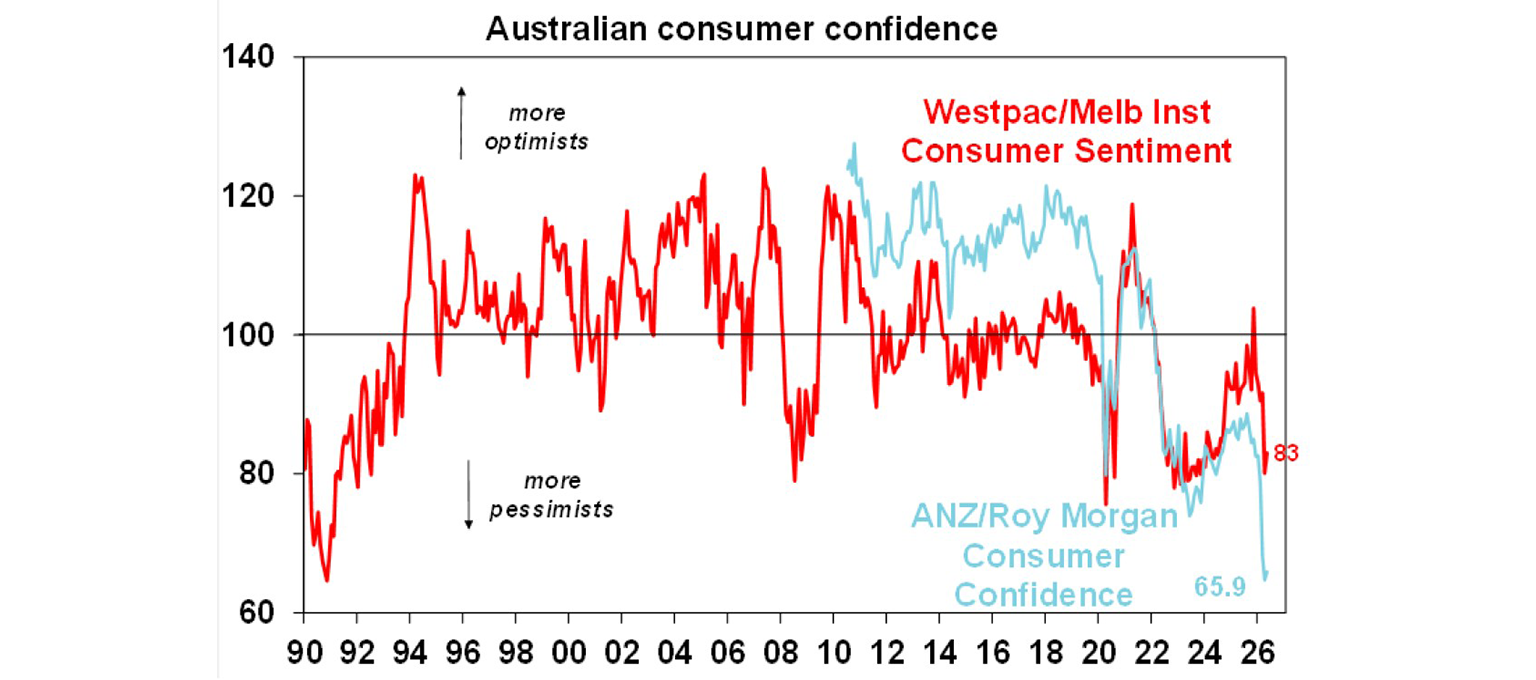

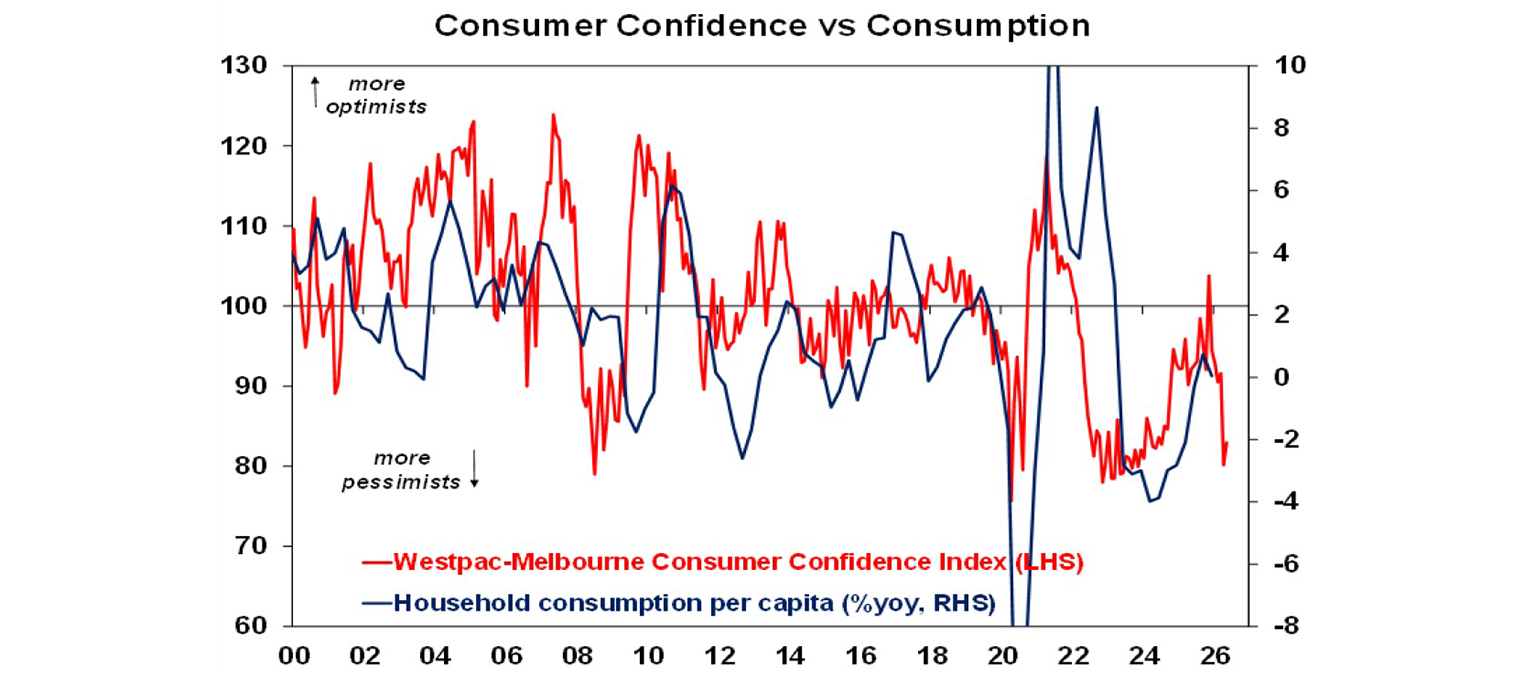

Consumer confidence improved slightly in May according to the Westpac/MI survey with lower fuel prices and Budget talk of small income tax cuts – but it remains very weak with the alternative ANZ/Roy Morgan index looking even weaker. The rise in confidence was amongst younger age groups suggesting a positive reaction to the changes to negative gearing and capital gains tax, whereas there was little change in confidence amongst those aged 45 and over.

The weakness in consumer confidence if sustained is warning of weakness in consumer spending ahead.

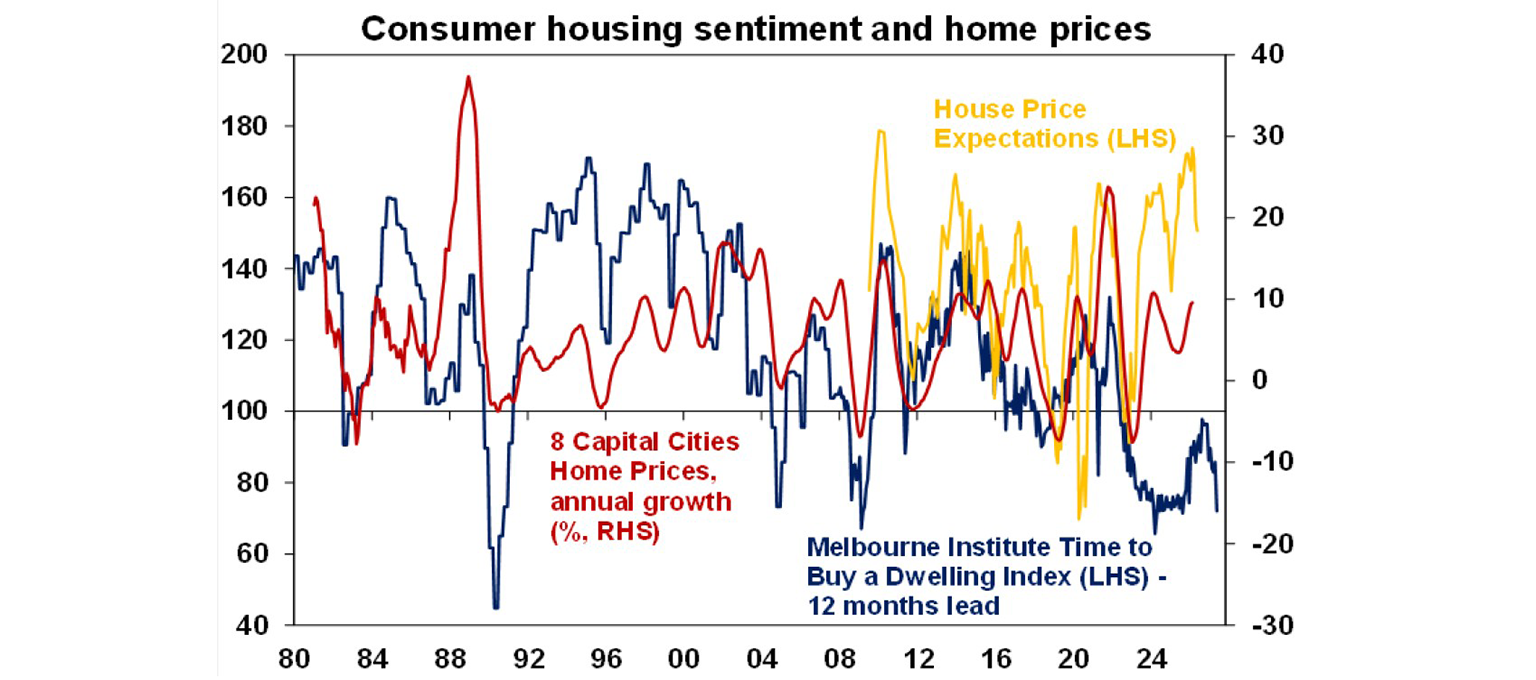

The Westpac/MI consumer survey showed a fall in home price expectations, but consumers continue to see now as a very poor time to buy a dwelling.

Consumer inflation expectations fell back in May with lower petrol prices but remain high.

What to watch over the next week?

In the US, expect consumer confidence to remain weak (Tuesday) but the trend growth in capital goods orders (Thursday) to remain strong with core private final consumption deflator inflation (also Thursday) expected to have increased further in April to 3.3%yoy.

The Reserve Bank of New Zealand (Wednesday) is expected to leave its cash rate at 2.25%, but signal hikes ahead.

In Australia, April inflation data (Wednesday) is expected to show a slowing to a 0.6%mom rise helped by flattish petrol prices partly due to the fuel tax cuts with annual inflation cooling to 4.4%yoy from 4.6%yoy in March. Trimmed mean inflation is expected to edge up though to 3.4%yoy as second round effects from the higher fuel prices start to show up consistent with the surge in price pressures evident in business surveys (see in the Australian section above). In other data expect a 0.9%qoq rise in March quarter construction activity (also Wednesday), a 1% rise in business investment for the March quarter and a slowing in April household spending growth to -0.7%mom/5.5%yoy (both Thursday) and signs of a slowing in housing credit growth for April (Friday) as rate hikes impact.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction remains high given uncertainty around the flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Trump still likely to pivot to consumer-friendly policies and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth this year is likely to slow to around 3% and could go negative over the year ahead due to poor affordability, RBA rate hikes, reduced investor demand likely to result from the Budget moves to wind back negative gearing and the capital gains tax discount and the hit to confidence from the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA holds or hikes. Fair value for the $A is around $US0.72.

You may also like

-

Weekly market update - 07-08-2026 Global shares had another ripper week with major share markets reaching new all-time highs, before retracing slightly on Thursday as the Iran “deal” seems further away than previously thought. -

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.