Weekly market update

Investment markets and key developments

The ASX200 slipped by 0.1% but this follows a record high last week. Materials, energy and real estate saw an increase but these were offset by large declines in communications, healthcare and consumer staples.

15 min read

Fresh record highs for US shares this week. The US S&P500 rose by 0.5% with large increases in energy, consumer discretionary, tech and communications. The ASX200 slipped by 0.1% but this follows a record high last week. Materials, energy and real estate saw an increase but these were offset by large declines in communications, healthcare and consumer staples. European equities have fallen by 1.7%, with a decline in France due to political uncertainty with the Prime Minister Bayrou calling a September 8 confidence vote over this deficit-cutting budget proposals. Chinese shares are booming, up 11% this week (and are outperforming since the beginning of the year), with an easing in home purchasing rules in Shanghai, less concern about growth and cheap valuations fuelling the recent rebound. US 10-year bond yields have fallen a little to 4.2%, oil prices were a touch higher this week on concerns that India will stop buying Russian energy, metal prices were higher, the $US has been trending up from July low (but only slightly) and the $A was fairly steady at just under 66 US cents.

But perhaps the bigger news of the week was Taylor Swift’s engagement (!) or was it the non-stop drama and cliffhanger at the end of The Summer I Turned Pretty cult show oh wait this is an economics and markets report… But are there economic implications of the engagement and Taylor’s diamond ring (did you know that diamond price have fallen by 53% in the past 3 years), even for those non-Swifities. We share our thoughts here.

Trump is attempting to fire one of the Federal Reserve Governors Lisa Cook, after threatening to a few weeks, back due to allegations that she falsified mortgage application documents. Cook is battling the charges and this is likely to go to the Supreme Court, so there is a fair way to go before this is settled. If Trump gets his way, then he would have a 4 person Trump-chosen majority on the seven person board who would be dovish, as Trump has been pressuring the Fed to cut interest rates. The US dollar fell and yields increased slightly on the back of this announcement as the politicisation of the Federal Reserve unnerves investors and probably means lower rates for longer and therefore higher inflation.

More tariff updates this week with the US doubling the tariff rate charged to India from 25% to 50% (which was previously threatened), as a “punishment” for buying Russian oil. This will impact about 1.5% of US imports from India, as smartphones and pharmaceutical products are exempt and increases the average US tariff rate only slightly to ~20%. Mexico also put tariffs on China (including for cars, textiles and plastics), as part of its 2026 budget proposal, bowing down from US pressure to do so.

The US “de-minimis” rule ended this week, which exempted imported items worth $800 or less from tariffs, because it was considered that administrative costs to collect the tariffs outweigh any revenue. But the ending of this rule now means that low-value imported items will be charged with the country tariff rate set by the US. This led to some confusion this week with many major national postal services (including Australia Post) delaying deliveries. So more supply chain disruptions and higher costs for US consumers and businesses, as well as potential higher costs for exporters shipping to the US.

The US chip maker Nvidia and the biggest company on the US S&P500 stock exchange released second quarter earnings and while actual outcomes were more or less in line with expectations, it wasn’t quite enough to boost the stock. But investors have probably gotten used to super-sized Nvidia outcomes (year over year earnings per share growth in the June quarter was 54% for Nvidia and expectations were for 48%). US second quarter earnings season has more or less finished, with 81% of companies beating expectations and earnings growth running up by 11% over the past year.

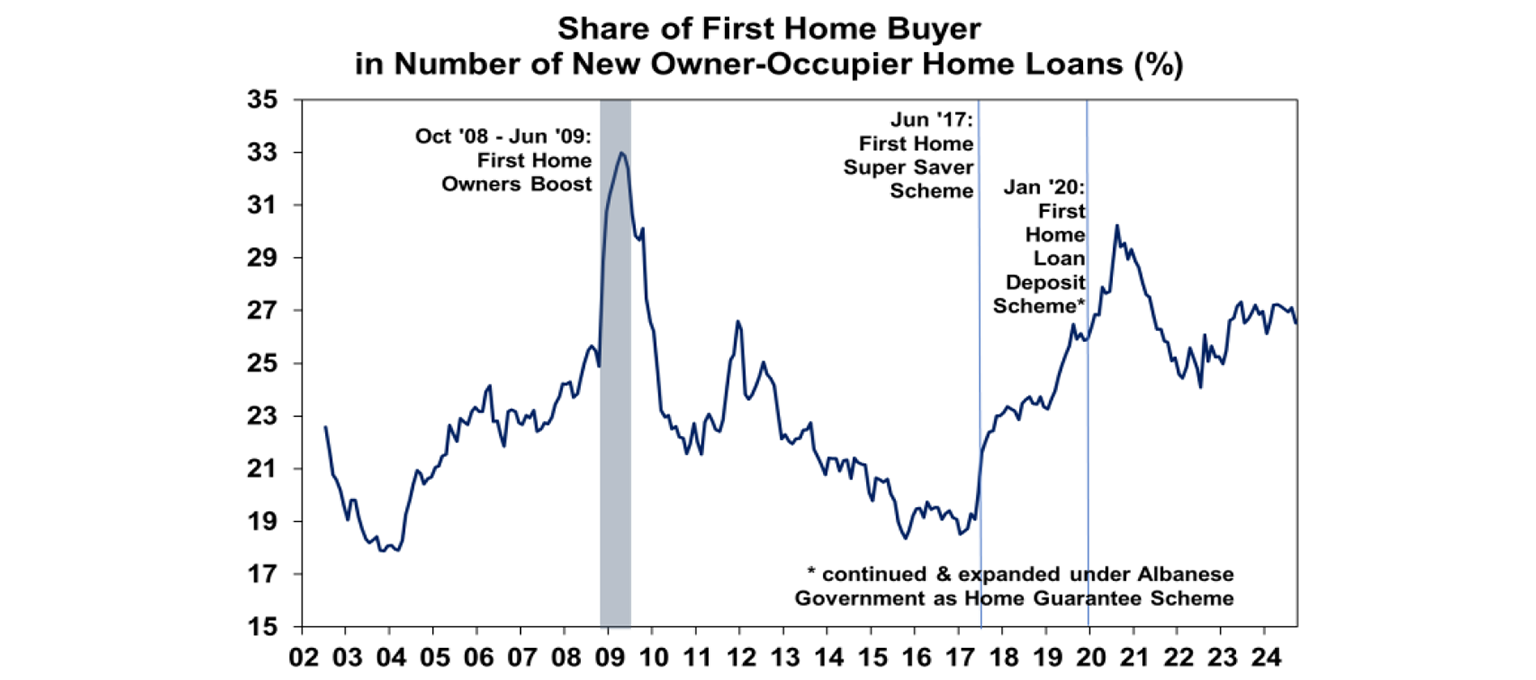

The Australia Labor government has expanded the Home Guarantee scheme. This scheme allows First Home Buyers to buy a property with only a 5% deposit. This scheme now has unlimited places, is not means tested, the government increased property price caps which reflect median home prices and brought the scheme forward to October (from January). Why make the change now? Well it happened after the Treasurer’s Economic Reform round table last week where housing (un)affordability would have been a key topic for discussion, so the government probably wanted to be seen to be doing something straight away. In the short-term these types of schemes tend to lift home prices, because there is more demand in the market without a subsequent lift in supply. We saw this in 2009 following the Rudd assistance for first home buyers (see the chart below) when first home buyers lifted to a higher share of the market and took out larger loans.

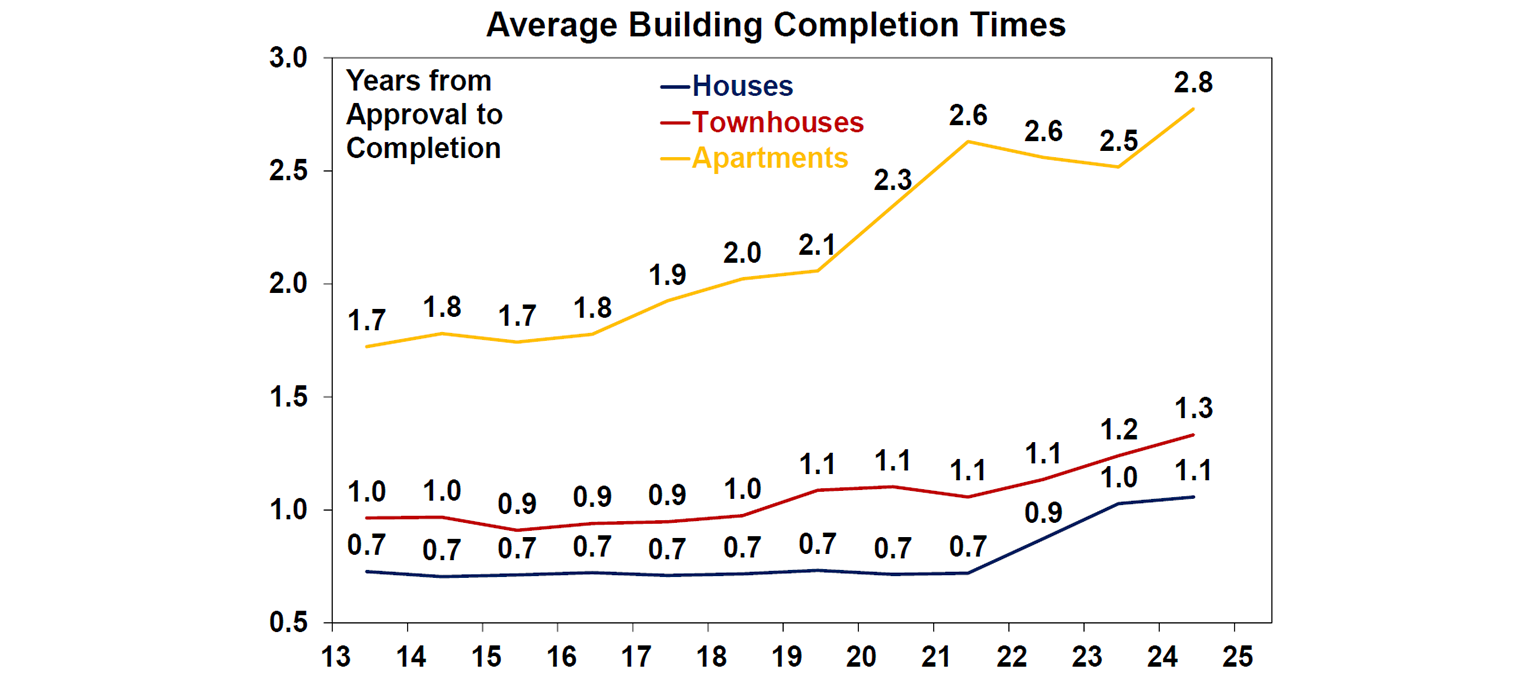

Some argue that over the long-term these schemes can put downward pressure on rents and home prices because lenders mortgage insurance is a significant cost to first time buyers (according to HIA it was $25,000 in 2025) which keeps households renting for longer to save for the cost of buying a home and pushes up rents. In the long-term we could see more supply come on the market from higher first-home buyer demand, but given that we are already in a supply-constrained environment where we are missing our annual construction targets by at least 60K, and productivity in housing is low with the time taken to build a home increasing by around 60% just in the last 10 years, more supply is proving hard to achieve. The government expects that 70,000 people will access the Home Guarantee scheme, which is around 60% of annual first home buyers.

Major global economic events and implications

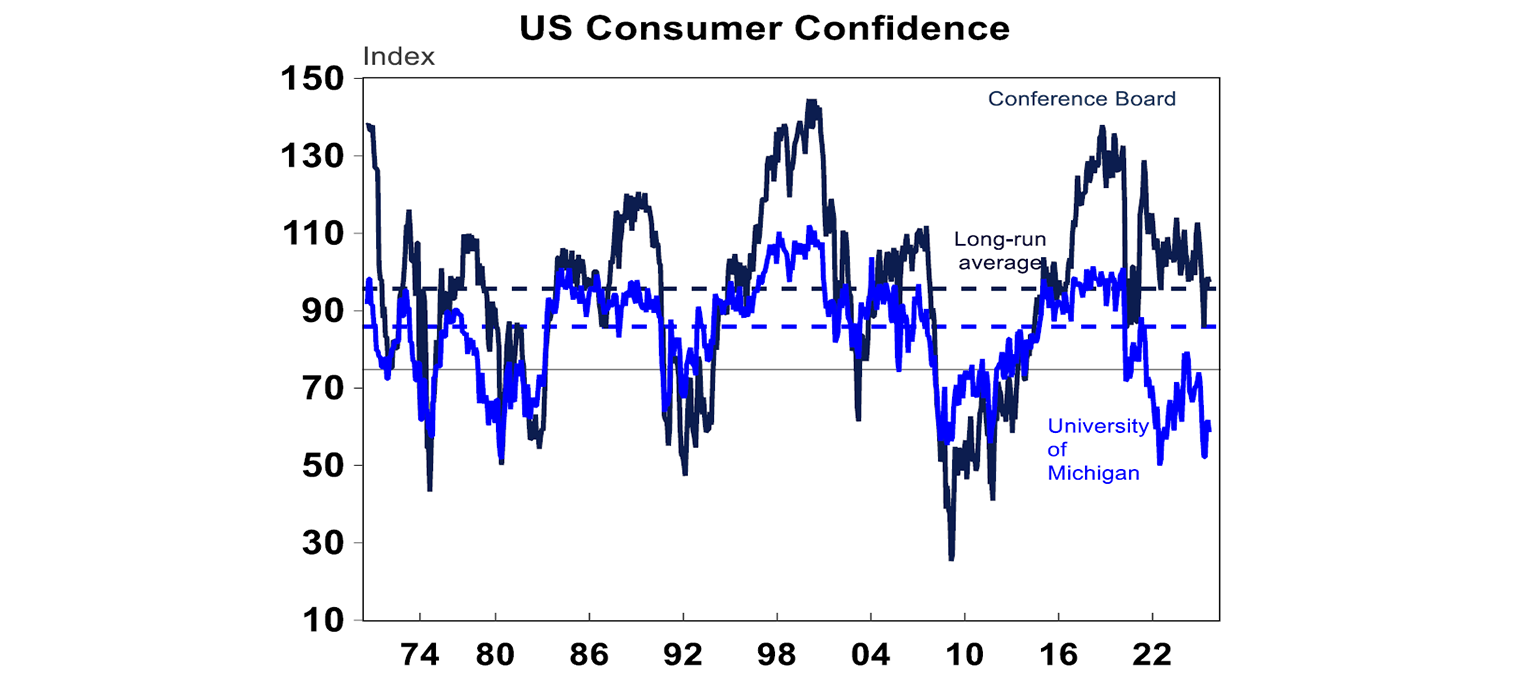

US economic data was overall positive this week. US consumer conference board dipped a little, but is still running around historical averages despite all the political chaos of this year (see the chart below).

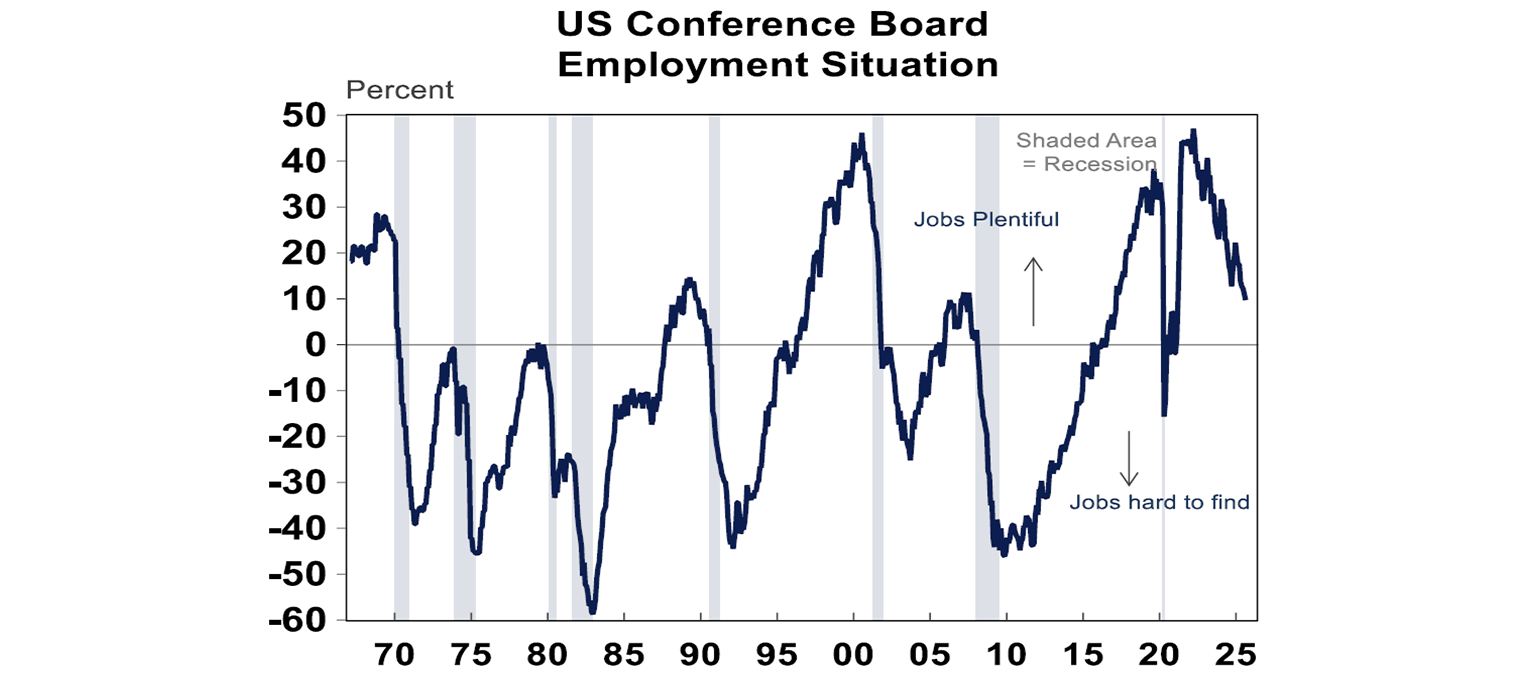

Consumers are reporting that job availability is deteriorating, which would be weighing on confidence but overall there are still reports that there are plentiful jobs (see the chart below).

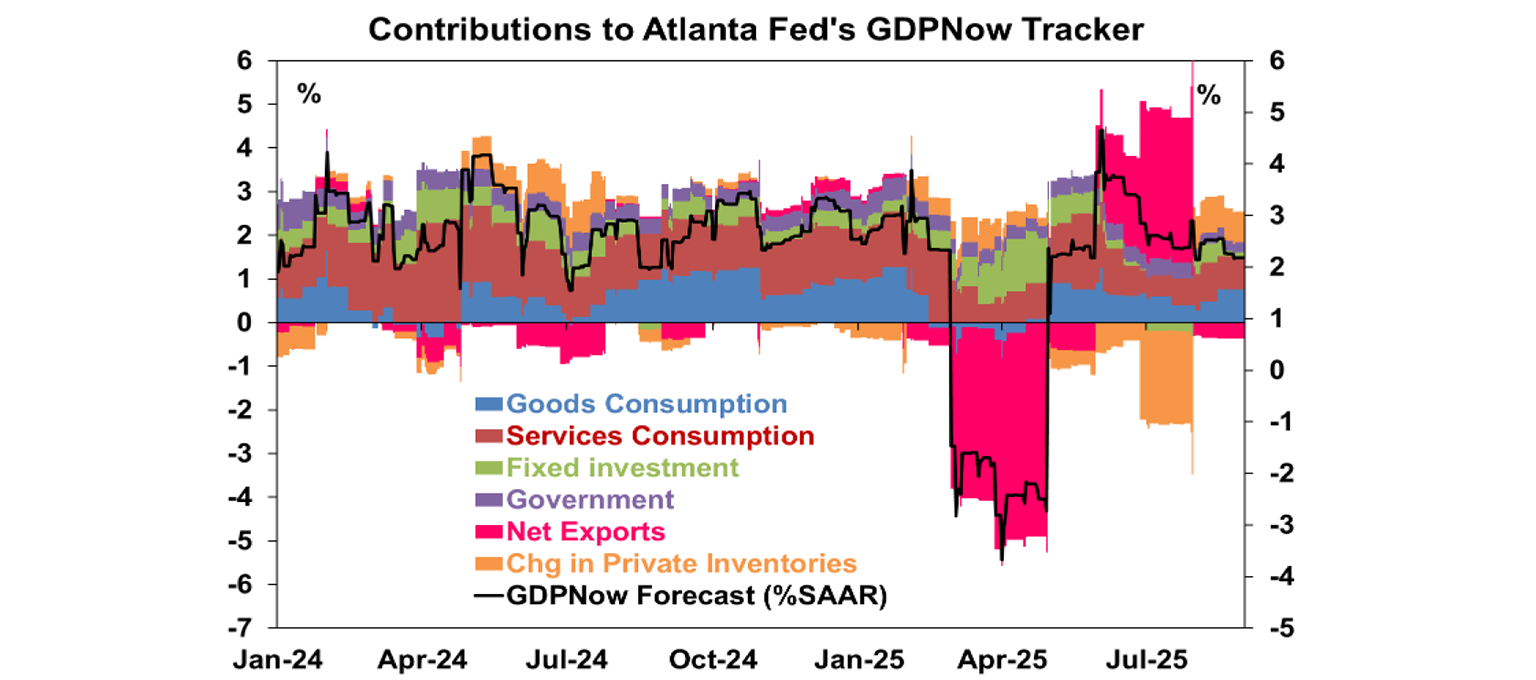

The second estimate of June quarter US GDP was revised up again, to 3.3% (from 3.0% previously). While this reverses the weakness in March quarter (GDP fell by 0.5%) growth as imports increased (another sign that the US economy is still holding up. Third quarter GDP estimates are running at over 2% annualised.

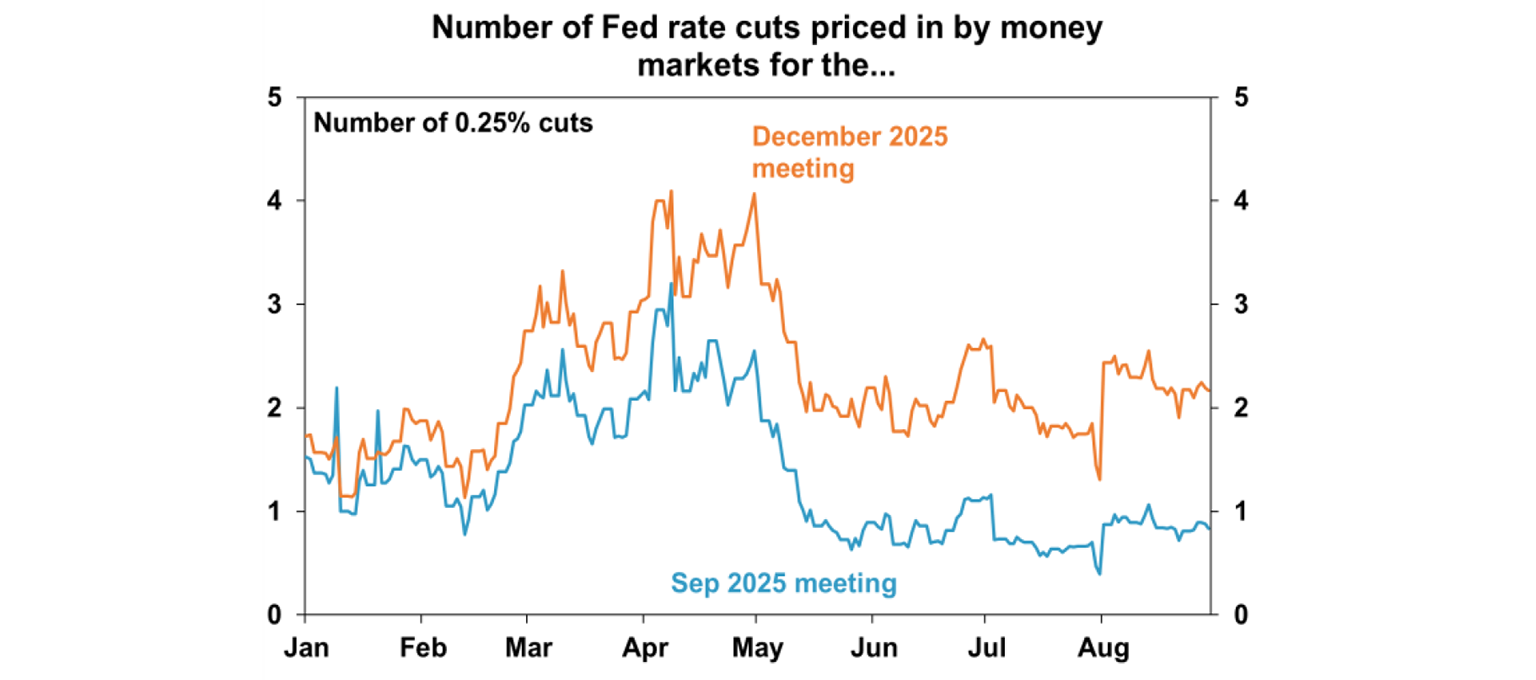

Despite signs that the US economy is holding up, investors are still pricing in an 84% chance of a rate cut in September, and around another 4 after that time, with rates bottoming at 3% by late 2026.

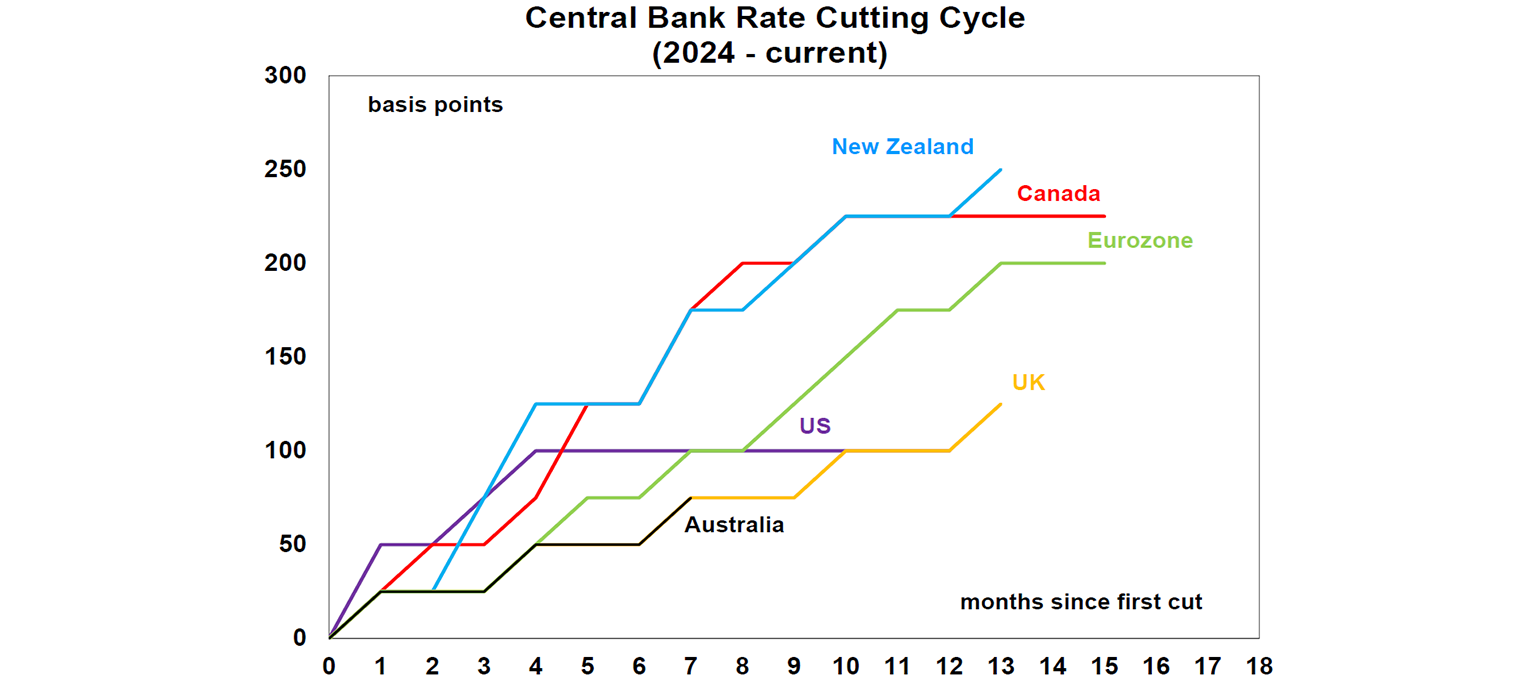

The meeting minutes from the European Central Bank’s July meeting showed that the Governing Council agreed on a wait-and-see approach, postponing any decision to September. There is no pressure on the ECB to change rates right now. The ECB has already cut by 200 basis points, with interest rates there at 2%.

Australian economic events and implications

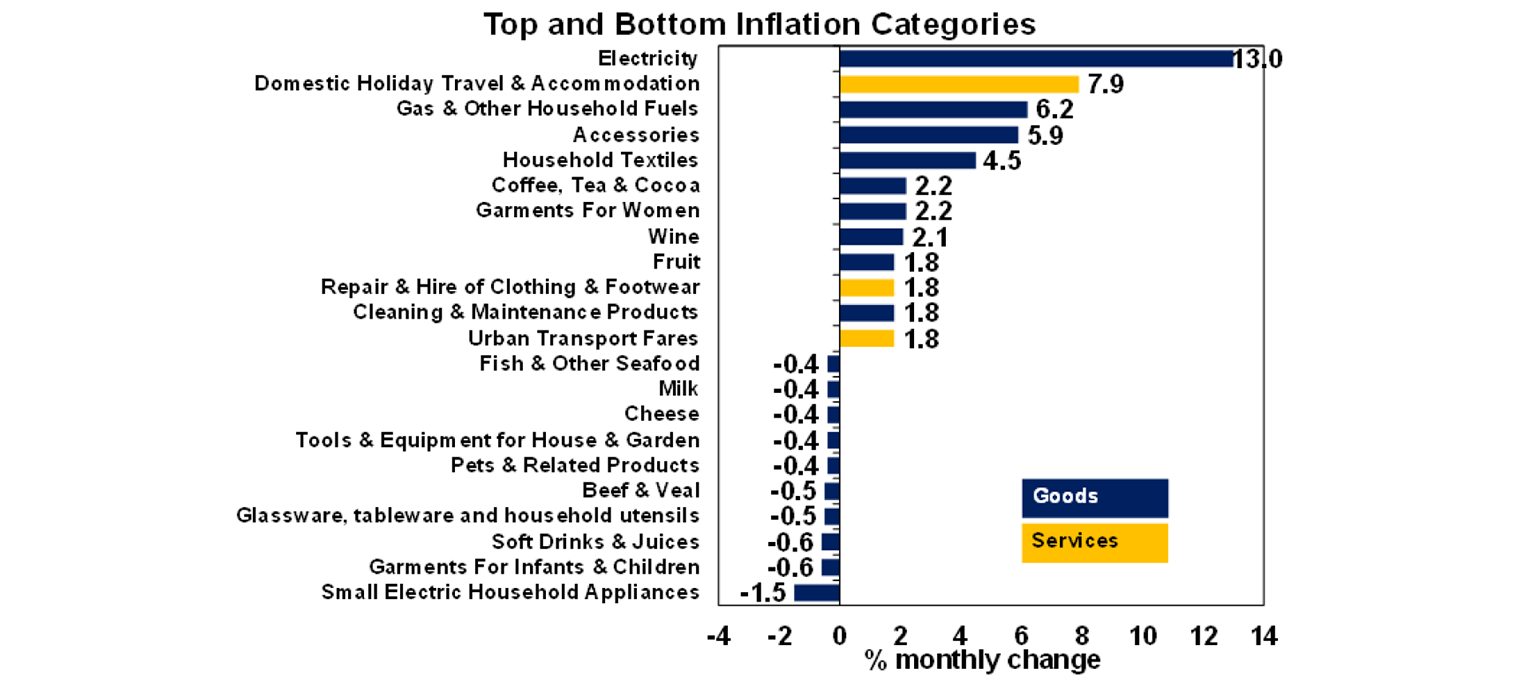

The July monthly consumer price indicator was stronger than expected, up by 2.8% over the year (expectations were for a 2.3% rise). This follows a downside surprise last month and we know that the monthly indicator has measurement issues which can make it volatile. The upside surprise came from a stronger lift in electricity prices which is being influenced by when government rebates hit consumer bank accounts, stronger domestic holiday travel prices (because of school holidays - can we get some sort of national agreement to have school holidays at different times!?), so some of these one-offs will be unwound next month. Some parts of consumer durables were a bit hotter than expected like garments but these were still only up 1.2% over the year and could just be “payback” after sales periods, accessories are elevated, up 6.9% over the year, postal services also jumped up but are still only up by 3.3% over the year and new dwelling construction costs have been a bit stronger in recent months after a lot of discounts have now passed through. Some of these upside inflation risks warrant keeping an eye on.

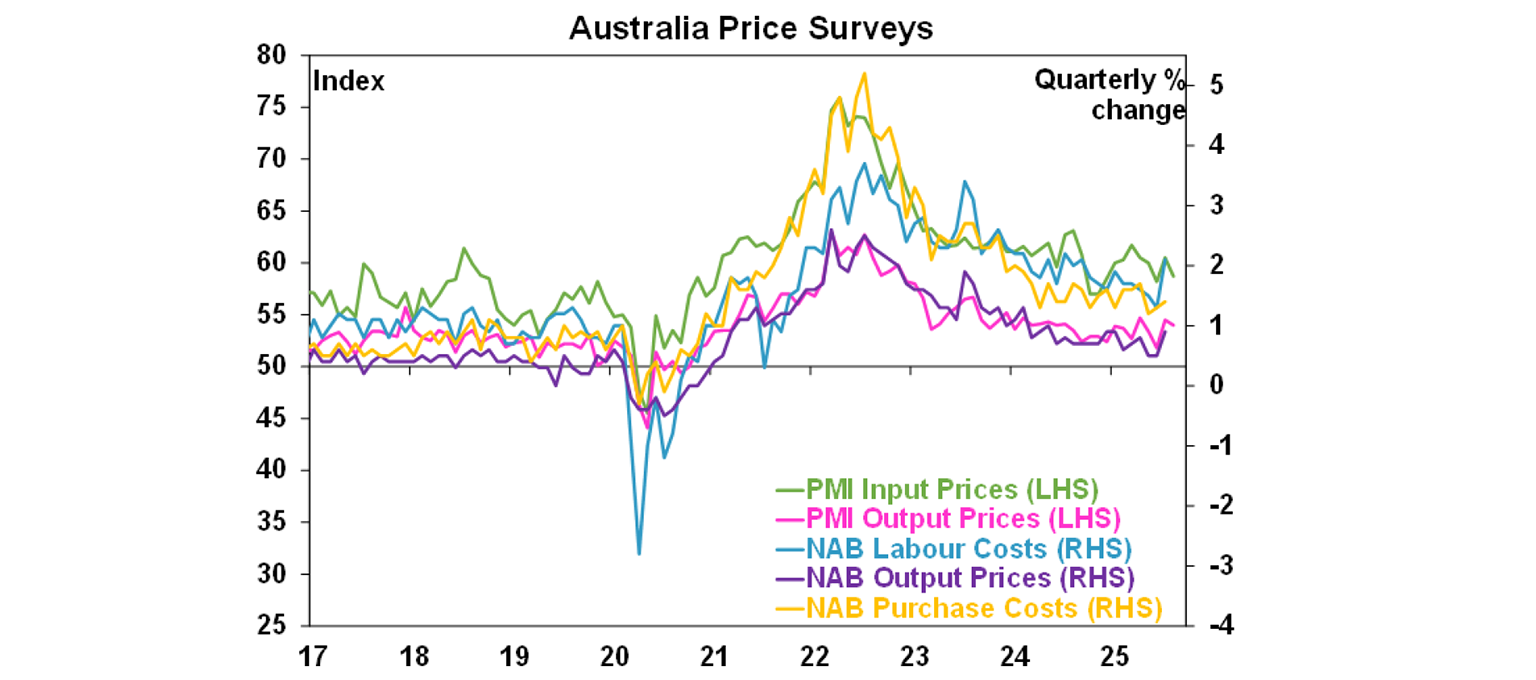

But at the same time, a rising unemployment rate and subsequent softer wages growth will keep a lid on services inflation. As well, price surveys from the PMI’s and NAB are still moving in the right direction (see the chart below), so we do not think we are going to see a significant rebound in inflation from here.

The July inflation update does mean upside risks to our September quarter trimmed mean inflation forecast (of 2.6% over the year), but given the volatility in the monthly read, we are cautious about placing too much emphasis on it. For the RBA, they meet again in September and get another reading on the monthly inflation figures before then. We see the central bank on hold in September, as there is no urgent need to cut rates right now, as the rise in the unemployment rate has been gradual and growth is sideways to up (rather than down!). We still see another 25 basis point cut in the November, February 2026 and May 2026 meetings, which would leave the cash rate at 2.85% by the end of this cycle.

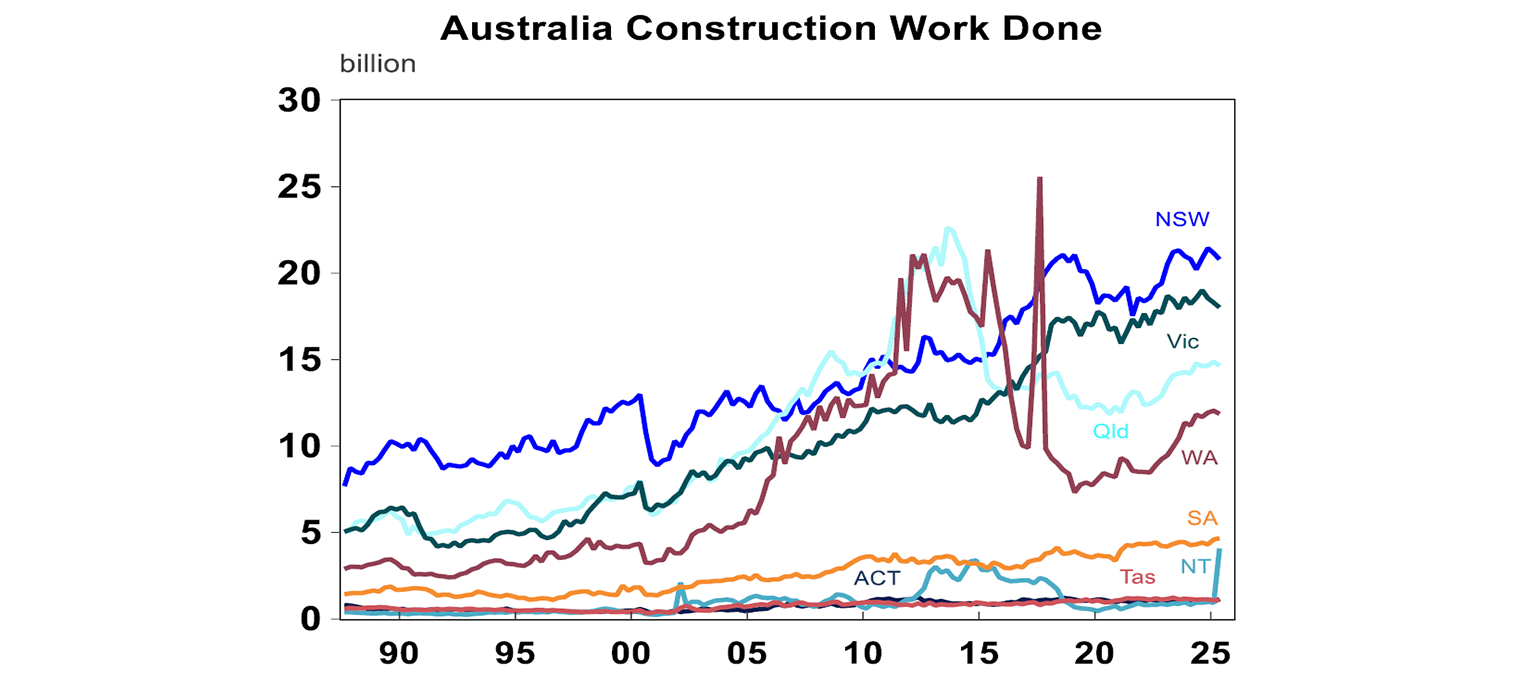

The June quarter construction work done showed a strong 3% increase over the quarter. But there was a 345% increase in Northern Territory which was probably related to imported LNG facilities that have historically also led to spikes in NT construction (see the chart below) as a lot of the increase was a once-off.

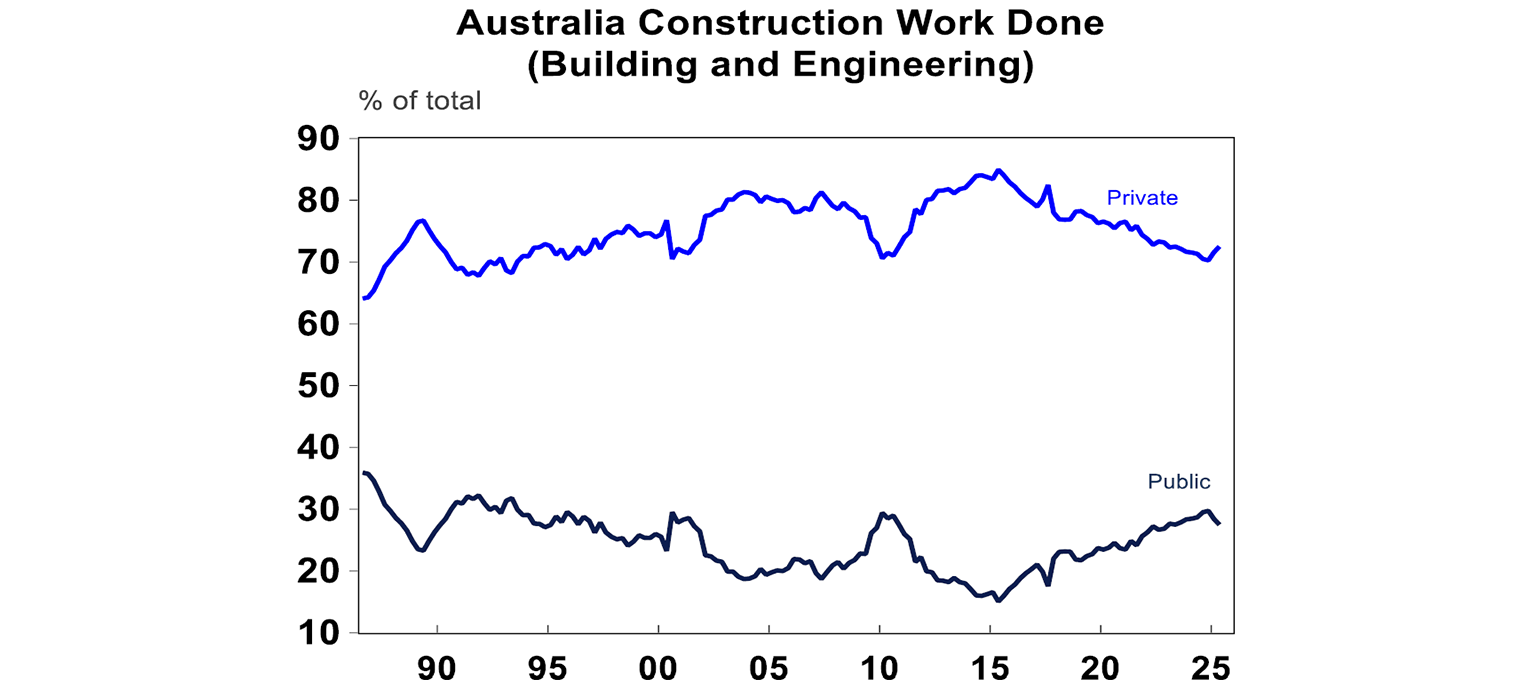

There is an expectation of a transition of investment from the public sector to the private sector. Private investment looks to have bottomed, but given that private construction has been slowing since 2015 and public has been increasing (see the chart below), it will take a while for private construction to make a decent contribution to growth.

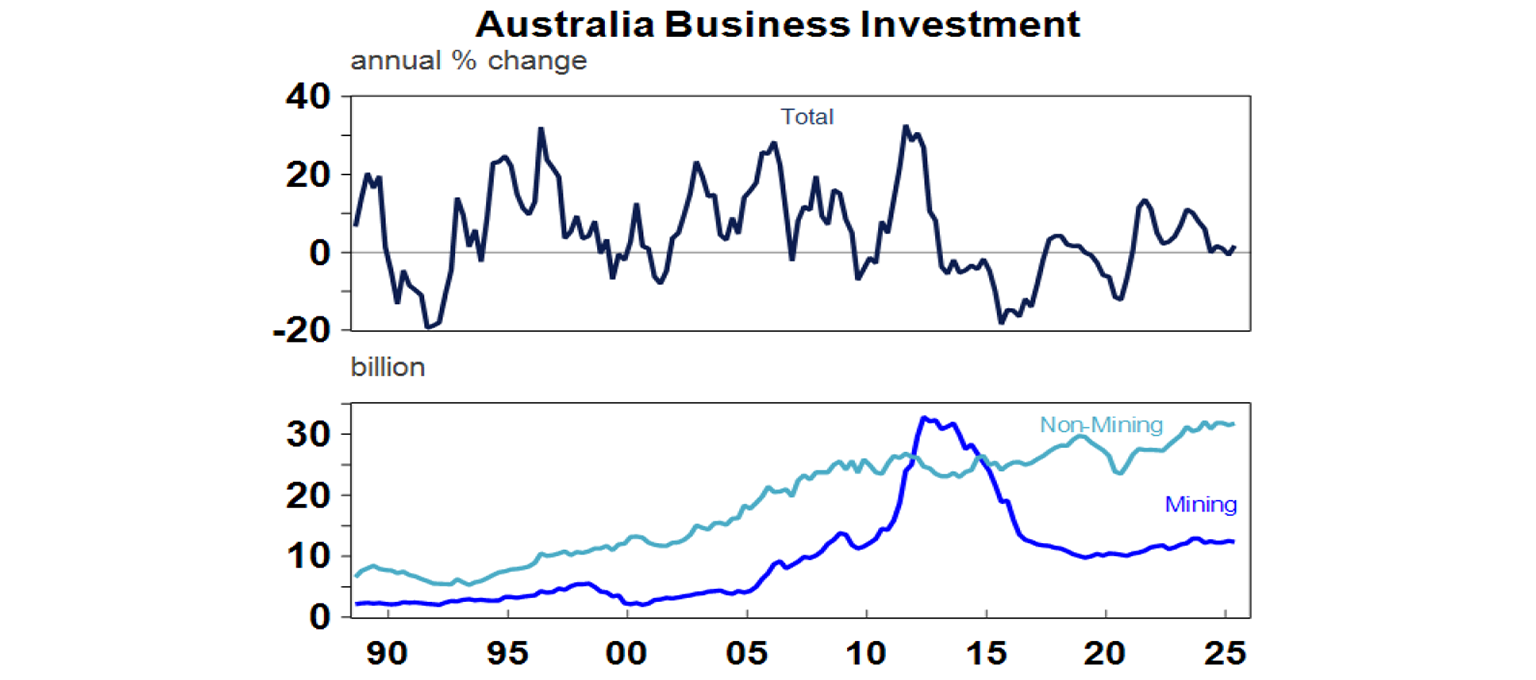

The June quarter capital expenditure figures showed a disappointing June quarter result with a fall in mining capital spending but the forward-looking expectations were better and business investment growth should be in the low single digits. A faster pace of growth would be welcome, especially for productivity and would help to offset a slowing public sector.

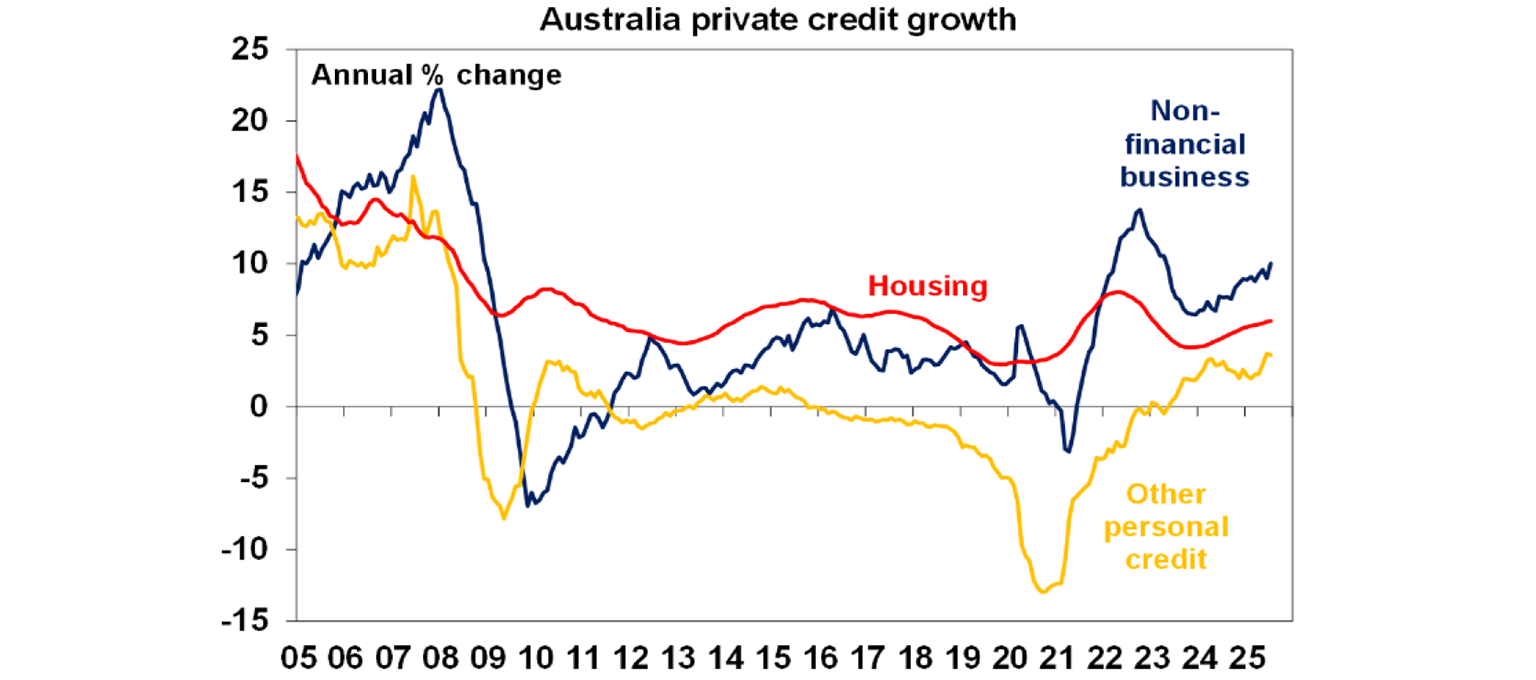

The July credit data rose by 0.7% and 7.2% over the year, helped along by housing (up 6% over the year), particularly for investors and business credit which is up 10% over the year.

The RBA Board minutes for the August meeting were uneventful, given the release of the Statement on Monetary Policy and the press conference that followed this meeting. Just a reminder that it was in this meeting that the RBA decided to cut the cash rate by 25 basis points, to 3.6%. The most notable differences between the minutes in August versus the last meeting in July was that 1) it was a unanimous decision to cut the cash rate (compared to a 6-3 vote to keep rates steady last meeting) 2) some further reduction in the cash rate was likely over the next year 3) the pace of reductions will depend on the data flow, with a lot of emphasis on the importance of the labour market and 4) The RBA’s bond holdings will be run down as they mature i.e. there was no discussion of quantitative tightening. Overall, the tone of the minutes was dovish and not too dissimilar to commentary from the central bank after its August meeting.

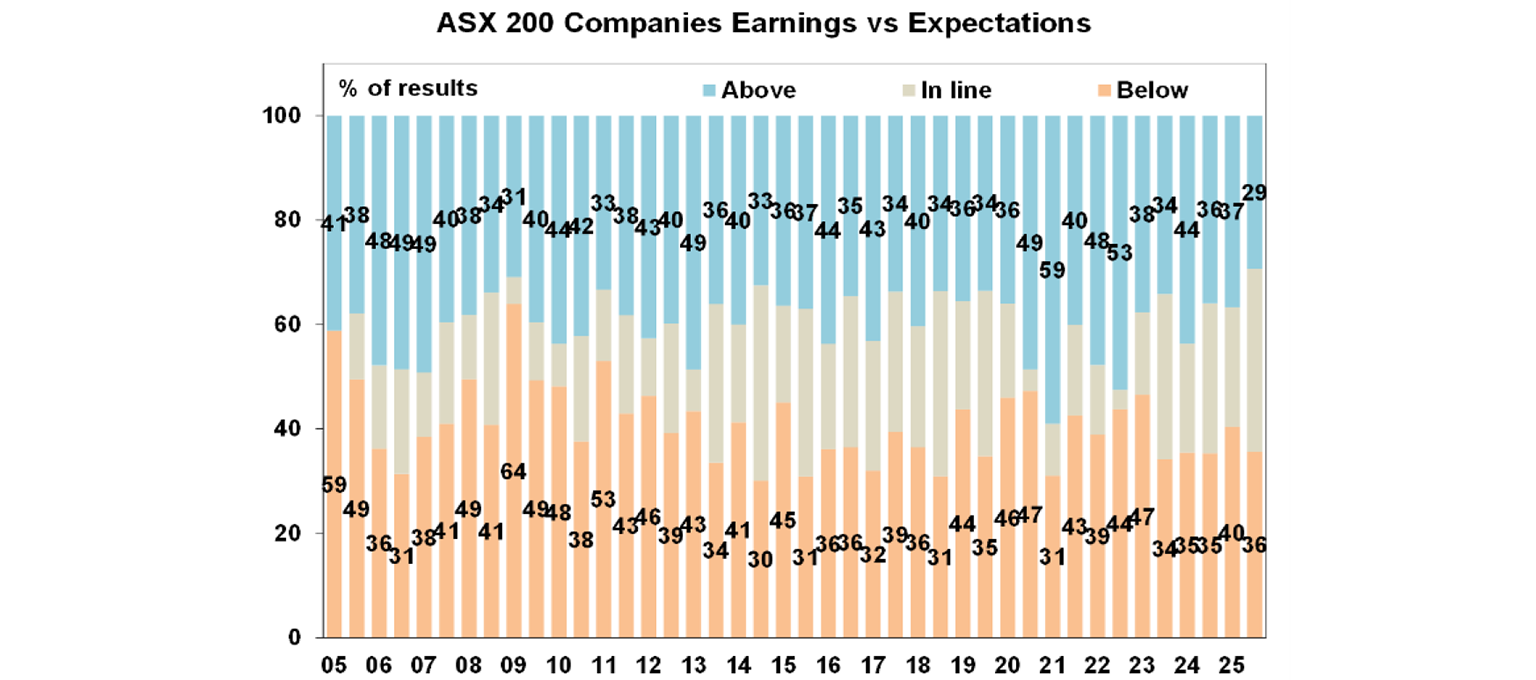

Australian corporate half-year profit results to August are nearly done with 95% of companies having reported results. It has been a fairly good earnings season, with 29% of companies beating expectations, 36% of companies missed expectations and 35% were in line (which is above the historical average).

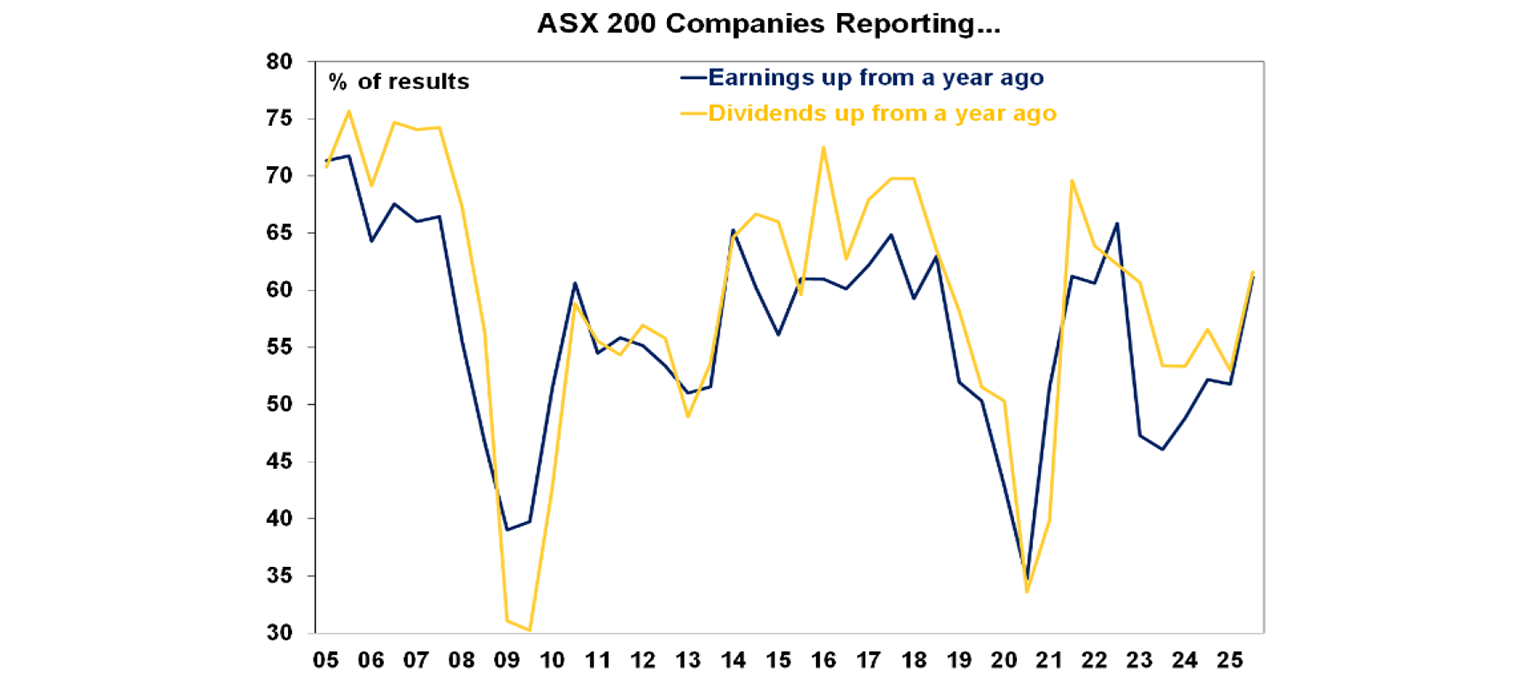

61% of companies had earnings above where they were a year ago and 62% had dividends higher than a year ago.

The Australian sharemarket performed strongly over reporting season, particularly in consumer discretionary. According to UBS, companies with US exposure like Amcor, Bluescope and James Hardie all had downbeat assessments on US businesses. Tech-related businesses like REA group, Car Group and Seek all had solid earnings growth.

What to watch over the next week?

In Australia, economists will be mulling over the June quarter GDP data and its components. On Monday, there is the company profits data (we expect a rise of 2.5%) and inventories (on our forecast there was a smaller build up in inventories compared to last quarter which will drag on June quarter GDP growth). Tuesday’s balance of payments data are expected to show a current account deficit of 2.6% of GDP and net exports making a slight detraction from June quarter GDP. We expect that GDP over the June quarter rose by 0.6% or 1.7% over the year, an improvement from 1.3% last month.

There is also a whole raft of monthly data including Cotality home prices (another solid monthly rise of 0.7% is expected), the TD/Melbourne Institute inflation gauge will give some reading on August inflation, July building approvals (expected to fall after a very large increase last month) July household spending (expected to show a more moderate rise of 0.4%) and the July trade data (a trade surplus of $5.5bn is expected).

The US personal consumption expenditure deflator (the Fed’s preferred measure of inflation is released tonight and is expected to be up 2.9% on the core readings, a touch above last month. Personal income growth is likely to hold up, up by 0.4% over July and spending should also be good at +0.5%. Next Tuesday, the August ISM manufacturing survey will hopefully show a lift above the poor reading of 48 for July (which means contracting activity) and the services ISM reading is also released. The US Fed Beige Book on Wednesday gives an update to regional performance. The job openings, hires and quits survey (Wednesday) and the ADP employment figures are all a prelude to Fridays non-farm payrolls which are expected to show another moderate month of jobs growth ~80K (which is stronger than last month). While demand for labour has slowed, labour supply has also been negatively impacted by lower immigration which means that monthly jobs growth will moderate.

The Chinese August manufacturing PMI is expected to be slightly negative at 49.4 (unchanged on last month) with services better at 50.3.Eurozone July unemployment rate figures on Monday are likely to be just over 6%, August CPI (on Tuesday) is expected to be up by 2.1% over the year which will be taken positively by the ECB.

Eurozone July unemployment rate figures on Monday are likely to be just over 6%, August CPI (on Tuesday) is expected to be up by 2.1% over the year which will be taken positively by the ECB.

Outlook for investment markets

Despite the strong rally in August (which is a seasonally weak month for shares), share markets are still at risk of a correction through the September given stretched valuations and risks around US tariffs and US debt and likely weaker growth and profits. But with Trump pivoting towards more market friendly policies and central banks, including the Fed and RBA, likely to cut rates further, shares are likely to provide reasonable gains into year end.

Bonds are likely to provide returns around running yield or a bit more, as growth slows, and central banks cut rates.

Unlisted commercial property returns are likely to improve as office prices have already had sharp falls in response to the lagged impact of high bond yields and working from home.

Australian home prices have started an upswing on the back of lower interest rates. But it’s likely to be modest initially with poor affordability and only gradual rate cuts constraining buyers. We see home prices rising around 6% this year.

Cash and bank deposits are expected to provide returns of around 3.75%, but they are likely to slow as the cash rate falls.

The $A is likely to be buffeted in the near term between the negative global impact of US tariffs and the potential positive of a further fall in the overvalued US dollar. Undervaluation should support it on a medium-term view with fair value around $US0.73.

You may also like

-

Oliver's insights Economics of happiness 28 July 2026 . The basic “economic problem” which economics is focussed on solving is: how to maximise utility or satisfaction when human wants are unlimited but resources available to satisfy those wants are limited. Of course, utility is basically happiness, so economics is all about happiness. -

Weekly market update - 24-07-2026 Renewed global worries weighed on the Australian share market which fell around 0.3%, but with its lower exposure to tech shares providing some protection. -

Oliver's insights Charts to watch 21 July 2026 Share markets had a strong first half despite the oil supply shock as expectations for de-escalation, okay economic data, strong profits and the AI boom provided an offset.

Important information

Any advice and information is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature. It hasn’t taken your financial or personal circumstances into account. Taxation issues are complex. You should seek professional advice before deciding to act on any information in this article.

It’s important to consider your particular circumstances and read the relevant Product Disclosure Statement, Target Market Determination or Terms and Conditions, available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you. The super coaching session is a super health check and is provided by AWM Services and is general advice only. It does not consider your personal circumstances.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you. You can also ask us for a hardcopy. All information on this website is subject to change without notice. AWM Services is part of the AMP group.