Case studies

How James could boost his retirement income

After decades of working and saving, James is ready to enjoy his retirement years. Like many Australians, he wants his retirement income to feel certain but still needs some flexibility. Find out how James uses a Lifetime Retirement Income which is designed to provide a regular stream for life that doesn’t run out.

6 min read

Meet James

- He’s 67

- He is ready to retire with $350,000 saved in his super

- Needs flexibility to access some of his super for bigger or unexpected purchases from time to time

- Wants more certainty knowing his regular bills are covered by an income that never runs out.

This is a hypothetical example to illustrate how different retirement income streams can be combined. It does not represent a recommendation or take into account personal circumstances.

How James sets up his retirement

He doesn’t put all his super into one product. Rather, he chooses a combined approach to maximise his overall retirement income goals.

James puts $175,000 into an AMP Flexible Retirement Income, also known as an AMP Super Allocated Pension. Provides income payments as well as flexibility for one-off bigger or unexpected purchases.

James puts $175,000 into an AMP Lifetime Retirement Income, also known as an AMP Super Lifetime Pension. Provides certainty his money lasts for a lifetime and won’t run out.

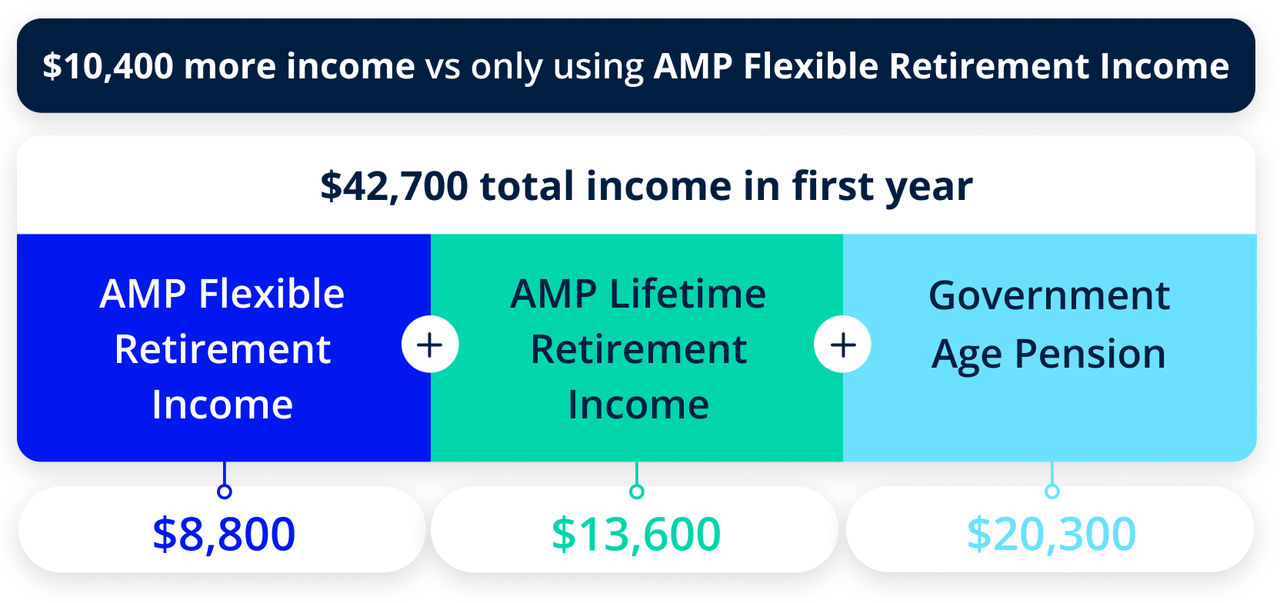

How much could James get in the first year?

James receives $42,700 income in the first year. This is $10,400 more income versus only using AMP Flexible Retirement Income.

James receives around $8,800 by drawing down at the government-set minimum.

He can take more if he needs to either as income up to the maximum or a lump sum but withdrawing extra means his balance may run out sooner.

James receives around $13,600.

The balance was converted into this income stream that will last for the lifetime no matter how long James live. This income amount will vary up or down each year depending on the investment performance of the underlying investments backing this product.

James receives around $20,300.

This figure is boosted because part of James’ super is invested in a Lifetime Retirement Income. This means his super is currently treated more favourably under the Age Pension asset test which can increase entitlement compared to allocated pensions.

The power of the Lifetime combination

By combining a Flexible Retirement Income with a Lifetime Retirement Income, we can see James receives around $10,400 more income in his first year. That’s compared to placing all his super into a Flexible Retirement Income and drawing only the minimum amount.

That extra income comes from:

- Around $5,500 more from the Government Age Pension, and

- About $4,900 more from the Lifetime Retirement Income higher initial income

Over the first 10 years of retirement, this approach could provide around $89,000 more income overall. This assumes the current Age Pension rates, deeming rules, minimum drawdown rates, and investment return assumptions as at June 2025. The actual amount could vary if assumptions change.

Your money is expertly invested in a balanced-style pool to support long-term income adequacy. Payments aren’t based on day-to-day market movements. Instead, we set each year's payment based on a full-year's investment performance, so you have peace of mind knowing your income won’t change during that financial year.

Scenario: 20% market drop (similar to the 2007-2009 Global Financial Crisis)

Even in such once-in-a-generation market crash, James continues to receive income from both sources, including a payment he knows will last for life. The Government Age Pension also provides an added safety net, as lower asset values and income may improve his eligibility under the means test.

While markets may move day to day, income from a Lifetime Retirement Income is only adjusted up or down once a year, in July. The adjustment is based on the pool’s full financial year investment performance — so short‑term market drops may have recovered by the time any adjustment is applied.

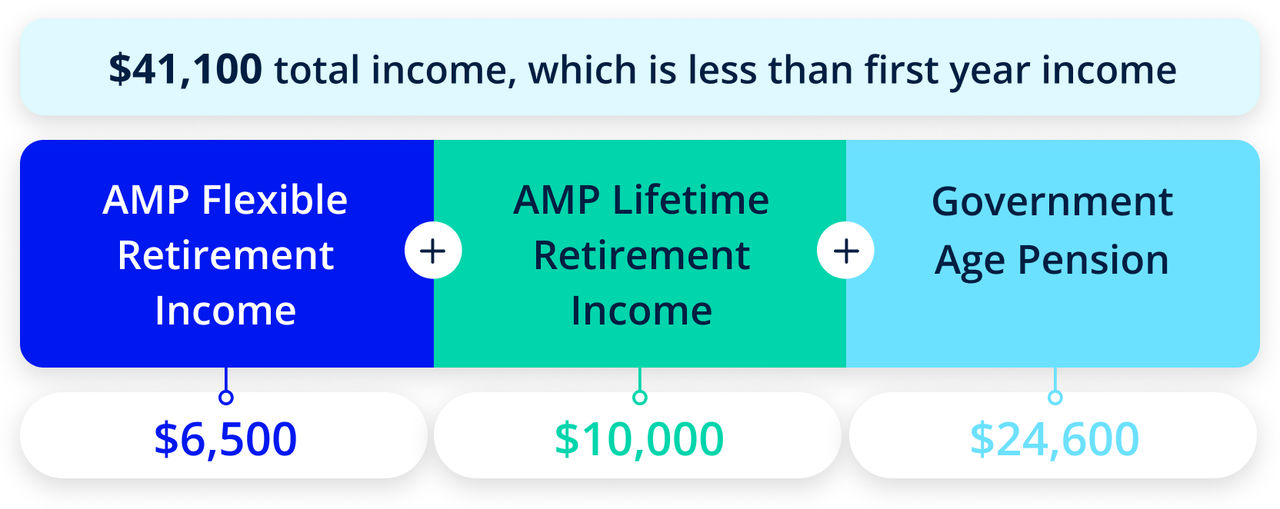

How much could James receive in the year post market crash?

James receives $41,100 income in the year post market crash which is slightly less than the first year income.

Flexible Retirement Income

$175,000 balance after taken out first year income could reduce to $133,000, falling in line with the market.

Income of $8,800 could reduce to around $6,500, about $2,300 less if continues drawing down at the minimum.

Lifetime Retirement Income

No balance to worry about.1

Income of $13,600 could reduce to around $10,000 per year, about $3,600 less.

Government Age Pension

Age Pension entitlement of $20,300 could increase to around $24,600 due to lower assets and income which improves Age Pension eligibility.

Could this work for you?

Everyone’s situation is different. The right mix depends on your super balance, retirement age, income needs, and assets and incomes outside super.

AMP Super members can project how an AMP Super Lifetime Retirement Income could work alongside an AMP Super Flexible Retirement Income using AMP’s Retirement Simulator, Digital Financial Advice or by speaking with an AMP retirement specialist.

Looking for some help or advice?

You don’t have to work this out on your own. If you’re an AMP Super member, you can access guidance and advice designed to help you feel clearer and more confident.

-

Speak to a retirement specialist If you’d like to talk through your retirement options, AMP Super members can access personalised advice through a financial adviser.

-

Digital Financial Advice Digital Financial Advice includes a retirement planner that provides a recommendation on turning super into a retirement income stream.

-

Retirement Simulator See how much you might have in retirement and how long it could last.

What you need to know

AMP Lifetime Retirement Income refers to AMP Super Lifetime Pension and AMP Flexible Retirement Income refers to AMP Super Allocated Pension which is issued by N.M. Superannuation Proprietary Limited ABN 31 008 428 322 AFSL 234654 (NM Super) and is part of the AMP Super Fund (the Fund) ABN 78 421 957 449. NM Super is the trustee of the Fund.

® SignatureSuper is a registered trademark of AMP Limited ABN 49 079 354 519.

1If you would like to fully withdraw from a Lifetime Retirement Income straight after a market crash, some market adjustment may be applied to determine the final exit payment you receive.

These cases are provided for illustration purposes only to help you understand how Flexible and Lifetime Retirement Income works and are not intended to replace financial advice. This information doesn’t represent the benefits that you could receive, and the outcome will depend on your personal circumstances.

Any advice is provided by AWM Services Pty Ltd ABN 15 139 353 496, AFSL No. 366121 (AWM Services) and is general in nature only. It doesn’t consider your personal goals, financial situation or needs. It’s important you consider the appropriateness of any advice and read the relevant product disclosure statement and target market determination available at amp.com.au, before deciding what’s right for you. AWM Services is part of the AMP group and can be contacted on 131 267 or askamp@amp.com.au.

You can read our Financial Services Guide online for information about our services, including the fees and other benefits that AMP companies and their representatives may receive in relation to products and services it provides. You can also ask us for a hard copy.

Digital Financial Advice is provided by AWM Services to eligible members of the AMP Super Fund.

Simple Super (Intrafund) advice is provided by AWM Services Limited (AWM Services) ABN 15 139 353 496 AFSL 366121 (AWMS) to eligible members of the AMP Super Fund. AWM Services is a wholly-owned subsidiary of AMP. This service may not be offered where it is deemed it is not within the scope of the service or your best interest.

The super coach session is a super health check and is provided by AWM Services. It is general advice conversation only. It does not consider your personal circumstances.