Econosights - the impact of rate hikes on the US housing market

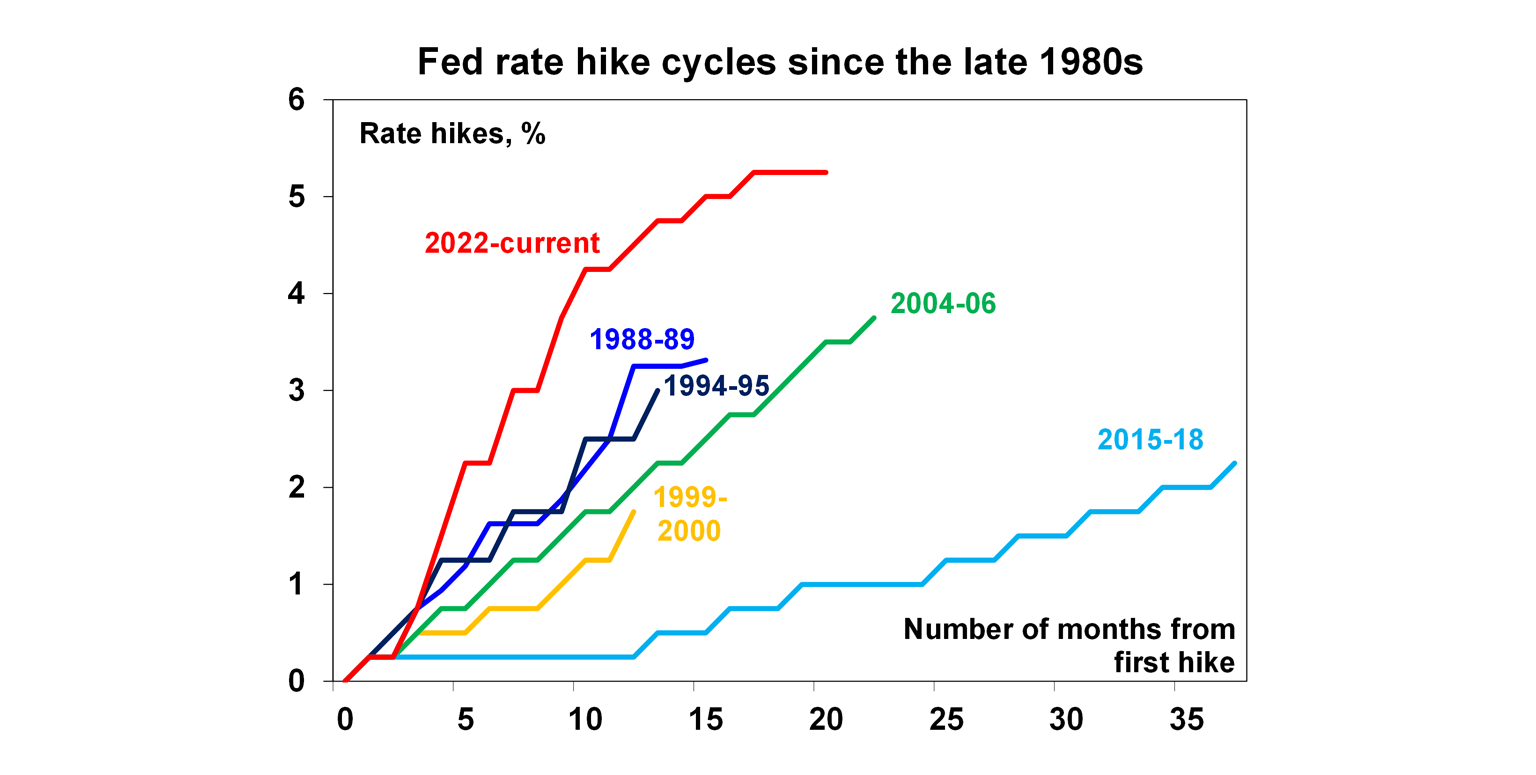

The US Federal Reserve has raised interest rates by 525 basis points (or 5.25%) since March 2022, which has been the fastest tightening cycle in the US since the late 1980s. We look at the impact of these interest rate increases on the US housing market in this edition of Econosights.

7 min read

Key points

The fastest interest rate tightening cycle in the US since the late 1980s has lifted borrowing rates to their highest levels since 2000.

However, the pass-through of interest rate hikes to indebted consumers has been minimal (outstanding mortgage rates have only increased by 0.43% versus a 5.25% increase to interest rates) because more than 95% of US home loans are on long-term fixed mortgage rates.

The impact on new borrowers is significantly different. New borrowers are paying nearly 30% of their income on their mortgage, up from an average of 15% in the last decade.

The tough conditions for new borrowers have led to a significant slowing in lending and refinancing activity. Residential construction has also taken a hit.

However, GDP growth has held up thanks to strong consumer spending from a strong labour market and as households spend by drawing down on their savings buffers.

Housing construction is not keeping up with demand and is leading to housing undersupply which is contributing to higher home prices and worsening affordability.

Introduction

The US Federal Reserve has raised interest rates by 525 basis points (or 5.25%) since March 2022, which has been the fastest tightening cycle in the US since the late 1980s (see the chart below). We look at the impact of these interest rate increases on the US housing market in this edition of Econosights.

The impact on households with a mortgage

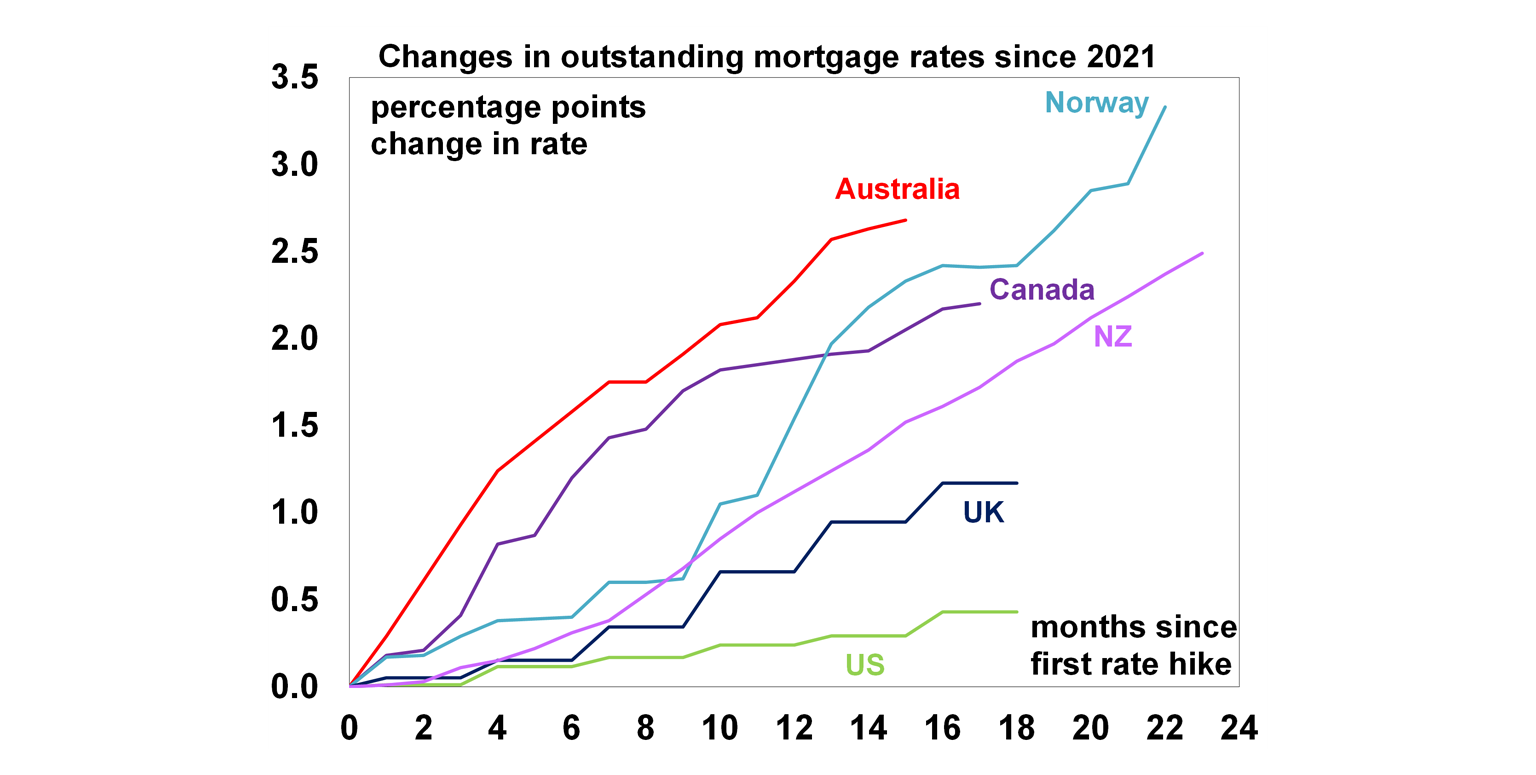

The pass-through of interest rate hikes on US households with an existing mortgage is low because more than 95% of US home loans are on long-term fixed mortgage rates (for ~ 30 years). The increase in outstanding mortgage rates has only risen by 0.43%, compared to the 5.25% lift in the Fed Funds Rate – see the chart below. This is significantly different to the higher pass through of rate increases in countries like Australia, Norway and Canada that have a high share of variable and short-term fixed home loans.

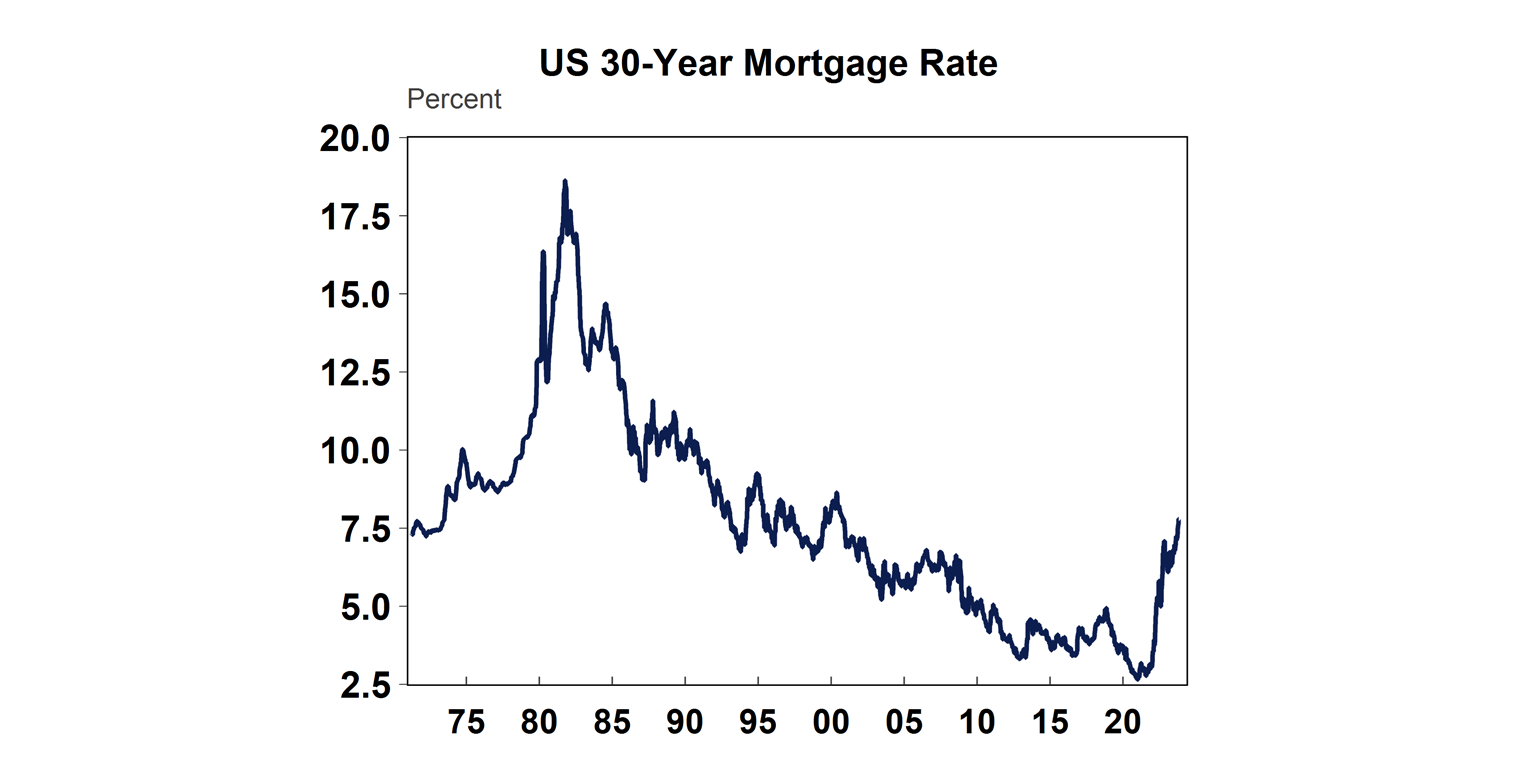

This means that in the US, the largest impact of interest rate increases is on new borrowers - those who are just entering the housing market or existing home-owners that need to refinance. The 30 year mortgage rate is now close to 7.8%, which is more than double early 2022 levels and the highest level since late 2000.

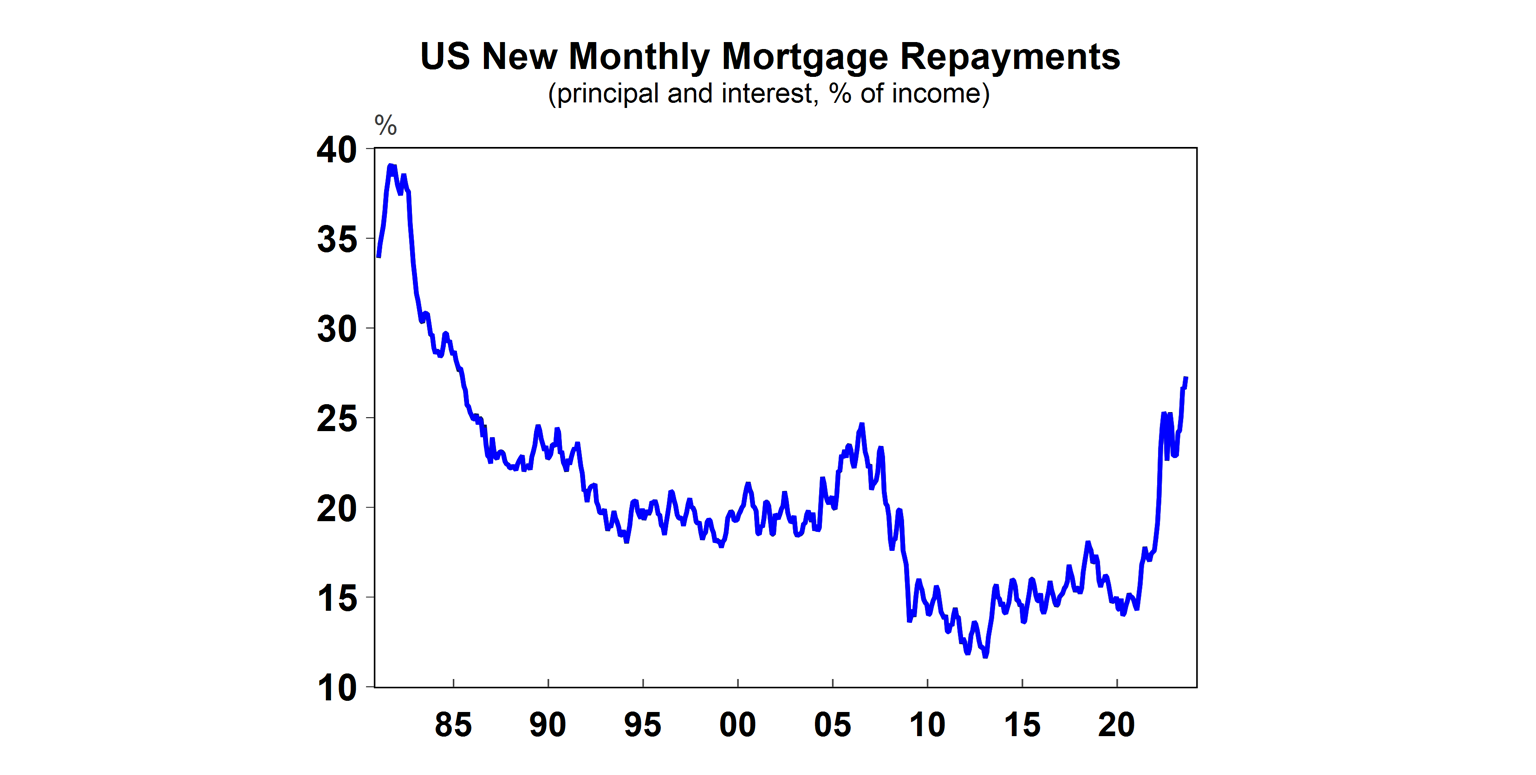

As a result, mortgage repayments as a share of income for new borrowers have risen to a 39-year high of 27% (see the chart below) after averaging at 15% in the past decade.

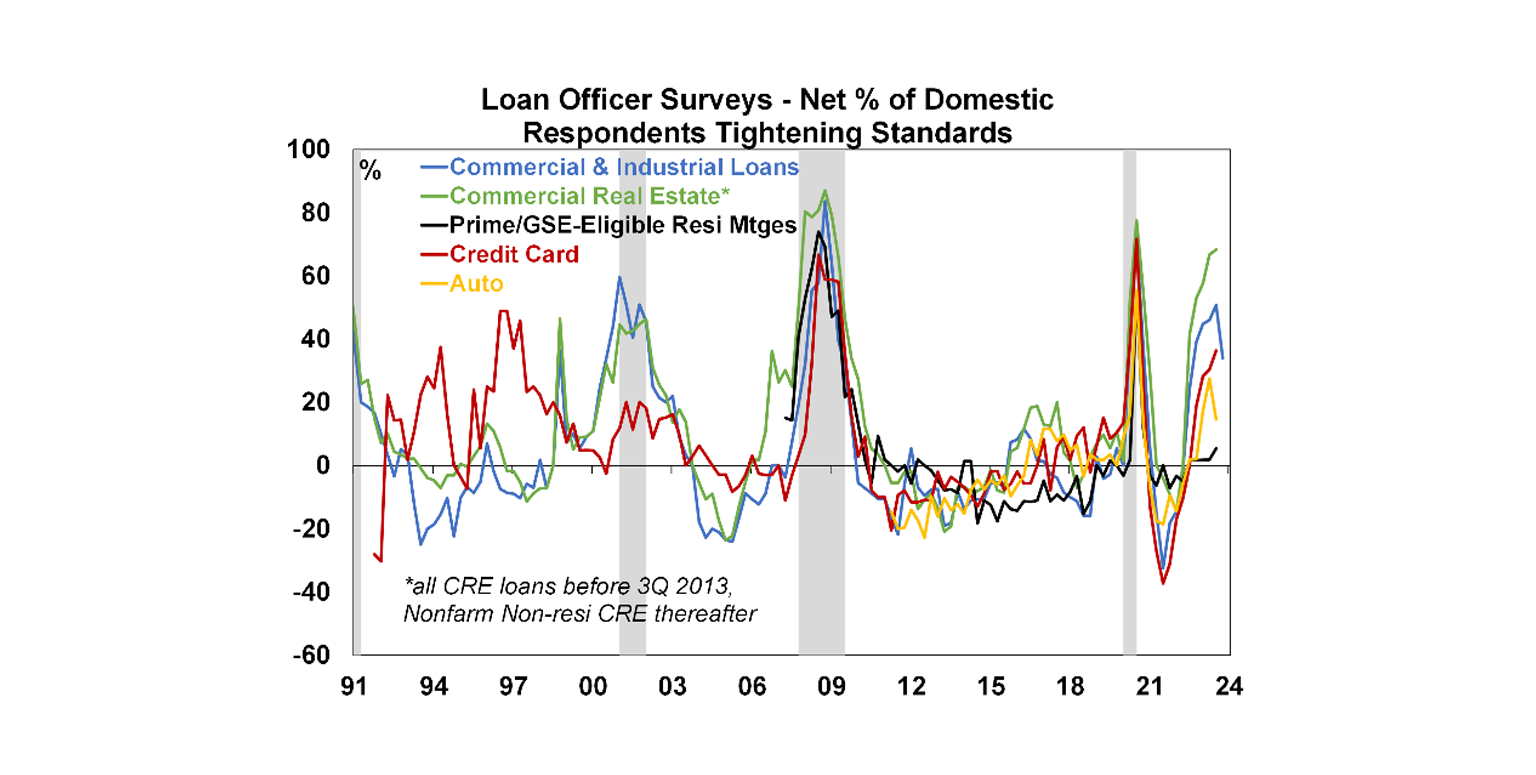

Mortgage applications have collapsed and are running around their lowest levels since 1997 and refinancing activity is tracking at its lowest levels since 2000 which was around the time of the US tech crash and the 2001 recession. Residential lending standards have tightened marginally, but not as much compared to the commercial sector (see the chart below) which was severely impacted by the banking crisis earlier this year.

The impact on residential construction and home prices

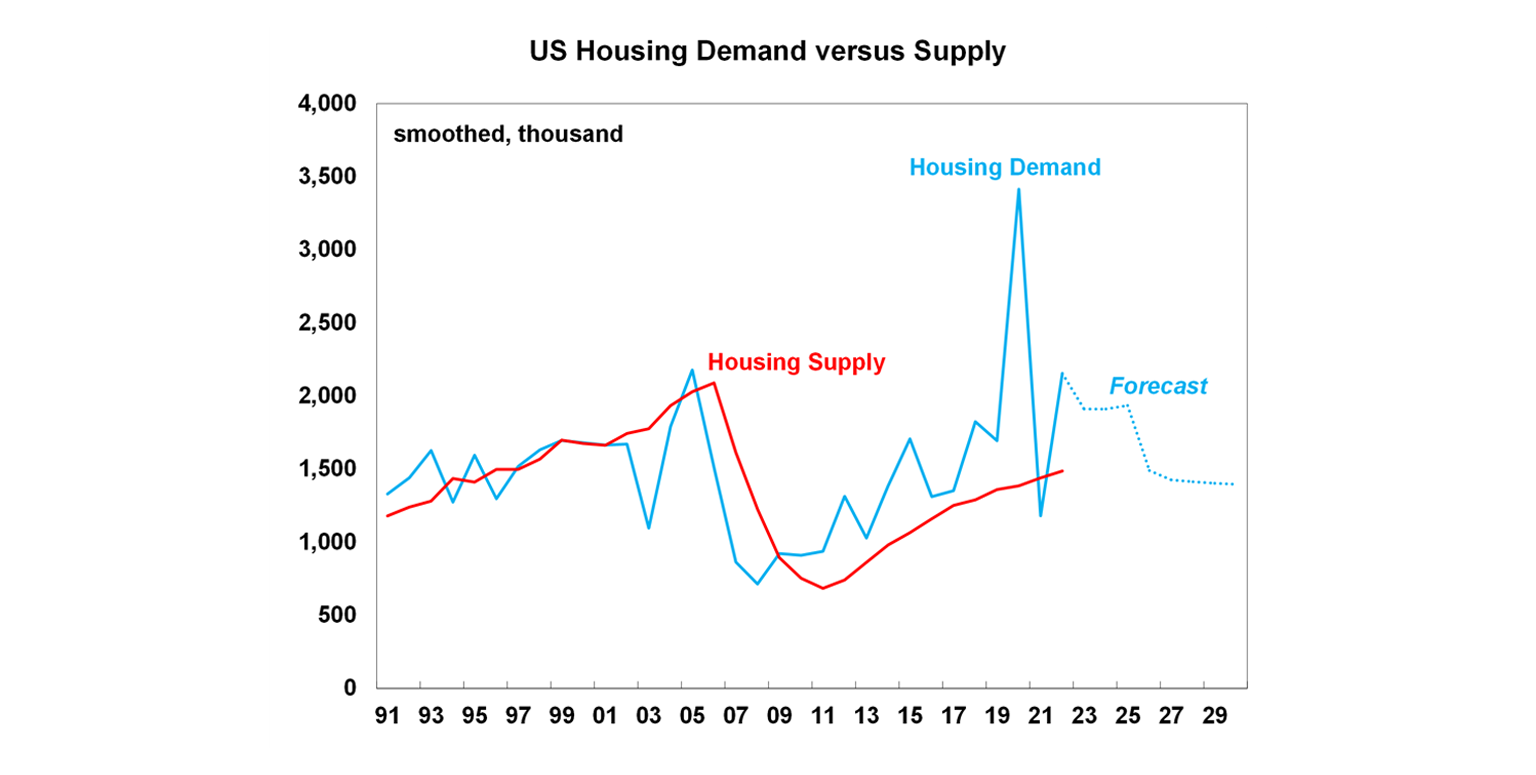

US residential construction has averaged 3.7% of GDP in the past decade. After peaking at 4.4% in the post-COVID upswing, it has since fallen to a cyclical low of 3.3% in September 2023. Rising interest rates are usually negative for housing construction because demand for new homes comes under pressure as the cost of credit increases. There is also a negative flow-on impact to other parts of the economy as reduced housing market activity leads to a reduction in housing purchases related to furnishings. Retail spending on household furnishings is down by nearly 6% compared to a year ago. Lower housing construction also means a decline in housing supply which has already been tracking below housing demand for most of the past 14 years (see the next chart). On our estimates, housing demand based on household formations will average around 1.9 million homes over the next few years. Housing supply (i.e. the completion of dwellings) has been running well below this level, at around 1.4 million homes over the past 3 years, which leaves around a 500,000 home short-fall every year. Continued home underbuilding leads to chronic housing undersupply which puts upward pressure on home prices and rents. Some good news has been that building permits and housing starts look to have bottomed earlier this year and are slowly starting to trend higher which will be positive for new housing construction.

US housing undersupply is a factor behind this year’s turnaround in home prices, despite the increase to interest rates. After reaching a bottom in January 2023, housing prices have increased by 6.4%, with prices now back to a record high, according to the S&P CoreLogic Case-Shiller national home price index. There are differences in conditions across different regions with high price growth in the east coast versus low growth in the west coast.

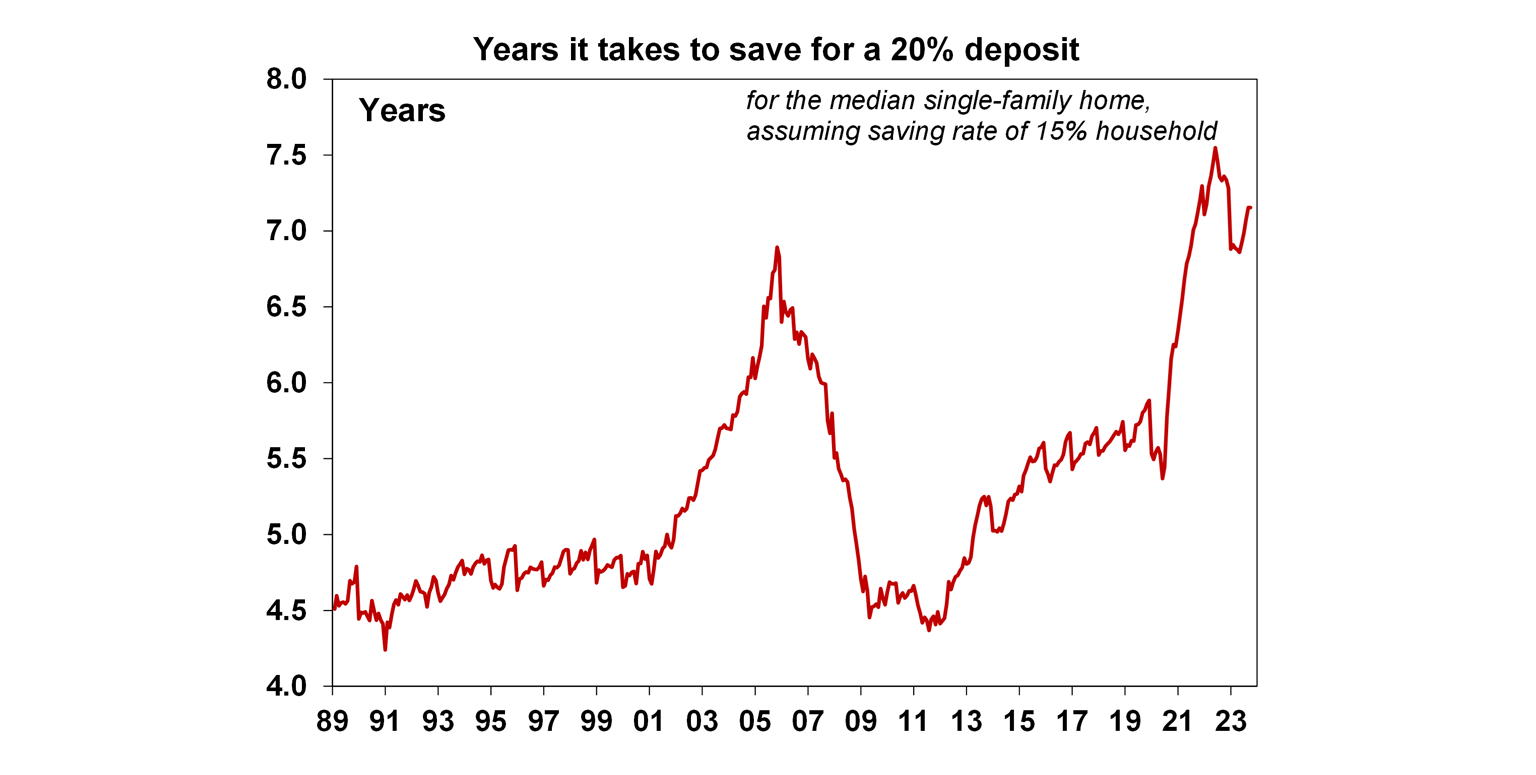

The lift in both prices and borrowing rates means that it has become increasingly difficulty to get into the housing market. On our calculations, it now takes 7 years to save for a deposit (see the chart below) up from around 5.5 years pre-pandemic and around its highest levels on record.

Implications for investors

The significant tightening in US interest rates since March of last year has led to some weakness in housing activity, predominantly in lending growth and a decline in residential construction. However, GDP growth has held up extremely well despite the weakness in these parts of the housing market because of continued strong growth in consumer spending as the impacts of rate hikes have not been felt by all households. Long-term fixed mortgage rates in the US have led to a low pass-through of rate hikes for households with existing loans that still have many years to finish.

However, US GDP growth is expected to slow in 2024 (we think to less than 0.8% over the year to December), from ~2% in 2023 as the lagged impacts of higher interest rates continue to impact more households and businesses. The lift in the unemployment rate will also weaken consumer spending power. The chance of a US recession in 2024 is still high.

We expect that the US Federal Reserve will have to cut interest rates in 2024 as a further slowing in inflation and growth gives the central bank cause to ease policy conditions.

You may also like

-

Weekly market update - 07-08-2026 Shares at all time highs (again) despite Middle East War rollercoaster, Japanese yen & the Disneyland index, Aussie consumers still spending despite rate hikes, and RBA to hold rates but hike can still come later this year -

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.