Weekly market update

Investment markets and key developments

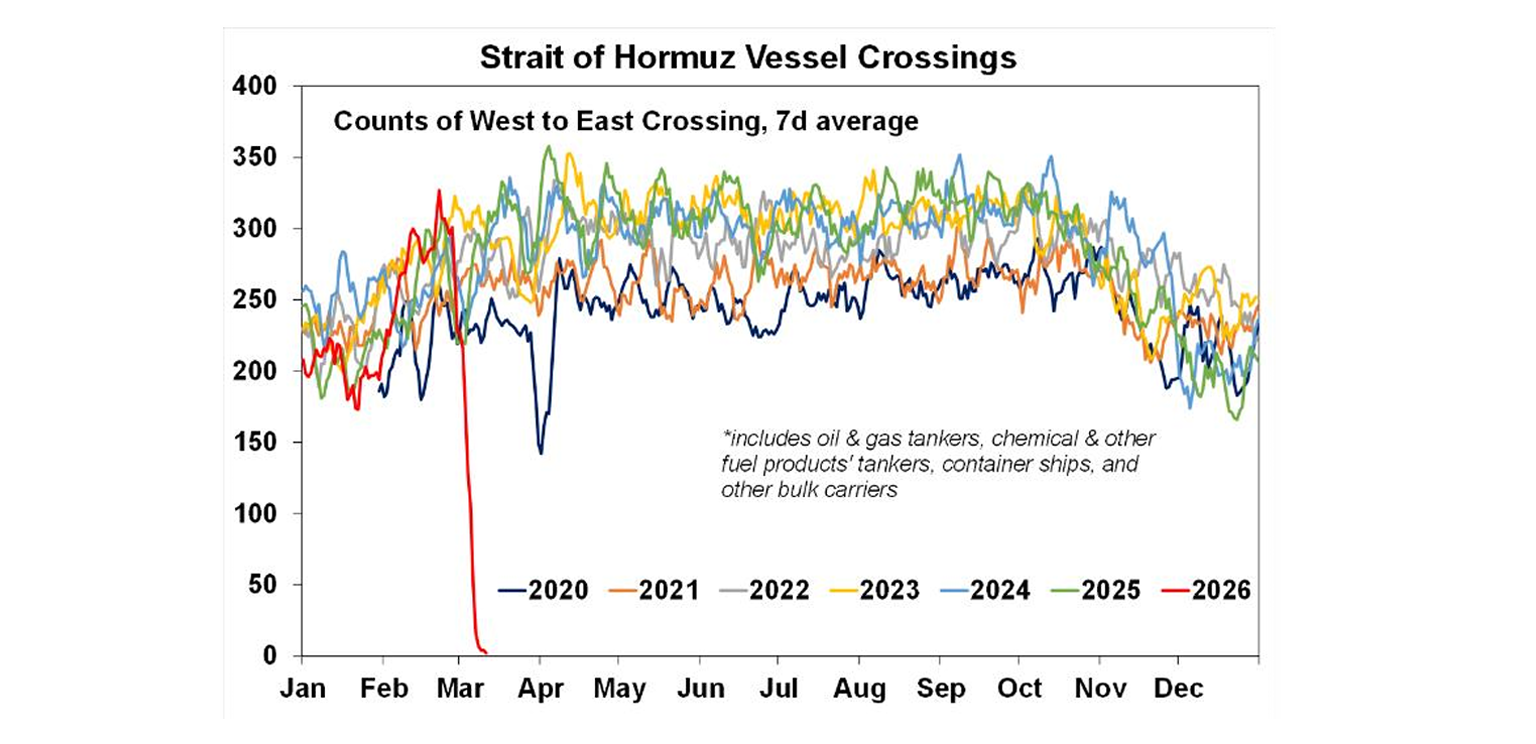

Global markets had a volatile week as the War with Iran continued with the Strait of Hormuz remaining effectively closed.

10 min read

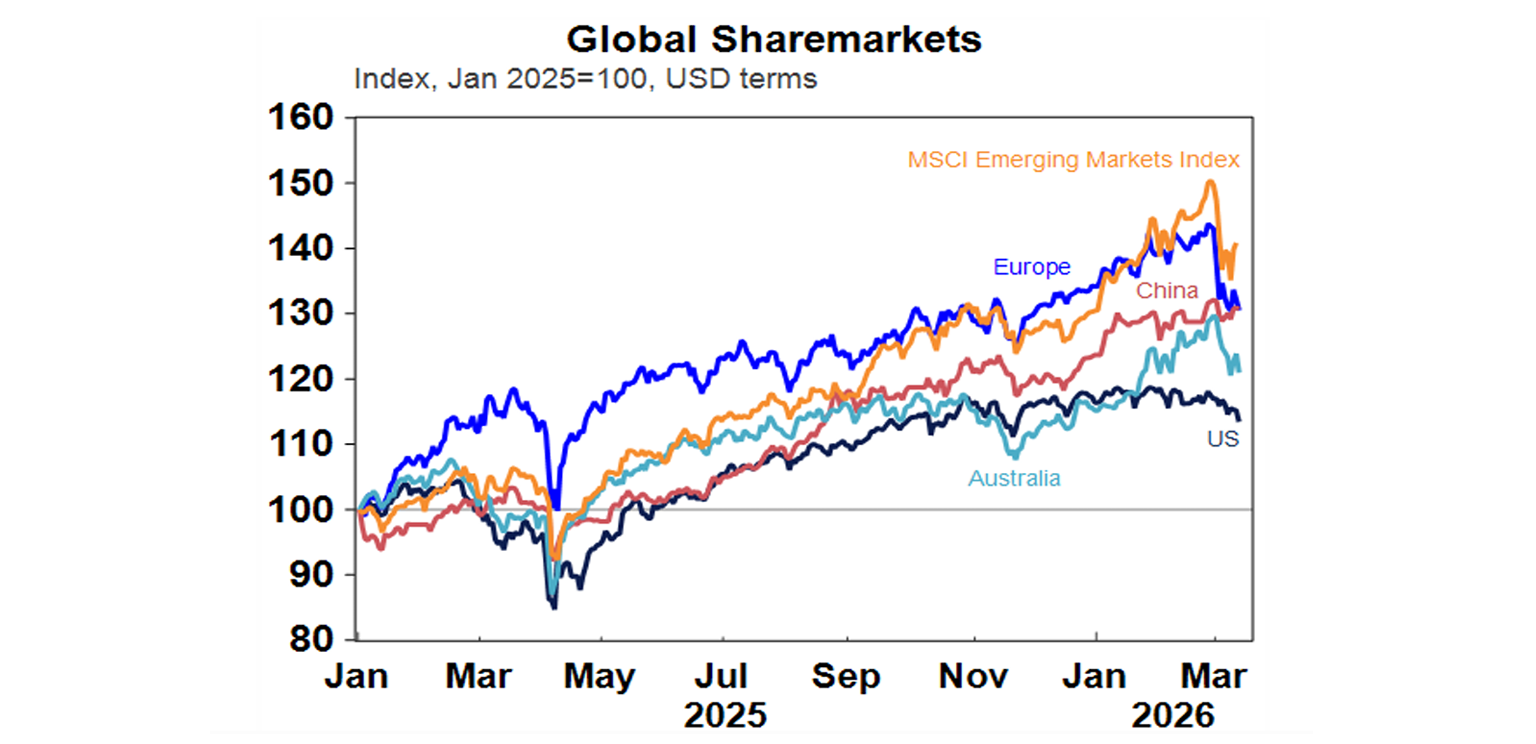

Global markets had a volatile week as the War with Iran continued with the Strait of Hormuz remaining effectively closed. Consequently, oil prices rose further, despite comments from President Trump earlier in the week that the war would soon be over. This in turn pushed bond yields up sharply on expectations for higher inflation and kept share markets under downwards pressure. For the week US shares fell 1.6%, Eurozone shares fell 0.1% and Japanese shares fell 3.2%, but Chinese shares rose 0.2%. Reflecting the worries about a boost to inflation and a hit to growth, ie stagflation, along with increased expectations for another RBA rate hike in the week ahead, the Australian share market fell another 2.6% with energy shares up but all other sectors down led by IT, health, property and materials. From this year’s highs US shares are down 5%, Eurozone shares are down 7%, Japanese shares are down 8.5% and Australian shares are down 6%.

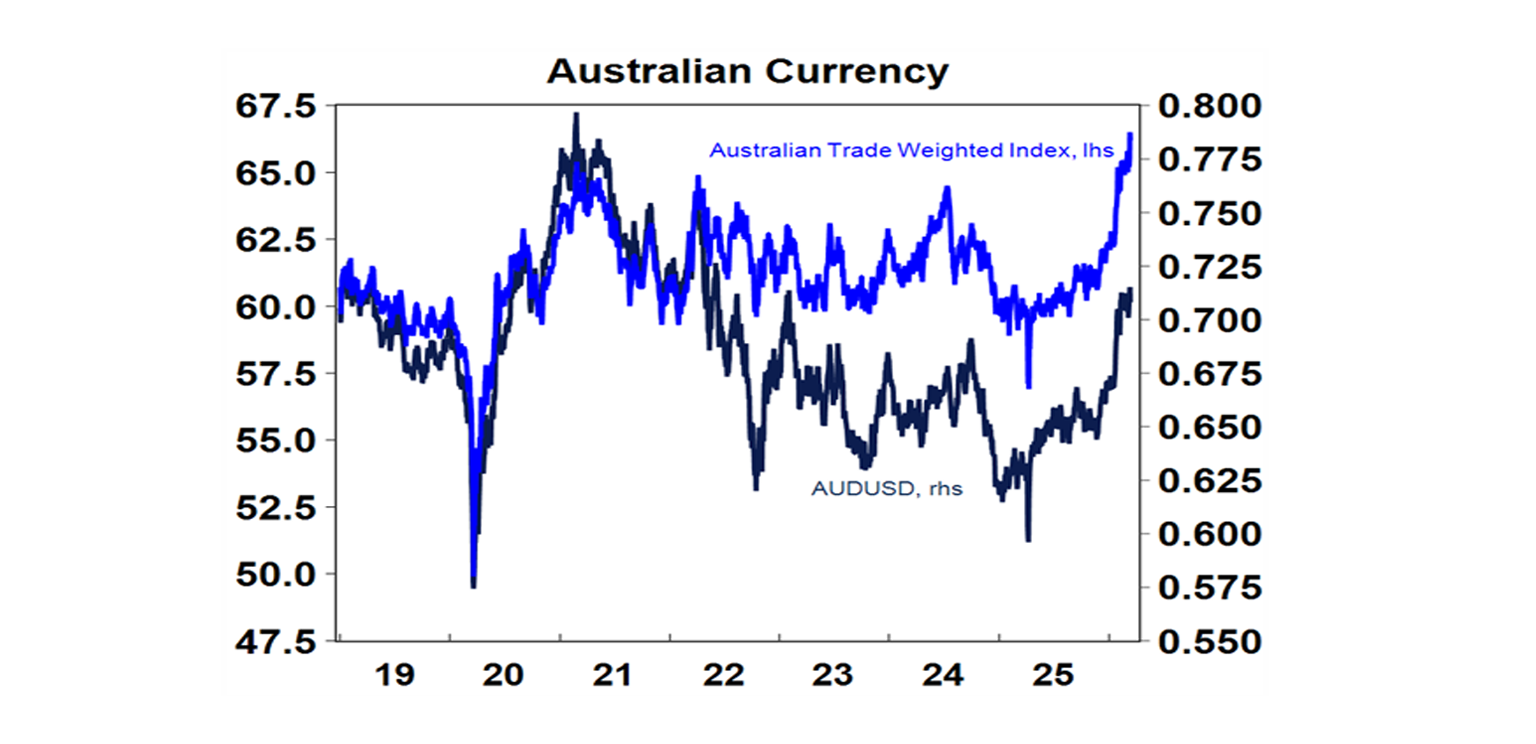

Gold fell slightly further over the last week – which is odd given the surge in geopolitical and inflation risk but could be a case of buy on the rumour and sell on the fact as a lot had already been factored into its price as it roughly doubled over the 12 months to its January high. By contrast Bitcoin continued to rise. Iron ore prices rose but metal prices fell. The $A fell slightly as the $US rose but it remains relatively resilient reflecting ongoing expectations for the RBA to hike rates this year and the Fed to cut, and it has remained strong on a trade weighted basis.

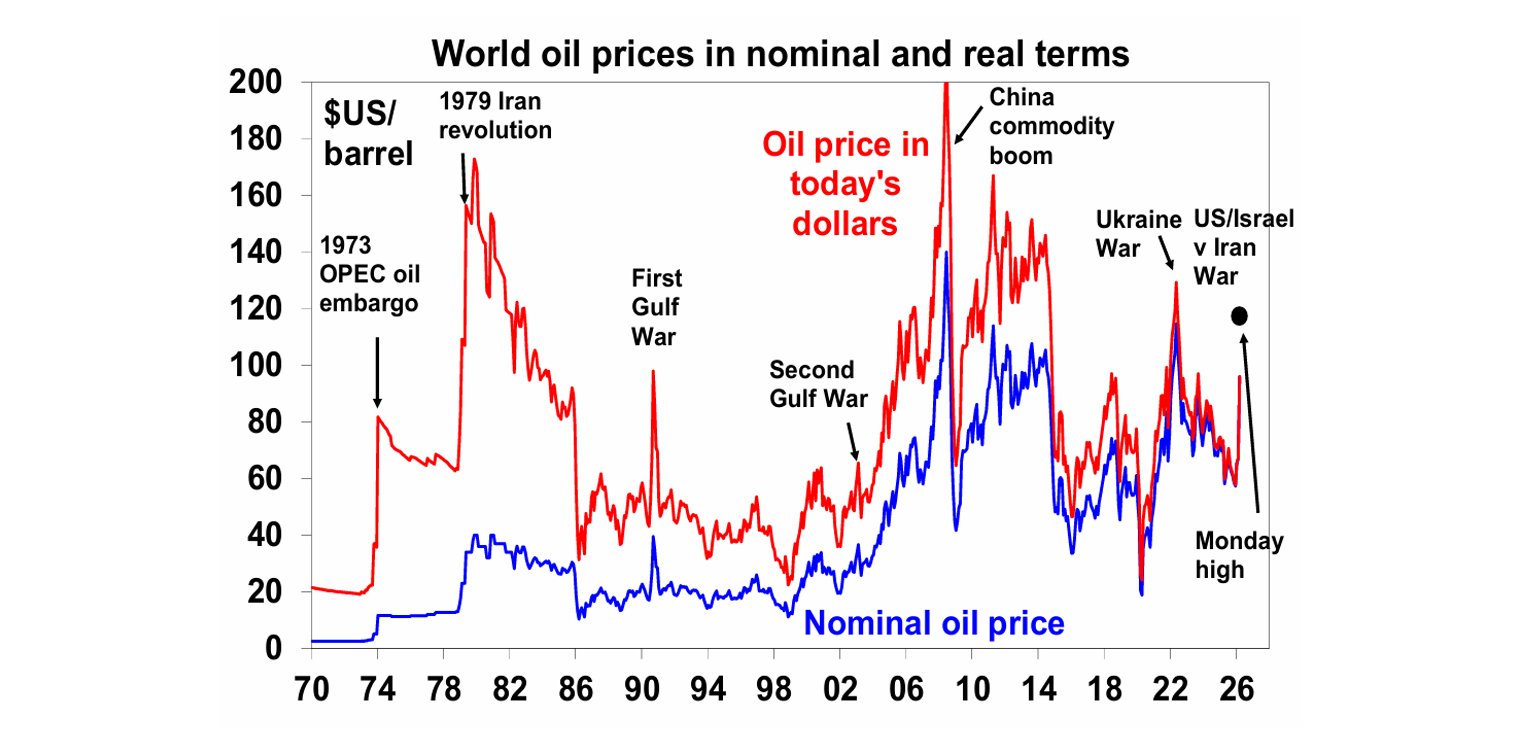

The past week highlighted the limits to TACO as the war with Iran continues and the Strait of Hormuz remains effectively closed. When markets started to panic on Monday with oil surging to $US119 a barrel and shares plunging Trump panicked too (surely, he must have expected the oil surge!) and declared that the War could be over “very soon” and that oil prices would plunge when it was. So, oil prices plunged and shares rebounded thinking a TACO (ie Trump chickening out) was here or near and that the crisis would soon be over. Unfortunately, oil has headed back up again and shares remain under pressure as its clear that the War has a way to go yet with Iran remaining defiant, attacking more energy infrastructure and ships in the Persian Gulf and Strait of Hormuz and warning of oil going to $US200 a barrel. So, Trump has no easy off ramp.

The bottom line is that TACO can work well when Trump has full control – like he did in relation to the tariffs last year. But that’s not the case right now with Iran refusing to play ball. In fact, it wants to see Trump pay a big economic and political cost and the best way to do this is to keep the Strait of Hormuz effectively closed to shipping. That is taking out around 15 million barrels a day of global oil supplies (which is around 15% and its similar or more for gas). And the longer the Strait stays effectively closed the more oil prices will trend up as inventories run down. Don’t forget the second oil crisis in 1979 on the back of the Iranian revolution saw a threefold rise in world oil prices but that only involved a hit to 5% of global oil supplies.

In the absence of securing the Strait of Hormuz most policy options to stop oil prices rising are band aid solutions. The release 400 million barrels of oil by IEA member countries, of which 172 million will come from the US, is to be welcomed. But it will only be released gradually and if its anything like the US release over 120 days it will at best only amount to 3.3 million barrels a day which will only cover 20% or so of the 15 million barrels a day of lost supply from the Persian Gulf. Easing sanctions on Russia would help but that might provide only another 1.5 million barrels a day, and that comes with all sorts of issues given its war with Ukraine. Trump has indicated the US can provide insurance and naval escorts for ships through the Strait but that was over a week ago and both ideas have huge challenges. The US Energy Secretary said the US Navy could start escorting tankers by the end of March..but that is still a few weeks away and sounds very iffy (like his claim that it had already escorted a ship). So the bottom line is that regardless of what Trump says the War likely has a way to go yet.

That said, Trump is under big political pressure to keep the conflict short and avoid troops on the ground and Iran’s military capability is being rapidly degraded. And while Iran will want to keep the Strait closed for as long as possible its ability to do so will decline over time as a result of US actions to degrade its capabilities and as other countries combine to force it open possibly assisting the US militarily to do so. There are also signs that Iran is making exceptions for ships from China and India to pass through which may eventually allow some other countries to piggy back to some degree (by eg flagging their ships as Chinese). So, while it’s looking more shaky, our base case remains that the War is limited. Our two scenarios are:

Limited war (55% probability, lowered from 60%) - our base case is that the War is still ultimately limited with Trump likely finding a way to declare victory sometime in the weeks ahead. This may still take a few more weeks so oil prices could still go a lot higher to say $US150 (seeing further falls in shares, possibly taking us to the 15% correction we have been expecting this year), before they go lower (shares higher). Along with providing a “wag the dog” distraction from the Epstein files, its probable that Trump’s intervention in Venezuela and War on Iran is partly motivated by a desire to get the upper hand over China and so the US is probably aiming to have the War nearer to being wrapped up by the Trump-Xi meeting at the end of the month. However, with Iran digging in and it looking increasingly like Trump has miscalculated we have cut the probability of a limited war to 55%.

Long war (45% probability, up from 40%) – however, while Trump may want to declare victory soon, Iran has an incentive to prolong the surge in oil prices and hence the cost to Trump and US consumers. Iran could also descend into chaos with various military groups continuing to threaten ships in the Strait of Hormuz even if Iran officially waves the white flag. This could necessitate a longer-term US involvement and mean a much longer disruption to oil supplies, conceivably resulting in oil prices going to $US200 & beyond driving a sharp sustained fall in global and Australian shares into a bear market. It would be a political disaster for Trump though and lead to a significant loss of confidence in the US – much as occurred in the 1970s!

The key things to watch for will be a sustained fall in missiles & drones coming from Iran, successful shipping through the Strait of Hormuz, indications Iran wants to negotiate and a 10% or more top to bottom fall in US shares which will up pressure on Trump to find a way out.

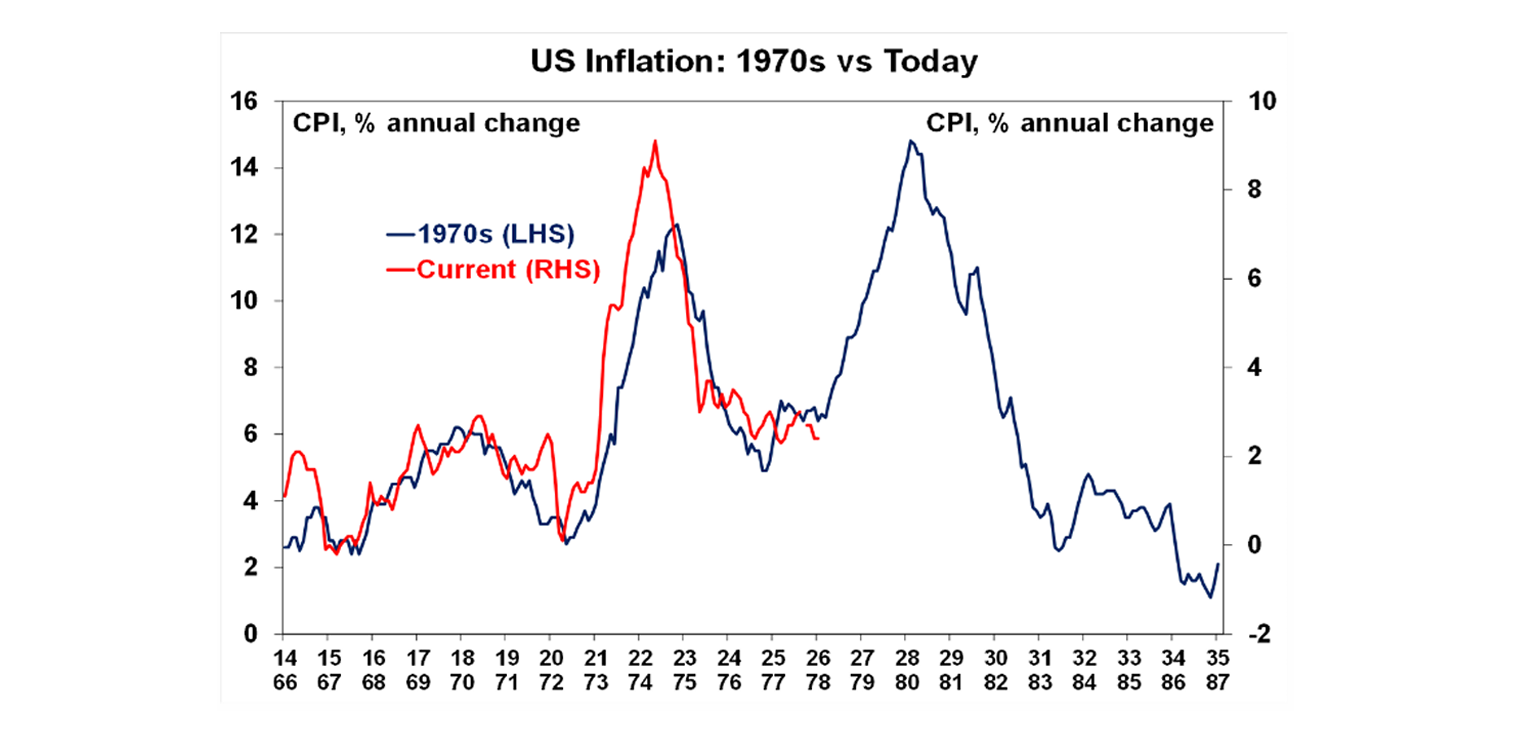

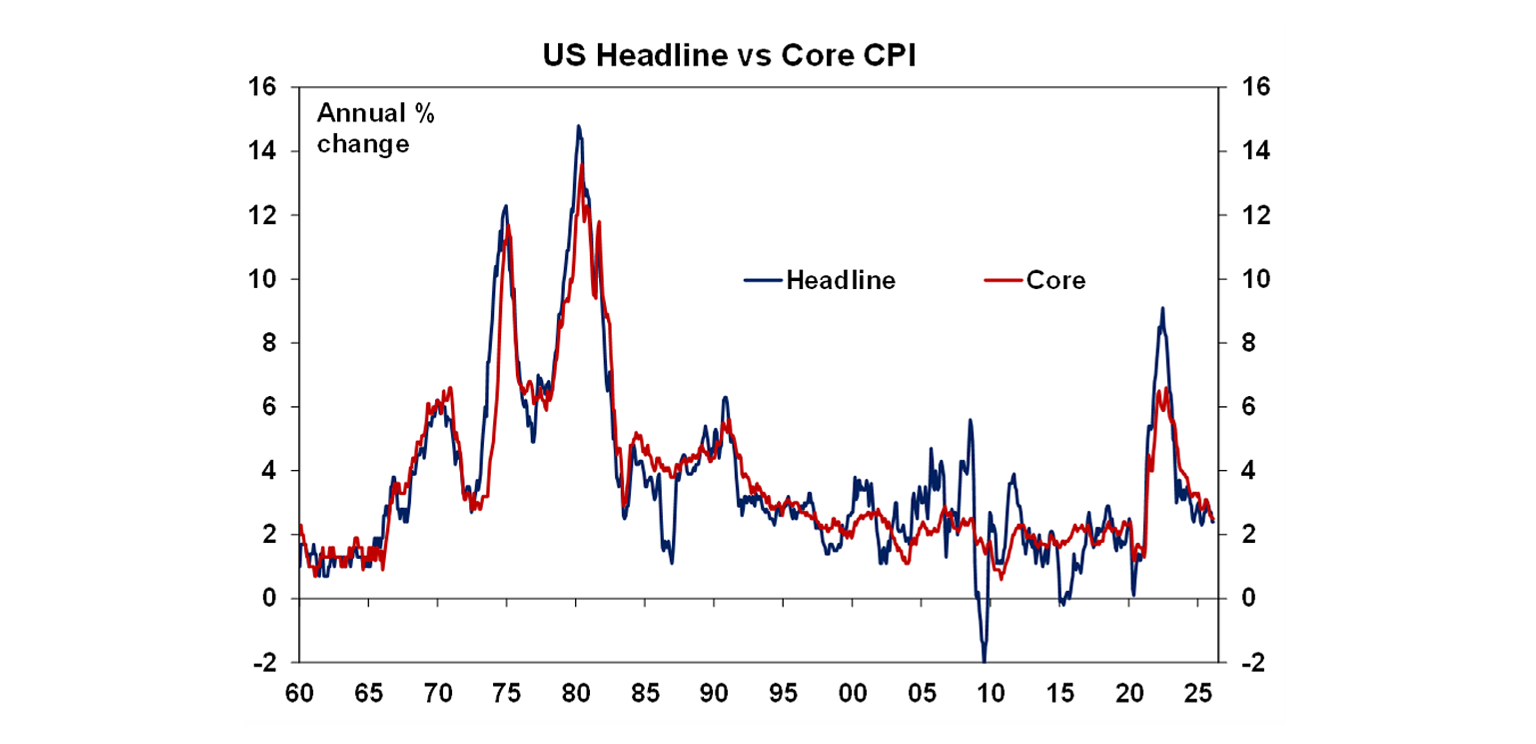

Longer term implications of the Iran war – more renewables and onshoring of supply chains. Like the pandemic, the Iran War and the impact on oil supplies will have longer term consequences including more pipelines to bypass the Strait of Hormuz, an accelerated push towards EVs, renewables and nuclear power, and even more pressure on countries to bring supply chains of strategic products back onshore. All of which is positive for metal demand. But the further hit to globalisation will potentially make the world even more inflation prone. No doubt many have seen the chart below before (in 2022 it was all the rage.) Could the US and global economy face another inflation wave as the chart implies – reflecting deglobalisation, weakening Fed independence and higher energy prices? It’s a bit odd that Iran figured back then in the third inflation wave and is figuring again now.

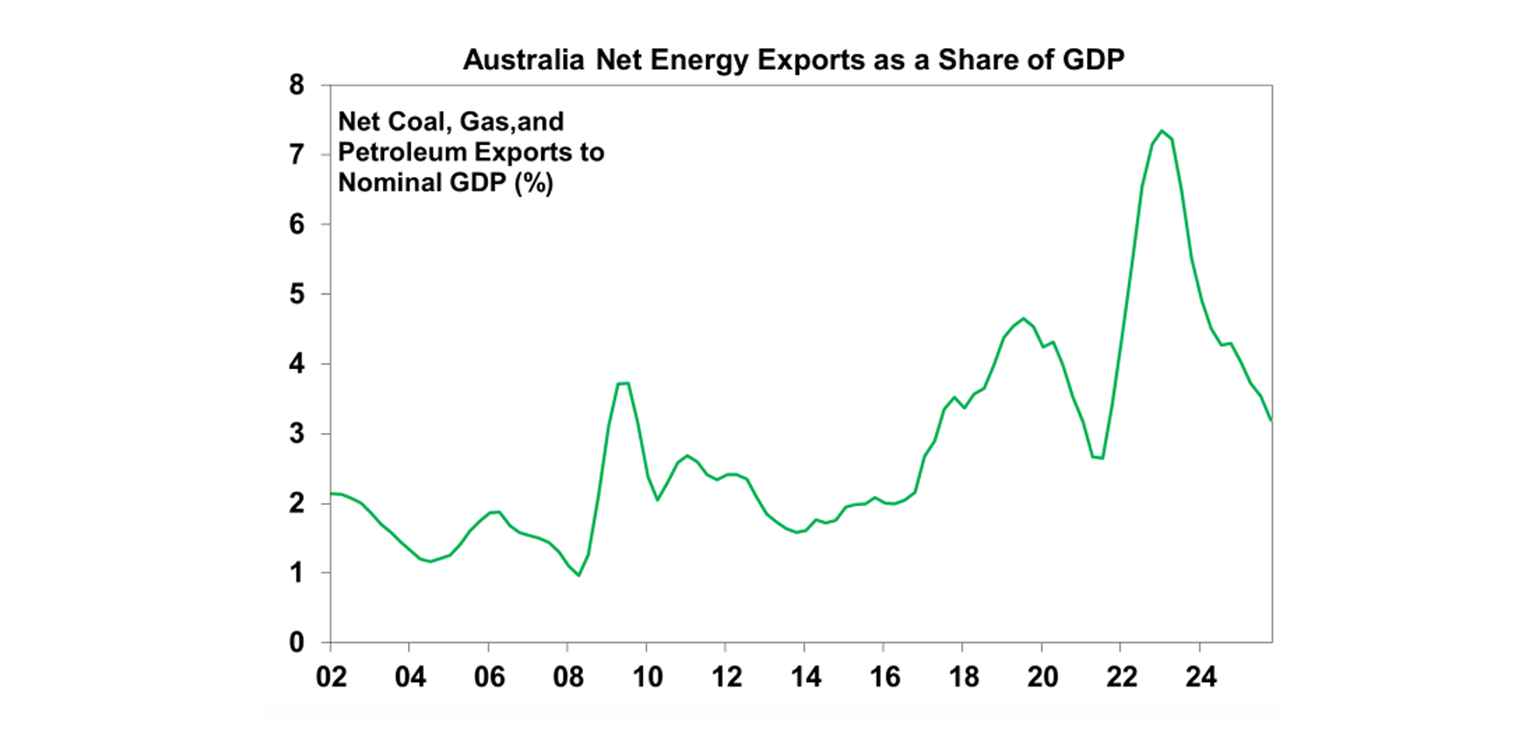

Australia is in a relatively good position but is very vulnerable if oil supplies are threatened for a lengthy period. While Australia is a net oil importer it’s a net energy exporter and so will benefit from higher prices for gas and maybe coal as we saw in 2022. This in turn will boost national income (and may provide some small boost to the Federal Government’s budget. By contrast most countries in Asia and Europe and net energy importers.

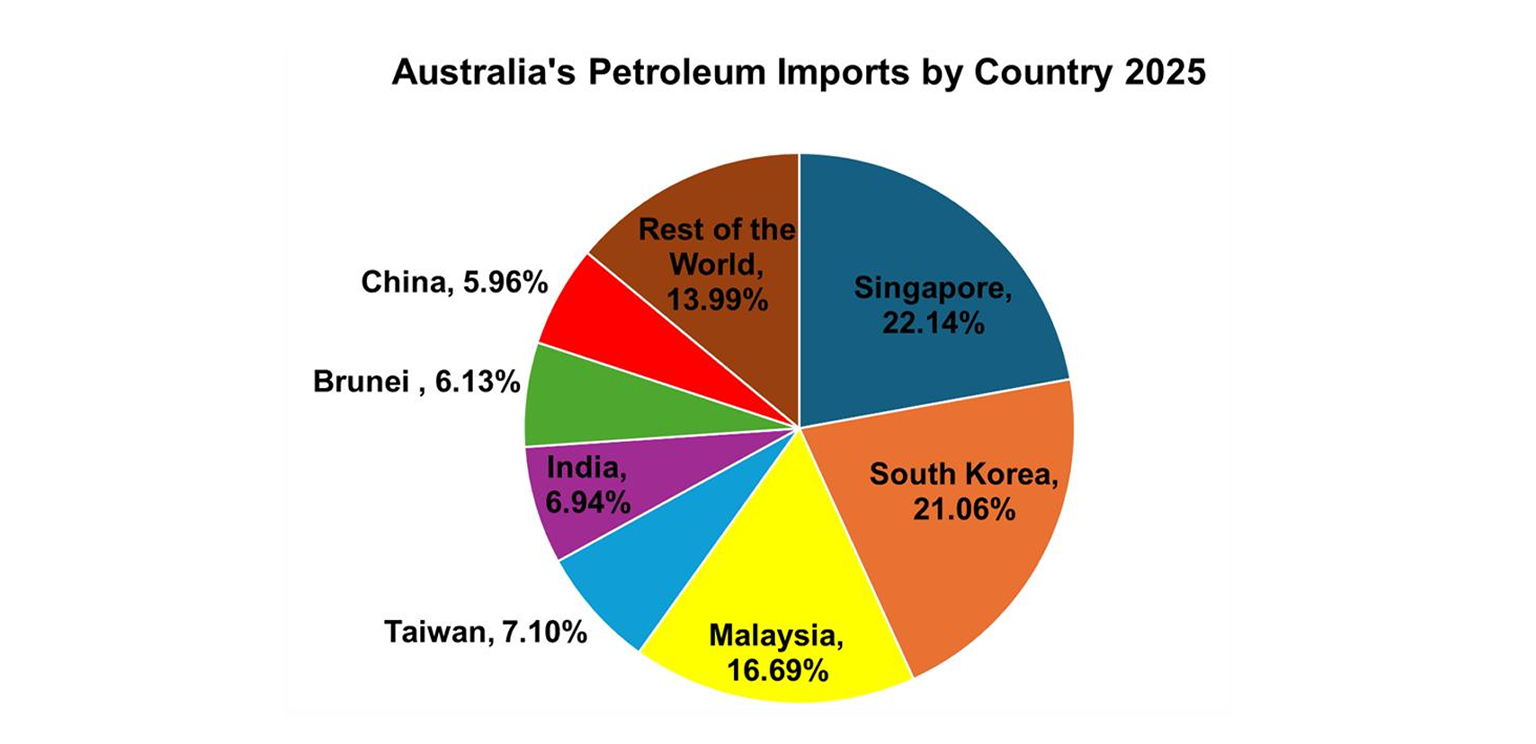

But Australia will be really vulnerable if the hit to oil supply continues beyond a month or two. In the 1980s, 90 to 100% of our oil consumption was sourced in Australia and it was mostly refined here. However, that has now fallen to around 20% for crude oil (as the Bass Strait field matured) and to 10 to 20% for refined products (as refineries closed). Of the 80-90% of refined product that is imported most of that comes from Asia (see the next chart) and most of the crude for that comes from the Middle East. The risk is that several of those Asian countries ban exports as their own oil supplies run down – and China has recently announced that. Then the focus will shift from the War being an inflation shock to an output shock for net oil importers like Australia. Of course, there is a way to go before we get to that and Australia does have reserves it can dip into - for about a month! (The IEA recommendation is to have 90 days of reserves, and we are way below that.) In the 1980s this would not have been an issue! So it turns out Australia didn’t have so much to worry about in the time of the original Mad Max films after all!

Given all the uncertainty we think the RBA should leave rates on hold at its meeting on Tuesday. We continue to see trimmed mean inflation falling a bit faster than the RBA is forecasting, recent data on consumer spending has been softer than expected with the CBA’s household spending indicator even falling in February, surging petrol prices will act as a dampener on consumer spending and it makes sense to wait for at least some of the dust to settle from the Iran war because it could end in a month making any boost to inflation from higher petrol prices a short term blip. So we think it makes more sense to wait till May before deciding what to do on rates, but to continue to sound hawkish in the interim.

However, we now think the RBA will hike on Tuesday. Since the last meeting stronger than expected growth and jobs data appear to have reinforced RBA concerns about capacity constraints and the Bank appears very concerned the boost to inflation from the war’s impact on oil prices (which at current petrol prices will add 1% to inflation taking it to around 5%) will add to inflation expectations – which were already on the rise again - making it even harder to get inflation back down. This has been reinforced by hawkish comments since the war started by both the Governor and Deputy Governor suggesting that they are inclined to act quickly to be more confident of getting inflation back down. As such, and while it’s a close call, we are now expecting another 0.25% hike in the cash rate to 4.1% on Tuesday. And we expect the post meeting statement and commentary to remain hawkish.

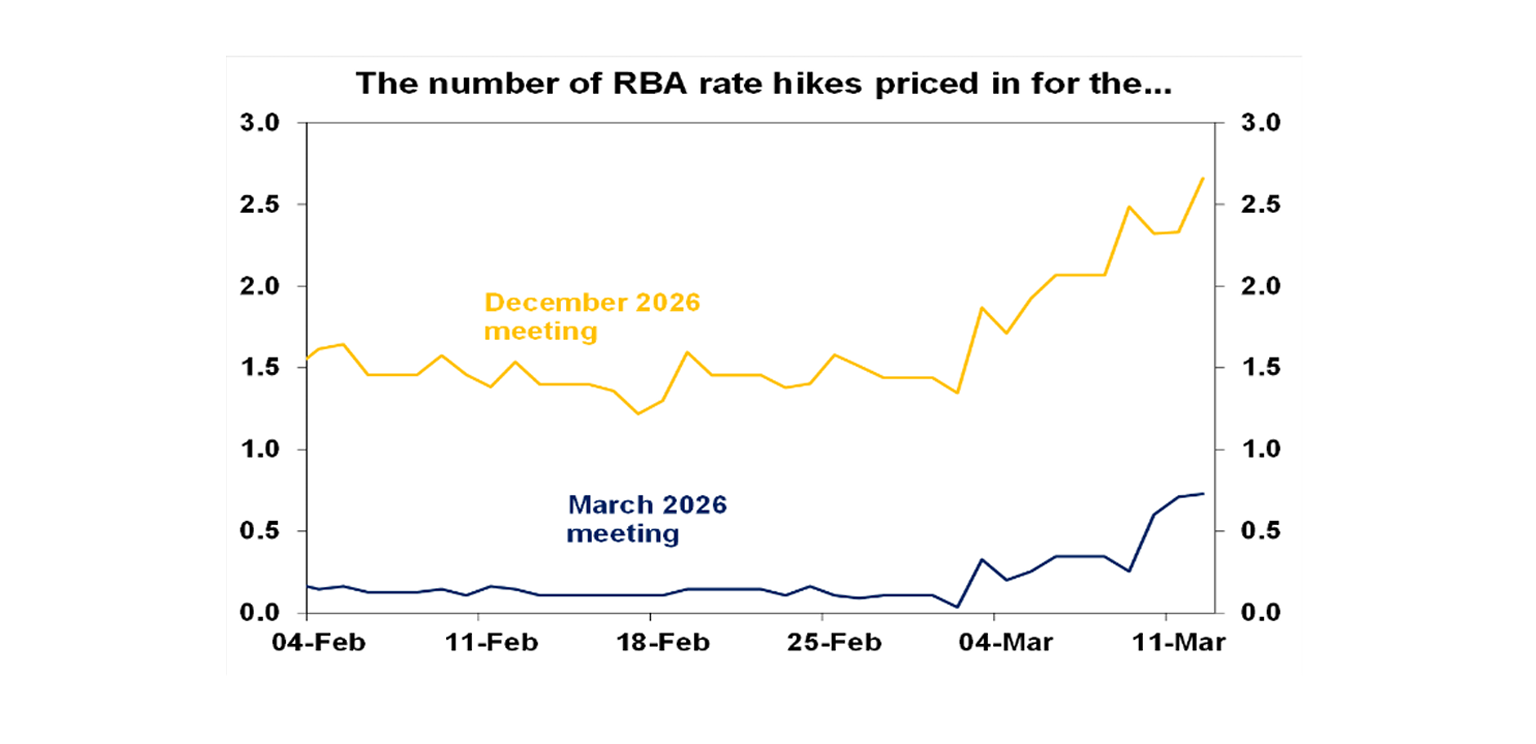

The money market has around a 66% chance of a rate hike priced in for Tuesday and nearly three hikes priced in by year end. This looks a bit overdone, and we reckon its closer to 52% chance of a hike on Tuesday.

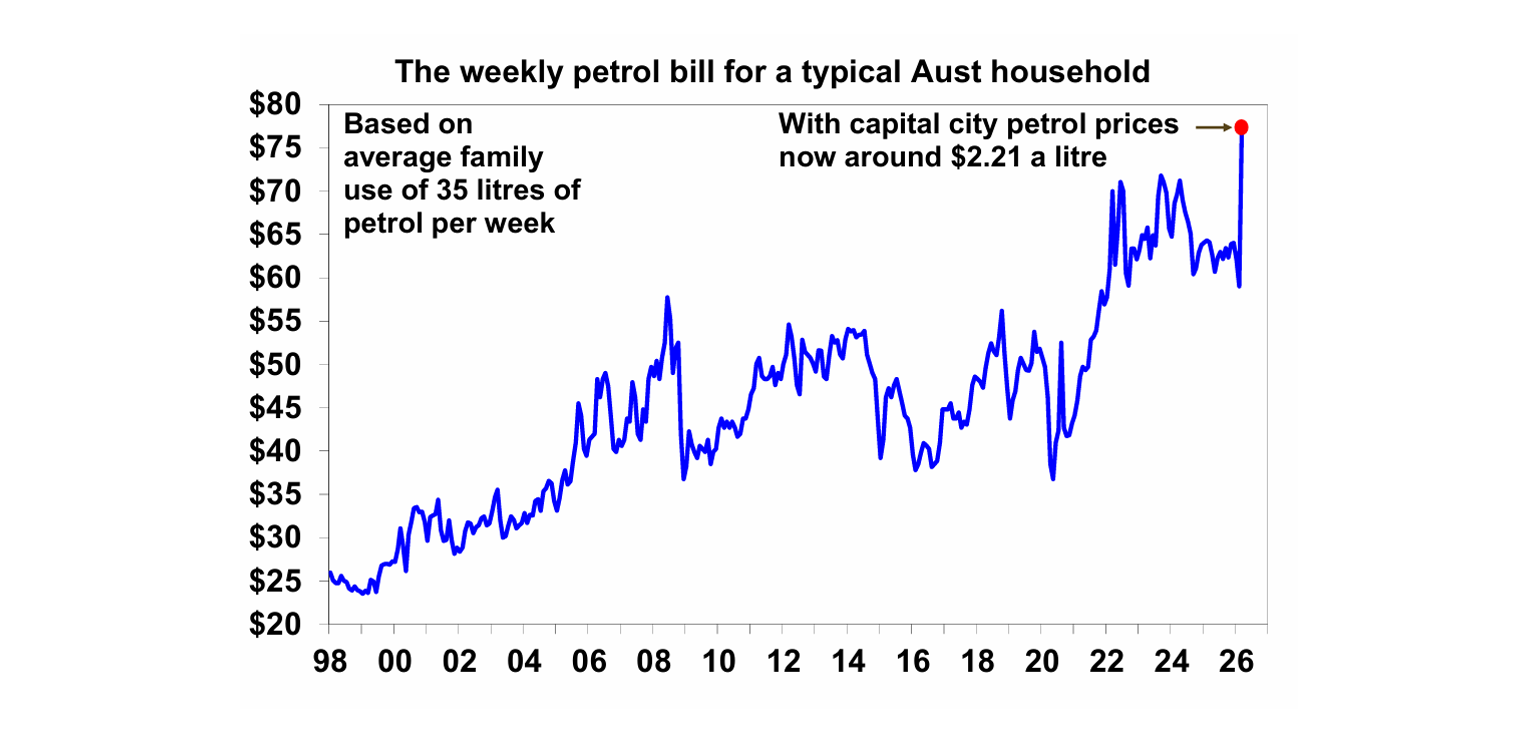

A potential double whammy hit for households. For mortgage holders another 0.25% rate hike would mean roughly an extra $110 a month in mortgage interest payments. If petrol prices stay at current levels, it will cost the average household around an extra $78 a month versus their February average. So nearly a $190 a month extra impost for those with an average mortgage and a car that’s not electric, which is quite a hit!

Major global economic events and implications

US data was mostly soft. December quarter GDP growth was revised down to just 0.7% annualised from 1.4%, with weaker consumer spending and trade. January real personal spending rose just 0.1%mom. Underlying capital goods orders were flat in January. Consumer sentiment fell, with weaker responses later in the survey period due to the War. Small business optimism fell slightly and remains around long term average levels. Housing starts rose strongly, but this was driven by volatile unit approvals and building permits and existing home sales fell and remain soft suggesting that the housing sector remains weak. Labour market data was okay though with jobless claims remaining low and job openings up in January and quits little changed.

On the inflation front the news was in line with expectations. The February CPI showed core inflation unchanged at 2.5%yoy. The complication is that because of different weights, the components imply another solid increase in the core private final consumption deflator for February of 0.4%mom which will leave the annual rate at 3.1%yoy as it was in January. And of course, March headline inflation data will show a spike due to higher gasoline prices. All of which will keep the Fed on hold next week.

US tariffs are out of the headlines – but Trump’s Plan B looks to be progressing, albeit with some threats. The processing of refunds of the illegal emergency power tariffs of around $US166bn is now underway. The 10%, possibly 15%, general tariff under Section 122 is now in place – but is being challenged in court. These tariffs will expire in July though and Section 301 investigations are now underway against China, Europe, Japan and 13 other countries with the likely outcome that the end result will be similar to the tariffs that prevailed prior to the Supreme Court striking down the reciprocal tariffs. This group does not include Australia, but it is included in a wider group of 60 countries subject to 301 reviews focussed on a failure to enforce bans on forced labour.

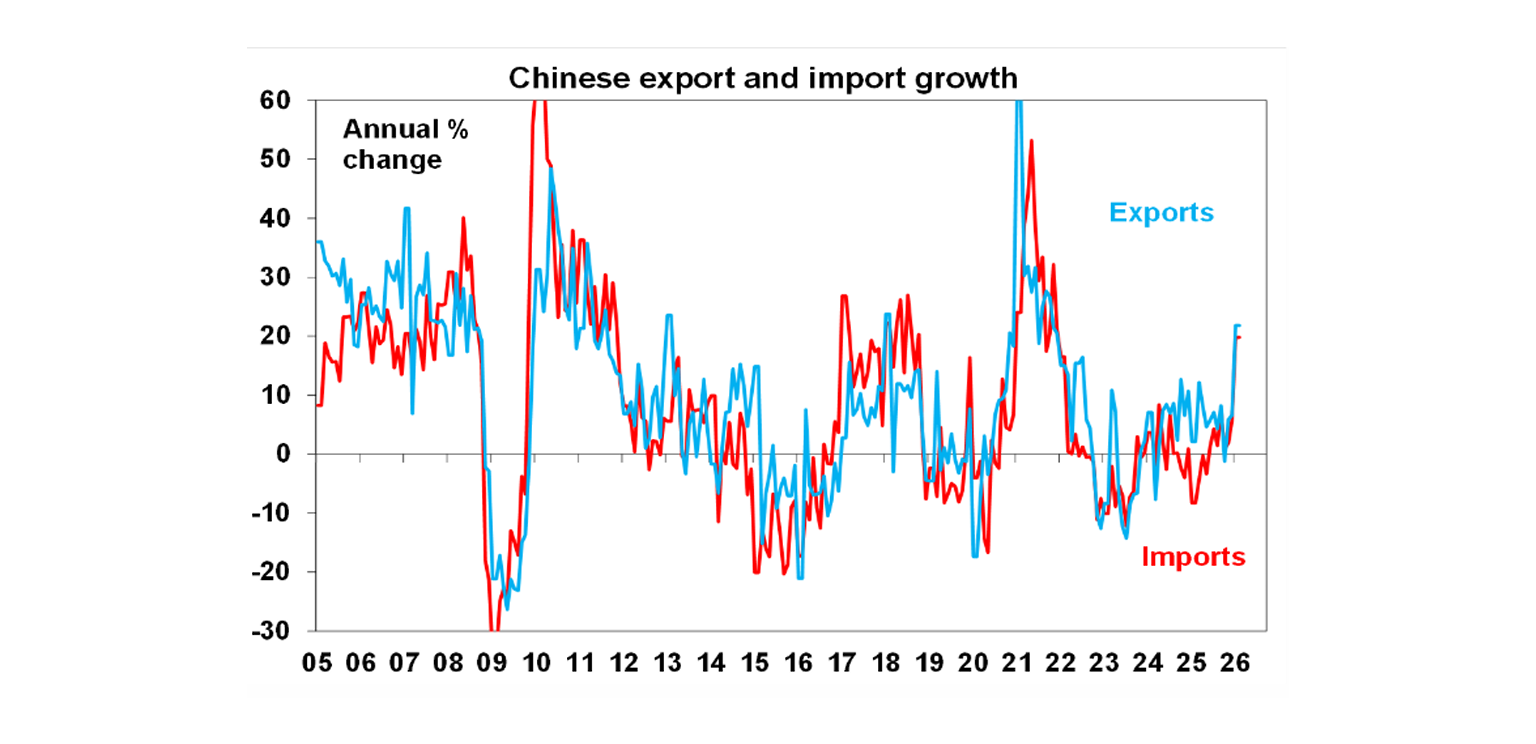

Chinese export and import growth boomed in January/February but it’s hard to see it being sustained at 20%yoy. Exports to the US were down 11%yoy, but they are up to other regions. Total credit growth remained at 8.2%yoy in February.

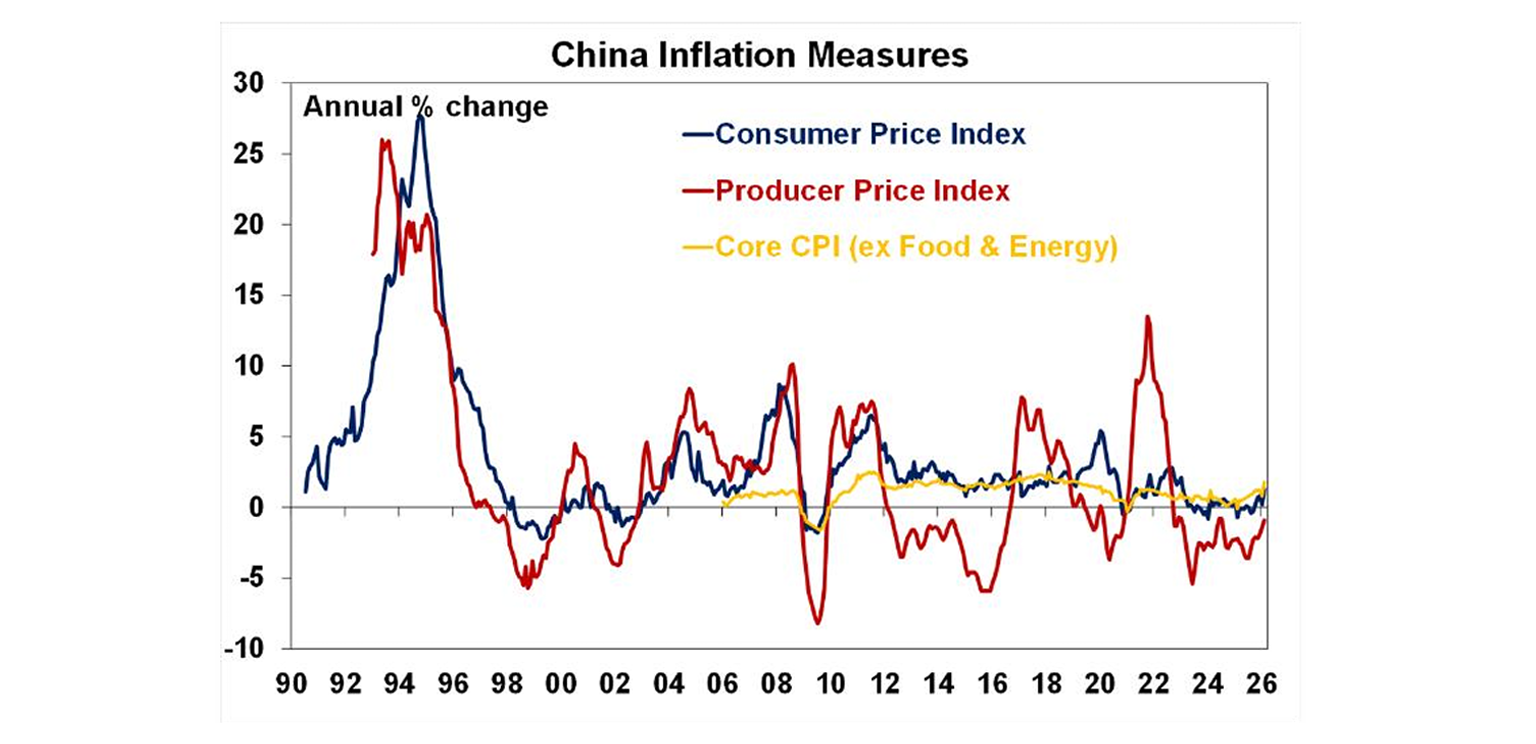

Chinese inflation also perked up in February, but this appears to be due to the late Lunar New Year boosting prices this February versus a year ago. It does appear that deflationary pressures are starting to ease though.

Australian economic events and implications

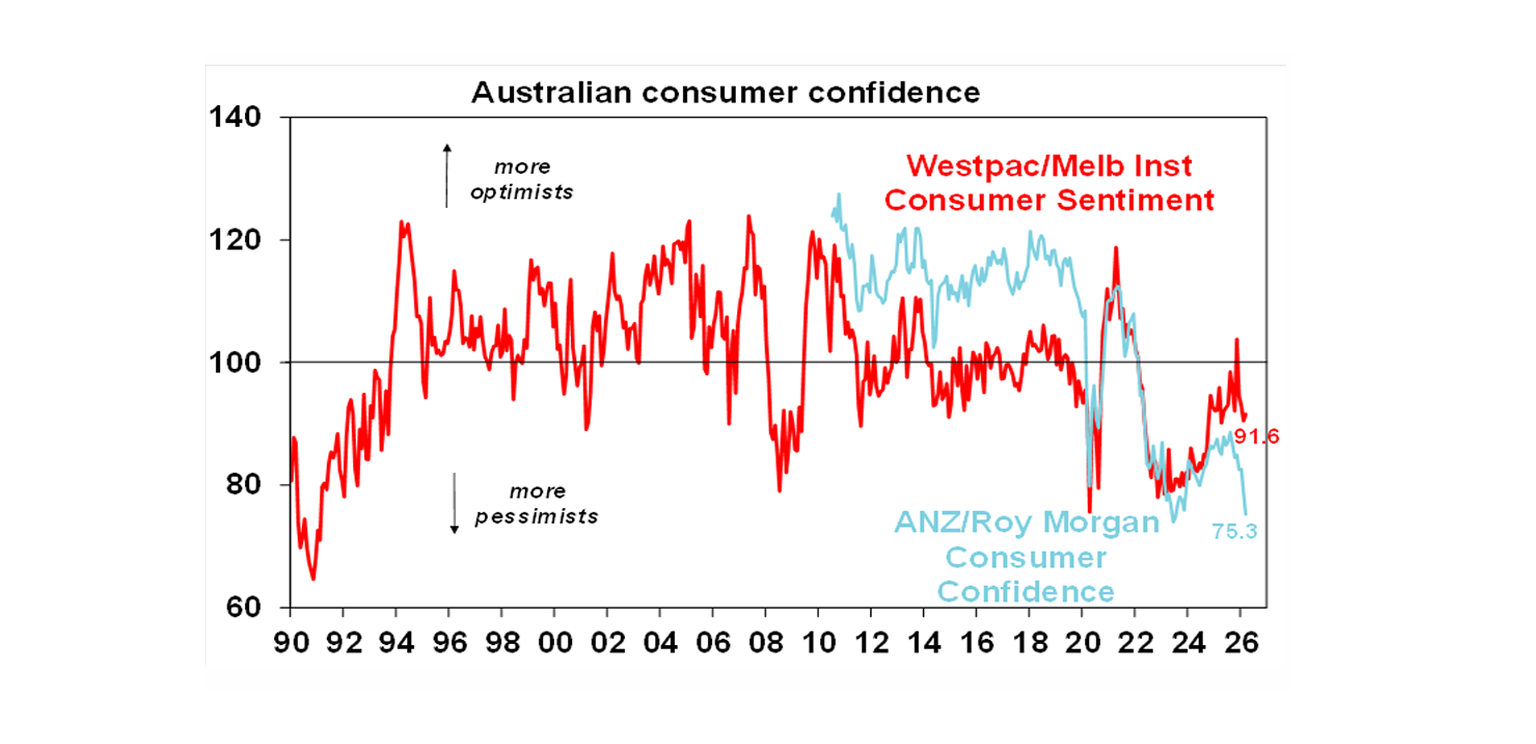

The Iran War has hit consumer confidence. While the Westpac/Melbourne Institute’s consumer confidence index rose 1.2% in March, survey responses in the latter part of last week as the Iran war intensified showed a sharp 7% fall and the alternative ANZ/Roy Morgan index fell another 4% taking it back to around its 2023 lows. This does not augur well for growth in consumer spending.

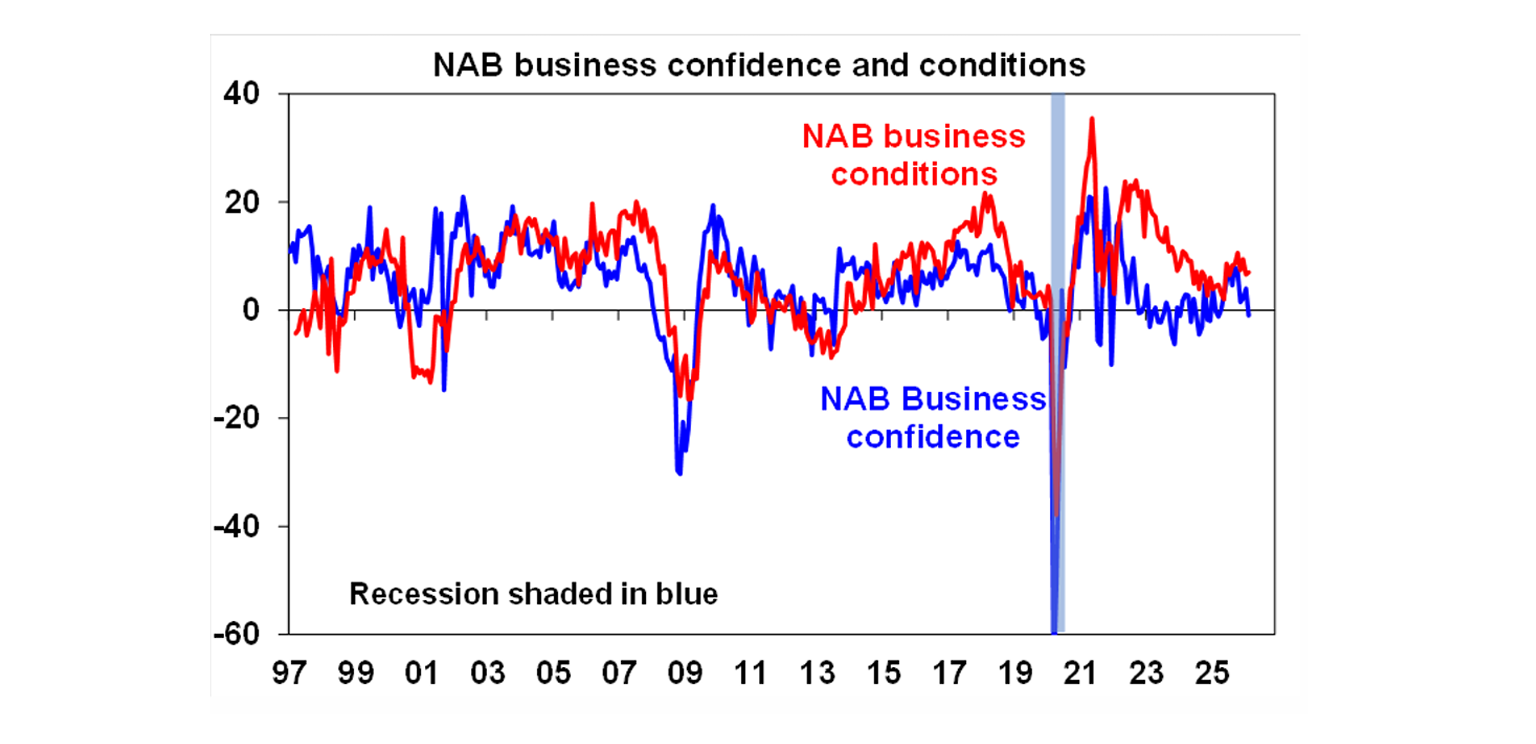

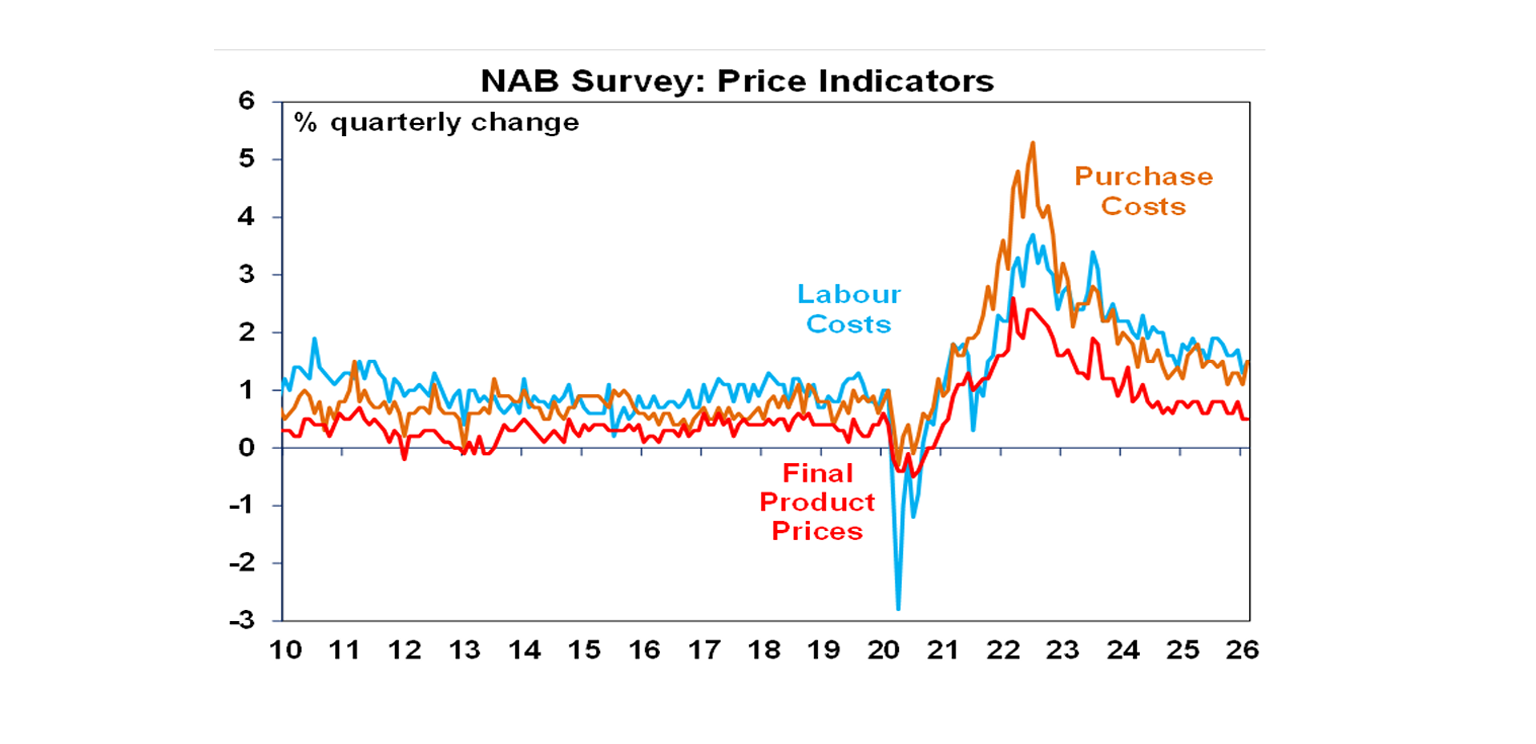

Australian business conditions remained around okay levels in the latest NAB business survey but confidence fell and this survey was in February, before the Iran war started.

The NAB survey showed mixed price pressures with labour and purchase costs up but the price of final products remaining subdued at 0.5%qoq or 2% annualised. This maintains confidence that the spike in inflation seen in the last half of last year could prove to be an aberration, but the NAB survey may be understating services inflation.

What to watch over the next week?

Apart from the War with Iran which will remain the main focus for investors, 8 major developed country central banks will meet in the week ahead. All are expected to indicate uncertainty regarding the implications of the war with Iran and its flow on to oil prices.

In the US the Fed (Wednesday) is expected to leave rates on hold at 3.5-3.75% after cutting rates three times last year as growth remains solid and core private final consumption inflation is still around 3%yoy. It’s dot plot of Fed officials’ interest rate expectations is expected to continue to allow for one cut this year and one next year. Powell is likely to express comfort with the current level of interest rates and indicate that it can afford to wait to see what happens to inflation. On the data front expect a small rise in industrial production for February (Monday) and March regional manufacturing indexes to show reasonable conditions.

The Bank of Canada (Wednesday) is expected to leave rates on hold at 2.25% with inflation (Monday) for February expected to show core inflation around 2.4%yoy.

The European Central Bank, Bank of England and the Swiss and Swedish central banks are also expected to leave interest rates on hold at 2%, 3.75%, zero and 1.75% respectively. The BoE is likely to lean dovish, and the ECB is likely to indicate a slight bias to raising rates in response to the inflationary impact of the Iran war.

The Bank of Japan (Thursday) is also expected to leave rates on hold at 0.75% and maintain a tightening bias.

Chinese economic activity data for January and February (Monday) is expected to show continued soft growth with retail sales slowing to 2.1%yoy and industrial production slowing to 5%yoy.

In Australia, the RBA (Tuesday) is expected to raise rates by 0.25% taking the cash rate to 4.1% reflecting concerns about the impact of a boost to headline inflation and inflation expectations from higher petrol prices on the back of the War with Iran at a time when inflation is already above target. It’s also expected to remain relatively hawkish. February jobs data (Thursday) is expected to show a 25,000 rise in employment but a slight rise in unemployment to 4.2%. The RBA’s Financial Stability Review (Thursday) will be watched for any assessment the RBA provides regarding the threat posed by the Iran war oil shock and the vulnerability of the household sector to rising rates.

Outlook for investment markets

Global and Australian share markets are at high risk of further falls in the near term in response to the War with Iran against the backdrop of stretched valuations, political uncertainty associated with Trump & the midterm elections and AI bubble & tech valuation worries. We continue to see a 15% or so top to bottom fall in share markets along the way this year. However, returns should still be positive for the year as a whole thanks to Fed rate cuts, Trump’s consumer friendly pivot ahead of the midterms and solid profit growth.

Bonds are likely to provide returns around running yield.

Unlisted commercial property returns are likely to be solid helped by strong demand for industrial property associated with data centres.

Australian home price growth is likely to slow to 5% or less due to poor affordability and the RBA raising rates with talk of more to come.

Cash and bank deposits are expected to provide returns around 4%.

The $A is likely to rise as the interest rate differential in favour of Australia widens as the Fed cuts and the RBA holds or hikes. Fair value for the $A is around $US0.72.

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.