Super

Supercharge your super with Lifetime Boost

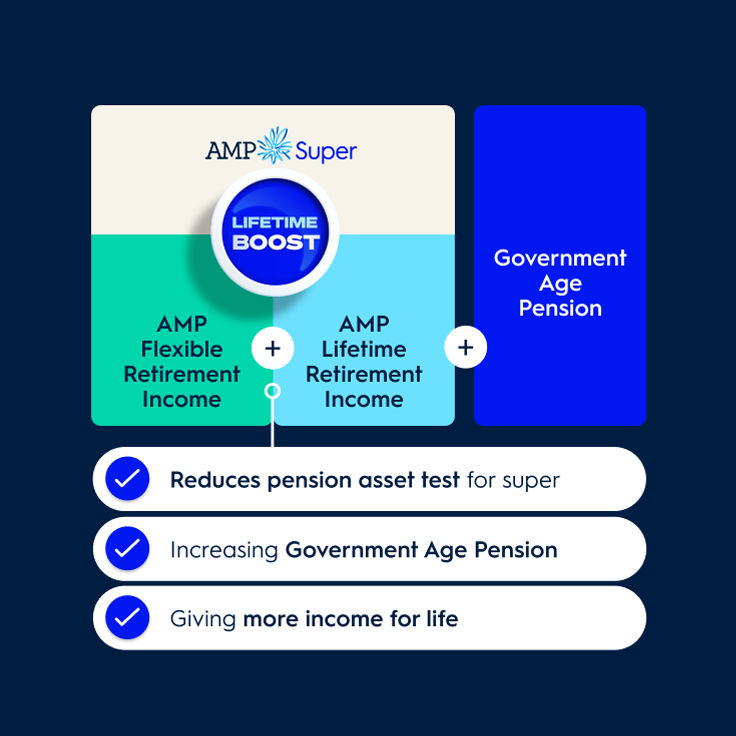

Lifetime Boost is a feature designed to maximise your overall retirement income as your super grows - all for no extra fees. See how it works with our personalised digital advice tool.

Manage your account anytime, anywhere with My AMP

The AMP Bank GO app is now available on your mobile

Or login to

Head to your app store to:

* This information is illustrative only and does not replace financial advice. It illustrates potential benefits for a representative AMP Super member with the AMP Super Lifetime feature activated for 20 years leading up to retirement and allocate 50/50 between an AMP Lifetime Retirement Income and an AMP Flexible Retirement Income. A representative AMP Super member is a 47-year-old single male, $90K super balance, $100K salary, contributes 12% with no career breaks, retires at 67 with $120K in other assets at retirement, homeowner and withdraws the minimum from the AMP Flexible Retirement Income. It assumes annual investment returns of 6.33%, wage inflation of 3% p.a. The benefits of Lifetime is only realised if you take out a AMP Lifetime Retirement Income.

There is no obligation however to take up this income stream if you have the Lifetime feature but the benefits will not apply.

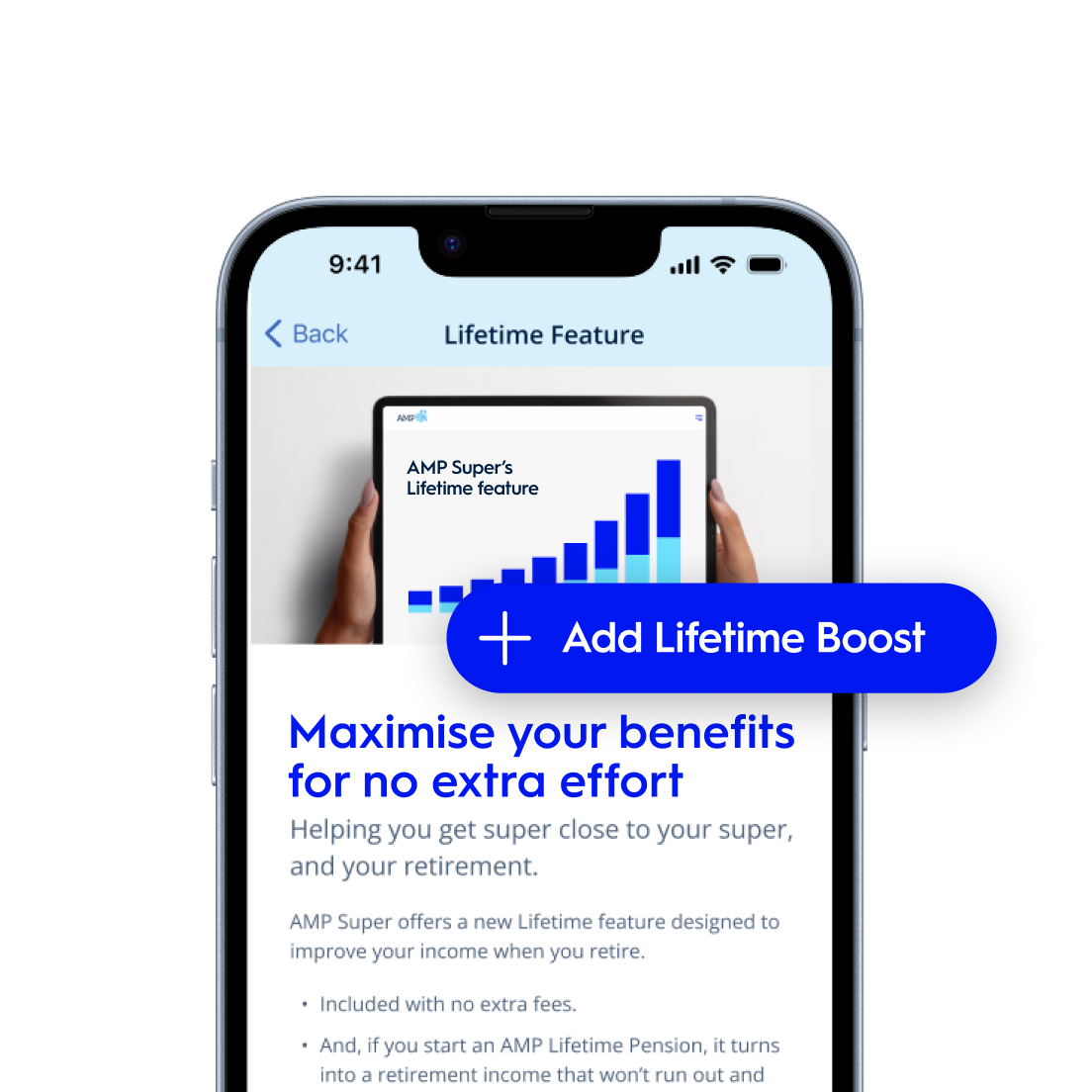

While for some of us planning for retirement feels far away or even overwhelming, there are things you can do now to set your future self up for the better. The new Lifetime Boost feature can give you a lot of benefit for not much effort. Best of all, you can get it for no extra fees and you’re under no obligation to convert to the AMP Lifetime Retirement Income*.

Improve your overall retirement income options for no extra fees or effort.

It works in the background to increase your eligibility for the Government Age Pension. The longer you have Lifetime Boost, the greater the boost could be.

The feature doesn’t lock you in, it just gives your future self greater retirement options.

There is no change to your other existing account features, or investment mix.*

Are you a ‘MySuper’ member?

MySuper members, will need to become a ‘Choice’ member to activate the Lifetime Boost feature. Learn more in the FAQs below.

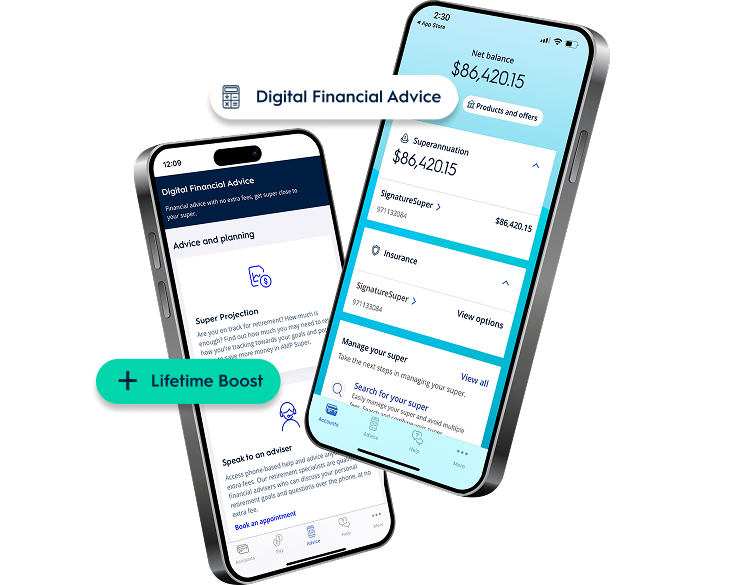

Adding the Lifetime feature to your account? You can do this and much more in My AMP. It's easy to register using your AMP account number (this can be found on your Lifetime feature communication).

Want to understand more about the Lifetime Boost feature? Watch our explainer video to see how it works while you grow your super.

Tools & calculators

Member information

AMP Super refers to SignatureSuper® which is issued by N.M. Superannuation Proprietary Limited ABN 31 008 428 322 AFSL 234654 (NM Super) and is part of the AMP Super Fund (the Fund) ABN 78 421 957 449. NM Super is the trustee of the Fund.

® SignatureSuper is a registered trademark of AMP Limited ABN 49 079 354 519.

* More members can expect to get a higher retirement income when investing in AMP Lifetime Retirement Income, along with an AMP Flexible Retirement Income . Based on analysis performed by a third-party consulting firm, assuming most members are in good health. The analysis made certain assumptions including about the AMP membership profile, product allocation, investment strategy, returns and draw down rates, and the age income stream rules and laws at the time of the analysis.

Any advice is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature only. It doesn’t consider your personal goals, financial situation or needs. It’s important you consider the appropriateness of any advice and read the relevant product disclosure statement and target market determination available at amp.com.au, before deciding what’s right for you. AWM Services is part of the AMP group and can be contacted on 131 267 or askamp@amp.com.au.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services it provides. You can also ask us for a hard copy.

The benefits of Lifetime Boost is only realised if you take out the AMP Lifetime Retirement Income. There is no obligation however to take up this income stream if you have the Lifetime Boost feature but the benefits will not apply.

AMP Flexible Retirement Income which refers to AMP Super Allocated Pension and AMP Lifetime Retirement Income which refers to AMP Super Lifetime Pension. AMP Lifetime Retirement Income is designed to work alongside other products issued by NM Super as well as the Lifetime Boost feature in AMP Super (SignatureSuper). Therefore, it may have features or conditions which may not be suitable for you. Before deciding to acquire or to continue to hold AMP Lifetime Retirement Income, you should consider your circumstances and read the “Retiring with AMP Super” PDS and TMD available on amp.com.au.

Digital Financial Advice is provided by AWM Services to eligible members of the AMP Super Fund.

By activating the Lifetime Boost feature, your account’s status will permanently change from a ‘MySuper’ to a ‘Choice’ account. Although MySuper accounts have additional legal protections in relation to fees and other characteristics, your fees, services and any insurance you hold would not change when Lifetime starts and you’d remain invested in your Lifestages option (unless you or we make changes in the future).

* This information is illustrative only and does not replace financial advice. It illustrates potential benefits for a typical AMP Super member with the AMP Super Lifetime feature activated for 20 years leading up to retirement and allocate 50/50 between an AMP Lifetime Retirement Income and an AMP Flexible Retirement Income. A typical AMP Super member is a 47 year old single male, $90K super balance, $100K salary, contributes 12% with no career breaks, retires at 67 with $120K in other assets at retirement, homeowner and withdraws the minimum from the AMP Flexible Retirement Income. It assumes annual investment returns of 6.33%, wage inflation of 3% p.a. Figures shown in today's dollars and adjusted for 3% annual inflation.