Oliver’s Insights

Nine key longer term consequences of the US/Israeli war with Iran

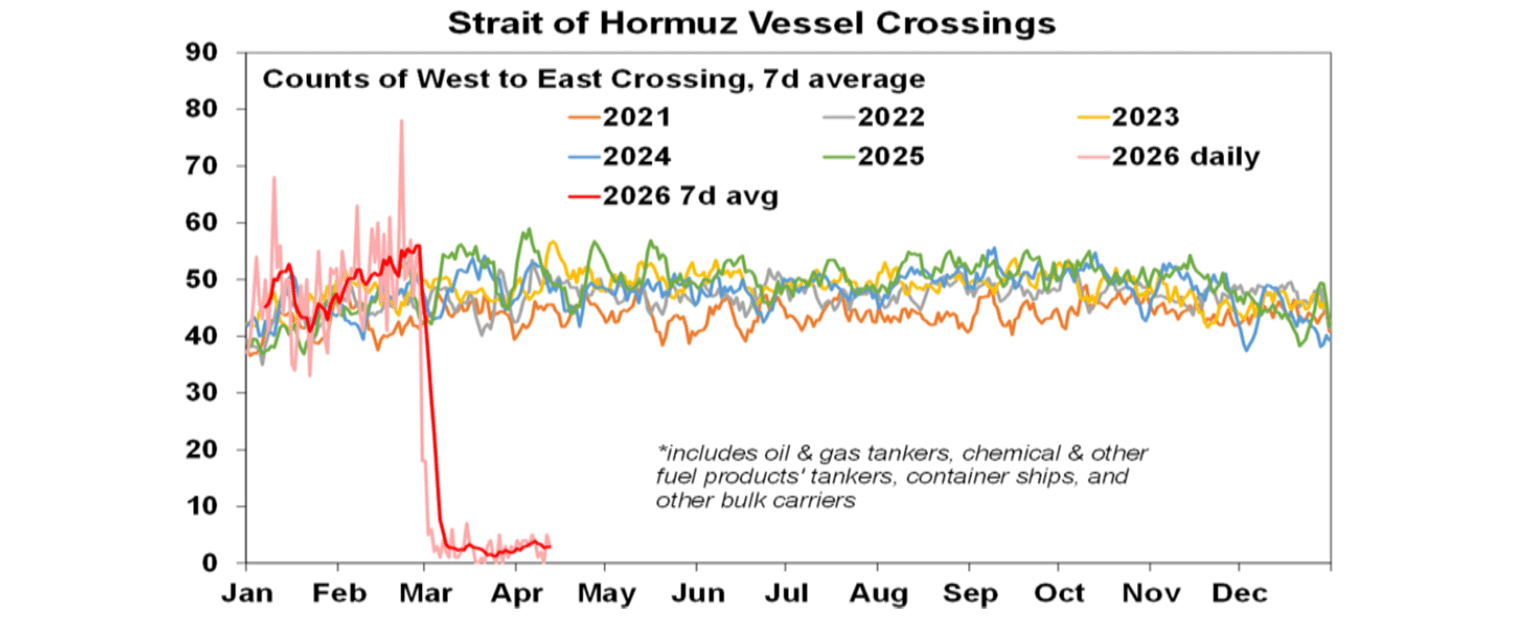

A stagflationary hit of higher inflation and weaker growth is now baked in with the uncertainty being how long it’s sustained. The flow of ships through the Strait of Hormuz remains the key - as it has been since day one of the War.

8 min read

Key points

Uncertainty remains high over the US/Iran War with a ceasefire declared but no agreement in talks so far. Tensions continue to remain high and oil flows remain restricted, with Trump announcing his own blockade on the Strait of Hormuz. But pressure on Trump to back down on the War is very high.

A stagflationary hit of higher inflation and weaker growth is now baked in with the uncertainty being how long it’s sustained. The flow of ships through the Strait of Hormuz remains the key - as it has been since day one of the War.

Beyond the near term uncertainty, there are likely to be nine key longer term consequences of the War: higher prices and inflation; escalated geopolitical risk; a renewed global terrorist threat; increased defence spending; increased spending on oil and gas infrastructure; increased focus on renewables and nuclear energy; more pressure to onshore supply chains; yet another reminder that the world is now more crisis prone; and bigger government and more public debt.

This is all flowing from and reinforcing the rise of populism. Over the long term this risks weaker growth, more inflation prone economies and more volatility which should mean higher risk premiums and risks lower investment returns.

Introduction

The past week provided welcome relief in the Iran War, with Trump delaying for two weeks his threat of the “complete demolition” of Iran’s power plants and bridges. So far its all very shaky, but whether the “ceasefire” holds or not and the War de-escalates or escalates from here, there will be significant long-term implications, beyond the near term stagflationary impact that already looks likely this year. The long-term implications will mostly serve to reinforce existing trends towards deglobalisation, increased geopolitical risk, even bigger government and higher inflation pressures.

TACO time - the current state of the War

Trump’s decision to backdown and announce a ceasefire was consistent with his pattern of making exorbitant demands then backing down as pressure grows intense. This time around his poll support was collapsing, markets were threatening to riot, and he was in a no-win situation with Iran. It clearly has plenty more missiles and drones and, if he escalates, it would use them, worsening the global impact. While Trump has military superiority, Iran has weaponised the Strait of Hormuz to control global oil supplies. So, it is a sort of MAD - mutually assured destruction - stand off from which Trump ideally has to back down. Renewed US/Iran talks have failed to reach agreement, with Trump declaring “whether we make a deal or not makes no difference to me. And the reason is because we’ve won”. But then he announced a new contradiction – the US will itself block shipping in the Strait, but at the same time its Navy will begin demining it! Of course he may soon say something completely different. Overall, we lean to the view Trump will find a way to keep the ceasefire going given the political pressure he is under, but uncertainty is high.

For now, the Strait remains the key, because the last ships that made it through at the end of February are now reaching their destinations meaning refineries in Asia will soon start to run low on oil to refine. So the resultant 10-15% hit to global oil supply (after allowing for diversions, eg, via the Saudi East-West tunnel) will start to bite this month. All of which risks a renewed surge in oil prices - to maybe around $US150/barrel in order to curtail consumption - and plunging share markets.

The nascent pick up in the flow of shipping could resume. But if this comes with Iran and/or the US controlling the flow (with fees and vetos) it will be an unstable solution – as the rest of the world won’t accept such an outcome indefinitely, given the precedent it will set. This would point to a resumption of the conflict. Maybe after the midterms are over, when Trump is less politically constrained, or if his and Republican polling gets so bad that he has nothing to lose by escalating again.

Even if there is a quick end to the War it will take months for global oil flows to return to normal given the time it will take to resume energy extraction in the Gulf (weeks & months for oil, years for some gas plants), to then load this on to ships and for those ships to arrive at refineries in Asia. And then for the refined products to reach Australia.

So, a near term stagflationary impact of higher inflation and weaker growth is now baked in. In Australia, we see inflation peaking around 5-5.5% in the current quarter and GDP growth slowing to around 1.5% this year. With oil supplies coming to crunch time this month the risk of recession in Australia is now high. For central banks wary of letting inflation expectations rise, the focus is likely to be initially on the boost to inflation rather than the hit to growth. This is the case in Australia where inflation was already well above target and signs of rising wage demands will worry the RBA. So, we are allowing for more RBA rate hikes this year.

The longer-term consequences

Beyond the uncertain short term stagflationary impact the War will leave a longer-term impact on economies and markets in nine key ways.

1. Higher prices, inflation and inflation expectations - having another hit to supply and boost to inflation so soon after the last one in 2022 and on top of the tariff impact in the US will lead to another leg up in prices. This runs the risk of a further boost to inflation expectations and loss of faith in central banks’ ability to get inflation back to target.

2. Increased geopolitical risk - this has been on the rise ever since the 2010s due to a loss of faith in liberal democracy reflecting rising inequality, increasing nationalism and populism and a shift away from a unipolar world (dominated by the US) to a multipolar world. The US has gone from chief defender of liberal democracies to a force propelling this shift under Trump with his focus on doing what he wants for America, trashing the global rules-based system, attacking allies (and treating them as scapegoats for his mistakes on Iran) and acting like a “madman” which is leading to a loss of credibility for the US. This has been particularly evident this year with the US intervention in Venezuela, attempt to take Greenland (which he is still on about) and now Iran. It’s hard to see this not being interpreted by other powerful countries as a green light to do whatever they want in their region and beyond. I would rather Ray Dalio’s assessment that the world is heading down a path that risks broader conflict be wrong, but it can’t be ignored. What’s going on now with Iran is the sort of thing that world wars start over.

3. A new generation of terrorists - the Israel/Gaza war and now the Iran War risk driving a renewed rise in terrorism. Economies and markets can look through terror attacks that are limited in impact - as we saw in the 2000s – but this would change if the damage was more general.

4. Increased defence spending - this is an inevitable result of increased geopolitical risk. It will also be fuelled by Trump’s renewed contradictory attacks on NATO countries and other allies including Japan and Australia - for not joining in on the attack on Iran. Particularly so if the US decides to leave NATO as it’s been alluding to.

5. Increased spending on oil and gas infrastructure - while Trump appears to have been surprised and frustrated by Iran’s move to control the Strait of Hormuz (through which 20% of global oil and gas flows) as evident in his “Open the F…… Strait, you crazy bastards” comment, it’s entirely logical and had long been predicted if Iran found itself threatened. It was why Saudi Arabia built its East-West oil pipeline in the 1980s. Now that it’s happened, it provides yet another reminder of the global energy dependency on a highly volatile part of the world. This was on display in the 1970s but was forgotten about from the 1980s as oil shocks were brief. It’s likely to mean increased efforts by Gulf countries to bypass the Strait and medium term moves by other countries to boost their own oil and gas reserves.

6. Increased focus on renewables and nuclear energy - over the longer term the crisis will further boost demand for renewables and nuclear on the simple logic that the sun, the wind and nuclear energy do not depend on volatile politics in the Middle East. This is already evident with motorists reportedly scrambling to buy electric cars (which are now around 15% of new car sales in Australia).

7. Yet more pressure to onshore supply chains - this is on top of the pressure flowing from the pandemic for medical equipment but will now focus on oil refining, aluminium, fertiliser etc which are all being impacted by the War. Future Made in Australia will likely see another leg up. Which all means more protectionism and deglobalisation.

8. Yet another reminder that it’s now a more crisis-prone world - the Iran War is now the fifth major global shock in the last 20 years with the others being the GFC, the Eurozone debt crises, the pandemic & the 2022 inflation shock. While there were crises before that - the tech wreck, the Asian crisis, the early 1990s recession - they now seem more frequent & less related to traditional economic cycles.

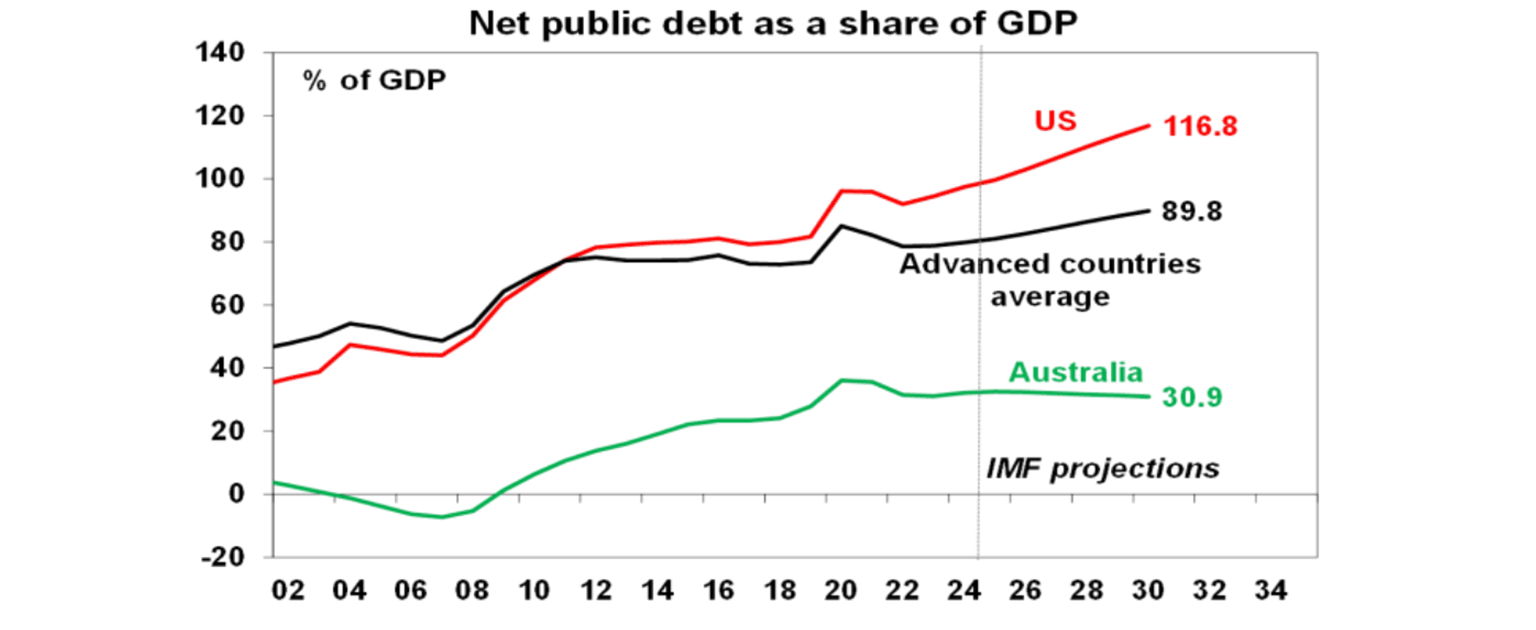

9. Bigger government and more public debt - more defence spending and government involvement in economies, eg in onshoring, mean more public spending, bigger budget deficits and ever higher public debt – at a time when its already high. The latter is particularly evident in the US with Trump pushing for a $500bn (or 42%) defence budget boost when the US budget deficit is running around 6.5% of GDP despite low unemployment suggesting it should be in surplus.

It could also be evident in the upcoming Federal Budget in Australia, which is likely to see more “cost of living” help for households and business at the expense of commitments just a few months ago for the Budget to focus on savings in the level of spending and on productivity enhancing reforms. Another year of stronger spending growth will add to concerns that it will never be brought back to more sustainable levels, as in 2027 the focus will return to the next election.

Ever higher public debt and rising bond yields also run the risk of a public debt crisis at some point.

Implications for investors

There are three key implications for investors.

First, a somewhat less favourable economic outlook – if governments play an increasing role in the economies (via more defence spending, onshoring and protectionism), it’s likely to mean lower productivity resulting in slower economic growth and higher inflation. In short, lower living standards. In the US at present, it’s being fortuitously masked by the AI boom – but this could be a double-edged sword in the near term.

Second, the boost to geopolitical risk and reinforcement of populism and nationalism (notwithstanding the counter trend election outcome in Hungary) means increased uncertainty, including for businesses.

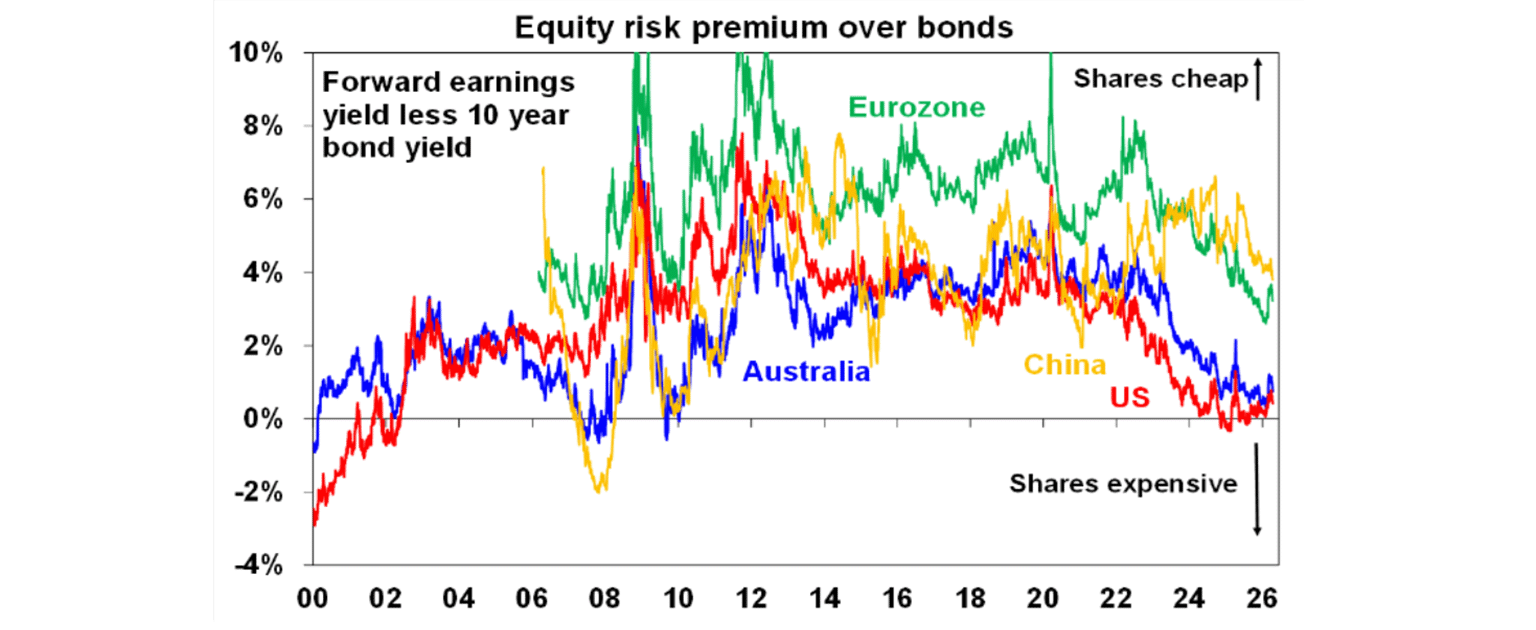

Finally, all of which runs the risk of more constrained and volatile investment returns. Which should mean that shares should be offering a higher risk premium over bonds. But at present the risk premium offered by US and Australian shares – as measured by the forward earnings yield less 10-year bond yields - remains very low.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist, AMP

You may also like

-

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset. -

Weekly market update - 17-07-2026 Following the renewed escalation in the US/Iran conflict, the Strait of Hormuz is effectively closed again with Iran attacking ships and the US attacking Iran and blockading its ports. Both are now back to attacking energy infrastructure which is a signficant & concerning escalation. -

Oliver's insights - Why have Australian living standards “fallen” and how do we fix it? For the last few years there has been much talk of a “cost-of-living” crisis in Australia and of “falling living standards”. This has flared up again lately with the pickup in inflation resulting in a renewed fall in real wages.

Important note

While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.