The RBA hikes again to control inflation – lessons learned from the 1970s

The RBA’s decision to hike rates to 4.35% was no surprise with it being about 75% factored in by the money market and 21 of the 22 economists surveyed by Bloomberg expecting a hike.

6 min read

Key points

The RBA hiked its cash rate for the third time this year by another 0.25% to 4.35% in response to inflation running above target and concerns that it will likely remain so for longer given price pressures partly flowing from the War with Iran, threatening higher inflation expectations.

The key lesson from the 1970s is that the RBA is right to be focussing first on getting inflation back to target – as it will avoid even more pain down the track.

We are allowing for a further rate hike in August, but the longer the Strait of Hormuz remains blocked the greater the risk of recession allowing a return to rate cuts next year.

The best things the Government can do in the Budget to help alleviate underlying inflation pressures is to lower the level of public spending and boost productivity.

The RBA hikes to 4.35%

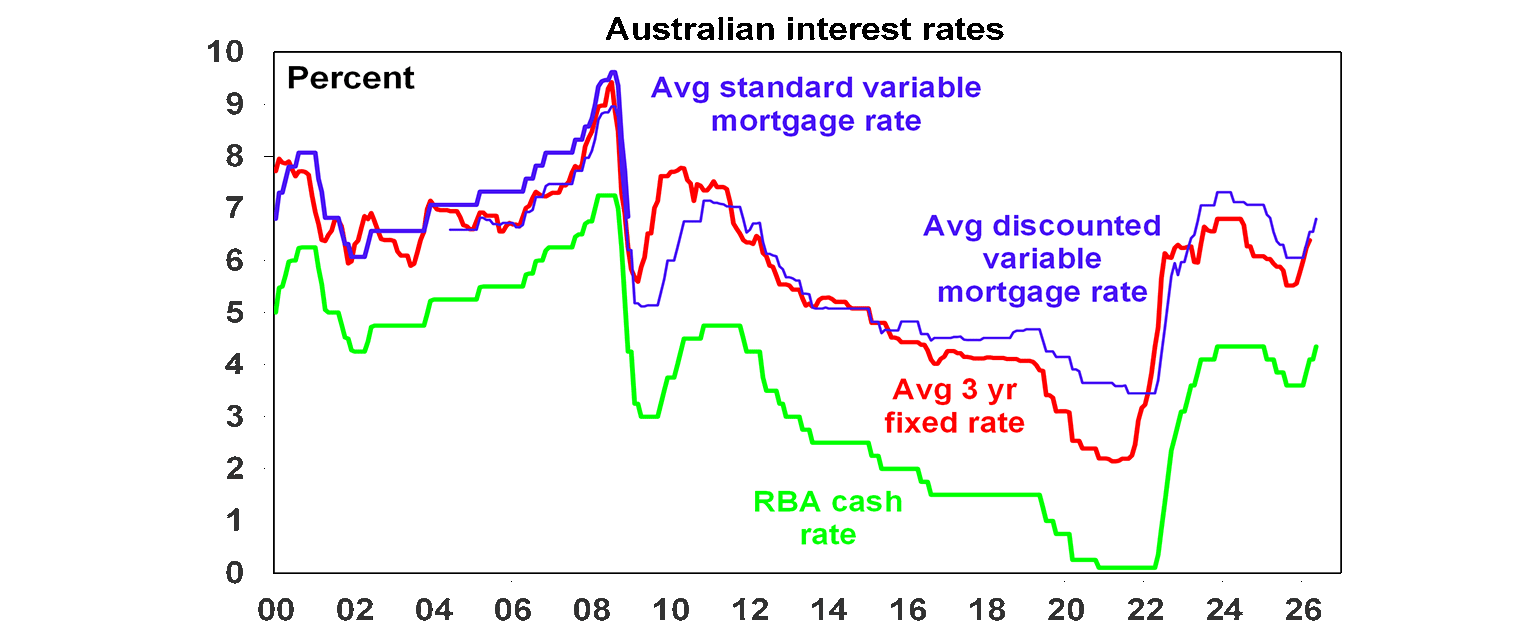

The RBA’s decision to hike rates to 4.35% was no surprise with it being about 75% factored in by the money market and 21 of the 22 economists surveyed by Bloomberg expecting a hike. The decision means that the RBA has now reversed all of the three rate cuts we saw last year, which followed 13 rate hikes in 2022 and 2023. Once passed on to mortgage holders it will leave mortgage rates around levels prevailing in late 2011. For a mortgage holder with an average $660 mortgage this will mean an extra $110 a month in mortgage payments or $1300 a year.

Growth down, inflation up – a whiff of stagflation

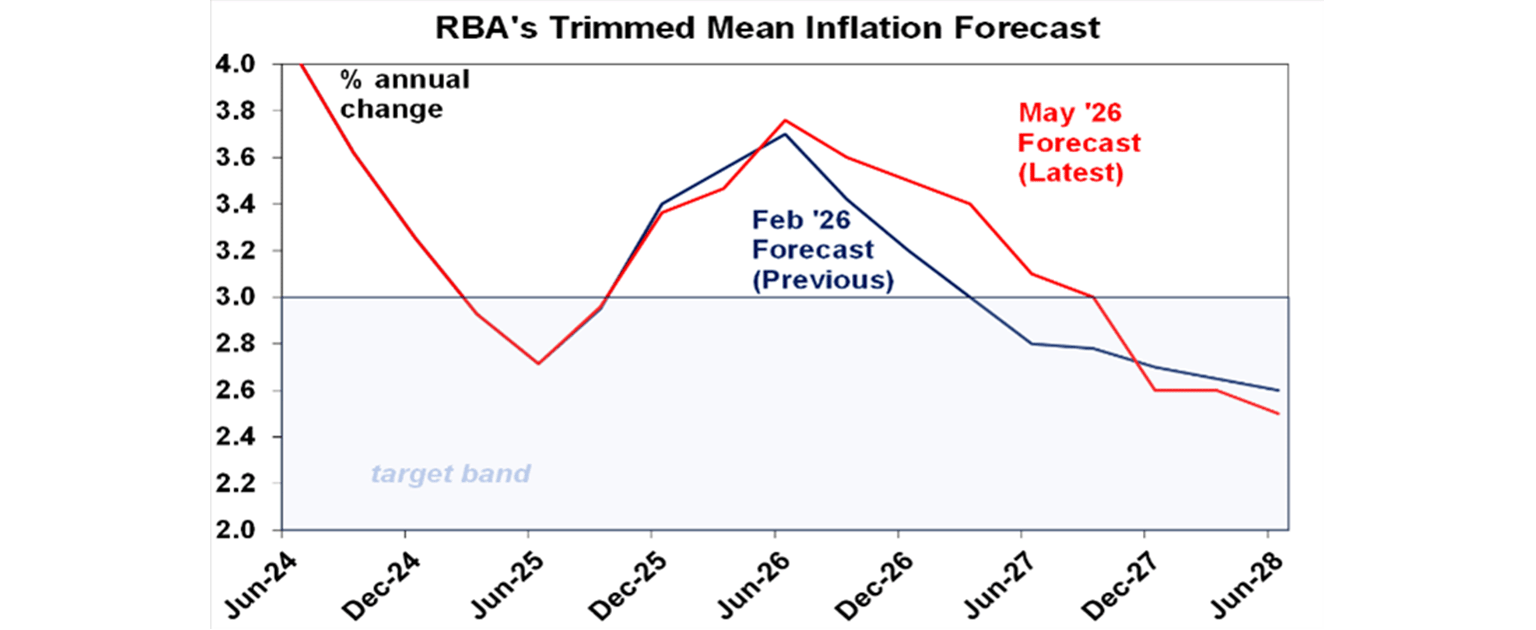

The RBA revised down its growth forecasts compared to February reflecting the impact of the War and a higher money market profile for the expected cash rate. While it revised up its unemployment forecast for 2028 it was only marginally to 4.7%. It also revised up its forecasts for trimmed mean inflation for the next year reflecting second round impacts from the War, but then sees it falling in 2027-28 back to target as higher rates and lower growth lead to lower demand and hence lower pricing.

This is a dismal outlook with growth of 1.3-1.4% for two years, a poor inflation/growth trade-off and higher unemployment. It’s a whiff of stagflation. The risk is that unemployment ends up much higher than the RBA’s 4.7% forecast.

Key reasons for the rate hike

In hiking rates again, the RBA noted an expected further boost to inflation from the War including via second round effects, at a time when inflation was already too high and increasing concern that inflation expectations will rise as a result. It is clearly more concerned at this point about inflation (where it is underperforming relative to its objective) than full employment (where it is arguably meeting its objective at least for now).

Governor Bullock’s press conference comments basically reinforced these concerns and left the door open for further interest rate hikes if needed.

The RBA also indicated it will remain “attentive to the data”. If unemployment remains lowish but underlying inflation high, then more rate hikes are likely. But if unemployment starts to rise sharply relative to inflation, then it will put a brake on RBA hikes.

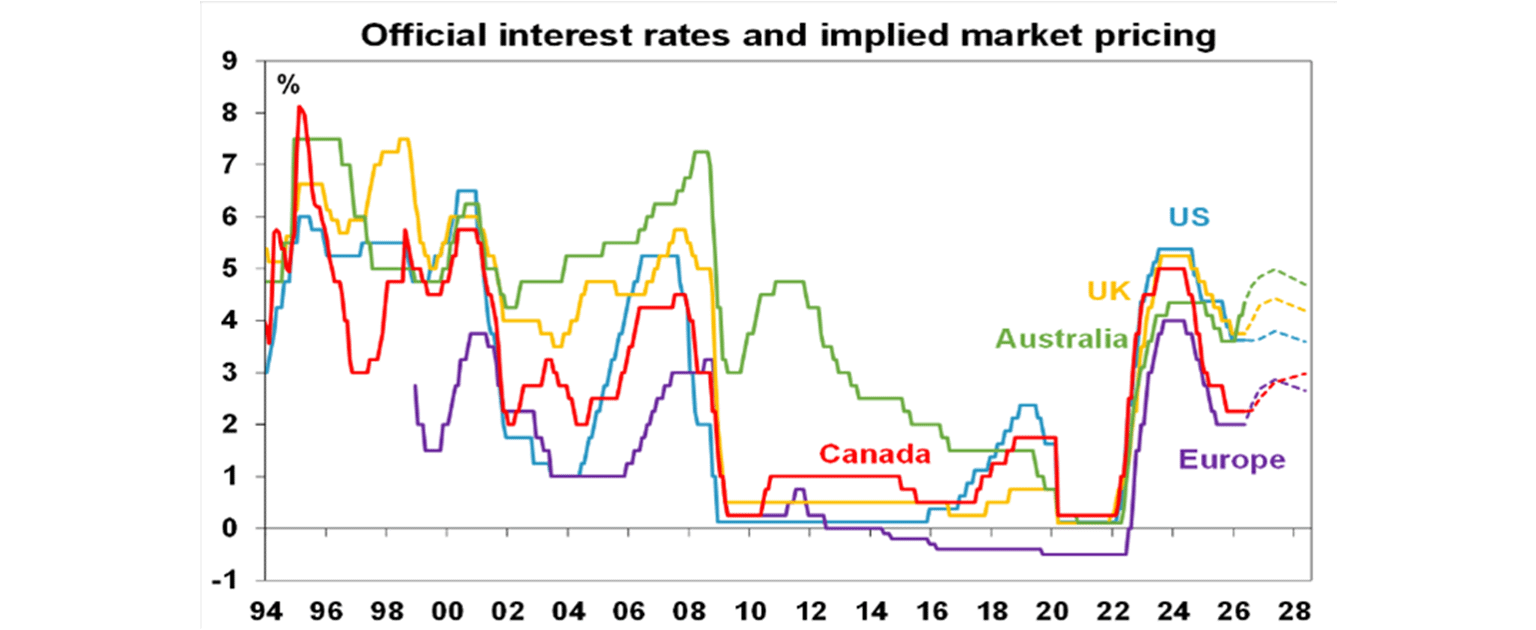

With the RBA hiking and the money market still expecting another 1.5 rate hikes by year end (on top of this one), interest rates in Australia are moving higher relative to other major countries. This reflects other major countries mostly having inflation much closer to target before the War started, whereas Australia already had an inflation.

The oil supply shock makes the RBA’s job difficult

It was hoped at the time of the last RBA meeting in March that we would have more clarity around the Iran War. And a collapse in Australian petrol prices to near pre-War levels helped along by the fuel tax cuts and an easing in the immediate fuel supply fears of a month ago may be providing a sense of complacency. Unfortunately, the outlook for the War is as clear as mud. Trump wants to TACO but Iran remains intent on inflicting economic pain until the US backs down more. The Strait remains closed and Iran is responding militarily to any move by the US to prize it open without at the same time the US lifting its own blockade on Iranian shipping. So, it’s a standoff.

And the longer the Strait remains closed the greater the odds of a severe bout of stagflation – with inflation well above 5% and recession – as the full implications of the implied 10-15% hit to global oil and gas supply will become apparent as oil reserves run down.

This would mean higher oil prices (possibly up to around $US150 a barrel), and for Australia a sharp rebound in petrol prices from the recent lull and fuel rationing which will lead to a bigger boost to inflation initially and hit to economic activity. It’s not our base case – as the pressure on Trump to strike a deal with Iran (no matter how vacuous) is very high given the approaching midterm elections. But the risk rises for each day the Strait remains effectively blocked. This leaves the RBA in a difficult balancing act – should it focus on inflation or worry about the hit to growth and the risk of a much bigger rise in unemployment?

The 1970s suggests keeping inflation down is key

The experience of the 1970s holds key lessons for today. It saw inflation progressively surge into double digits in response to labour and oil shocks, rapidly rising government spending and overly easy monetary policy. Importantly, inflation had already started to rise before the first oil shock in 1973. It contributed to even higher inflation and weak growth and rising unemployment giving rise to the term stagflation. Then like now central banks grappled with whether to target inflation or weak economic activity but initially ran too easy monetary policy which allowed inflation to get out of control with surging inflation expectations which then meant that ultimately to get it under control in the 1980s (and 1990s in Australia) very tight monetary policy and deep recession were required. The key lessons were that: entrenched inflation is bad for the economy as most lose from cost of living pressures; once the inflation genie gets of the bottle it gets harder and harder to get it back in as inflation expectations rise; and that whether its initially due to a hit to supply or strong demand the central bank has to respond by tightening monetary policy and focussing initially on keeping inflation down to avoid a higher cost later.

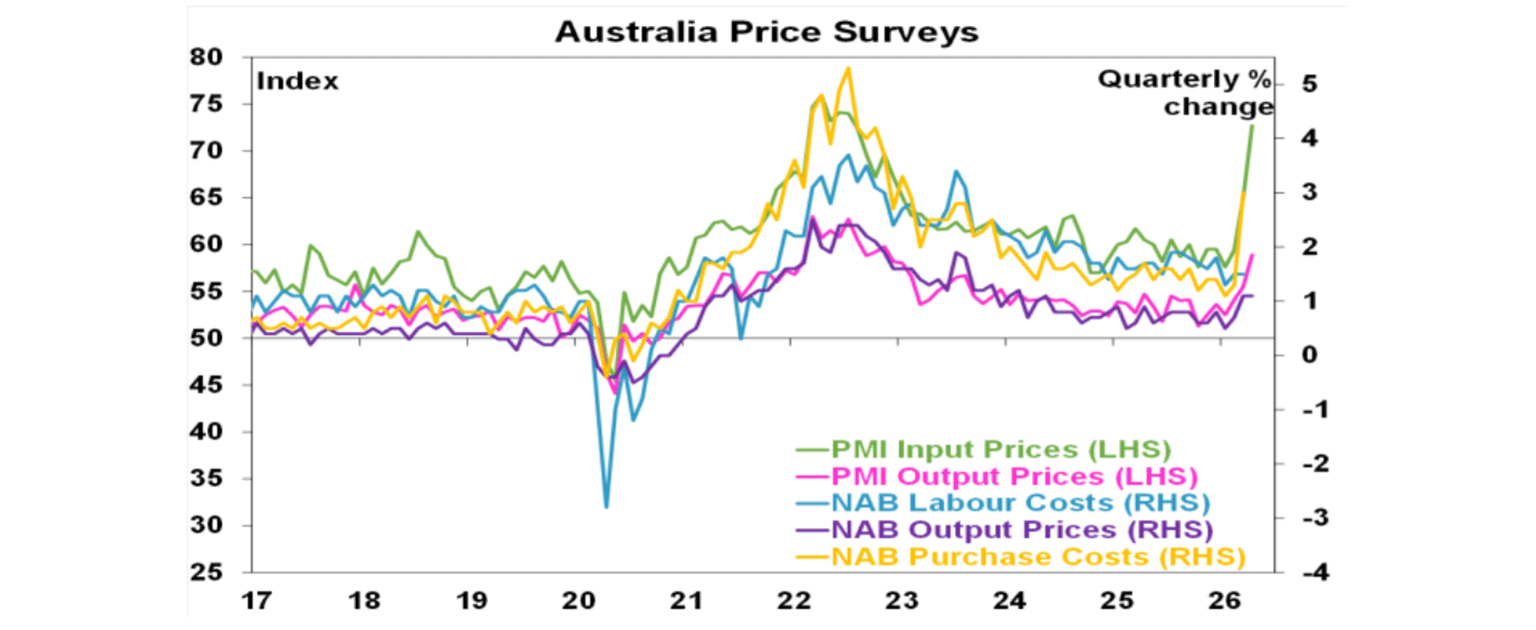

History doesn’t repeat but it does rhyme and there are several parallels today with the 1970s – bigger government, deglobalisation, decarbonisation and aging populations have already made the economy more inflation prone and with the oil shock we are now seeing the third supply shock this decade (following the pandemic and the Ukraine War). And the Iran War threatens a further rise in underlying inflation with many reports and anecdotes of price rises for everything from airfares to toilets. Underlying inflation may also be boosted if fuel shortages lead to supply side problems. And with Australian inflation already above target and now likely to be more so the greater the risk that this will flow through to higher inflation expectations leading to higher wage demands and business being more inclined to put through bigger price rises. The longer inflation stays above target, and it now looks like doing so for five of the last six years including the present year, the more people will expect it to stay above target and the harder it will be for the RBA to get it back down. Businesses are already reporting a big rise in price pressures. This effectively blew my pre-War optimism on inflation out of the water!

So the RBA is right to be concerned and wants to show that it remains determined to get inflation back to target and to not let it spiral higher as occurred in the 1970s. This is not about thinking that higher rates can get fuel costs back down but rather is about bring demand in the economy back into line with supply and showing that its serious about: preventing a further flow on to underlying inflation; wanting to see inflation go back to target in a reasonable time frame; and trying to keep inflation expectations down.

The risk of course is that higher mortgage rates combined with War drag Australia into recession. Household spending power will be hit by a combination of the three rate hikes (which in total will cost around $300 a month in higher interest payments for those with a mortgage) and a likely rebound in petrol prices with the Strait remaining closed. Households with a mortgage are far more sensitive to changes in their disposable income than older Australians who may benefit from higher rates on their bank deposits. It’s also worth noting that the value of household debt in Australia is almost double the value of household bank deposits so higher rates cost the household sector far more than it benefits it. And fuel rationing possibly in June if the Strait remains closed will have a broader impact on the economy in curtailing some activities. Australia is particularly vulnerable on this front as we import 80-90% of our oil products.

All up and depending on how long the oil disruption lasts, in a worst case scenario the hit to economic activity could knock 1 to 2 percentage points off GDP growth and knock the economy into a recession.

On balance we think that the potential significant hit to economic growth cannot be ignored by the RBA. Although the June RBA meeting will be “live” for another hike our base case for now is that it will leave rates on hold waiting to get a better handle on the hit to the economy from the rate hikes so far and the impact from the oil supply shock. We are pencilling in one last rate hike for August though, but see the RBA cutting rates next year as weaker growth starts to bear down on inflation.

How can the Government take pressure off the RBA?

Further cost of living relief in the Budget should hopefully be limited given the risk of just adding to demand and hence inflation. More fundamentally the Government should focus on reducing capacity pressures in the economy and boosting capacity. The three key things it needs to do this are: to cut government spending back to the normal levels that prevailed pre covid; deregulate the economy to make it easier to start new businesses, employ people and supply more homes; and reform the tax system to in particular lower income tax and encourage business to invest more. Fiddling with negative gearing and capital gains tax – while they have some merits - are more about optics than fundamentals on this front.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset. -

Weekly market update - 17-07-2026 Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.