Guide to your preservation age

Preservation age is the earliest age you can generally access your super, provided you meet a condition of release. Understanding how preservation age works can help you plan when and how you use your retirement savings.

5 min read

Key takeaways

- Preservation age is 60 for everyone.

- Reaching preservation age does not mean you have to retire.

- You can access some or all of your super once you reach preservation age and meet a condition of release.

- Preservation age is different from the Age Pension age, which is currently 67 (subject to income and assets tests).

- How and when you access your super can affect tax and Centrelink payments.

What is preservation age?

Your preservation age is the earliest age you can generally access your superannuation savings, as long as you meet a condition of release (a legal reason that allows super to be paid to you).

Preservation age used to depend on your date of birth, but this transition has now finished. Preservation age is 60 for everyone, as anyone with an earlier preservation age has already reached it.

Preservation age is different from the Age Pension eligibility age, which is currently 67 and subject to income and assets tests.

Do I have to retire when I reach preservation age?

No. Your preservation age doesn’t need to be the age you retire unless you want it to be. If you’re willing and able, it’s possible to carry on working beyond age 60 and keep building your super. This can be by making personal deductible contributions, or if you are an employee, this can also be achieved through employer contributions (using the Super Guarantee rate, if eligible), or salary sacrifice contributions.

Reaching preservation age simply gives you more options for accessing your super; it does not force you to stop working.

What can I do once I reach preservation age?

If you’ve reached preservation age and meet a condition of release, you can access your super. Some options have restrictions on the amount of super you can access. Here are some common options:

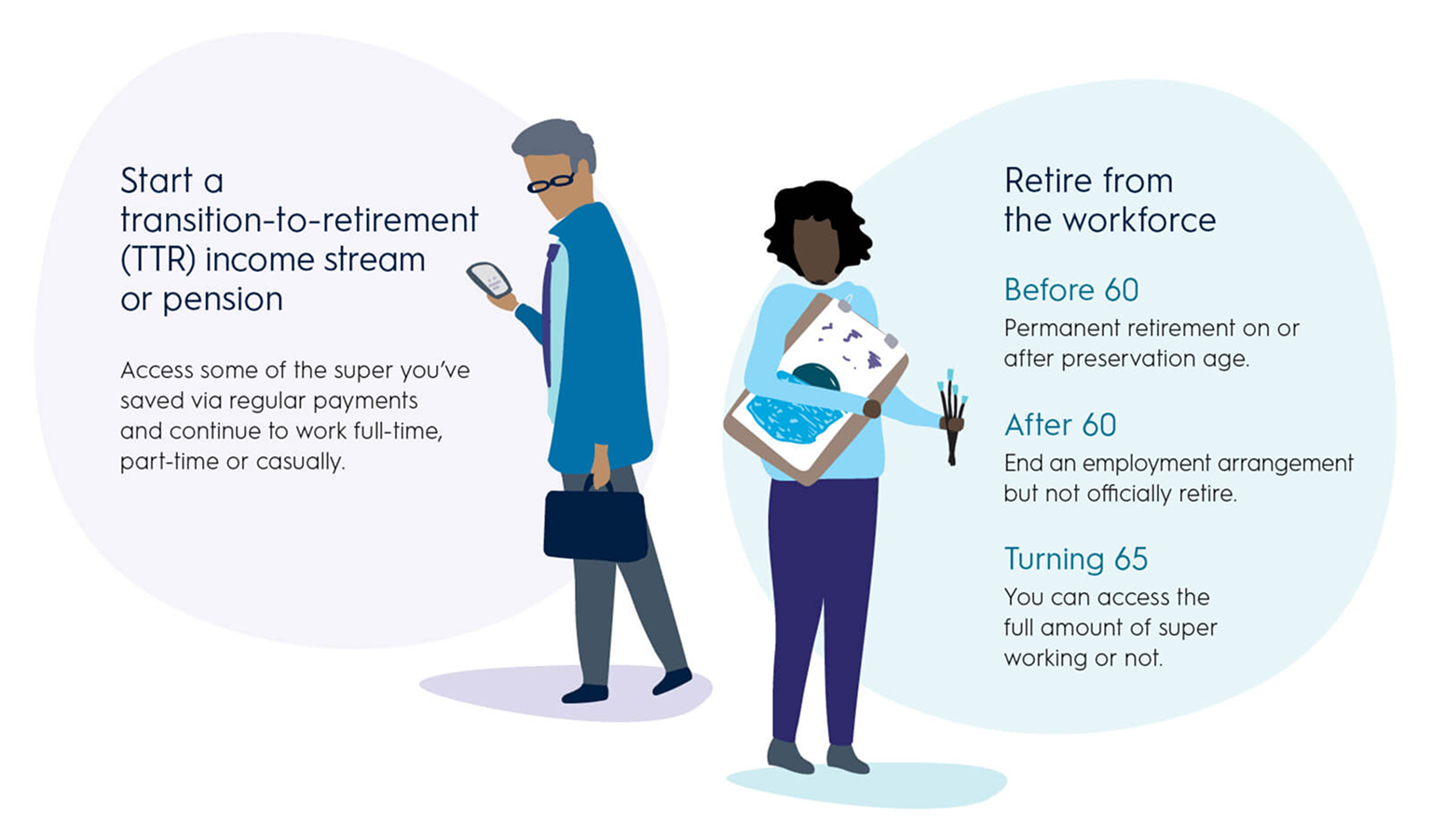

1. Starting a transition-to-retirement (TTR) income stream or pension

Under this condition you can access some of the super you’ve saved via regular payments once you reach your preservation age, while continuing to work full-time, part-time or casually.

2. Retiring from the workforce

Once you’ve met a retirement condition of release, there are no restrictions and you can access the full amount of your superannuation savings. The definition of retirement can be different depending on your age:

If you retire before age 60: If you retire before turning 60, access to your super is more restricted. You’ll generally need to permanently retire and make a declaration that you do not intend to return to gainful employment.

If you stop working after age 60: From age 60, you can leave your job (but not officially retire), and don’t have to make any declaration about your future employment intentions. You can access your super and, if you wish to at some point, return to work. However, any earnings or contributions accrued after you leave your job can’t be accessed until a fresh condition of release is met.

If you turn 65: Whether you’re still working or not, once you’ve reached 65, you can access the full amount of your super.

There are also some specific circumstances not related to retirement, such as financial hardship, where the law allows early access to your super, even if you haven’t reached preservation age.

What’s the best way to access my super?

This will depend on your circumstances, the kind of lifestyle you want and how long you’d ideally like your savings to last.

Drawing on your superannuation in the form of a pension is a common option. A pension is a series of regular payments made as a super income stream. There are different types of pensions to suit your needs and circumstances such as transition to retirement pensions or account-based pensions (also known as allocated pensions).

You can also choose to receive your super via an annuity, or as a lump sum. Find out more about the different types of retirement and superannuation pensions.

An account-based pension or annuity is a retirement income stream that pays out your super savings but will stop once your super savings are depleted, or if you convert your income stream to a lump sum.

It’s worth considering how withdrawing super can affect your tax, and any Centrelink payments (including the Age Pension).

Remember, your super is entirely separate to the Age Pension. Depending on your financial situation, you may be entitled to a full or part Age Pension from the government, or nothing at all.

Where can I get more help?

Taking the time to research your options and plan ahead can help you make the most of your retirement savings. A financial adviser can help you understand what’s right for your situation and next steps.

If you're an AMP Super member, you can access Digital Financial Advice at no extra cost, and speak to an expert financial adviser to talk about your specific needs.

You may also like

-

Understanding retirement income options Not sure how to turn your super into income? This guide explains your options – from flexible income streams to income for life – and how they work. -

Retirement income in Australia: how it works and where it comes from Where does retirement income actually come from? This article explains how super, the Government Age Pension and savings work together in Australia. -

Feeling unsure about retirement? Here’s where to start Not sure where to start with retirement? This guide breaks down where your income could come from and how it all fits together.

Important Information

Products in the AMP Super Fund and the Wealth Personal Superannuation and Pension Fund are issued by N. M. Superannuation Proprietary Limited ABN 31 008 428 322 (NM Super), who is part of the AMP group.

AMP Super refers to SignatureSuper® which is issued by NM Super and is part of the AMP Super Fund (the Fund) ABN 78 421 957 449. ® SignatureSuper is a registered trademark of AMP Limited ABN 49 079 354 519.

Any advice and information is general in nature. It hasn’t taken your financial or personal circumstances into account. You should seek professional advice before deciding to act on any information in this article. It’s important to consider your particular circumstances and read the product disclosure statement (PDS) and Target Market Determination (TMD) for AMP Super (SignatureSuper), available from AMP at amp.com.au, or by calling 131 267, before deciding what’s right for you.

You can read our Financial Services Guide https://www.amp.com.au/financial-services-guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services it provides. You can also ask us for a hard copy. All information on this website is subject to change without notice.

The AMP Lifetime Pension is not currently available but is expected to be available in 2026. The issuer of AMP Lifetime Pension is NM Super. The TMD and PDS for AMP Lifetime Pension is expected to be available in mid-2026 on www.amp.com.au/resources#pds. Please review the PDS before deciding to acquire or hold the Lifetime Pension as there may be features or conditions of the Lifetime Pension that may not be suitable to you. NM Super may withdraw or change the Lifetime pension in the future and therefore these benefits may not apply.