Super

Get super close

to your super

With digital tools and simple advice, get super close to your super with AMP.

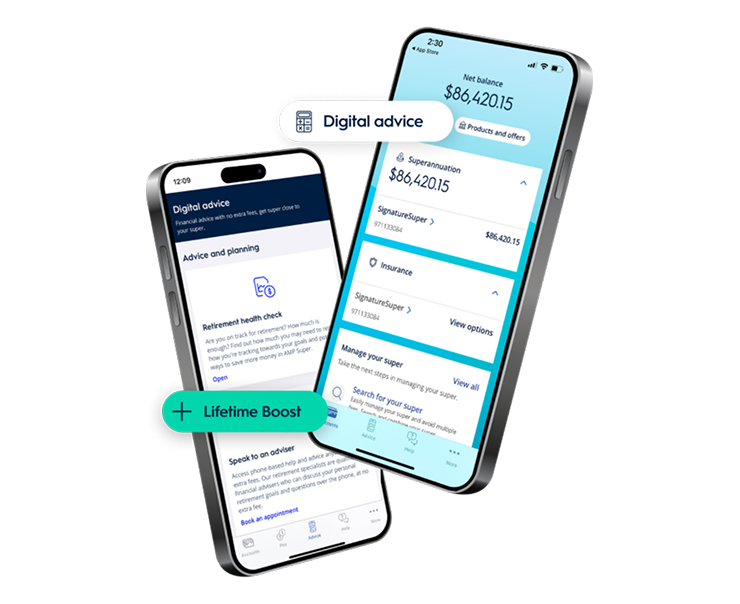

Manage your account anytime, anywhere with My AMP

The AMP Bank app is now available on your mobile

Or login to

Head to your app store to:

* This information is illustrative only and does not replace financial advice. It illustrates potential benefits for a typical AMP Super member with the AMP Super Lifetime feature activated for 20 years leading up to retirement and allocate 50/50 between an AMP Lifetime Pension and an AMP Allocated Pension. A typical AMP Super member is a 47-year-old single male, $90K super balance, $100K salary, contributes 12% with no career breaks, retires at 67 with $120K in other assets at retirement, homeowner and withdraws the minimum from the allocated pension. It assumes annual investment returns of 6.11%, wage inflation of 3% p.a.. Figures shown in today's dollars and adjusted for 3% annual inflation.

As an AMP Super member, you get access to a range of features to help grow your super, with no extra fees to pay.

Find out which approach to investing could be right for you. The Investment Risk Profiler uses four simple questions to help work out what investment style may suit you.

Play with different scenarios to understand the retirement lifestyle you want. Or use the simulator to find out how much you could spend in retirement and how long your money may last.

Check your balance, switch investment options and manage your insurance all in real time in one place with My AMP and the My AMP app.

Speak to a super coach - they’ll help you to understand your current balance, contributions, investments and insurance, and answer general super questions.

Have a question about your AMP Super? Connect with a qualified super financial adviser to get personalised advice on five super topics including investment options and insurance.

Approaching retirement? Our retirement specialists are qualified financial advisers who can discuss your personal retirement goals and questions.

AMP Super member? Your returns are looking good.

Returns might vary depending on investment options. If you’re an AMP Super member, log in to My AMP to see how your super’s tracking.

Join in minutes

Learn how to take control of your super and feel more confident and informed when making decisions about your financial future.

All your member info - product disclosure statements, fund details, forms and docs.

Advice. Tools. Webinars. Articles. Everything you need to get super close to your super.

Start planning for tomorrow today and find out how an AMP pension can help you enjoy your retirement.

AMP Super has been recognised and awarded by the industry for many years. And we’re proud to add more awards to our long list.

Tools & calculators

Member information

Let's get started

AMP Super refers to SignatureSuper® which is issued by N.M. Superannuation Proprietary Limited ABN 31 008 428 322 AFSL 234654 (NM Super) and is part of the AMP Super Fund (the Fund) ABN 78 421 957 449. NM Super is the trustee of the Fund.

® SignatureSuper is a registered trademark of AMP Limited ABN 49 079 354 519.

Before deciding what’s right for you, it’s important to consider your particular circumstances and read the relevant Product Disclosure Statement and Target Market Determination from AMP at amp.com.au or by calling 131 267.

Read AMP’s Financial Services Guide for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services provided to you.

Any advice and information provided is general in nature, hasn’t taken your circumstances into account, and is provided by AWM Services Pty Ltd (AWM Services) ABN 15 139 353 496 AFSL 366121, which is part of the AMP group (AMP). All information on this website is subject to change without notice.

The super coach session is a super health check and is provided by AWM Services. It is general advice conversation only. It does not consider your personal circumstances.

Digital Financial Advice is provided by AWM Services to eligible members of the AMP Super Fund.

Simple Super (Intrafund) advice is provided by AWM Services Limited (AWM Services) ABN 15 139 353 496, AFS Licence No. 366121 (AWMS) to eligible members of the AMP Super Fund. AWM Services is a wholly-owned subsidiary of AMP. This service may not be offered where it is deemed it is not within the scope of the service or your best interest.

Issued by SuperRatings Pty Ltd (SuperRatings) ABN: 95 100 192 283 a Corporate Authorised Representative (CAR No.1309956) of Lonsec Research Pty Ltd ABN 11 151 658 561, AFSL No. 421445 (Lonsec Research). Ratings are general advice only and have been prepared without taking account of your objectives, financial situation or needs. Consider your personal circumstances, read the product disclosure statement and seek independent financial advice before investing. The rating is not a recommendation to purchase, sell or hold any product. Past performance information is not indicative of future performance. Ratings are subject to change without notice and SuperRatings assumes no obligation to update. SuperRatings use proprietary criteria to determine awards and ratings and may receive a fee for the use of its ratings and awards. Visit superratings.com.au for ratings information. © 2025 SuperRatings. All rights reserved.

Footnotes

1Based on the simple average of total administration and investment fees and costs across all AMP MySuper Lifestages options (Capital Stable, 1950s, 1960s, 1970s, 1980s, 1990s Plus). Compared against the simple average of all super funds’ MySuper options included in the Chant West Super Fund Fee Survey March 2025 at balances of $50,000 to $500,000.

2AMP MySuper 1970s, 1980s, or 1990s Plus investment options delivered an average return of 13.26% for the year to 30 September 2025. AMP MySuper Lifestages investment options are based on your decade of birth and take you through your working life, continuously evolving as you approach retirement. Past performance is not a reliable indicator of future performance. Investment performance is as at 30 September 2025 and is net of investment fees, costs and tax (but excludes administration fees, trustee fees, member fees, amounts paid from the super fund’s assets and member activity fees).

*This information is illustrative only and does not replace financial advice. It illustrates potential benefits for a typical AMP Super member with the AMP Super Lifetime feature activated for 20 years leading up to retirement and allocate 50/50 between an AMP Lifetime Pension and an AMP Allocated Pension. A typical AMP Super member is a 47-year-old single male, $90K super balance, $100K salary, contributes 12% with no career breaks, retires at 67 with $120K in other assets at retirement, homeowner and withdraws the minimum from the allocated pension. It assumes annual investment returns of 6.11%, wage inflation of 3% p.a.. Figures shown in today's dollars and adjusted for 3% annual inflation.