Weekly market update

Investment markets and key developments

It was a mixed ride for global share markets over the last week as there was little progress towards ending the US War with Iran and the Strait remained effectively closed to shipping with blockades from both sides.

9 min read

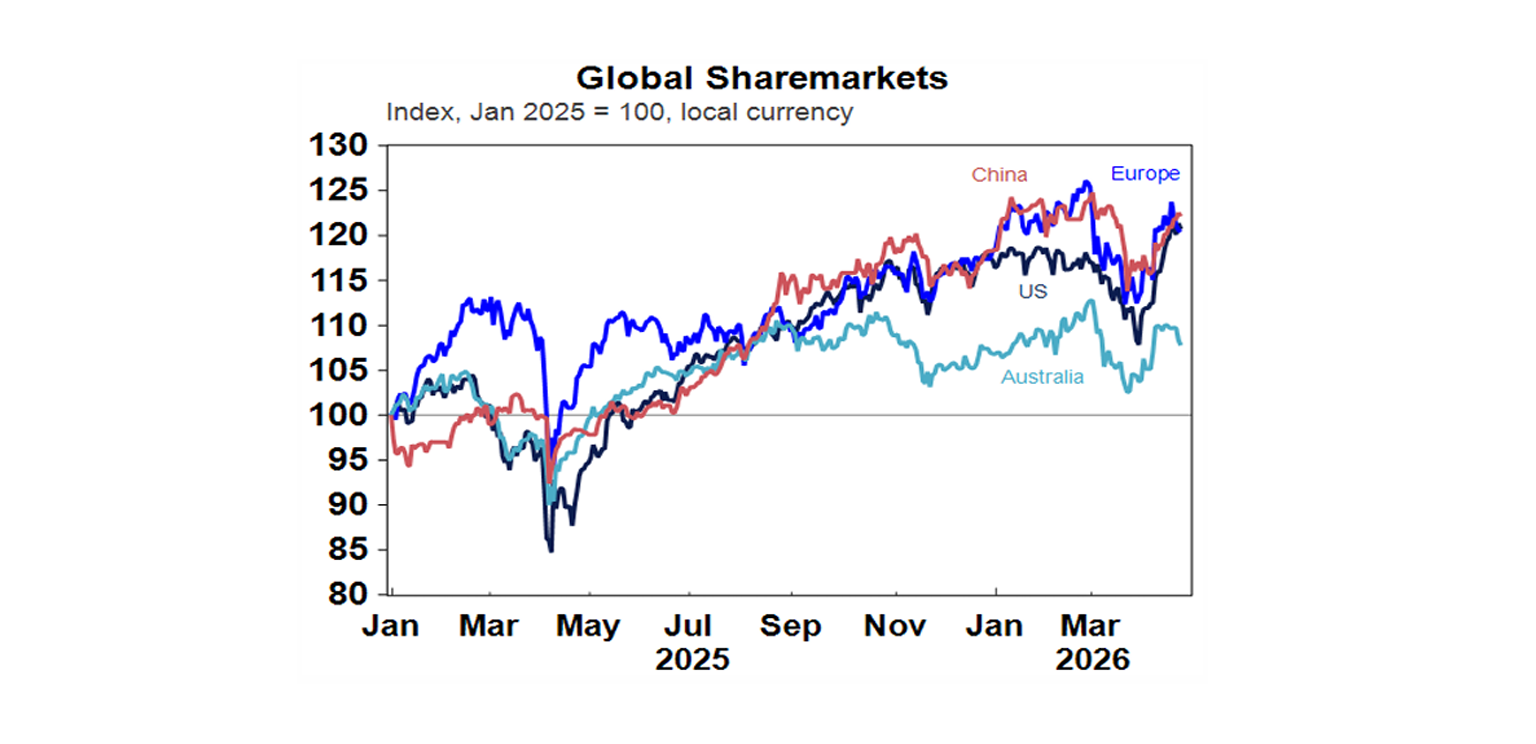

It was a mixed ride for global share markets over the last week as there was little progress towards ending the US War with Iran and the Strait remained effectively closed to shipping with blockades from both sides. US shares rose 0.6% for the week to a new record high with optimism on Friday for fresh Iran talks - with reports that the US was sending envoys to Pakistan to meet with Iranian officials - and good earnings results, Japanese shares rose 2.1% and Chinese shares rose 0.9%. But Eurozone shares fell 2.7%. The volatile global lead, bigger concerns about Australia’s vulnerability to an extended closure of the Strait of Hormuz and profit downgrades saw the Australian share market fall 1.8% led by health, financial and mining shares. Global bond yields rose on concerns about higher inflation flowing from the continuing high level of oil and hence fuel prices, but Australian bond yields fell slightly.

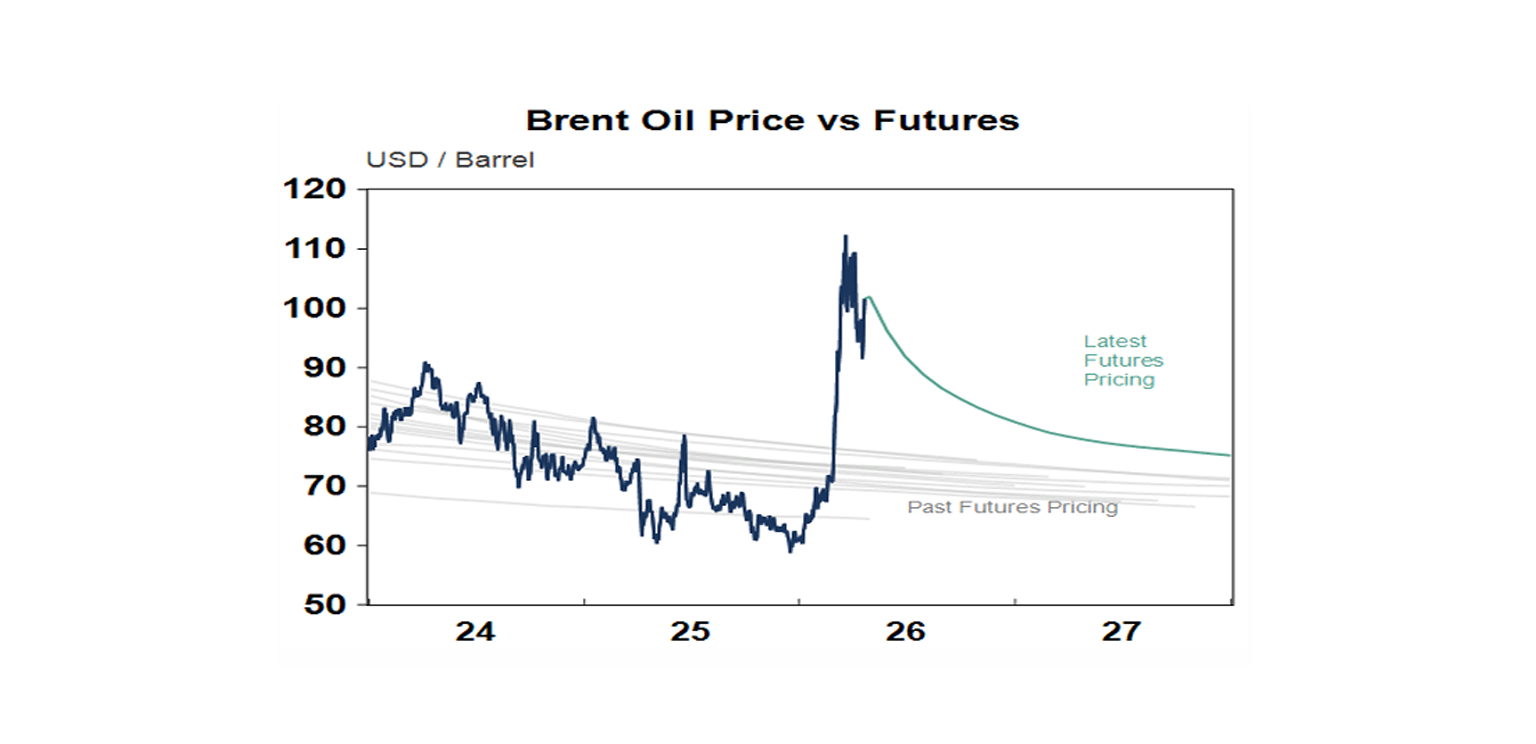

The effective ongoing closure of the Strait of Hormuz to oil flows and the risk of a re-escalation of the War saw oil prices rise with West Texas rising to around $US94 a barrel and Brent around $US105. Oil futures pricing still points a to fall back in oil prices as the market continues to assume there will be a resolution soon but even for next year oil futures imply pricing settling at higher levels than before the War.

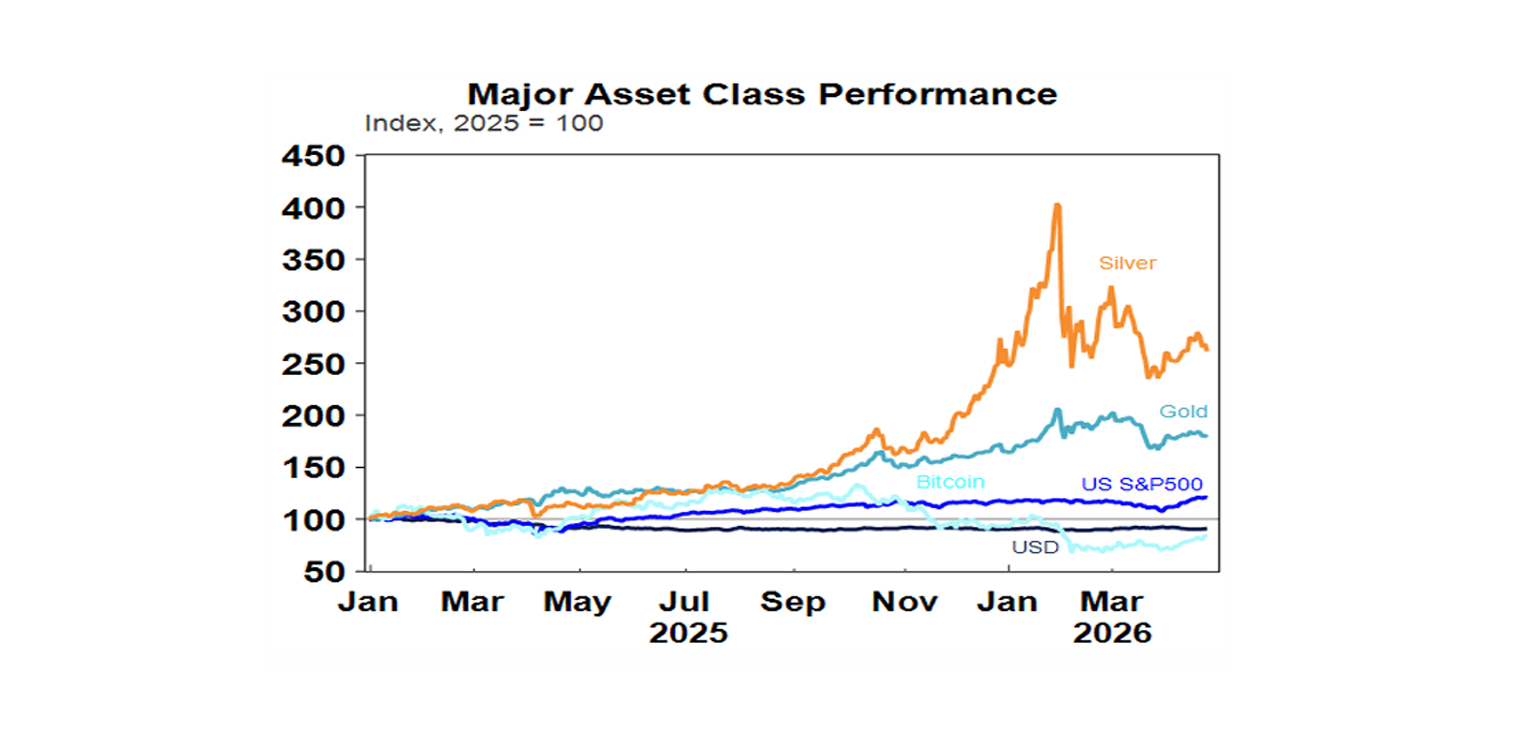

With worries about re-escalation and a longer closure of the Strait returning in the past week the $US ticked up a bit and the $A, gold and copper fell back a bit. That said Bitcoin and iron ore rose.

Another TACO Tuesday - our view remains that Trump wants to TACO and will find a way to stay on the off ramp from the War. But it all remains very messy and uncertain. Despite no more talks, Trump extended the ceasefire indefinitely on Tuesday (after saying he wouldn’t) to allow Iran to come up with a “unified proposal” but the Strait remains closed with Iran refusing to remove its blockade of ships from other countries until the US removes its blockade of ships to or from Iran. So, it’s at a standoff with occasional attacks on ships from each side to reinforce the blockade. What’s more Trump’s demeaning and humiliating social media posts may also be encouraging Iran to dig in. Uncertainty remains high but several things are apparent:

There is still a significant risk that the War could re-escalate again if agreement on a deal is not reached soon. This could see the US expanding its bombing and Iran retaliating by hitting more ships in the Strait of Hormuz and getting the Houthi’s to do the same in the Red Sea. Maybe Trump’s ceasefire extension is just allowing a further military buildup. Share markets appear to be underestimating this risk.

But, Trump by his actions has shown he wants to end the War and declare victory (however vacuous that victory may be). Pressure on Trump to back down remains very high with only a third of Americans supporting the War and his approval lower than Biden’s. As things stand the GOP could see a loss of both the House and the Senate in November, which could open the door to numerous Congressional enquiries and possible impeachment of Trump.

And pressure on Iran to reach a deal is high as the US switch from bombing (which can unite a population) to even tougher economic sanctions via the blockade of Iranian oil exports will intensify popular discontent with the Iranian Government. And it may conclude that its ability to cause pain for the US by effectively blocking 20% of global oil supply means it has no need for nuclear weapons to ensure it survives. But Iran has a fractured unclear leadership and still has a relatively strong hand.

Which means that some sort of deal to end the War and reopen the Strait is more likely than not but that it could be a low quality deal – leaving the regime in place aided by an easing in sanctions but more aggressive than ever (with the new Ayatollah reportedly losing multiple family members in Israeli/US attacks) and arguably more powerful with its now proven control of the Strait. So, 6000 lives and $US40bn plus in war costs later, the War may not have achieved much, meaning it could all flare up again down the track if there is a deal.

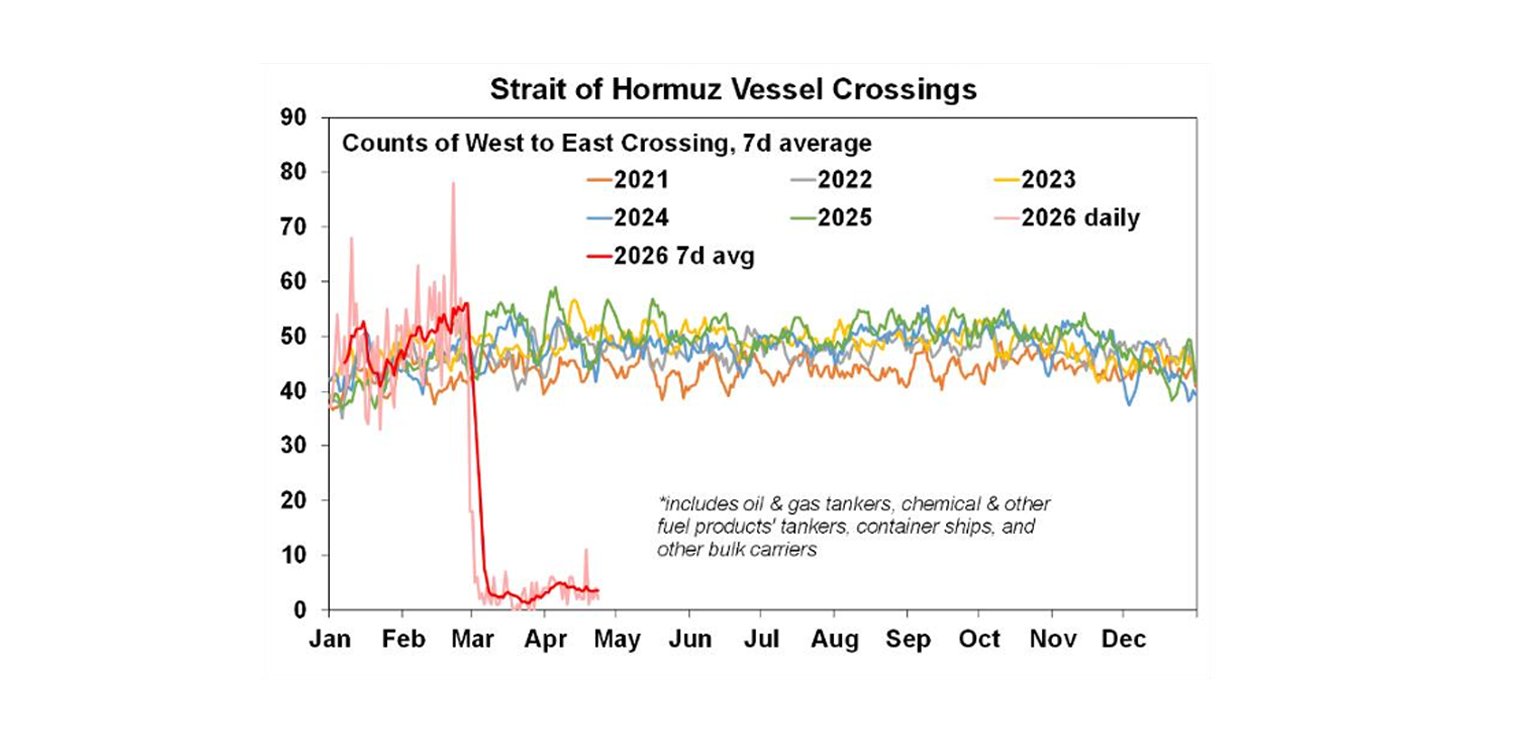

The key to watch remains the Strait of Hormuz and despite a brief spike in ship traffic it remains effectively closed. While a bout of mild stagflation is baked in the clock is now ticking on whether this turns into a more severe bout like that seen in the 1970s. So far we have been able to get by because refineries still had oil to refine from ships that left in February and could rely on reserves but the longer it stays shut the more the global and Australian economies will have to face the consequence of the 10-15% reduction in global fuel supply its resulting in – which would mean even higher fuel prices (a rough calculation is that oil would need to go to around $US150/barrel) and fuel restrictions.

So, if our base case is right that Trump will stay on the off ramp and soon find way to get the Strait open then share markets have more upside. Particularly, with US March quarter earnings growth likely to come in at a strong 18%yoy. But, the risk of a renewed spike in oil prices and more volatility in shares remains high if a deal is not reached soon and the Strait if not reopened. So it remains a time for caution for those investors with a short time horizon.

This presents a very uncertain outlook for global central banks with five – including the Fed and ECB – due to meet in the week ahead. We expect all to leave rates on hold as they continue to assess the impact, but most are likely to remain biased to the upside on rates based on the experience of the 1970s oil shocks which suggests that the key is to initially focus on keeping inflation expectations down rather than cutting rates to support employment.

In Australia, we expect the RBA to hike again in May as inflation was already more problematic here and March inflation data to be released in the week ahead will reinforce this. It seems that its not just higher fuel prices and fuel levies that are on the way up but everything from airfares to toilets.

And here’s a happy song for my sister Tracy.

Major global economic events and implications

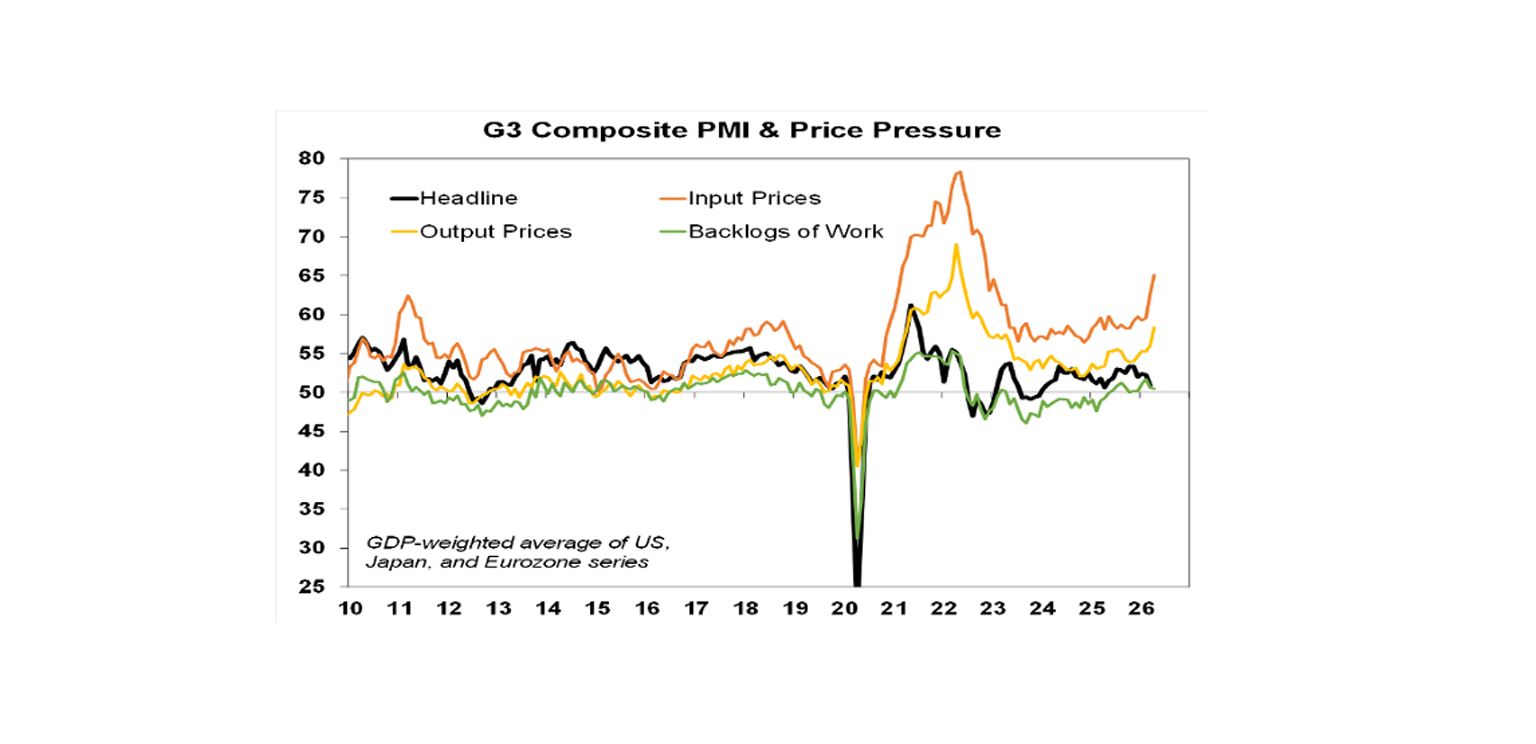

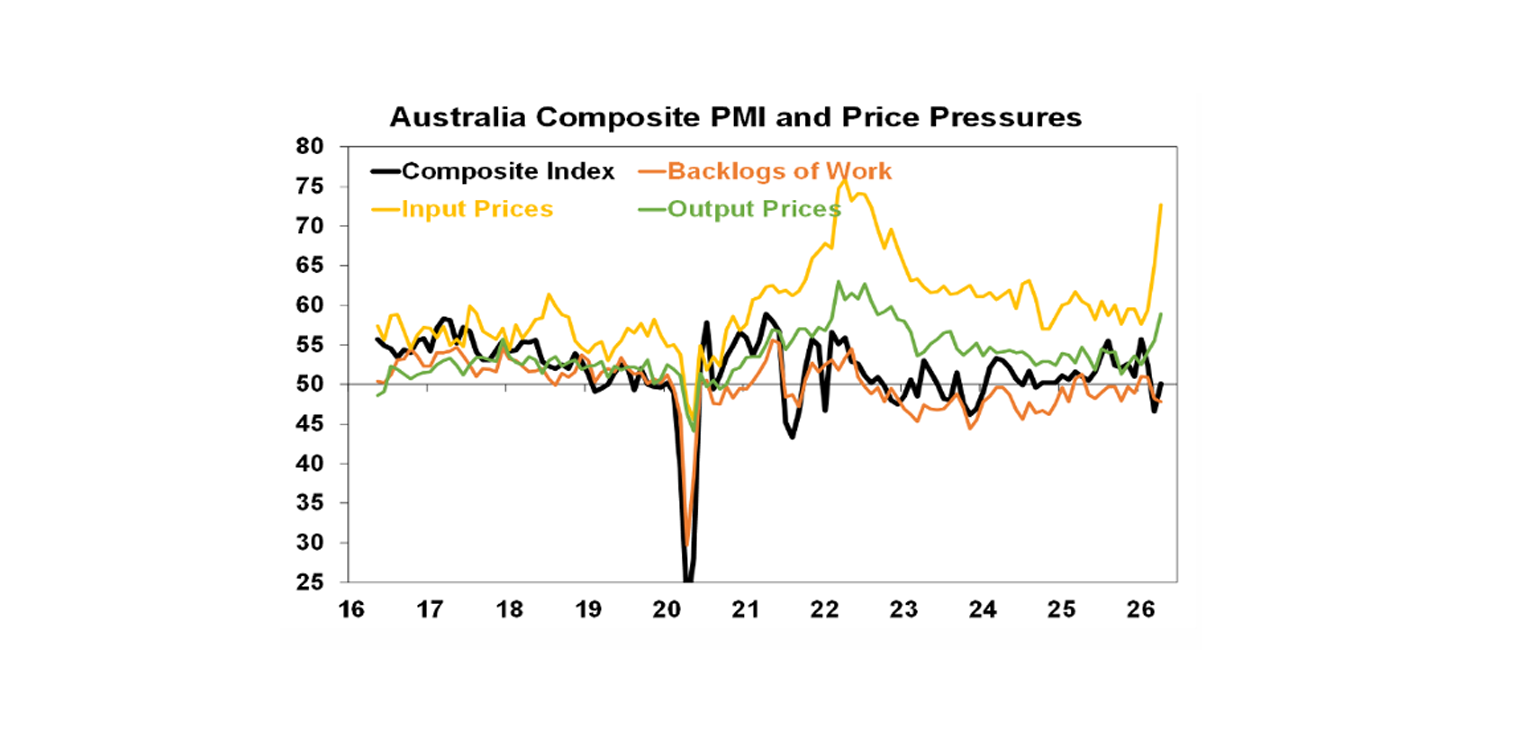

Developed country PMIs for April showed a further whiff of stagflation with slightly weaker business conditions and higher price pressures. The weakness in activity was concentrated in Europe and Japan, but with manufacturing up and services down. Both input and output price pressures rose further to levels last seen in 2022. So, a whiff of stagflation, but so far its mild and not indicating recession – at least not yet.

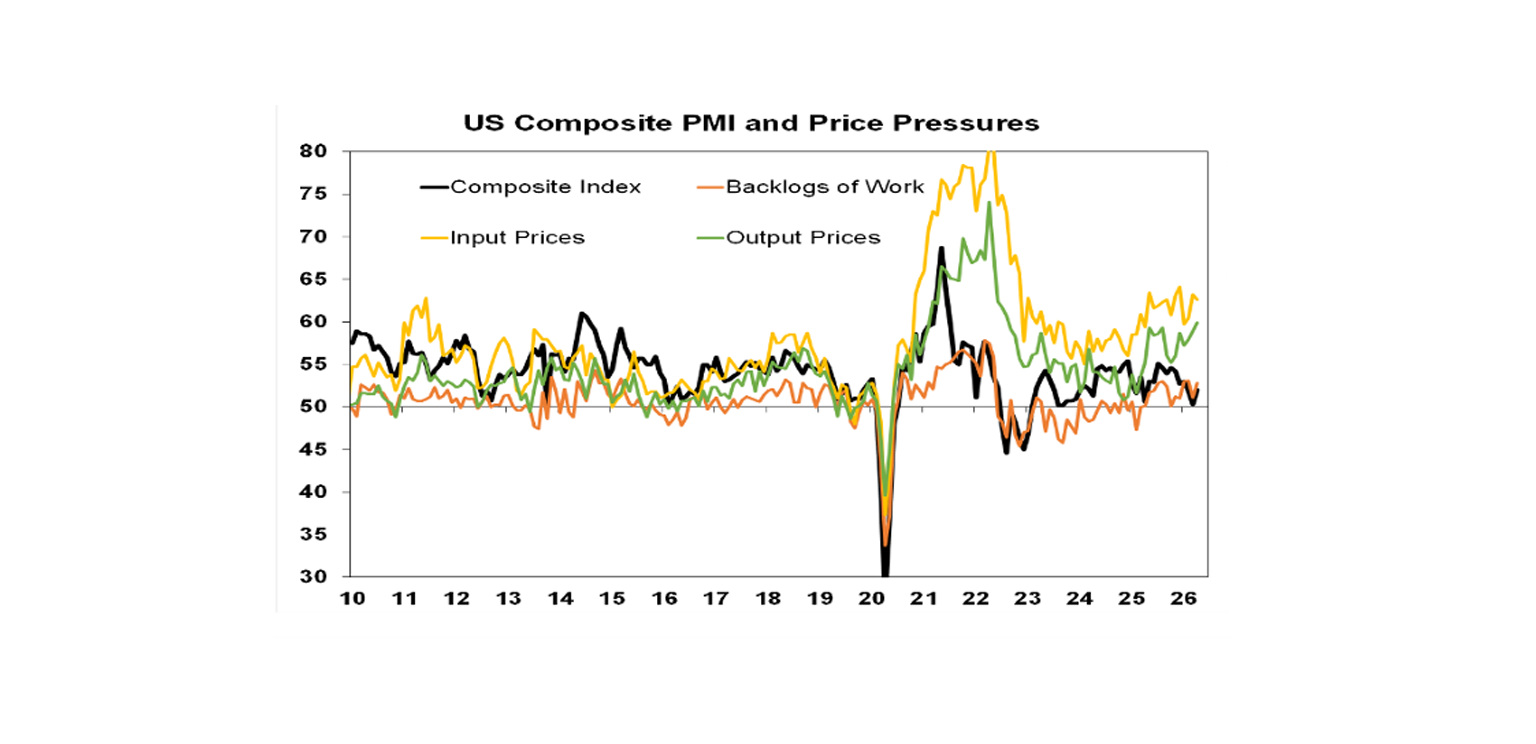

The US composite PMI improved in April. It’s below last year’s highs but its relative resilience highlights that the US is less impacted by the oil shock being a net oil exporter. Input price pressures remain elevated, and output prices rose to their highest since 2022.

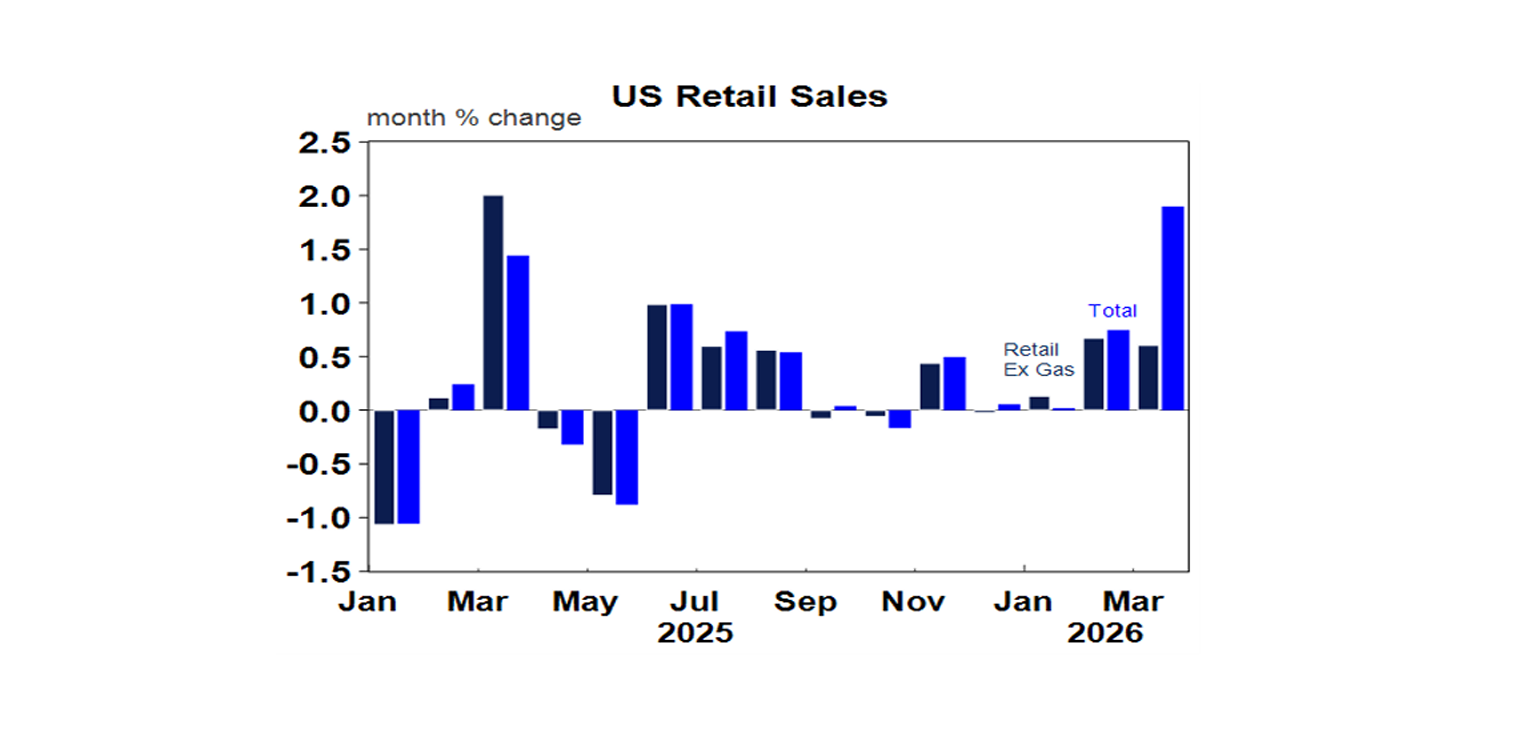

US retail sales for March suggest that the consumer remains resilient despite the surge in gasoline prices and falls in confidence. A 15.5% surge in gasoline prices drove retail sales up 1.7%mom, but underlying retail sales rose a solid 0.6% for the second month in a row although this was likely also boosted by high goods price inflation. Meanwhile, jobless claims remain low.

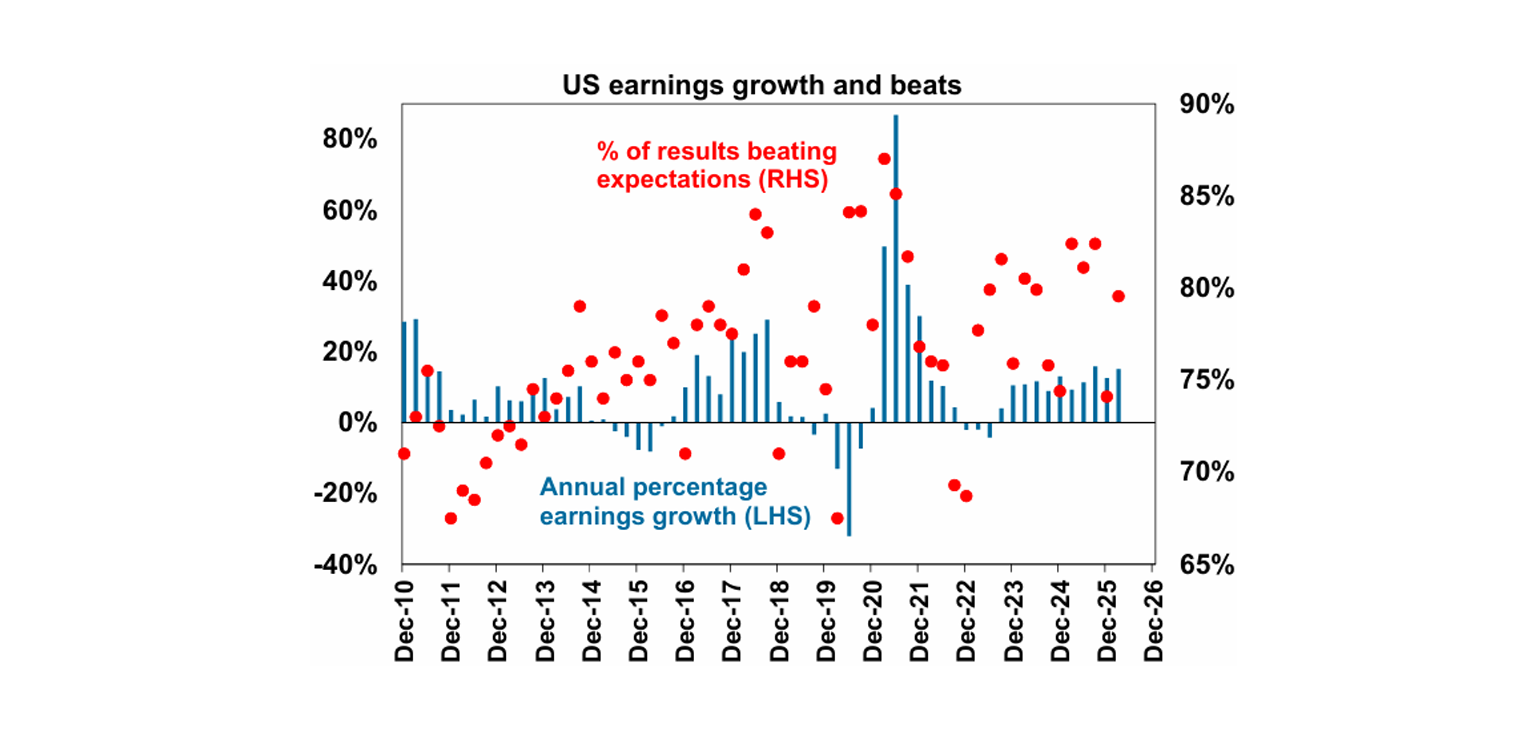

It still early days in the US March quarter earnings reporting season with only around 27% of S&P 500 companies reporting so far but results have been strong with 78.8% beating expectations and consensus earnings growth for the quarter moving up from 14%yoy to 15%% and likely to end up around 18%yoy, which will be the strongest in five years. Tech companies are again leading the charge with earnings growth around 32%yoy.

Fed in wait and see mode and unlikely to change much under Kevin Warsh. Some guide to a Warsh Fed was provided by his Senate hearing. At a high level Warsh is committed to Fed independence, he may put more weight on the AI transformation and less on employment (but this may lead to the same thing for rates), he may put more weight on the trimmed mean and median measures of inflation than the core PCE (although this may be seen as cherry picking because they are lower at present because they screen out more of the impact of tariffs), he leans towards lower rates but a smaller Fed balance sheet and he leans towards less communications and forward guidance from the Fed (which may be good). Overall, he probably leans a bit more dovish that Powell but not radically so. In the near term like others on the Fed he looks like he would lean to waiting to see the impact of the War on inflation and in any case he has to bring the rest of the Fed along with him. And on that front Trump appointees Waller, Bowman and Miran have all become less dovish. The decision by the DoJ to drop its investigation of Powell potentially clears the way for Warsh to be confirmed as Fed Chair by the 15 May expiry of Powell’s term, but Powell may still opt to stay on as Governor where his term extends to 2028 partly because it’s not clear that the DoJ has completely given up.

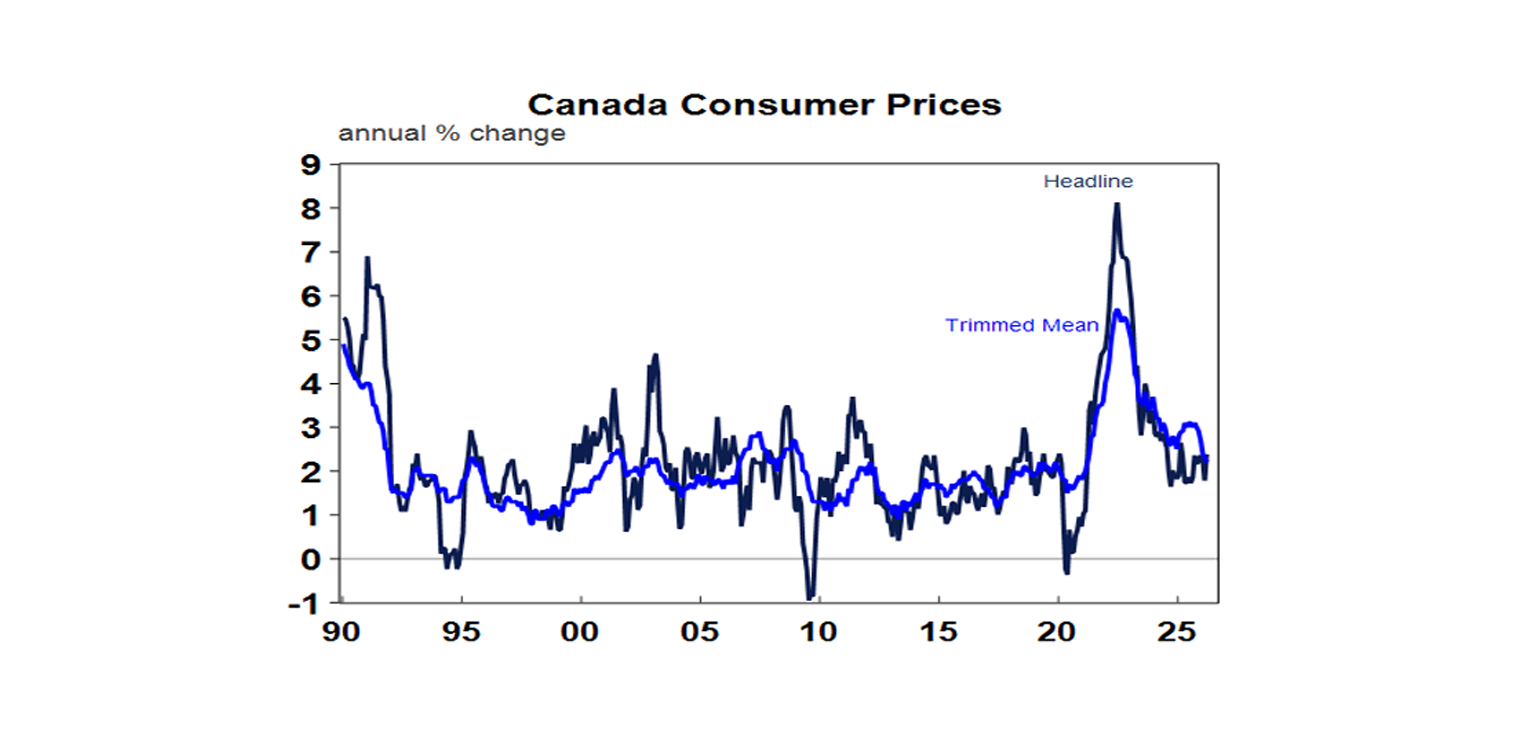

Canadian inflation rose to 2.4%yoy in March with a 21% rise in petrol prices, but underlying measures were a bit softer around 2%yoy, suggesting that the Bank of Canada can look through the headline inflation spike for now.

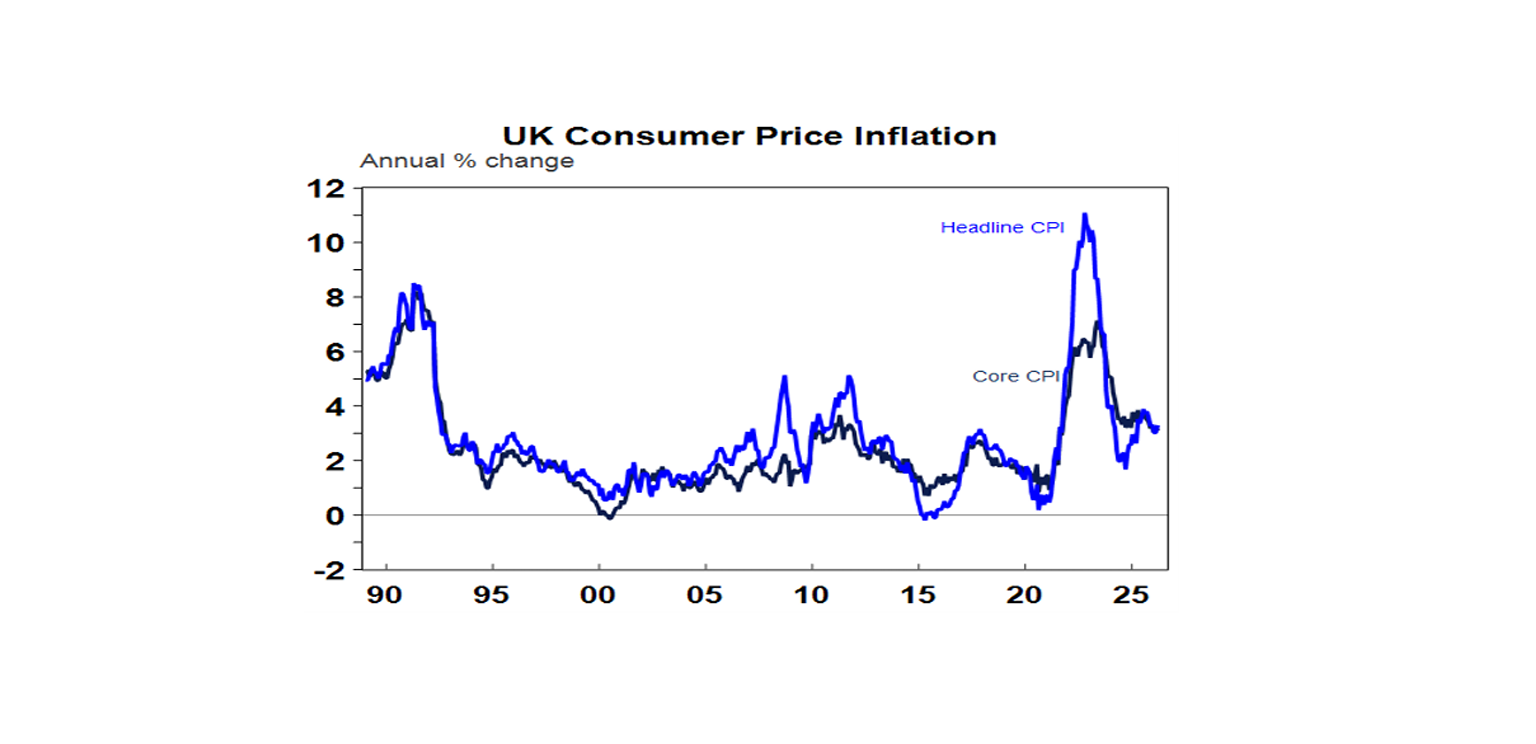

It was a similar story in the UK with headline inflation rising to 3.3%yoy with higher fuel prices, but underlying inflation was pretty steady, albeit at still high levels. The Bank of England is also expected to hold rates for now.

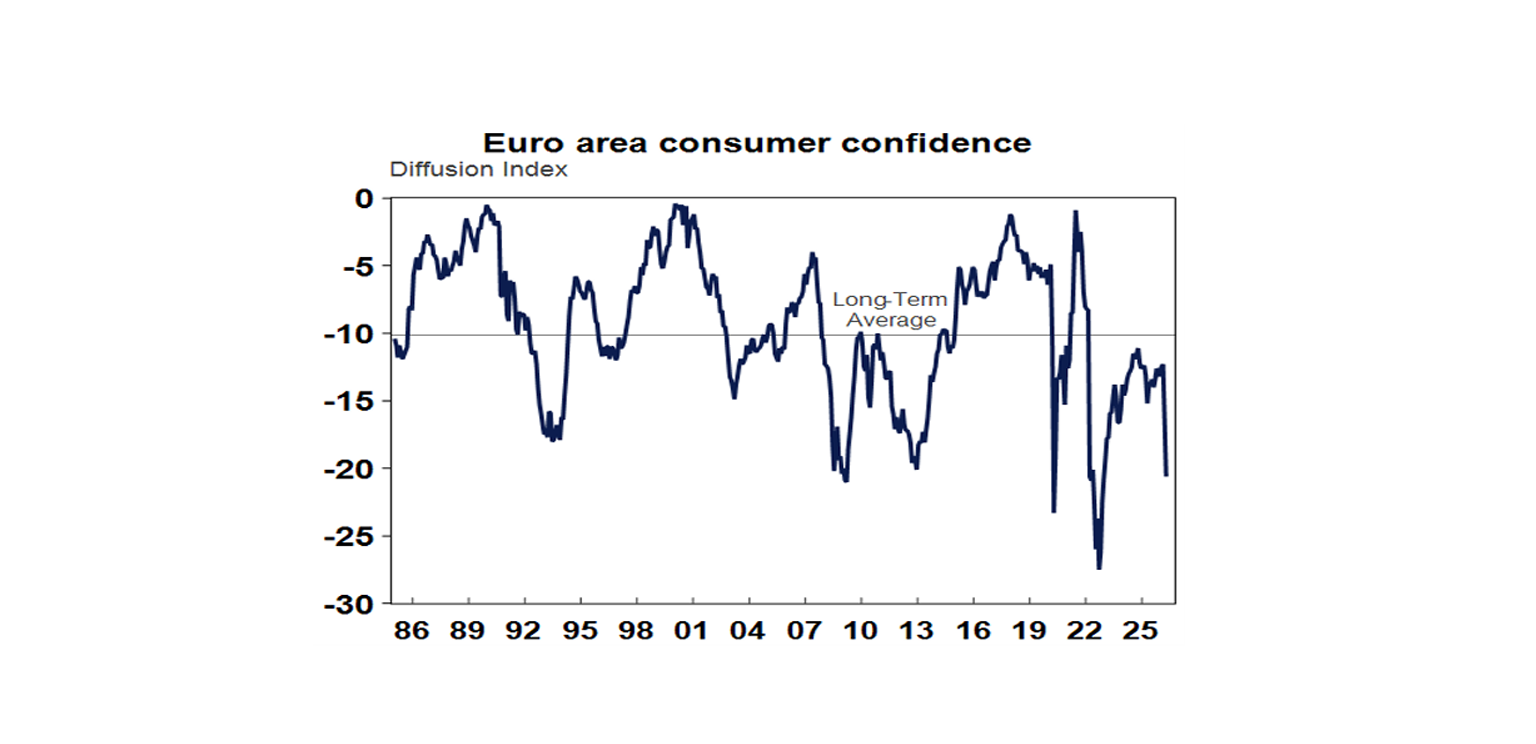

Eurozone consumer confidence plunged in April pointing to weaker consumer spending ahead.

Japanese inflation in March also rose but only to 1.5%yoy. Core inflation was unchanged at 1.4%yoy, leaving no reason for the BoJ to rush into another rate hike.

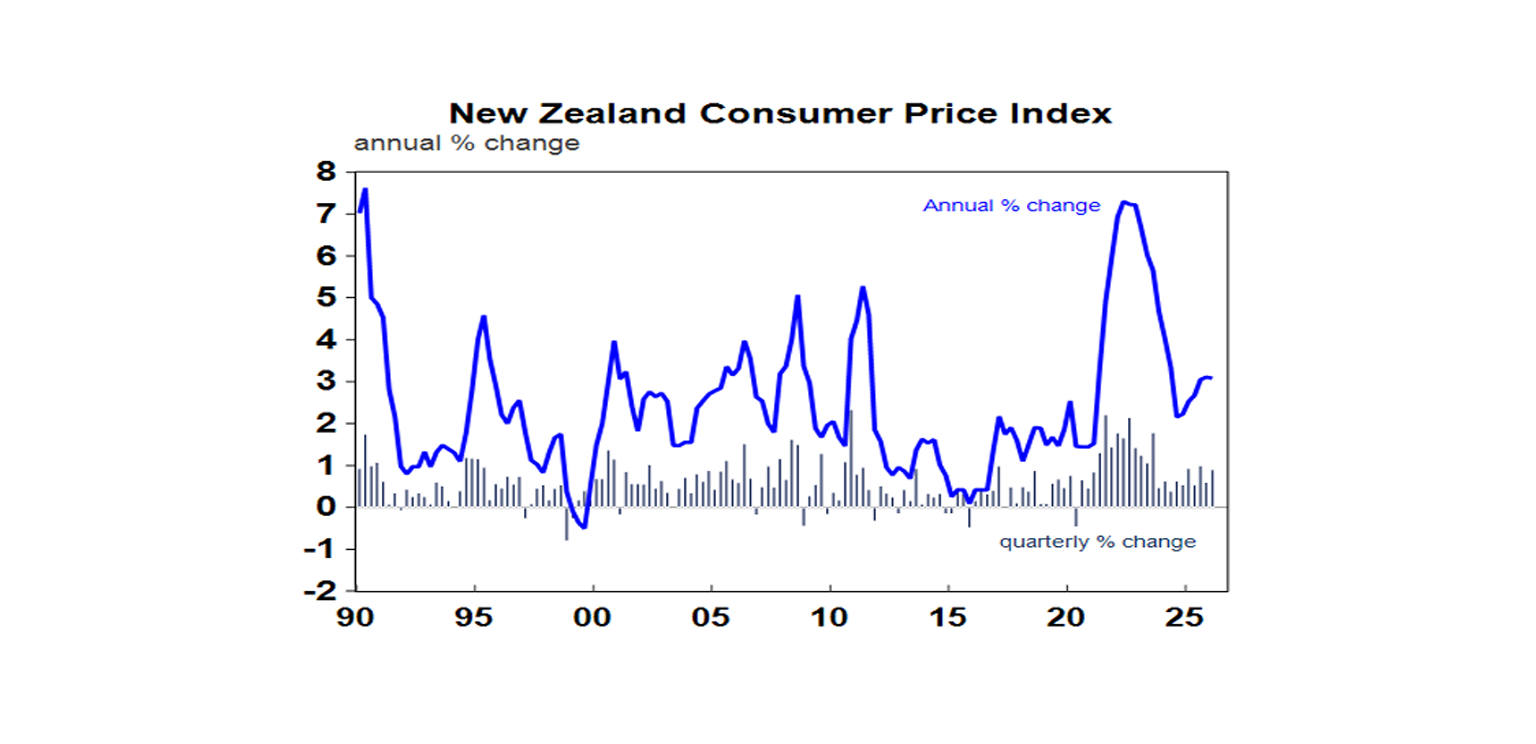

New Zealand inflation rose to 3.1%yoy in the March quarter, but of course its only showing one month of the War’s impact. Underlying inflation measures are mostly a bit above the 2%yoy inflation target midpoint with business surveys pointing to higher inflation ahead. The money market expects three RBNZ rate hikes this year.

Australian economic events and implications

Business conditions PMIs for April showed further signs of stagflation. The business conditions PMI rebounded after a very sharp fall in March but only to a soft 50.1 which leaves it well below prior readings, with orders remaining well down. At the same time the input and output price indicators rose to around 2022 levels.

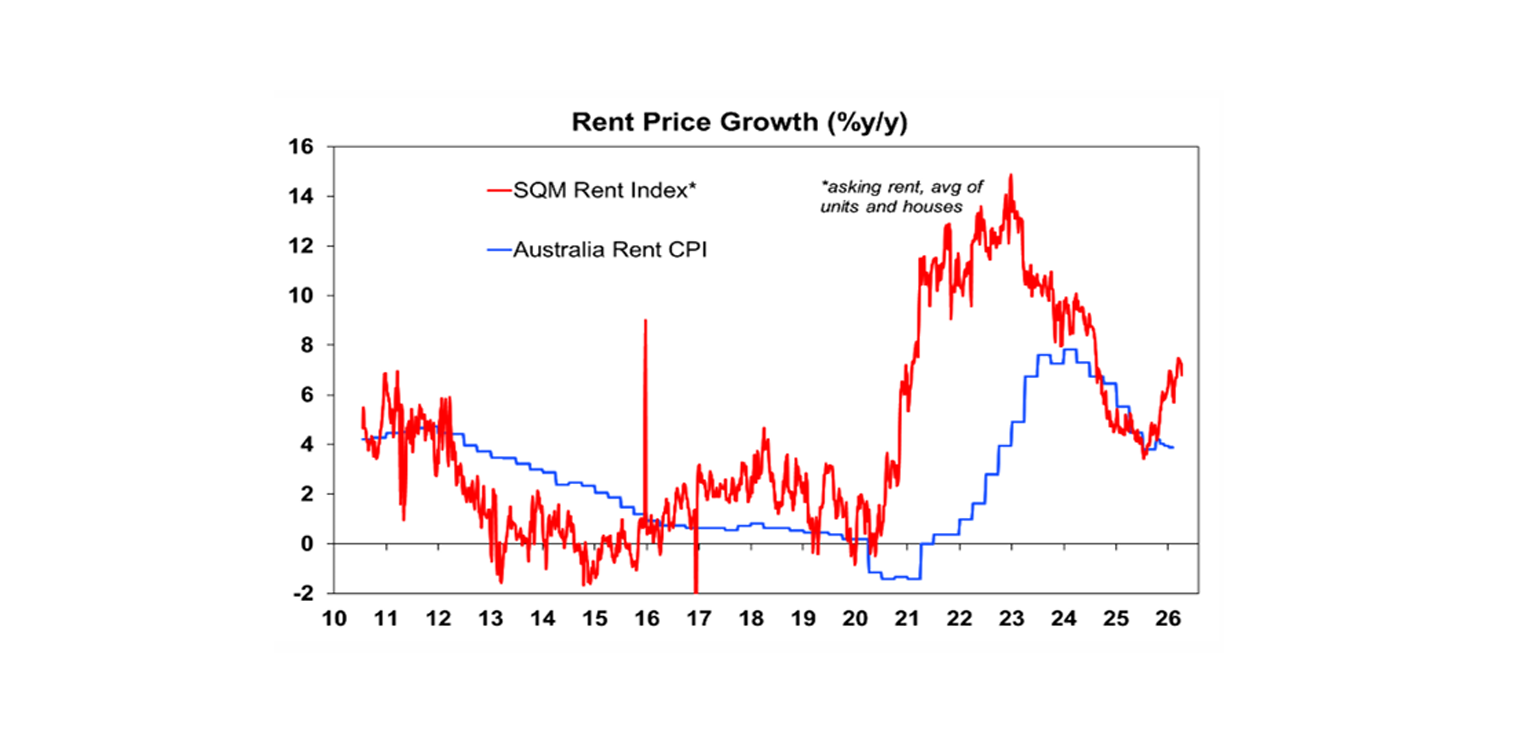

With housing related inflation being a big part of Australia’s inflation problem, the RBA won’t take much comfort from the next chart showing SQM’s measure of asking rents pointing to higher rent inflation in the CPI.

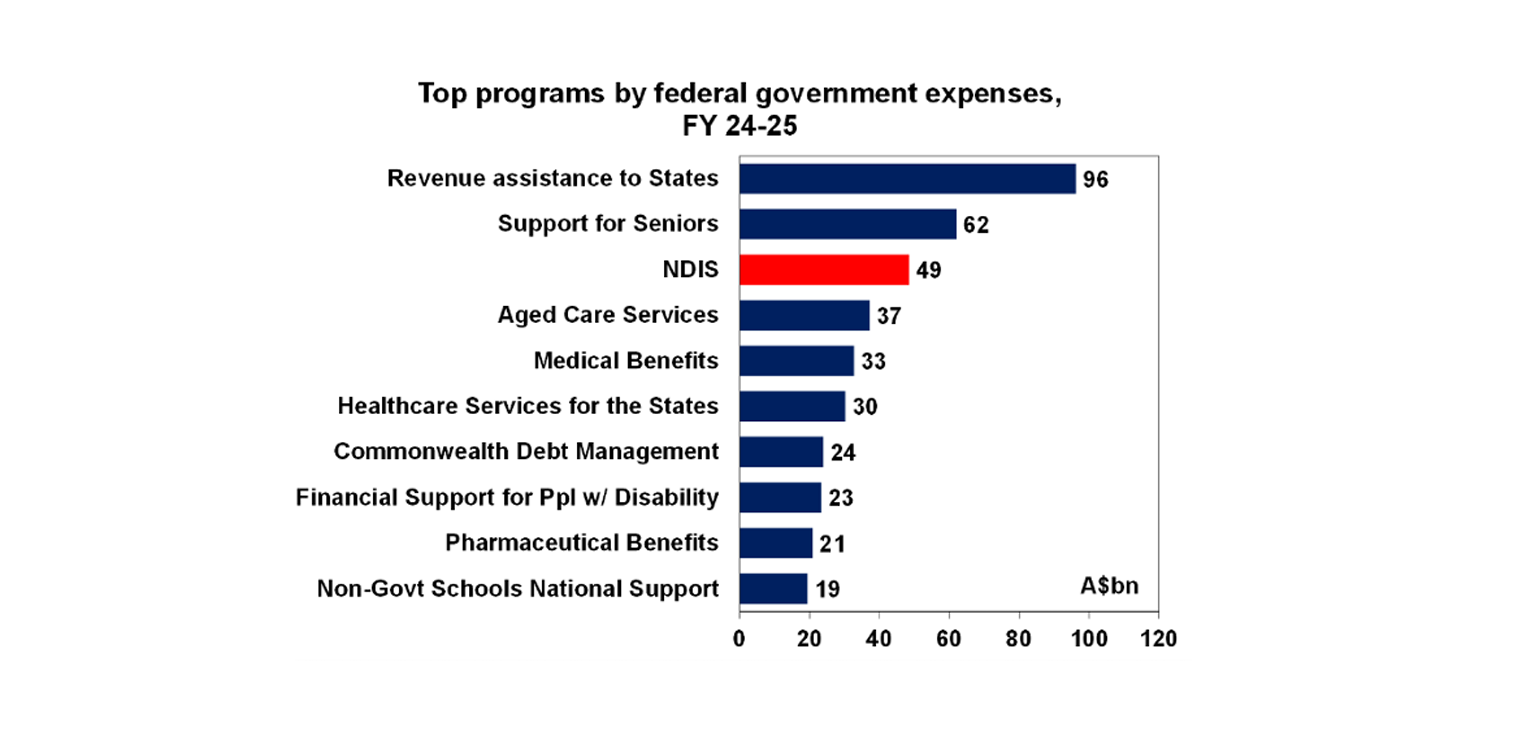

Meanwhile, it was welcome news to see the Federal Government moving to rein in the rapid growth in spending on the NDIS. A blowout in government spending as a share of the economy by leaving less room for private spending and acting as a drag on productivity growth has been a major reason behind Australia’s cost of living and inflation problem and the blowout in spending on the NDIS has been part of that. The NDIS is a great program, but it has grown much faster than originally anticipated to be now bigger than Medicare. With this has come explosive growth in health care and social assistance jobs (which have risen by about 2 percentage points as a share of total employment over the last four years). If the NDIS is not reined in there is a danger that it could lose its social licence, particularly with increasing reports as to how it’s being rorted. This is what happened to relatively unrestricted unemployment benefits in the 1980s and gave rise to the term “dole bludger”.

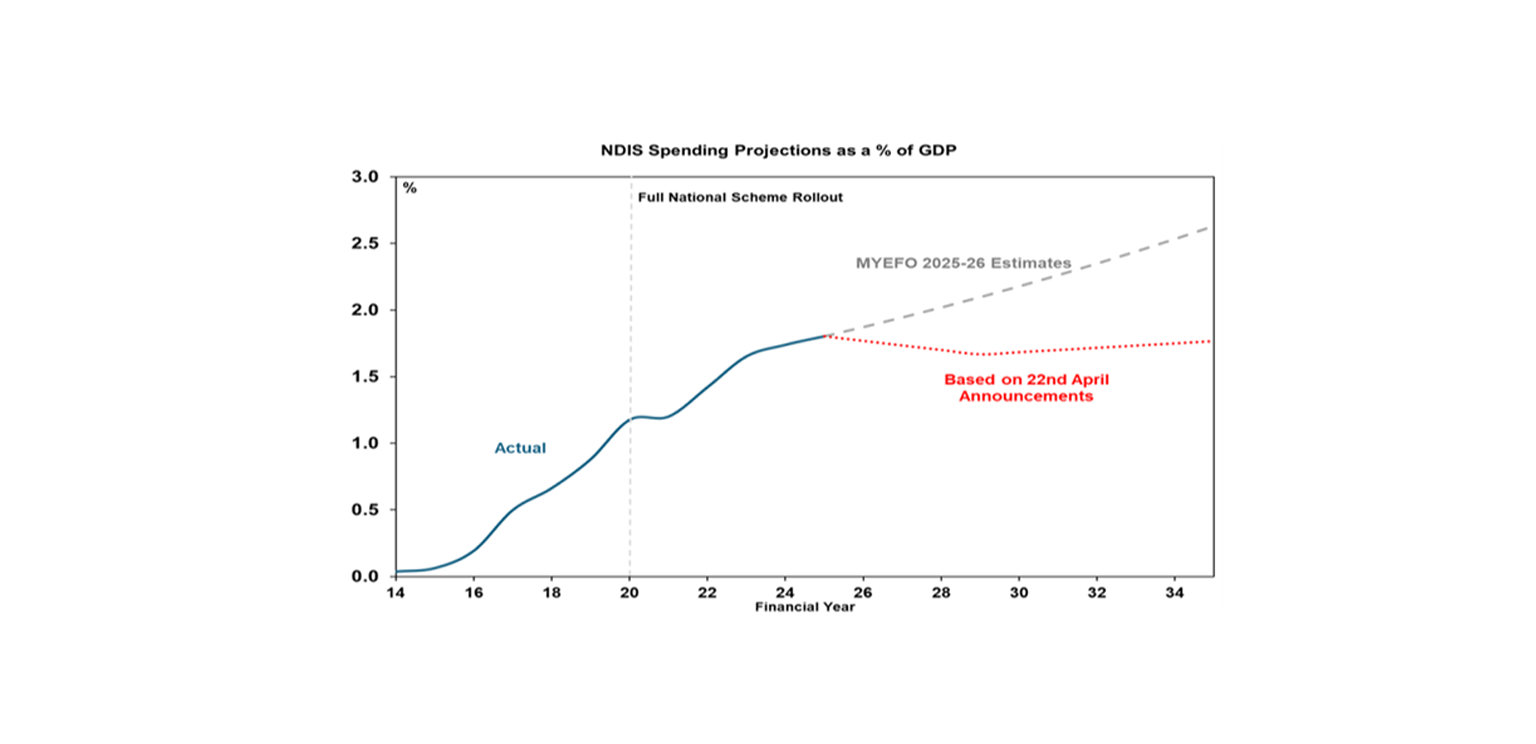

If the Government can deliver on its announced NDIS savings, spending on it should stabilise as a share of GDP.

What to watch over the next three weeks?

The week ahead will see major central banks – including the Bank of Japan (Tuesday), the Fed and Bank of Canada (Wednesday) and the ECB and Bank of England (Thursday) – all leave interest rates on hold as they continue to assess the boost to inflation flowing from the higher fuel prices against the drag on growth. While the Fed is still expected to cut rates this year its unlikely till later this year and other central banks are expected to raise rates

In the US expect a fall in consumer confidence but continued modest growth in home prices (both Tuesday), the trend in capital goods orders to remain up but housing starts to fall 6% (both Wednesday). March quarter GDP data to show growth picking up to 1.2% annualised and the manufacturing ISM for April (Friday) to show a slight fall and continued solid rises in prices. Core PCE inflation for March (Thursday) is likely to have increased to 3.2%yoy. The US March quarter profit reporting season will continue.

Eurozone March quarter GDP data (Thursday) is expected to show growth of just 0.2%qoq slowing to 0.9%yoy. Inflation data for April (Thursday) is expected to show a further rise to 2.9%yoy due to rising energy costs but with core inflation falling to 2.2%yoy. Unemployment for March is expected to have remained at 6.2%.

Chinese business conditions PMIs (Thursday) for April are expected to remain around the 50.5 level.

In Australia, the focus will be back on inflation with the release of inflation data for both the March quarter and the month of March expected to show a further rise at the headline level. Thanks to a roughly 30% rise in fuel prices in March, the monthly CPI is expected to rise 1.6%mom or 5.1%yoy, from 3.7%yoy. The March quarter CPI won’t show the full impact as petrol prices only surged in March but will likely also accelerate to 1.5%qoq or 4.2%yoy, up from 3.6%yoy, as electricity prices surged in January with the end of government rebates and medical costs rose sharpy. Trimmed mean, or underlying inflation, will be more benign but still well above target at 3.5%yoy in the month of March and 0.9%qoq or 3.5%yoy in the March quarter. It’s too early for the much of the flow on of higher oil prices to show up in underlying inflation via fuel levies, higher fertiliser costs and higher costs for other materials derived from oil but this will show up in the months ahead, with the NAB and PMI business surveys confirming a sharp rise in cost and price pressures in March and April. With the surge in inflation threatening a further rise in inflation expectations and wages claims likely further pushing out the RBA’s expectations for when inflation will return to target we expect the RBA to hike rates again, probably at its May meeting. However, with a collapse in confidence pointing to a hit to growth we remain of the view that it will be a close call and put the probability of a hike versus a hold at 60/40.

Outlook for investment markets

Global and Australian share markets have likely seen the worst from the War and oil shock if the flow of oil quickly resumes but the risk of further falls taking us to a 15% top to bottom correction remains high given uncertainty around the peace talks and flow of ships through the Strait along with still stretched valuations, political uncertainty associated with Trump & the midterm elections and increasing worries about private credit and the impact of AI. However, returns should still be positive for the year as a whole thanks to Fed rate cuts likely later in the year, Trump still likely to pivot to consumer-friendly policies ahead of the midterms and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to around 3-5% due to poor affordability, RBA rate hikes and the hit to confidence from higher fuel prices and the War.

Cash and bank deposits are expected to provide returns around 4.25%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA hikes. Fair value for the $A is around $US0.72.

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.