Oliver's Insights

The RBA hikes again on the back of the boost to inflation from the Iran War

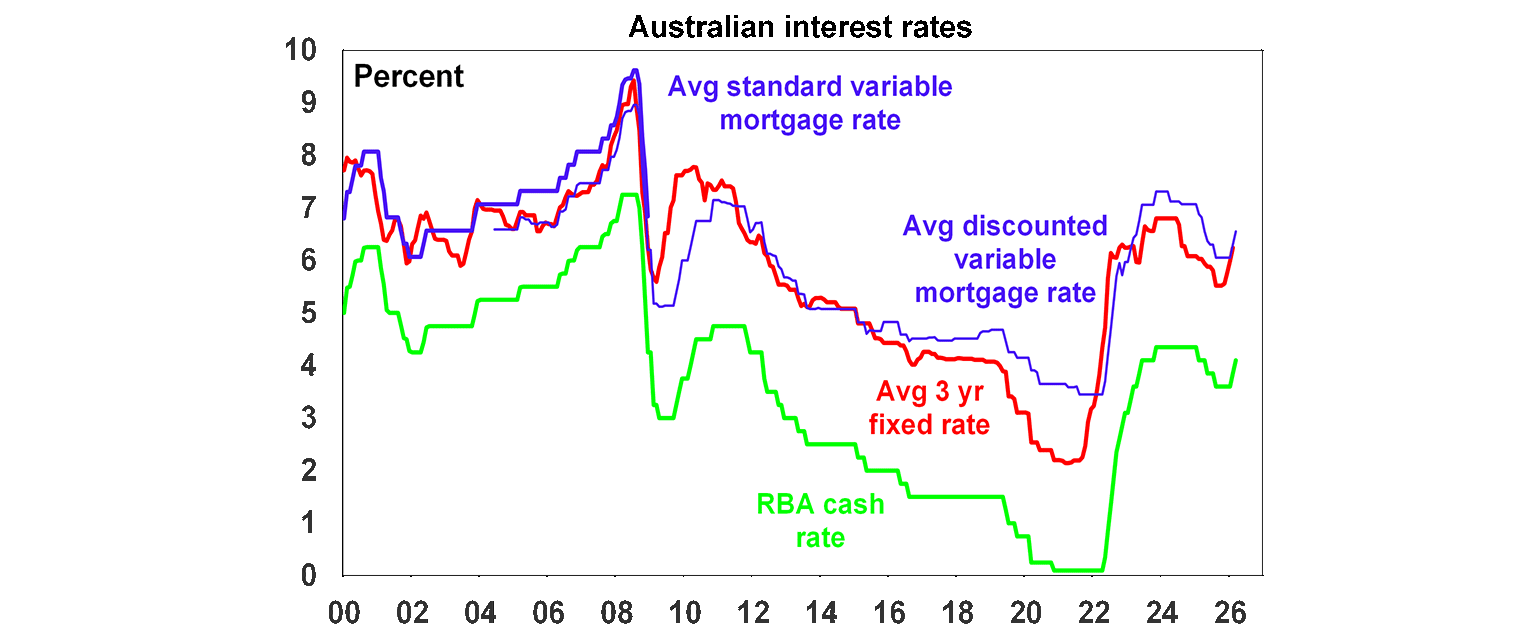

The RBA’s decision to hike rates to 4.1% means that it has now reversed all but one of the three rate cuts we saw last year, which of course followed 13 rate hikes seen in 2022 and 2023.

6 min read

Key points

The RBA hiked its cash rate for the second time this year by another 0.25% to 4.1% in response to inflation running above target and the War with Iran likely to boost it further.

A further rate hike is highly possible, but the longer the conflict persists the greater the risk that the inflation shock will turn into an output shock.

As such our base case is for the RBA to leave rates on hold at its May meeting.

The best thing the Government can do to help alleviate underlying inflation pressures is to lower the level of public spending and introduce reforms to help boost productivity.

Introduction

The RBA’s decision to hike rates to 4.1% means that it has now reversed all but one of the three rate cuts we saw last year, which of course followed 13 rate hikes seen in 2022 and 2023. Once passed on to mortgage holders it will leave mortgage rates around levels prevailing 14 years ago. Of course, it should also mean a slight rise in deposit rates.

In hiking rates again, the RBA noted higher than expected capacity pressures in the economy, some further tightening in the labour market, sharply higher fuel prices due to the War which will add to inflation if sustained, a material risk that as a result of the War inflation will stay above target for longer and that inflation expectations will rise.

While the 5/4 vote in favour of a hike versus a hold suggests a close decision, Governor Bullock indicated that the debate was about timing not the direction of rates.

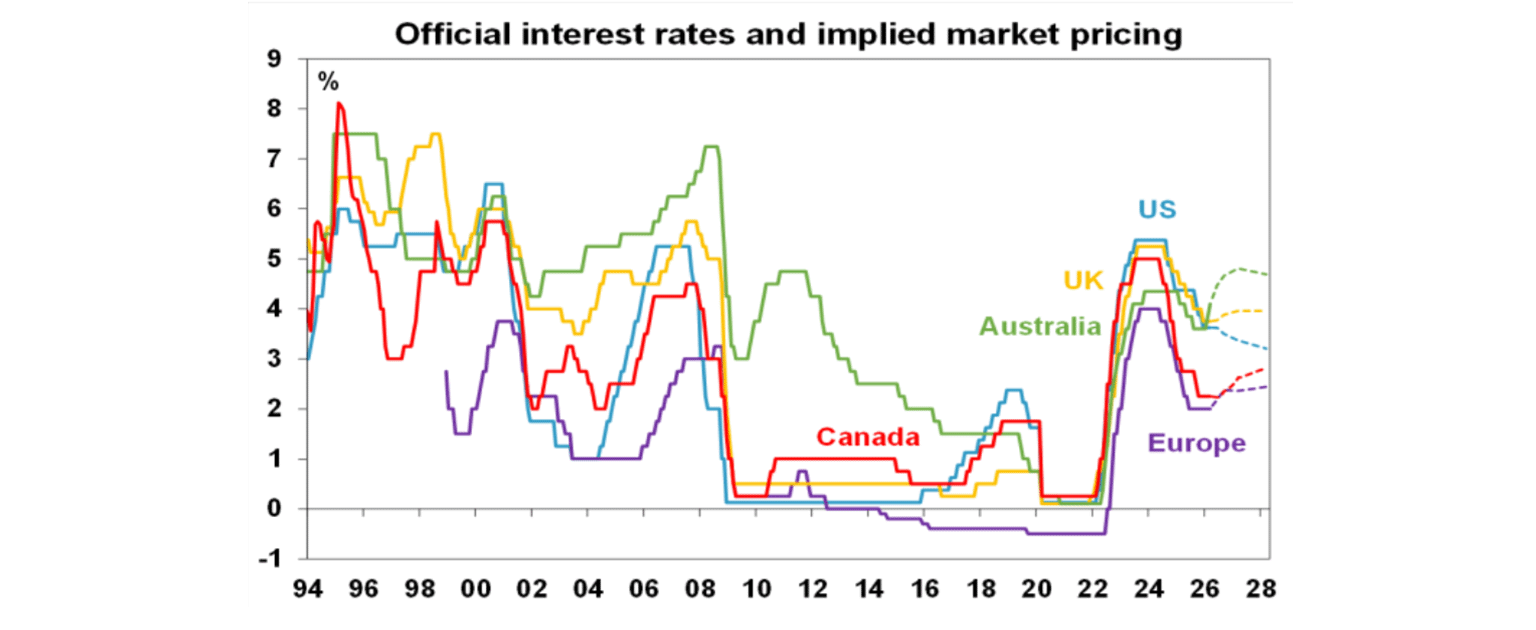

With the RBA hiking and the money market expecting nearly two more hikes by year end, interest rates in Australia are moving very differently to other major countries. This partly reflects inflation being further above target in Australia than in most other countries, but there is also a risk that the RBA has over-reacted.

The supply shock from the Iran War risks stagflation

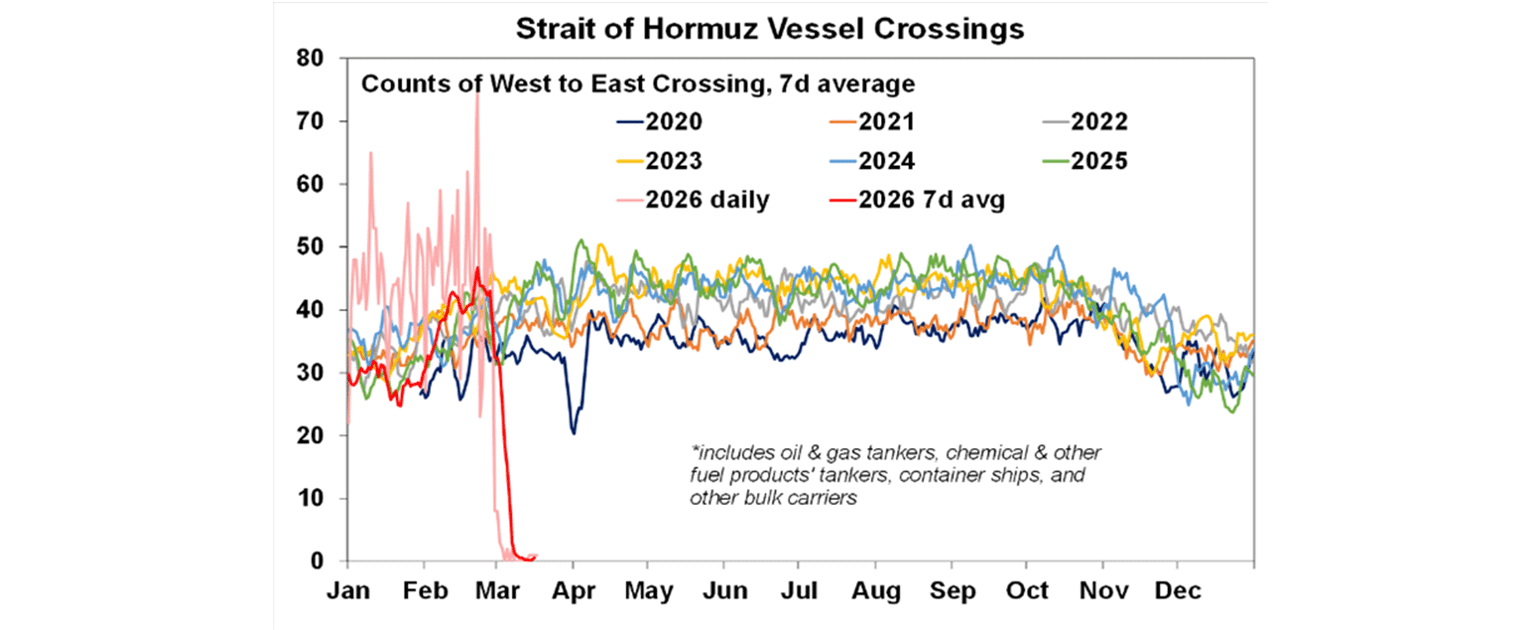

As was the case with the 1970s oil shocks the current oil shock is a double-edged sword in terms of its impact on the economy. Of course, the economic impacts may not be as bad as they were in the 1970s because of a sharp 60% fall in the oil intensity of GDP since then. But working the other way, the International Energy Agency has noted that the current event could be the biggest oil supply shock on record if it persists. This is because the hit to oil supplies flowing through the effective closure of the Strait of Hormuz could be at least 15 million barrels a day or 15% of global oil consumption (after allowing for some diversion to pipelines) whereas the second oil shock in 1979, for example, was only a hit to around 5% of oil supply and yet saw a threefold rise in world oil prices. The IEA release of oil reserves (maybe 3.3% of daily global oil consumption), an easing of Russian sanctions (maybe another 1.5%) and Iran allowing ships from non-enemy countries (eg China, India and Pakistan which normally take 7.5% of global oil consumption) to pass through may ease some pressure but not all of it. So, it remains potentially at least as big an oil supply shock as the 1979 oil shock.

In terms of the impact on inflation:

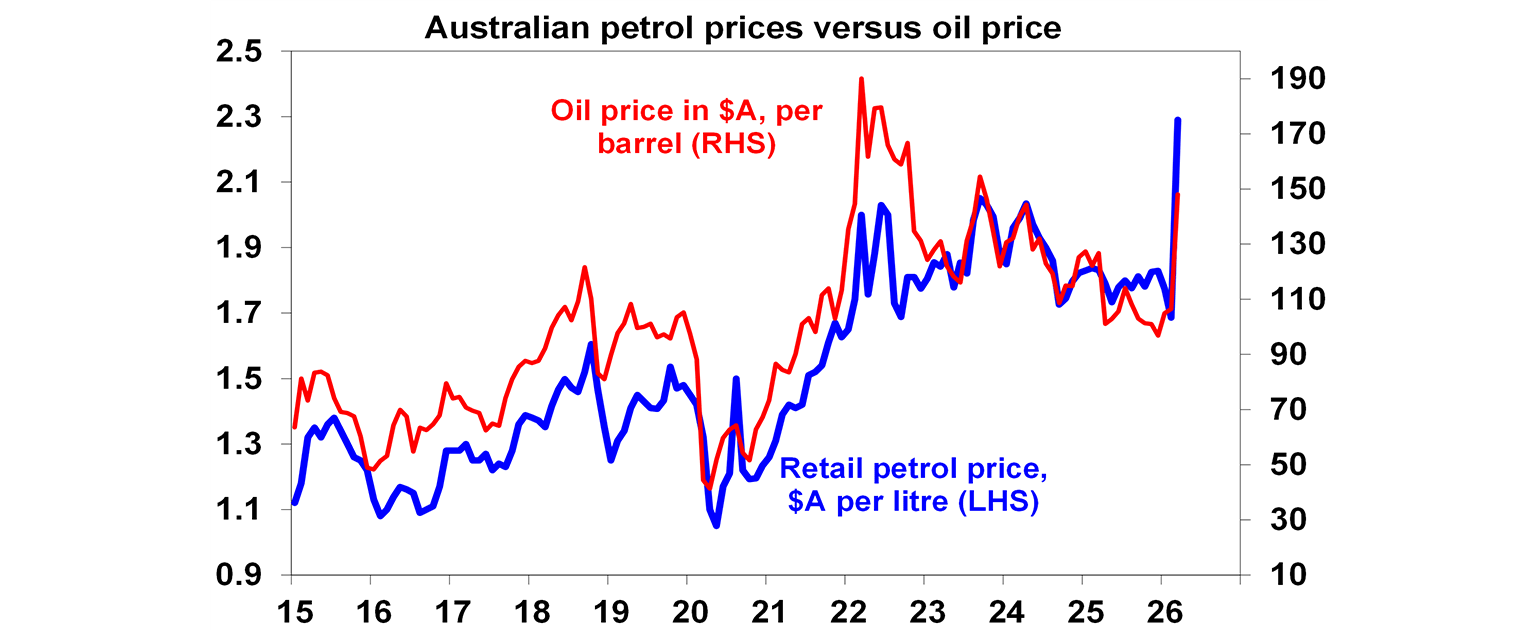

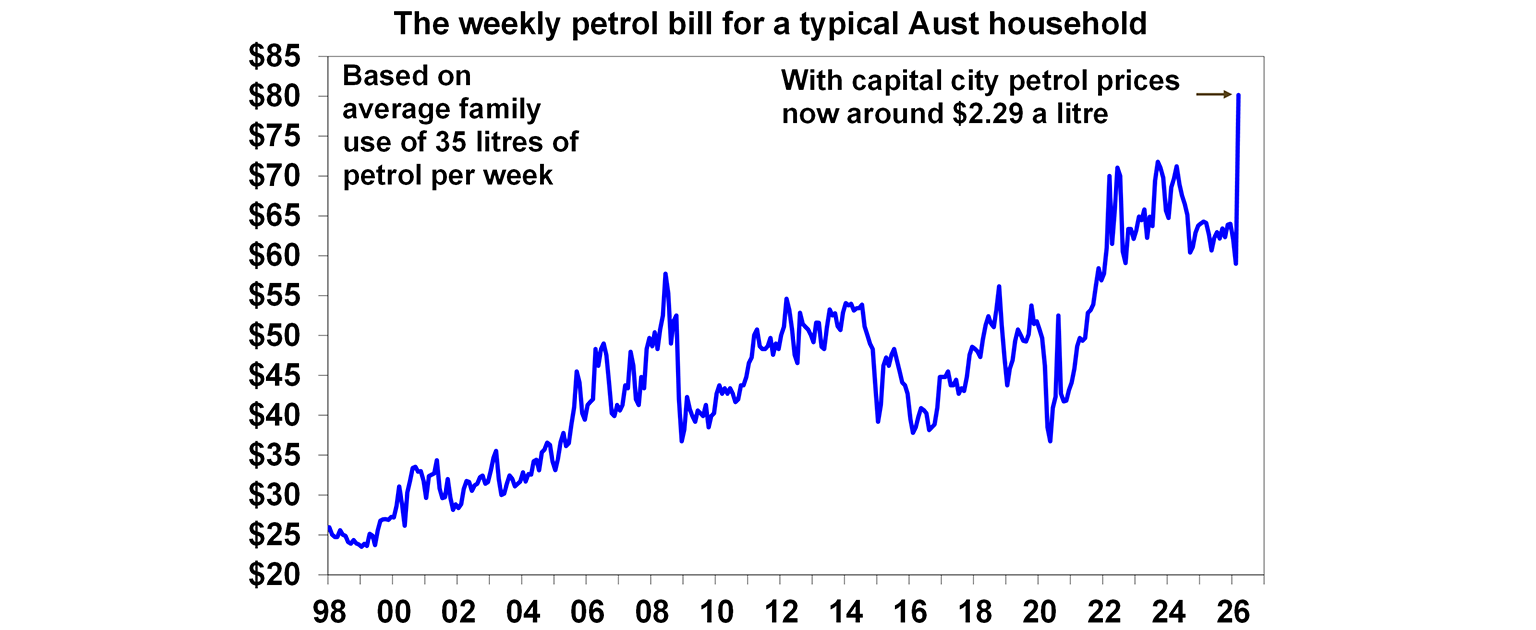

Petrol prices have already increased by around 35% from their average in February which if sustained implies a direct boost to inflation of around 1.2 percentage points which will take it to around 5% if prices stay around current levels.

Obviously if oil and hence petrol prices rise further the boost to headline inflation from higher petrol prices will rise. The longer oil supply is constrained the more oil prices risk going even higher and could reach say $US150 a barrel even if the War ends next month. This could add roughly another 50 cents a litre to petrol prices, adding another 0.7% or so to inflation.

The longer this persist the more there will be some flow through to higher underlying inflation via higher costs for transport (eg airlines and groceries) and products like plastic. Underlying inflation may also be boosted if fuel shortages lead to supply side problems.

And with Australian inflation already above target and now likely to be more so the greater the risk that this will flow through to higher inflation expectations leading to higher wage demands and business being more inclined to put through bigger price rises. The longer inflation stays above target, and it now looks like doing so for five of the last six years including the present year, the more people will expect it to stay above target and the harder it will be for the RBA to get inflation back down.

So it’s understandable that the RBA is concerned and wants to show that it remains determined to get inflation back to target and not let it spiral higher as occurred in the 1970s partly because central banks at the time, including the RBA, were too lax in trying to head off higher inflation expectations flowing from the then oil supply shocks.

Working the other way though, and complicating the RBA’s job, is the hit to growth from the War which could be big. And weaker growth or demand in the economy will lower underlying inflation.

Global growth is likely to be depressed by the rise in oil prices if its sustained. Rough IMF estimates suggest that each 10% rise in world oil prices will knock 0.1-0.2% off global growth and so far they are up 50% since the War started implying a 0.75% or so hit to global growth. This would mean less demand for Australian exports.

The rise in petrol prices in Australia if sustained at current levels will mean a roughly $20 a week rise in the average household’s fuel bill or around $86 a month. It’s now at a record high. This is effectively like a tax hike and along with the $110 a month in extra mortgage interest payments flowing from the latest RBA rate hike (for a mortgage holder with a $660,000 mortgage) on top of that flowing from the February rate hike implies a roughly $300 a month hit to household spending power for those households with a mortgage and a petrol car. And this demographic is far more sensitive to changes in their disposable income than older Australians who may benefit from higher rates on their bank deposits. It’s also worth noting that the value of household debt in Australia is almost double the value of household bank deposits so higher rates cost the household sector far more than it benefits it. While households have been boosting their saving rate it’s hard to see this coming down much given the fall in consumer confidence levels since the War started. So, household spending growth is likely to soften significantly.

Finally, because Australia now imports 80-90% of its oil products and only has about 30-35 days in reserve we could suffer shortages if the crisis continues for another month as refining countries restrict their exports, as China announced it would do two weeks ago. This worst-case scenario would impose a restriction on economic activity similar to pandemic lockdowns – back to “work from home” for those who can!

All up and depending on how long the oil disruption lasts, the hit to economic activity could knock 1 percentage point of GDP growth and knock the economy back into a per capita recession.

Of course, the War may quickly end in which case the RBA may have reacted prematurely. But the duration of the War and more importantly the restriction of oil through the Strait is a bit of a guessing game with Trump saying it may end soon but in reality, being dependent on Iran which seems to be digging in and Trump now asking other countries for help in reopening the Strait of Hormuz. Our Base Case remains a limited war but that could still take us into April and oil prices could still spike as to $US150 a barrel or so in the interim. Of course, a longer effective closure of the Strait could result in a much bigger impact.

On balance we think that the potential significant hit to economic growth cannot be ignored by the RBA and is a reason why having hiked for two months in a row its now likely to remain on hold for several meetings at least to see how long the oil disruption lasts and to get a fuller picture of the inflationary and deflationary impacts from the crisis.

How can the Government take pressure of inflation?

Another fuel excise cut would just be a band aid solution which as the 2022 experience and the energy rebates show provides no lasting solution once the relieve is removed.

Rather the best approach for the Government would be to deliver on its commitment to announce spending savings, productivity and tax reform packages in the May budget.

Ever since the GFC it seems the global economy is subject to more periodic crises – partly due to the rise of populist leaders and geopolitical tensions. The best way to insulate Australia from this is to make our economy as productive as possible which in turn requires freeing up individuals and business to produce more.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.